Tamper-proof Fasteners Market Outlook (2025 to 2035)

The tamper-proof fasteners market is valued at USD 2.5 billion in 2025. As per Fact.MR's analysis, the market will grow at a CAGR of 6.3% and reach USD 4,750 million by 2035.

The tamper-proof fasteners industry saw steady growth in 2024, driven by increased demand from sectors prioritizing security and durability. Industrial and manufacturing applications dominated purchases, especially in aerospace, defense, and public infrastructure projects.

Fact.MR analysis found that governments across the globe increased their emphasis on the protection of critical infrastructure, and this resulted in increased adoption of security fasteners in smart city projects and public utilities.

The automotive industry also played a big role as producers incorporated specialized fasteners to guard against unauthorized tampering in electric vehicles.

North America was still the greatest contributor, generating some 33% of worldwide revenue. At the same time, the U.S. had particularly high growth as a consequence of regulation-backed requirements to make high-risk plants secure.

Europe was a prominent performer, however, with government-driven uptake somewhat behind that seen in North America. South Asia & Oceania demonstrated moderately expansionist behaviour, mostly down to development activity in India and Australia's building sectors.

Looking ahead to 2025 and beyond, Fact.MR opines that rising cybersecurity concerns in hardware applications will further drive demand in IT infrastructure. Increasing integration in self-service kiosks, energy grids, and medical devices will also contribute to sustained expansion, keeping the industry on a strong trajectory through 2035.

Key Metrics

| Metric | Value |

|---|---|

| Estimated Global Size in 2025 | USD 2.5 billion |

| Projected Global Size in 2035 | USD 4.7 billion |

| CAGR (2025 to 2035) | 6.3% |

Fact.MR Survey Results: Industry Dynamics Based on Stakeholder Perspectives

(Surveyed Q4 2024, n=250 stakeholder participants evenly distributed across manufacturers, distributors, procurement executives, and end-users in North America, Europe, Japan, and South Korea)

Key Priorities of Stakeholders

- Security Enhancement: 78% of stakeholders ranked security against unauthorized access as their top concern.

- Material Durability: 72% emphasized the need for high-durability materials (steel, aluminum) to justify procurement costs.

Regional Variance:

- North America: 66% highlighted the growing demand for tamper-resistant fasteners in IT hardware and cybersecurity applications, far exceeding Japan's 39%.

- Europe: 82% emphasized compliance with evolving security regulations, compared to 57% in the U.S.

- Japan/South Korea: 58% stressed cost-effectiveness due to budget constraints, contrasting with 31% in North America.

Embracing Sophisticated Technologies

High Variance:

- U.S.: 54% of procurement executives reported increased investment in biometric authentication and electronic tracking fasteners.

- Europe: 47% prioritized tamper-resistant coatings and corrosion-resistant finishes, particularly in maritime and aerospace.

- Japan: Only 33% adopted next-generation fasteners, citing cost concerns and preference for robust traditional solutions.

- South Korea: 38% invested in smart security fasteners integrated with IoT for industrial applications.

Convergent and Divergent Perspectives on ROI:

- 69% of U.S. manufacturers saw value in high-security fasteners, compared to only 29% of Japanese firms.

Material Preferences

Consensus:

- Steel: Chosen by 67% globally for its durability and tensile strength, particularly in high-security sectors.

Regional Variance:

- Europe: 55% preferred aluminum-based fasteners due to sustainability mandates.

- North America: 69% relied on high-grade stainless steel for critical security applications.

- Japan/South Korea: 42% opted for hybrid steel-aluminum fasteners to balance cost, durability, and corrosion resistance.

Price Sensitivity

Shared Challenges:

- 86% cited rising raw material prices (steel up 27%, aluminum up 19%) as a significant concern.

Regional Differences:

- North America/Europe: 63% of buyers were willing to pay a 15-20% premium for enhanced security features.

- Japan/South Korea: 41% showed interest in leasing models for high-end security fasteners, compared to only 18% in the U.S.

- South Asia & Oceania: 76% preferred cost-effective solutions under $5,000 per bulk order, with minimal demand for premium offerings.

Pain Points in the Value Chain

Manufacturers:

- U.S.: 58% struggled with labor shortages affecting specialized fastener production.

- Europe: 49% cited complex regulatory requirements delaying product approvals.

- Japan: 63% faced slow demand due to stagnation in industrial sectors.

Distributors:

- U.S.: 72% encountered inventory shortages due to fluctuating steel and aluminum prices.

- Europe: 51% faced pricing pressure from Eastern European low-cost manufacturers.

- Japan/South Korea: 62% struggled with logistics issues in rural and industrial hubs.

End-Users:

- U.S.: 46% reported high maintenance costs as a key issue.

- Europe: 38% cited difficulties in retrofitting older structures with new fastening systems.

- Japan: 57% expressed dissatisfaction with the lack of technical support for complex security fastener installations.

Future Investment Priorities

Alignment:

- 73% of manufacturers planned to invest in R&D for next-generation tamper-resistant fasteners.

Divergent Regional Strategies:

- North America: 60% prioritized advanced anti-theft mechanisms for IT and automotive applications.

- Europe: 56% invested in sustainable production methods, such as green steel.

- Japan/South Korea: 48% focused on compact and lightweight fasteners for electronics and aerospace applications.

Regulatory Impact

North America:

- 67% of stakeholders indicated that stringent cybersecurity and infrastructure protection mandates were driving fastener innovations.

Europe:

- 80% viewed evolving aerospace and defense security standards as a key factor for premium product adoption.

Japan/South Korea:

- Only 34% considered regulatory frameworks a major influence on purchasing decisions, citing weaker enforcement mechanisms.

Conclusion: Variance vs. Consensus

High Consensus:

- Security compliance, material innovation, and cost pressures remain universal concerns across all regions.

Key Variances:

- North America: Leading in cybersecurity-driven tamper-proof fastener innovations.

- Europe: Prioritizing sustainability and compliance with evolving regulations.

- Japan/South Korea: Balancing cost-effectiveness with selective technology adoption.

Strategic Insight:

A “one-size-fits-all” approach will not succeed. Regional adaptation is necessary- steel for North America, aluminum for Europe, and hybrid materials for Japan and South Korea to drive industry penetration.

Impact of Government Regulation

| Country/Region | Key Regulations & Mandatory Certifications |

|---|---|

| United States | The National Institute of Standards and Technology (NIST) and Cybersecurity & Infrastructure Security Agency (CISA) mandate high-security fasteners for critical infrastructure, defense, and IT hardware. Compliance with ITAR (International Traffic in Arms Regulations) is necessary for defense applications. The ASTM F879 standard applies to stainless steel fasteners, while the ISO 9001 certification is widely required for quality management. |

| Canada | The Canadian Centre for Cyber Security (CCCS) sets guidelines for hardware security, influencing demand in telecom and IT applications. The CSA Group provides standards for fasteners used in construction and electrical applications. |

| European Union | The EN 14399 and EN 15048 standards regulate fastener strength and security levels in construction and industrial applications. The EU Cybersecurity Act (2019) has led to increased demand for high-security fasteners in IT infrastructure. Companies must comply with CE marking for product safety and environmental impact regulations under REACH (Registration, Evaluation, Authorisation, and Restriction of Chemicals). |

| United Kingdom | The UKCA (UK Conformity Assessed) Mark has replaced CE certification post-Brexit for fasteners used in industrial and critical security applications. Compliance with BS EN 14399 and ISO 27001 (for cybersecurity hardware) is essential for suppliers. |

| Germany | The German Institute for Standardization (DIN) sets strict material and security standards for industrial fasteners. DIN 7991 and DIN 933 regulate mechanical fasteners, while aerospace and defense sectors follow DIN EN 9100 standards. |

| France | The French Cybersecurity Agency (ANSSI) enforces security regulations for hardware components, impacting demand for tamper-resistant fasteners in IT and telecom. Compliance with NF (Norme Française) certification is necessary for construction and industrial applications. |

| China | The CCC (China Compulsory Certification) is mandatory for fasteners used in automotive, aerospace, and critical infrastructure applications. The National Security Law (2015) has increased demand in sensitive industries. |

| Japan | The JIS (Japanese Industrial Standards) regulates fastener quality and security. JIS B 1180 is mandatory for bolts and screws, while JIS Q 9100 applies to aerospace fasteners. The Cybersecurity Basic Act (2014) has driven higher demand in IT and telecom. |

| South Korea | The KCS (Korea Certification Scheme) and KC Mark are required for industrial fasteners. The Korean Cybersecurity Strategy (2022) has led to increased demand for secure fastening solutions in data centers and IT hardware. |

| India | The BIS (Bureau of Indian Standards) IS 1367 mandates quality standards for fasteners used in infrastructure. The National Cybersecurity Policy (2013) is influencing demand in IT and telecom. |

| Australia | The AS/NZS 1252 standard applies to structural fasteners. The Essential Eight Cybersecurity Framework is pushing demand for high-security fasteners in defense and IT applications. |

Market Analysis

The industry is on a steady growth path, driven by rising security concerns across sectors such as aerospace, defense, automotive, and critical infrastructure. Fact.MR analysis found that regulatory mandates and the increasing need to prevent unauthorized access in public utilities, electric vehicles, and IT hardware are fueling demand. Manufacturers specializing in high-security fastening solutions stand to gain, while traditional fastener suppliers may struggle to compete without innovation.

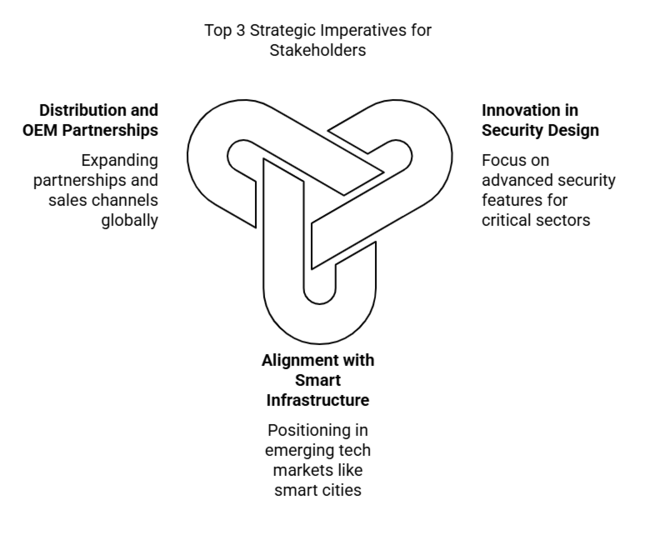

Top 3 Strategic Imperatives for Stakeholders

Strengthen Innovation in Security Design

Executives should invest in R&D to develop advanced fasteners with enhanced resistance to sophisticated tampering techniques, such as anti-picking and self-locking mechanisms, to meet rising security demands in aerospace, defense, and critical infrastructure.

Align with Smart Infrastructure and EV Growth

Companies must position themselves as key suppliers in emerging sectors like smart cities, electric vehicles, and IoT hardware, ensuring their fasteners comply with stringent regulatory and cybersecurity standards to capture long-term demand.

Expand Distribution and OEM Partnerships

Strengthening partnerships with OEMs in automotive, electronics, and industrial automation while expanding e-commerce and direct sales channels will be crucial for maximizing global reach and securing high-value contracts in high-growth regions.

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability & Impact |

|---|---|

| Supply Chain Disruptions- Raw material shortages, logistical bottlenecks, and geopolitical tensions can delay production and increase costs, affecting profitability and delivery timelines. | High Probability, High Impact |

| Rising Regulatory Compliance - Stricter safety and cybersecurity regulations, particularly in aerospace, defense, and IT hardware, could increase compliance costs and limit industry entry for non-compliant manufacturers. | Medium Probability, High Impact |

| Technological Obsolescence - Advancements in smart locking systems and alternative fastening technologies could reduce demand for conventional fasteners, forcing companies to accelerate innovation cycles. | Medium Probability, Medium Impact |

Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Raw Material Sourcing Stability | Run feasibility on nickel-based insert sourcing to mitigate supply chain risks. |

| Product Alignment with Industry Needs | Initiate OEM feedback loop on hybrid insert demand to ensure relevance in evolving applications. |

| Channel Expansion & Industry Penetration | Launch aftermarket channel partner incentive pilot to strengthen distribution and drive sales growth. |

For the Boardroom

To stay ahead, companies must prioritize securing a stable supply chain, fast-track innovation in high-security fastening solutions, and deepen partnerships with OEMs in aerospace, EVs, and smart infrastructure.

Fact.MR analysis found that rising regulatory scrutiny and shifting industry needs demand immediate investment in compliance-driven product development and digital sales expansion. Strengthening R&D in anti-tamper technology while optimizing distribution channels will be key differentiators in the next 12 months. Executives should act now to capture high-growth opportunities before competitors scale their security offerings.

Segment-wise Analysis

By Material

Steel fasteners are projected to grow at a 6.1% CAGR from 2025 to 2035, maintaining their dominance due to high tensile strength, durability, and affordability. Their extensive use in industries such as construction, automotive, and manufacturing ensures continued demand. Heavy machinery, infrastructure projects, and load-bearing applications heavily rely on steel fasteners, making them indispensable.

The rising demand for corrosion-resistant variants, particularly stainless steel, is driving expansion in the marine, energy, and automotive sectors. Stainless steel fasteners, known for their high resistance to extreme environments, are being increasingly used in offshore installations, renewable energy projects, and high-performance vehicles. As global industrialization progresses, the demand for steel fasteners is expected to remain robust.

By Product Type

The screws & bolts segment is set to grow at a 5.9% CAGR from 2025 to 2035, driven by their widespread application across industries such as electronics, public infrastructure, and manufacturing. These fasteners offer superior security, preventing unauthorized access and tampering. Industries such as aerospace and defense also favor screws and bolts due to their structural reliability and ease of application.

Manufacturers are developing advanced coatings and high-strength alloys to enhance durability and corrosion resistance. The introduction of specialized designs, including one-way, pin-in-torx, and hex-lobe drive styles, is boosting their use in high-security applications. With increasing emphasis on theft prevention and secure assemblies, demand for innovative screws and bolts will continue rising.

By Sales Channel

The online sales segment is expected to grow at a 7.1% CAGR from 2025 to 2035, fueled by the rapid expansion of e-commerce platforms and direct-to-consumer sales models. The ability to compare products, access bulk discounts, and receive expert guidance has made online procurement increasingly attractive for industrial buyers. The global shift towards Industry 4.0 is further strengthening this trend.

With rising digital adoption, manufacturers are enhancing their online presence by offering virtual product demonstrations, AI-based recommendations, and automated reordering systems. E-commerce platforms such as Amazon Business, Grainger, and Alibaba are playing a critical role in reshaping industrial procurement, making online channels the fastest-growing distribution network.

By End Use Industry

The industrial & manufacturing sector is forecast to grow at a 6.2% CAGR from 2025 to 2035, driven by increasing automation and the need for secure fastening solutions in modern production facilities. Advanced robotics, AI-driven assembly lines, and smart factories require high-performance fasteners to ensure operational efficiency and prevent system failures.

With global supply chains expanding, industries are shifting towards corrosion-resistant, high-strength fasteners for long-term reliability in harsh environments. The growing focus on sustainable manufacturing and waste reduction is also driving demand for reusable and eco-friendly fastening solutions. As automation and industrial growth accelerate, these fastening solutions will remain an integral part of modern manufacturing operations.

Country-wise Insights

U.S.

The U.S. industry will grow at 7.1% CAGR, driven by aerospace, defense, and IT security regulations. NIST and CISA mandates boost demand for tamper-resistant fasteners in telecom and infrastructure. The IIJA accelerates adoption in public utilities, highways, and critical infrastructure projects.

EV adoption increases demand for high-strength fasteners in battery enclosures. The Buy American Act favors domestic manufacturers, reducing import dependency. Despite rising raw material costs, automation and R&D in corrosion-resistant alloys ensure sustained industry expansion.

UK

Sales in the UK are set for 5.9% CAGR, driven by UKCA Mark regulations and cybersecurity laws. Post-Brexit standards increase demand for compliant fasteners. Public infrastructure projects in railways and highways sustain industry growth alongside expanding defense and aerospace applications.

Leading aerospace firms integrate high-security fasteners in advanced aircraft. Sustainability trends drive the adoption of low-carbon materials. Supply chain challenges from Brexit impact imports, but rising domestic production and automation investments help stabilize long-term growth.

France

Sales in France will grow at 5.5% CAGR, fueled by EU safety regulations, aerospace expansion, and cybersecurity needs. The EU’s Machinery Directive mandates high-security fasteners in industrial equipment, driving adoption. Defense and aerospace sectors, led by Airbus and Dassault Aviation, are key consumers.

Sustainability drives demand for recyclable and lightweight materials. Government-backed railway and renewable energy projects further boost usage. Despite fluctuating raw material prices, R&D in corrosion-resistant alloys and localizing supply chains ensure steady industry expansion.

Germany

Sales in Germany will grow at 5.7% CAGR, supported by automotive, defense, and industrial automation. EU regulations on machinery safety and VDI standards drive demand for high-security fastening solutions. The automotive sector, led by Volkswagen and BMW, integrates specialized fasteners in EVs.

The shift to carbon-neutral manufacturing increases the demand for sustainable materials. Growth in railway expansion and smart infrastructure accelerates adoption. High labor costs and supply chain disruptions pose challenges, but automation and advanced production technologies ensure steady industry growth.

Italy

Sales in Italy are set to expand at 5.3% CAGR, driven by the automotive, aerospace, and construction industries. EU compliance requirements push demand for high-security fastening solutions in machinery and infrastructure. The automotive sector, led by Ferrari and Stellantis, integrates advanced fastening technologies.

Growth in renewable energy projects increases demand for corrosion-resistant solutions. Infrastructure investments in bridges, highways, and public utilities support steady expansion. Supply chain dependencies on imported raw materials remain a challenge, but local production incentives help mitigate risks.

South Korea

Sales in South Korea will grow at 5.8% CAGR, driven by the electronics, automotive, and defense sectors. The government's push for semiconductor and 5G expansion increases demand for secure fastening technologies in IT hardware. Korean defense programs drive adoption in military applications.

EV production by Hyundai and Kia fuels growth in lightweight fastening solutions. High demand for compact, high-strength designs in urban construction projects supports steady expansion. Rising raw material costs challenge profitability, but investments in localized supply chains provide stability.

Japan

Sales in Japan are set to grow at a 5.2% CAGR, driven by automotive, robotics, and construction. JIS safety standards push the adoption of high-security fastening solutions in industrial applications. Toyota and Honda integrate precision-engineered fasteners in EVs and autonomous vehicles.

Smart infrastructure projects and seismic-resistant buildings drive demand for durable fastening solutions. Despite high manufacturing costs, automation in production ensures efficiency. Increasing imports from China create competition, but local innovations in high-precision fastening technologies sustain growth.

China

China will expand at 6.1% CAGR, fueled by industrial expansion, automotive growth, and infrastructure megaprojects. Government mandates on cybersecurity and smart city initiatives boost demand for secure fastening technologies. BYD and Geely integrate advanced solutions in EVs.

Massive investments in railways, bridges, and 5G infrastructure sustain high demand. Supply chain disruptions and fluctuating steel prices remain challenges, but state-backed R&D in high-strength alloys ensures long-term growth. Export demand for precision-engineered fasteners continues to rise.

Australia & New Zealand

Sales in Australia-New Zealand are set for a 5.4% CAGR, driven by construction, mining, and defense. Government infrastructure spending on highways, bridges, and energy projects boosts demand. Defense procurement policies favor locally manufactured high-security fastening solutions.

Mining expansion increases demand for corrosion-resistant fastening solutions. The transition to renewable energy drives the adoption of high-durability fasteners in wind and solar projects. Despite reliance on imports, domestic manufacturing incentives ensure industry stability.

Market Share Analysis

Elgin Fastener Group: 12-15%

Elgin will maintain its industry leadership but face pressure from Asian competitors. In 2025, it will focus on aerospace-grade tamper solutions with new titanium alloys and AI-driven counterfeit detection. A partnership with Lockheed Martin will expand its defense sector footprint across NATO countries.

KD Fasteners, Inc.: 10-12%

KD is projected to gain a share in 2025 with its new line of EV battery security fasteners featuring patented anti-vibration technology. Sustainable packaging firms are adopting the company's recently developed biodegradable tamper-proof screws. KD is expanding in Europe through a distribution deal with Würth Group.

PCC Fasteners: 8-10%

PCC's 2025 growth will be driven by its hypersonic aircraft fastener program and blockchain-based authentication system. The Berkshire Hathaway-backed company is opening a new R&D center in Ohio focused on extreme-environment fasteners. A recent acquisition in Germany strengthens its European industrial client base.

LISI Group: 7-9%

LISI is betting on automotive lightweighting solutions with its new titanium tamper-proof range. The company's 2025 strategy includes a joint development program with Airbus for 3D-printed security fasteners. A new hydrogen-resistant coating technology is being tested with energy sector clients.

Tamper-Pruf Screws, Inc.: 6-8%

Tamper-Pruf is innovating with IoT-enabled screws that alert to unauthorized removal attempts. The company's 2025 "unpickable" series is targeting high-security facilities and critical infrastructure. Expansion into Latin America begins with a new distribution center in Mexico City.

Hangcha Fastener Tech: 5-7%

Hangcha is disrupting the industry with cost-competitive security fasteners, gaining traction in Africa and Southeast Asia. Its 2025 IPO will fund the development of advanced anti-corrosion coatings. A partnership with Huawei aims to supply tamper-proof solutions for 5G infrastructure projects.

Noblelift Security Fasteners: 4-6%

Noblelift is growing through specialized solar-powered tamper solutions for remote applications. The company's new Vietnam factory will serve the ASEAN regions starting Q2 2025. A technology-sharing agreement with a Polish manufacturer will facilitate European expansion.

Key Companies

- Anzor Fasteners

- Bryce Fasteners

- Electronics Fasteners

- Elgin Fastener Group

- Extreme Bolt & Fastener

- GHS Fasteners

- Hafren Fasteners

- Insight Security

- KD FASTENERS, INC.

- Klein Tools

- LISI Group

- Loss Prevention Fasteners

- MCP Fixings

- Mudge Fasteners

- Ocean State Stainless, Inc.

- Parker Fasteners

- PCC Fasteners

- RS Pro

- Security Fasteners UK

- Sentinel Group

- Tamperproof

- Tamper-Pruf Screws, Inc.

- Tanner Bolt

- Trifast

- Zoro UK

Tamper-proof Fasteners Market Segmentation

By Material :

By material, the industry is segmented into steel, alloy steel, stainless steel, aluminium, others.

By Product Type :

In terms of product type, the industry is segmented into screws & bolts, nuts, and others.

By Sales Channel :

Based on sales channel, the industry is segmented into online sales, offline sales, and others.

By End Use Industry :

By end use industry, the industry is segmented into industrial & manufacturing, aerospace & defense, automotive, electricals & electronics, it & telecom, construction & utilities, oil & gas, self service & automation, public facilities, energy & power, and others.

By Region :

The industry is segmented by region into North America, Latin America, Western Europe, South Asia & Pacific, East Asia, Middle East, and Africa.

- Frequently Asked Questions -

What are tamper-proof fasteners used for?

Tamper-proof fasteners prevent unauthorized access and are widely used in public infrastructure, electronics, automotive, and industrial sectors.

How do tamper-resistant screws and bolts enhance security?

These fasteners feature unique head designs that require specialized tools for removal, preventing unauthorized disassembly.

Which materials are most commonly used for tamper-proof fasteners?

Stainless steel, alloy steel, and aluminum are preferred for their strength, corrosion resistance, and durability.

What factors are driving the demand for tamper-resistant fasteners?

Rising security concerns, stricter regulations, and increasing automation in industries are key demand drivers.

Where can businesses source high-quality, tamper-proof fasteners?

They are available through online platforms, specialty hardware stores, and authorized distributors.

Author:

Shubham Patidar

Editor:

Naved Ahmed