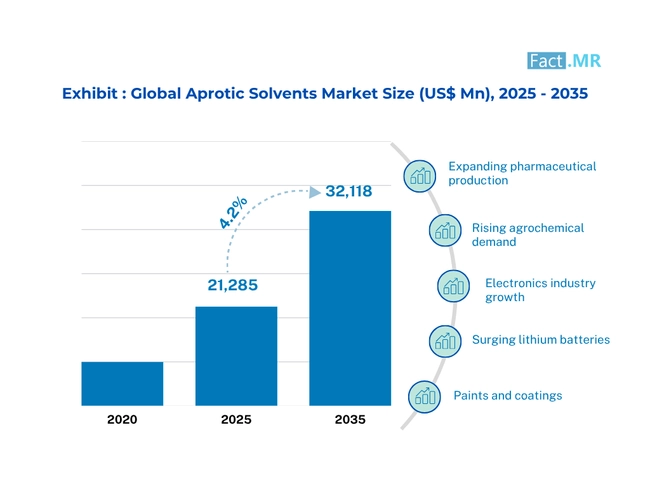

- Base Value(2025): 21285 Mn

- Forecast Value (2035): 32118 Mn

- CAGR (2035): 4.2%

Aprotic Solvents Market Outlook from 2025 to 2035

The global aprotic solvents market is expected to reach USD 32,118 million by 2035, up from USD 20,455 million in 2024. During the forecast period 2025 to 2035, the industry projected to expand at a CAGR of 4.2%, driven by increasing demand in electronics and pharmaceutical manufacturing. Their high chemical stability and ability to dissolve polar compounds make them ideal for advanced applications.

What are the drivers of Aprotic Solvents Market?

The pharmaceutical industry relies heavily on aprotic solvents for drug formulation, utilizing them as essential components during the production of active pharmaceutical ingredients. The rising demand for high-purity aprotic solvents continues to grow as the pharmaceutical industry advances through healthcare advancements, increased investments in R&D, and higher rates of chronic diseases.

Specialized solvents with high stability, low toxicity, and strong solvency properties have gained increased demand from the pharmaceutical industry due to their requirements for precision medicine technologies, biologic compounds, and innovative drug delivery methods. Pharmaceutical manufacturing centers in North America, the Asia-Pacific region, and Europe have stringent requirements for high-quality solvents, as regulatory authorities enforce strict standards in drug production.

Aprotic solvents find their applications in the electronics manufacturing industry as a primary market force. The manufacturing process of semiconductors, together with printed circuit boards and electronic components, heavily depends on these solvents for successful production.

Semiconductor fabrication relies on aprotic solvents for material cleaning and etching to dissolve various components, which produces accurate and reliable manufacturing outcomes. Aprotic solvents continue to grow in usage for lithium-ion battery electrolyte production because they optimize the performance and operational lifetime of such batteries.

Aprotic solvents act as essential components in all major refining operations throughout the oil & gas sector and in multiple petrochemical applications. Global energy consumption continues to rise, so industries sustain their exploration and production efforts mainly through regions containing natural resources, such as North America and the Middle East.

What are the regional trends of Aprotic Solvents Market?

The Asia-Pacific region leads the aprotic solvents market due to its strong dominance, as it contains active electronics sectors and dynamic pharmaceutical production capabilities. High-performance solvents experience continuous demand from Chinese, Japanese, and South Korean manufacturers who process semiconductors, consumer electronics, and pharmaceutical ingredients. The Chinese chemical industry remains a global leader due to its well-established industrial base and government funding for high-tech production.

Pharmaceutical-grade solvents are expected to continue growing due to the expansion of healthcare operations and increasing research and development investments in the region. Asian manufacturers are engaging in environmental sustainability by seeking eco-friendly alternatives that also meet regulatory requirements for solvent consumption.

The aprotic solvents market in North America continues to advance through manufacturing technologies for chemicals, semiconductors, and electric vehicle production activities. The region is home to several chemical industry giants that continually advance their product development alongside sustainability practices.

The rise of electric vehicle uptake in the United States requires numerous high-quality aprotic solvents for manufacturing electric vehicle batteries on a large scale at manufacturing facilities. Manufacturers must develop environmentally friendly solvent solutions for the renewable energy and bio-based chemical sectors that meet stringent regulatory standards set by organizations such as the Environmental Protection Agency (EPA) and the Food and Drug Administration (FDA).

The aprotic solvent market in Europe is experiencing continuous growth due to stringent environmental regulations, as well as a persistent push for sustainable solutions. The European Union directs member states to prevent the release of volatile organic compounds while promoting green chemistry processes through requirements that encourage the use of bio-based and non-harmful solvents. The pharmaceutical and chemical industries in Germany, France, and the United Kingdom have established themselves as developed economies that power the solvent market.

Country-Wise Outlook

Pharma Funding and EV Growth Power USA Aprotic Solvents Market Amid Green Shifts

The USA aprotic solvents market is driven by pharmaceutical innovation, as well as lithium-ion battery manufacturing and industrial coating operations. Drug synthesis, along with biotechnology, receives increased funding, creating a rising demand for DMSO and NMP solvent applications. EV production growth accelerates battery electrolyte production specifically because aprotic solvents serve as critical components.

The implementation of harsh restrictions on environmental pollutants DMF and NMP has motivated industry to transition to bio-based solvent solutions. The USA market understands the benefits of green chemistry and semiconductor investments, which will drive ongoing market expansion through the forecast period. Sustainability trends will influence the innovation of future solvents that promise environmental conservation.

Battery Leadership and Green Policy Cement China’s Dominance in Aprotic Solvents

China primarily drives the global aprotic solvents market due to its extensive chemical manufacturing, as well as electronic production and battery manufacturing activities. The strong market demand for high-performance solvents throughout China persists, as it leads the lithium-ion battery production sector.

The strong pharmaceutical industry, along with agrochemical production bases, propels solvent consumption in the country. Modern automotive developments in China, combined with the country's national emphasis on new energy vehicles, demand advanced electrolytes due to the industry's growth.

The government supports pollution reduction through environmental regulations about low-toxicity and eco-friendly solvents, which leads industries to invest in research and development projects. China presents ongoing market potential for solvent consumption because of its developing sustainable practices and extensive industrial activities.

High-Tech Innovation and Green Chemistry Drive Japan’s Aprotic Solvents Market

Japan’s demand for aprotic solvents depends heavily on technological advancements, battery innovations, and the manufacturing of semiconductors. The market for lithium-ion batteries globally leads to increasing demand for electrolytes that use solvent-based systems. Buyers in semiconductor fabrication and display manufacturing units demand high-purity aprotic solvents, including NMP and DMAC, for their operations. Japan's pharmaceutical production plays a major role in advancing the market expansion.

Japan develops bio-based solvent alternatives through its efforts to provide sustainable chemical production. Industry regulations for environmental safety compel companies to seek safer, eco-friendly solvents, which places Japan at the forefront of green solvent development.

API Expansion and EV Policies Accelerate India’s Aprotic Solvents Growth

The market for aprotic solvents in India is growing substantially due to the steady increase in pharmaceutical manufacturing, agrochemical production, and industrial finishing requirements. The rapidly expanding API manufacturing industry in the country leads to substantial solvent use of DMSO and DMF solutions. Both the automotive industry and the electric vehicles segment need battery electrolytes due to the FAME-II government program. The Indian solvent market growth is expected to intensify due to an increase in foreign investments in specialty chemicals and electronics.

The adoption of non-hazardous alternative solvents is increasing due to existing restrictions on hazardous substances imposed by regulatory bodies. The industrial development of India is expected to result in sustained growth of high-performance aprotic solvent consumption.

Country Wise Insights

| Countries | CAGR (2025 to 2035) |

|---|---|

| United States | 4.8% |

| China | 6.4% |

| Japan | 4.3% |

| India | 9.1% |

Category-Wise Analysis

Battery Boom and Industrial Coatings Sustain Demand for NMP in Aprotic Solvents

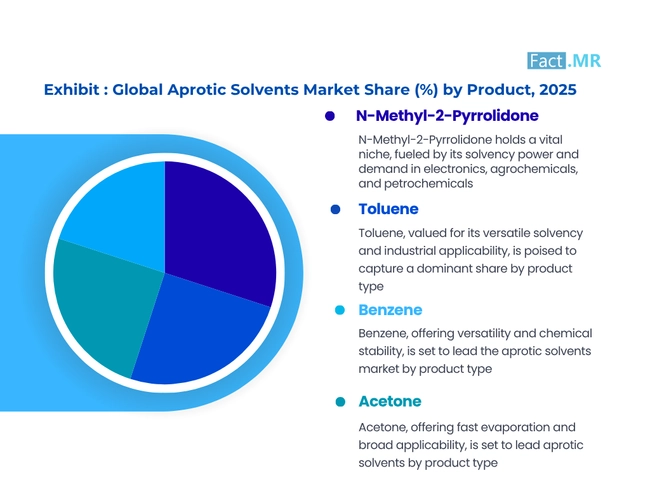

The market segment for aprotic solvents leads with N-Methyl-2-Pyrrolidone (NMP) because this solvent finds extensive use within the oil & gas industry. The oil and gas purification, extraction, and refining sector heavily depends upon N-Methyl-2-Pyrrolidone since it ensures the compliance of fuels with worldwide regulations through desulfurization procedures.

The rising oil refining capacity in Asia-Pacific especially China and India creates additional demand. The European Chemicals Agency through its regulatory actions has assigned NMP a Substance of Very High Concern (SVHC) status so industries must either replace it with alternative solvents or create environmentally friendly solvent variants to fulfil safety requirements.

Process Efficiency and Extraction Needs Drive Aprotic Solvent Use in Oil & Gas

Economic activities in the oil and gas industry extensively rely on aprotic solvents, including NMP and other high-performance solvents, because these solvents are essential for extraction as well as refining and purification operations. The market demand for low-sulfur fuel production, together with growing global energy consumption, has boosted solvent usage.

Petrochemical capacities in Saudi Arabia, the USA, and China are expanding, resulting in increased demand for the market. The pressure from environmental regulations concerning VOC emissions, along with stricter norms in North American and European regions, has caused refinery operators to invest more in sustainable solvent development and process improvements.

API Synthesis and Drug Innovation Propel Aprotic Solvent Demand in Pharmaceuticals

The pharmaceutical industry uses toluene and acetone as major aprotic solvents to develop drug formulations and API production, together with laboratory research practices. The Asia-Pacific region becomes a major market driver for solvent use because of rising generic drug and specialty pharmaceutical production, primarily funded by Chinese and Indian companies. The market is evolving toward utilizing high-purity and low-residue solvents because of strict requirements from the FDA and GMP regulations.

Green chemistry is developing new sustainable alternatives to drug manufacturing solvents because drug manufacturers have started investing in bio-based and water-based solvents due to increasing concerns about toxic residues.

Formulation Stability and Finish Quality Fuel Aprotic Solvent Use in Paints & Coatings

Solvent-based coatings applied to construct and automotive infrastructure and industrial facilities use benzene and toluene as aprotic solvents in the paints and coatings industry. The expanding infrastructure activities across emerging markets such as China, Brazil, and India continue to strengthen market demand. The automotive and aerospace industries require high-performance, solvent-based formulations to achieve coating longevity alongside rapid drying capabilities.

The industry moves toward sustainable low-VOC waterborne and bio-based coatings due to limitations on volatile organic compounds and benzene carcinogenic properties, which require substantial investments into environmentally friendly solvents.

Competitive Analysis

The aprotic solvents market is characterized by established market players and a growing number of small to medium-sized enterprises that are pursuing new opportunities in this evolving industry. Major chemical companies BASF SE, The Dow Chemical Company, Eastman Chemical Company, and INEOS Group currently lead the aprotic solvents market through their broad ranges of products, their advanced scientific research, and broad distribution systems, which provide them with competitive advantages.

The major players in this sector expand their market dominance through strategic business deals that combine acquisitions with partnership arrangements and more. Competitive forces rise because small companies and specialty producers serve specific applications with customized products that match individual client needs. Large companies invest significant resources into environmentally friendly, safe aprotic solvents because sustainability rules and market demand for green products both motivate them to do so. The market competition is growing significantly because of newly developed superior solvents with higher solvency power and reduced levels of toxicity, together with minimized VOC emissions.

The companies that unite continuous innovation practices with the goal of sustainable production will probably achieve increased market dominance through upcoming years. Industrial corporations have chosen to establish new facilities and sales outlets across Asia-Pacific countries, mainly targeting China and India, due to growing product requirements in these regions. Enterprises will experience rapid market changes because they seek to differentiate their operations by combining innovative product development and strategic partnership work with committed environmental sustainability initiatives.

Key players in the aprotic solvents industry include AlzChem Group AG, Arkema SA, Asahi Kasei, Ashland, BASF SE, Celanese Corporation, China National Petroleum Corporation, Dow, Eastman Chemical Company, INEOS, Mitsubishi Chemical, Solvay SA, Vizag Chemical International, and other notable players.

Recent Developments

- In September 2024, Huntsman introduced E-GRADE® MEOX, a high-performance aprotic solvent designed as an alternative to NMP. E-GRADE® MEOX offers excellent solvency, low vapor pressure, and is suitable for applications in lithium battery cathode slurries and electrochromic glass.

- In June 2024, Huntsman launched E-GRADE® THEMAH, a safer alternative to TMAH in semiconductor cleaning processes. E-GRADE® THEMAH provides lower corrosion rates, reduced toxicity, and effective performance in next-generation semiconductor cleans.

Methodology and Industry Tracking Approach

The global aprotic solvent market research was conducted by Fact.MR in 2025 engaged 6,900 participants across 27 countries. The study ensured that each national market included a minimum of 200 qualified respondents. The majority of respondents (~63%) were drawn from core end-use verticals, including pharmaceutical manufacturers, electronics and battery chemical processors, and polymer formulation specialists.

Data collection was conducted over a 12-month timeframe from June 2024 to May 2025. The primary objective of the study was to analyze procurement preferences, toxicity and safety management trends, and the transition in demand from traditional aprotic solvents to greener, low-VOC alternatives.

The findings were supported by over 190 varied information sources, including scientific journals on solvent behavior, patent registries detailing solvent innovation, government guidelines on volatile organic compound (VOC) emissions, and annual reports of top-tier chemical suppliers.

Since 2018, Fact.MR has consistently tracked developments in the aprotic solvent industry, highlighting emerging solvent systems, regulatory shifts affecting solvent use in sensitive applications, advances in dipolar aprotic chemistries, and the influence of sustainability on solvent selection in high-performance industries.

Fact.MR has provided detailed information about the price points of key manufacturers in the aprotic solvents market, positioned across regions, including sales growth, production capacity, and speculative technological expansion, in the recently published report.

Segmentation of Aprotic Solvents Market

-

By Product :

- N-Methyl-2-Pyrrolidone

- Toluene

- Benzene

- Acetone

- Others

-

By End-Use Industry :

- Oil & Gas

- Pharmaceuticals

- Paints & Coatings

- Electrical & Electronics

- Other End Uses

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What was the Global Aprotic Solvents Market Size Reported by Fact.MR for 2025?

The Global Aprotic Solvents Market was valued at USD 21,285 Million in 2025.

Who are the Major Players Operating in the Aprotic Solvents Market?

Prominent players in the market are AlzChem Group AG, Arkema SA, Asahi Kasei Ashland, BASF SE, Celanese Corporation, China National Petroleum Corporation, Dow, Eastman Chemical Company, INEOS, Mitsubishi Chemical, Solvay SA, Vizag Chemical International and among others.

What is the Estimated Valuation of the Aprotic Solvents Market in 2035?

The market is expected to reach a valuation of USD 32,118 Million in 2035.

What Value CAGR did the Aprotic Solvents Market Exhibit Over the Last Five Years?

The historic growth rate of the Aprotic Solvents Market was 3.9% from 2020 to 2024.