Catalyst Carriers Market Outlook (2025 to 2035)

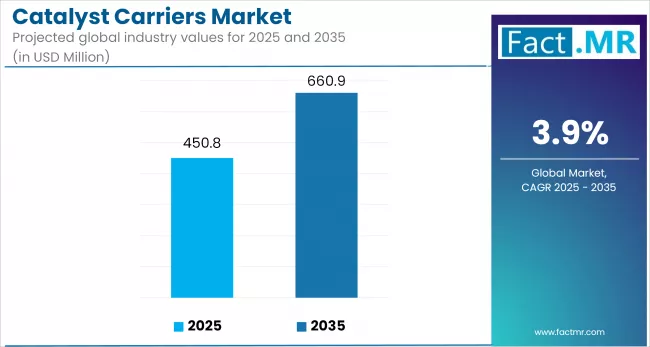

The global Catalyst Carriers Market is projected to reach USD 660.9 million by 2035, rising from USD 450.8 million in 2025. Over the forecast period, the market is expected to grow at a CAGR of 3.9%, driven by increasing demand from the petrochemical and refining industries.

Advancements in nanomaterials, 3D printing, and optimized porosity designs are enhancing carrier efficiency and durability. Additional opportunities lie in scaling the production of eco-friendly catalyst carriers. The catalyst carriers market is also supported by tightening environmental regulations and rising demand for cleaner processing technologies.

What are the Drivers of the Catalyst Carriers Market?

Global industrial energy efficiency goals and resource optimization efforts are driving demand for catalyst carriers. Industries require advanced catalytic solutions that enhance process efficiency, conserve energy, and reduce carbon emissions. Catalyst carriers enhance catalyst performance, improve chemical reaction efficiency, and optimize energy utilization in industrial systems. In petrochemical and refining operations, even marginal improvements in catalytic efficiency can yield measurable cost savings and environmental benefits.

Growth in the petrochemical sector is a significant driver for the adoption of catalyst carriers. According to the USA Energy Information Administration (EIA), global petrochemical output is projected to increase at a rate of 3.5% annually through 2027.

The rising demand for polymers and chemical intermediates, both of which rely on efficient catalytic systems, is driving this expansion. Catalyst carriers play a key role in enhancing catalyst activity and extending lifespan in refining and chemical manufacturing. Increased investments in petrochemical infrastructure, particularly in the Middle East and Asia-Pacific, underscore the strategic importance of catalyst carriers in meeting sector needs.

Tightening environmental regulations are also boosting demand for catalyst-based fuels, including petrol and diesel. Catalytic converters, widely used in vehicles and industrial facilities, help reduce NOx and SOx emissions. As developed regions enforce stricter air quality standards, demand for efficient catalyst carriers is expected to increase. Cleaner fuel production and emissions control technologies will remain central to the growth trajectory of the catalyst carriers market.

What are the Regional Trends of the Catalyst Carriers Market?

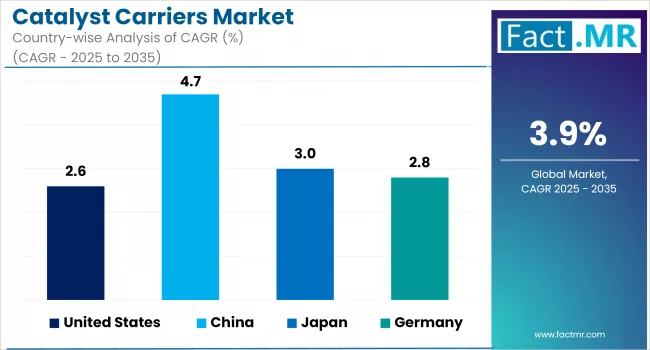

North America's catalyst carriers market remains strong, supported by a well-established refining and petrochemical sector. In the United States, catalyst carriers are in demand for hydroprocessing and catalytic cracking applications. This demand is reinforced by EPA regulations that mandate the use of more efficient and environmentally compliant catalysts.

In Europe, environmental policies such as REACH and the European Green Deal are driving uptake in a mature market. Sustainable manufacturing goals and energy transitions in Germany, the United Kingdom, and France are increasing the need for advanced catalyst carriers in emissions control systems. The automotive and chemical processing sectors generate significant demand across the region.

In the Asia-Pacific region, China, India, Japan, and South Korea lead the growth in catalyst carrier consumption. Industrial expansion, rising petrochemical production, and increasing energy demands are driving demand. Government-led initiatives to reduce pollution and adopt cleaner technologies are accelerating the shift toward advanced catalysts. The region also plays a key role in global supply due to its cost-effective manufacturing capabilities.

In the Middle East and Africa, countries such as Saudi Arabia, the UAE, and South Africa are contributing to market growth through their large oil refining and petrochemical bases. Continued investments in downstream processing and industrial diversification, particularly in GCC nations, support long-term demand. While Africa's market remains nascent, it is expanding steadily, driven by industrial development and growing interest in clean energy adoption.

What are the Challenges and Restraining Factors of the Catalyst Carriers Market?

The high cost of developing and producing advanced catalyst carrier materials is a major concern. Carrier structures with specific properties often require complex manufacturing processes, specialized equipment, and high-purity raw materials. This cost barrier may hinder smaller manufacturers and price-sensitive applications. Research and development aimed at improving carrier performance and meeting industry demands may increase costs, potentially limiting adoption in certain sectors.

The long lifespan and slow replacement cycle of many industrial catalytic systems limit market growth. Replacement of catalyst carriers and systems can take years. Long lifecycles may limit carrier demand to new installations or major process upgrades, slowing market growth. Durable and regenerable catalyst carriers may reduce end-user market volume growth by extending replacement cycles.

The catalyst carriers market faces raw-material scarcity and concentrated supply chains, especially for rare-earth elements used in high-performance ceramic carriers. In April 2025, China imposed export restrictions and a tracking system for rare-earth magnets, leading to a 75% decline in export volumes and global production delays. High prices, procurement volatility, and increased efforts by manufacturers to secure alternative sources and develop non-rare-earth carrier technologies evolved from this disruption.

Country-Wise Outlook

Catalyst Carrier Production in the United States Rises Due to Demand, Innovation, And Local Resources

Catalyst carrier production in North America, particularly in the United States, has increased significantly over the years due to the expansion of production facilities, the establishment of research laboratories, and the ease of sourcing raw materials locally. Governments have increased their spending on chemical synthesis and related processes.

Moreover, the increasing use of chemicals and petrochemicals in the United States is a significant driver of demand for the market. The presence of prominent market players in the United States, combined with timely value-added innovations and advancements, is also driving the catalyst carriers market growth.

Under the Clean Air Act, the USA EPA restricts emissions from industrial, electricity, and transportation sectors. New refinery and chemical plant NOx and VOC emission regulations in 2024 have raised demand for improved catalyst carriers. Under the Inflation Reduction Act (IRA), incentives encourage the use of cleaner technology and high-efficiency, low-emission catalytic processes that employ specialized carriers.

China Witnesses Rapid Industrial Growth

China's robust industrial base, combined with its leadership in the chemical, petrochemical, and refining sectors, drives demand for catalyst carriers. With over USD 1.9 trillion in chemical output in 2024, the country's increasing emphasis on efficiency and process optimization in its production facilities is accelerating the adoption of catalysts. The rising demand for clean energy and polymers, along with the expansion of downstream sectors, supports continued market growth.

Rapid industrialization, large-scale refinery expansions, and China's role as a global manufacturing hub position it as the region's largest consumer of catalyst carriers. Its strong presence in the chemical, oil and gas, and environmental sectors reinforces this status. The Made in China 2025 initiative, which focuses on domestic innovation and high-end manufacturing, including advanced catalyst technologies, is a key driver of the market.

The Ministry of Ecology and Environment (MEE) is tightening regulations on VOC emissions and waste treatment, prompting industries to adopt more efficient catalysts. Eco-friendly carrier materials and local production of high-value carriers are also gaining momentum. Increasing investments in renewable energy, combined with the country's goal for carbon neutrality by 2060, are creating growth opportunities in green chemistry and pollution control.

Japan's Catalyst Carriers Market Thrives on Technology and Sustainability

Japan's catalyst carriers market is defined by precision manufacturing, advanced technology, and regulatory alignment. The automotive and chemical sectors, both of which are significant users of high-performance catalyst carriers, drive much of the demand. Government initiatives, such as the Green Growth Strategy, promote cleaner technologies and fuel-efficient vehicles, thereby increasing the need for innovative catalyst solutions.

Titania- and zeolite-based carriers, widely applied in energy and environmental uses, are being developed domestically. Circular economy approaches, including catalyst regeneration and recycling, are gaining traction. Specialized carriers for clean energy benefit from Japan’s ongoing push toward hydrogen and fuel-cell vehicle technology.

Japan’s commitment to net-zero emissions by 2050, alongside public investment in clean technologies, opens significant opportunities. The country aims to support CO₂ capture pilot plants and reach 200,000 fuel-cell vehicles by 2025. Catalyst carriers are in growing demand for hydrogen production, reforming processes, and CO₂ conversion. Japan’s precision chemical and pharmaceutical sectors, valued at over USD 70 billion, also use ultra-pure, high-surface-area carriers for niche applications.

Category-wise Analysis

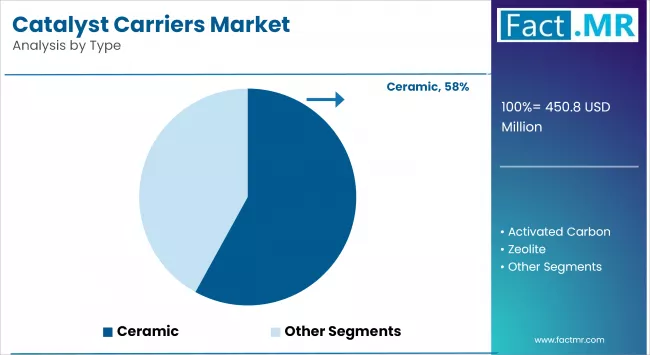

Activated Carbon Emerges as a Competitive Catalyst Carrier Alternative to Ceramics

Ceramics are nonmetallic inorganic solid compounds composed primarily of metals or, in some cases, nonmetals. These compounds become strong and hard through intensive heating in high-temperature applications. Ceramic materials are hard and brittle, offering corrosion resistance across a wide range of uses.

Activated carbon, among other forms of carbon, has become one of the most widely used catalyst carriers. It offers several strategic advantages over alternatives, such as alumina and silica. Key benefits include a significant increase in internal surface area, substantial cost reduction per cubic meter, and suitability for various shapes, particularly in powder, granular, or extruded forms.

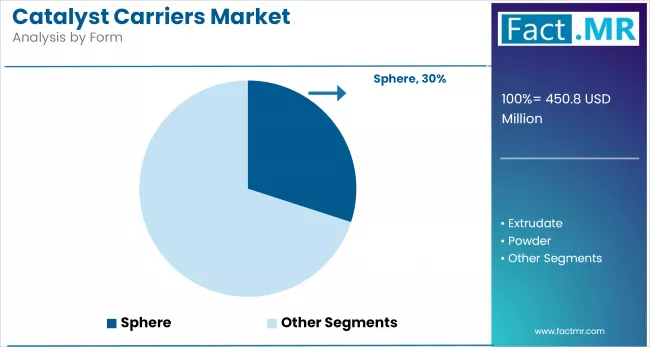

Powder and Spherical Catalyst Carriers Improve Efficiency via Surface Area and Dispersion

Powder catalysts have a higher surface area-to-volume ratio, providing more active sites for chemical reactions. This enhances their catalytic efficiency compared to other forms, such as pellets or granules, and makes them more effective at accelerating processes. Powders are easily combined with reactants to ensure uniform dispersion of the catalyst in the reaction mixture. Catalytic activity must be consistent; this consistency is essential. They are suitable for a wide range of industrial applications because they dissolve easily in various solvents and substrates.

Spherical-shaped carriers are porous catalyst carriers used across a wide range of catalyst support applications. These carriers stand out due to their structural advantages in catalysis. Their spherical form features surface-engraved pores, offering a large surface area for catalyst distribution and accelerating the reaction rate.

High Surface Area Leads the Market, While Intermediate Segment Grows Fastest

The high surface area segment takes over the catalyst carriers market due to its superior performance in complex catalytic reactions. Refining, petrochemicals, and emission control require these carriers due to their high porosity and surface reactivity. Activated alumina, silica, and zeolites are the primary materials in this segment. Their ability to improve catalyst dispersion and lifespan has driven demand in high-efficiency industrial processes. Environmental regulations and the shift to clean fuels boost this segment's global dominance.

The intermediate surface area segment is growing fastest due to its balanced performance and low cost. It is increasingly used in specialty chemicals, gas purification, and moderate-temperature processes where high surface area is not needed. Advancements in water treatment, the adoption of renewable energy sources, and the development of carrier materials are driving growth. The industry values this segment for its affordability, mechanical strength, and catalytic activity, particularly in developing regions.

Catalyst Carriers Enable Effective Diffusion and Stability in Reactions

Catalyst carriers have a bulk pore volume of 0.3-0.7 cm³/g, striking a balance between surface area and accessibility. The moderate porosity allows reactant diffusion and stability under high pressure, making it ideal for catalytic hydrocracking, desulfurization, and chemical synthesis. The consistency of this segment’s gas- and liquid-phase reactions is valued by the industry. Because it works with alumina, silica, and clay-based carriers, it is reliable across multiple end-use sectors.

The rising demand for advanced catalysts in high-mass transport applications, such as environmental remediation and biofuel production, drives the fastest growth in the segment, with a mass transport rate exceeding 0.7 cm³/g. Heavy hydrocarbons and complex organics can be processed with these carriers because bulky molecules pass through more easily. In fuel processing and emission control, demand is rising for clean energy technologies. Global R&D favors their high porosity for catalyst longevity and thermal resistance.

Oil and Gas Dominate Catalyst Carrier Market for Refining Processes

The oil and gas industry controls the catalyst carrier market due to its heavy use of catalytic refining and petrochemical production. Oil and gas companies, among the world's most critical industries, utilize catalyst carriers to enhance hydrocracking, catalytic reforming, and hydrotreating processes. These steps are essential for converting crude oil into petrol, diesel, and other petrochemical products. Advances in catalytic technologies are being driven by global energy demand and rising fuel quality standards.

Petrochemical products are utilized in various industries, including electronics, automotive, construction, packaging, and textiles, thereby increasing global consumption. To meet this demand, petrochemical production facilities have expanded, leading to increased catalyst usage. Due to environmental regulations and efficiency targets, the industry is adopting eco-friendly and effective catalytic processes.

Competitive Analysis

The global catalyst carriers industry is moderately consolidated and highly competitive, driven by rising demand from industries such as oil and gas, petrochemicals, the automotive sector, and environmental applications. Almatis, Evonik Industries, BASF, Cabot Corporation, Magma Catalysts, Noritake Co., Ltd., CeramTec, CoorsTek, Sasol, W.R. Grace, and other players dominate the market due to their diverse product portfolios and global reach.

These companies compete based on material innovation (for instance, high-purity alumina, silica, activated carbon, and zirconia), carrier shapes (such as spheres, extrudates, and honeycombs), and application-specific performance (including thermal stability, surface area, and mechanical strength). BASF and Evonik Industries are market leaders in integrated catalyst systems and R&D-driven solutions, while Almatis and Noritake Co. dominate the structured ceramics and automotive carrier segments.

Companies are also focusing on backward integration and local production to reduce supply chain risks and increase profit margins. However, the market faces challenges such as raw material price volatility (particularly for rare earths and alumina), stringent regulatory standards, and high capital costs, which create entry barriers for new players.

Recent Development

- In February 2024, BASF SE introduced a new high-performance alumina catalyst carrier for the hydrogen production industry. This new carrier has improved thermal stability and mechanical strength, making it suitable for harsh operating conditions.

- In April 2024, Clariant, a specialty chemical manufacturer that prioritizes sustainability, announced the release of CATOFIN 312, its most recent catalyst for propane dehydrogenation. The new catalyst lasts 20% longer and is more selective in its application.

Segmentation of the Catalyst Carriers Market

-

By Type :

- Ceramic

- Alumina

- Titania

- Magnesia

- Silicon Carbide

- Silica

- Others

- Activated Carbon

- Zeolite

- Others

- Ceramic

-

By Form :

- Sphere

- Extrudate

- Powder

- Honeycomb

- Others

-

By Surface Area :

- Low (0-10 m2/g)

- Intermediate (10 - 120 m2/g)

- High (>120 m2/g)

-

By Pore Volume :

- 0-0.3 cm3/g

- 0.3-0.7 cm3/g

- >0.7 cm3/g

-

By End-use Industry :

- Chemicals

- Petrochemicals

- Oil & Gas

- Automotive

- Pharmaceuticals

- Agrochemicals

- Others

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the Global Catalyst Carriers Market size in 2025?

The Catalyst Carriers market is valued at USD 450.8 million in 2025.

Who are the Major Players Operating in the Catalyst Carriers Market?

Prominent players in the market include Almatis, Evonik Industries, BASF, Cabot Corporation, and Magma Catalysts.

What is the Estimated Valuation of the Catalyst Carriers Market by 2035?

The market is expected to reach a valuation of USD 660.9 million by 2035.

What Value CAGR did the Catalyst Carriers Market Exhibit over the Last Five Years?

The historic growth rate of the Catalyst Carriers market was 2.5% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed