Fired Heaters Market Outlook (2025 to 2035)

The global fired heaters market is projected to increase from USD 1.3 billion in 2025 to USD 2.3 billion by 2035, with a CAGR of 6.0%, driven by increasing demand for energy-efficient heating solutions that comply with stringent emission regulations. Stringent emission regulations and energy efficiency mandates are accelerating the adoption of modern, low-emission fired heater technologies.

What are the Drivers of Fired Heaters Market?

The growth of the fired heaters market is primarily driven by the expansion of refinery and petrochemical infrastructure worldwide. As energy consumption continues to rise, particularly in developing regions such as the Asia Pacific and the Middle East, there is a significant push to increase crude oil refining capacity and chemical processing capabilities.

Fired heaters are essential in these operations for preheating crude oil, thermal cracking, and reforming processes. Governments and private entities are investing in large-scale refining and petrochemical projects, further reinforcing the demand for high-capacity, reliable fired heaters.

Another major driver is the growing emphasis on emission control and energy efficiency. With global environmental regulations tightening, especially in Europe, North America, and parts of Asia, industries are under increasing pressure to reduce greenhouse gas emissions and adopt low-NOx combustion technologies.

As a result, many operators are phasing out old and inefficient heaters in favor of modern units equipped with advanced burner systems, better insulation, and energy recovery solutions. These upgrades not only help companies comply with regulations but also reduce operational costs through improved thermal efficiency.

The fired heaters market is benefiting from broader industrial growth in sectors such as food processing, chemicals, pharmaceuticals, and metallurgy. These industries require consistent and efficient heating solutions for their operations and are increasingly adopting fired heaters that offer flexibility and high-temperature performance.

Moreover, the fired heaters market is witnessing a gradual shift toward cleaner alternatives, including electric-fired and hybrid heaters, driven by the increasing availability of low-cost electricity and the growing need for carbon-neutral solutions. This diversification is creating new avenues for growth, particularly in regions aiming to transition to more sustainable industrial practices.

What are the Regional Trends of Fired Heaters Market?

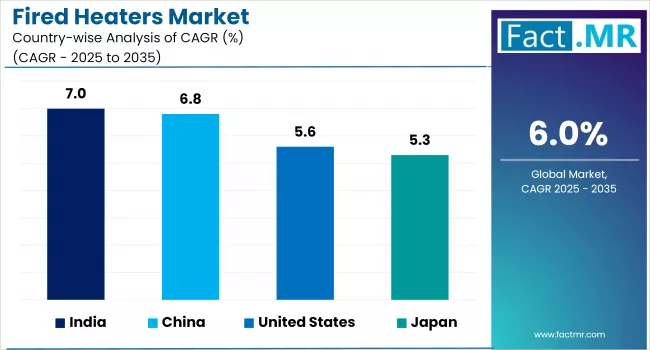

Asia Pacific holds the largest share of the global fired heaters market and is also projected to witness the fastest growth in the coming years. This is primarily due to rapid industrialization, population growth, and substantial investments in refineries and petrochemical complexes, especially in countries such as China, India, South Korea, and Indonesia.

China's focus on refining capacity upgrades and India’s long-term energy infrastructure plans (such as HPCL and IOCL expansions) are major contributors. Moreover, government initiatives to boost domestic manufacturing and industrial output are further fueling demand for fired heaters in sectors like chemicals, fertilizers, and food processing.

North America, particularly the U.S., represents a mature market, where growth is driven more by upgrades and modernization than by new capacity additions. The focus is on replacing aging fired heater units with low-NOx, energy-efficient, and IoT-integrated systems in compliance with EPA and regional environmental standards. The U.S. also has a robust natural gas-based chemical industry, which sustains consistent demand for fired heaters. In Canada, industrial activity and cross-border trade in oil and gas further support steady demand.

The Europe’s fired heaters market is shaped by decarbonization goals and strict emissions regulations, with the EU’s Green Deal and national climate commitments encouraging companies to adopt cleaner combustion systems. The region is focused on retrofitting older units, integrating smart technologies, and exploring hybrid or electric-fired heater solutions. Countries such as Germany, the U.K., France, and the Netherlands are leading the transition toward sustainable industrial heating.

The Middle East, particularly Saudi Arabia, the UAE, and Qatar, remains a significant market due to its dominance in oil and gas production and processing. The region’s investments in downstream petrochemical facilities, such as the Jazan Refinery, Ruwais expansion, and SABIC projects, are driving strong demand for high-capacity fired heaters. Furthermore, national strategies such as Saudi Vision 2030 and ADNOC’s expansion plans are driving the installation of energy-efficient and low-emission heating systems.

What are the Challenges and Restraining Factors of Fired Heaters Market?

One of the foremost challenges is the tightening of environmental regulations worldwide. Fired heaters, which typically rely on fossil fuels like natural gas or oil, are major sources of carbon dioxide (CO₂), nitrogen oxides (NOx), and other pollutants.

As governments and regulatory bodies push for stricter emission controls to combat climate change, operators are under pressure to upgrade existing systems or invest in cleaner alternatives. Compliance with these regulations often requires costly retrofitting, adoption of low-NOx burners, or complete system replacements, which not all businesses are prepared for financially.

Another key restraint is the high capital and operational costs associated with installing and maintaining fired heaters. While these systems are essential in various industries, their upfront installation costs, especially for advanced models with modern controls and emission-reduction technologies, can be prohibitive for small and mid-sized operators.

Moreover, ongoing operational costs, such as fuel, maintenance, and regulatory testing, can further strain budgets. In markets where energy prices are volatile or carbon pricing is implemented, fired heaters can become less economically viable, prompting end users to consider alternative heating solutions.

The market is also facing growing competition from alternative and cleaner heating technologies, such as electric-fired heaters, renewable-powered thermal systems, and industrial heat pumps. These alternatives offer advantages in terms of energy efficiency, reduced emissions, and simpler maintenance.

In regions where electricity from renewables is becoming more accessible and affordable, such as Europe and parts of North America, electric heating technologies are becoming increasingly attractive. This trend poses a threat to the long-term dominance of traditional fired heaters, particularly in sectors actively pursuing decarbonization and sustainability goals.

Technical complexity and safety risks associated with fired heaters further add to the challenges. These systems operate under high temperatures and pressures, requiring careful design, skilled operation, and regular maintenance to prevent failures and ensure the safety of workers.

The process of modernizing or retrofitting older fired heaters to integrate smart technologies or meet new efficiency standards can be both technically demanding and time-consuming. These challenges, combined with a shortage of skilled technicians in some regions, can hinder adoption and slow the rate of system upgrades or replacements.

Country-Wise Outlook

U.S. Fired Heaters Market sees Growth Driven by Rising Demand for Energy-Efficient Systems

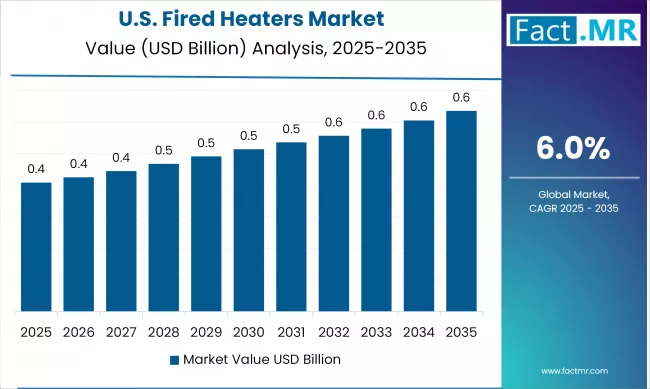

The fired heaters market in the U.S. is experiencing stable growth, largely driven by the modernization of industrial infrastructure and rising demand for energy-efficient systems. As one of the most mature and industrialized economies, the U.S. maintains a vast network of refineries, petrochemical plants, and power generation facilities that rely heavily on fired heaters for high-temperature process heating.

While the country is not adding significant new refining capacity, there is a strong emphasis on upgrading and replacing older fired heater systems with advanced, low-emission, and digitally integrated units to meet modern operational and regulatory standards.

A major contributor to market growth is the need to comply with stringent environmental regulations, particularly those enforced by the Environmental Protection Agency (EPA). Fired heaters, especially older models, are known for emitting substantial quantities of nitrogen oxides (NOx) and carbon dioxide (CO2), which are regulated under various Clean Air Acts.

To meet these standards, industries are increasingly investing in retrofitting fired heaters with low-NOx burners, enhanced combustion controls, and advanced monitoring systems. This compliance-driven upgrade cycle is generating steady demand across industries such as oil & gas, chemicals, and power.

The integration of digital technologies and automation is shaping the U.S. market. Operators are adopting smart-fired heaters equipped with IoT-enabled sensors, predictive maintenance capabilities, and AI-based controls to optimize fuel usage and minimize downtime.

This shift aligns with broader trends toward Industry 4.0, where industrial facilities are embracing intelligent systems to increase reliability and efficiency. These technological advancements are helping mitigate some of the operational risks associated with traditional fired heater systems and are contributing to long-term market expansion.

China witnesses Rapid Market Growth Backed by Rapid Industrialization

The fired heaters market in China is experiencing robust growth, driven by rapid industrial expansion and strong investment in energy infrastructure. The ongoing boom in petrochemical, refining, and power-generation projects continues to push demand for both direct- and indirect-fired heaters, sustaining a high growth momentum.

One of the key drivers behind this growth is the shift towards more efficient and lower-emission heating systems. As Chinese industries work to meet national air-quality targets and global sustainability goals, there's increasing investment in low-NOx burners, insulation upgrades, and smart monitoring systems. These upgrades not only help with regulatory compliance but also reduce fuel consumption, a crucial benefit amid fluctuating energy prices.

China's pursuit of greater manufacturing localization is boosting the local production of fired heater components and systems. By enhancing domestic supply chains, Chinese manufacturers are capitalizing on regional demand to offer faster delivery, better customization, and competitive pricing. This synergy of industrial expansion, regulatory alignment, and supply-chain optimization positions China as a high-growth hotspot for fired heaters over the next several years.

Japan sees Advancements in Industrial Automation Fuels Demand for Fired Heaters

The fired heaters market in Japan is experiencing moderate yet steady growth, driven by advancements in industrial automation, infrastructure modernization, and a shift toward energy-efficient heating technologies.

One of the primary growth drivers in Japan is its emphasis on advanced manufacturing and smart factory environments. As a part of its broader Industry 4.0 adoption, Japanese industries are investing in high-performance fired heaters equipped with digital controls, IoT-based monitoring, and energy optimization features. These smart systems support predictive maintenance, reduce downtime, and improve energy efficiency, aligning with Japan’s goals of boosting industrial productivity and sustainability.

However, the market is also navigating a transition toward cleaner and low-emission alternatives, in line with the country’s commitment to carbon neutrality by 2050. This has led to a gradual shift from conventional gas- or oil-fired systems to electric and hybrid heating technologies in applications where feasible. While this transition may slightly dampen growth for traditional fired heaters in the long term, it also presents opportunities for manufacturers offering low-NOx, high-efficiency, and digitally integrated heater solutions.

Overall, Japan’s fired heaters market is characterized by technological sophistication, regulatory compliance, and high-quality industrial standards. The steady growth in sectors like precision metals, automotive parts, and chemicals continues to sustain demand, even as the market evolves toward more sustainable and intelligent heating systems. The focus on modernization rather than new capacity also means much of the demand will come from retrofitting, efficiency upgrades, and digital transformation, creating a dynamic landscape for both domestic and global heater manufacturers.

Category-wise Analysis

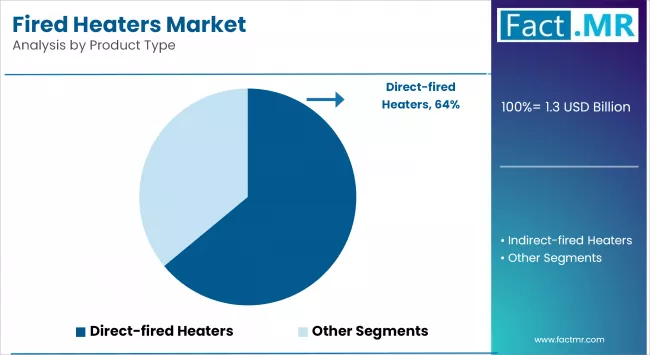

Direct-Fired to Exhibit Leading by Product Type

The direct-fired heaters segment dominates the global fired heaters market and is anticipated to grow at the highest CAGR during the forecast period. These heaters are widely used in refineries, petrochemical plants, and large-scale industrial applications due to their high thermal efficiency and ability to provide intense, direct heat to the process stream. Their cost-effectiveness drives the popularity of direct-fired units, faster heat transfer rates, and relatively lower installation costs.

Direct-fired gas oil hydrocrackers are expected to be the fastest-growing segment. This growth is fueled by the rising demand for ultra-low sulfur diesel and cleaner fuels, prompting refineries to invest in advanced hydrocracking units. Gas oil hydrocrackers offer high conversion efficiency and flexibility, making them essential in modern refining operations. As environmental regulations tighten globally, the need for deeper processing of heavier feedstocks is driving the rapid adoption of these high-performance fired heaters.

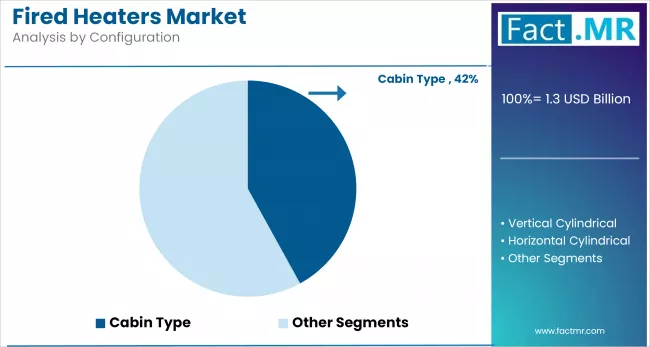

Cabin-Type to Exhibit Leading by Configuration

The vertical cylindrical configuration is the dominant segment in the global fired heaters market due to its widespread use in refineries, petrochemical plants, and large-scale industrial processing facilities. These heaters are favored for their compact footprint, ease of installation, and efficient heat distribution, especially in space-constrained facilities. Their design enables efficient thermal circulation, making them well-suited for applications such as crude oil heating, distillation, and catalytic reforming.

The cabin-type configuration is emerging as the fastest-growing segment, driven by rising demand for modular, custom-built heating systems that offer flexibility in design and enhanced energy control. Cabin-type heaters are particularly gaining traction in process industries such as chemicals, power generation, and specialty manufacturing, where precise temperature control and footprint optimization are critical. These systems are also easier to integrate with digital monitoring, low-NOx burners, and emissions control technologies, aligning well with current industrial decarbonization goals.

11 to 50 MMBtu/hr To Exhibit Leading by Heating Capacity

The 11 to 50 MMBtu/hr segment dominates due to its widespread use across various industries, including petrochemicals, refining, and power generation. This range offers an ideal balance between performance and energy consumption, making it suitable for mid- to large-scale processing operations. Industries prefer this capacity for its ability to efficiently handle a wide range of heating requirements while maintaining flexibility and operational cost-effectiveness, contributing significantly to its leading market share.

The above 50 MMBtu/hr segment is projected to be the fastest growing, fueled by rising investments in large-scale industrial projects and energy infrastructure. As demand for high-volume processing grows, particularly in emerging economies and mega refineries, industries are shifting toward higher-capacity fired heaters that offer enhanced throughput and thermal efficiency. Technological advancements and environmental regulations are also pushing manufacturers to develop cleaner, high-capacity systems that can meet both performance and emission standards.

Oil & Gas to Exhibit leading by End-Use Sector

The oil & gas sector is the dominant end-use segment in the global fired heaters market, accounting for the largest revenue share. Fired heaters are extensively used in upstream, midstream, and downstream oil and gas operations, particularly for applications such as crude oil heating, separation processes, thermal cracking, and refinery distillation.

The dominance of this sector is driven by the continuous expansion of refining capacity, particularly in regions such as the Middle East and Asia-Pacific, as well as the need for high-temperature, high-efficiency heating in critical processes. Moreover, the replacement of aging refinery infrastructure with modern, low-emission fired heaters is helping sustain demand in developed markets such as the U.S. and Europe.

The petrochemical sector is expected to be the fastest-growing segment, driven by rising global demand for polymers, plastics, fertilizers, and synthetic materials. Petrochemical plants rely heavily on fired heaters for processes such as steam cracking, reforming, and hydroprocessing, where consistent high-temperature heating is crucial.

Growth is further accelerated by massive investments in new petrochemical complexes, particularly in China, India, and Saudi Arabia, where governments are actively expanding downstream capacities to diversify their economies and reduce import dependencies. The push for energy-efficient and low-NOx heating technologies in these new facilities is driving rapid adoption of advanced fired heater systems in this segment.

Competitive Analysis

The fired heaters market is becoming increasingly competitive, with a mix of global engineering conglomerates and specialized thermal equipment manufacturers competing across key industrial regions. Key players focus on delivering technologically advanced, highly efficient fired heaters customized for complex applications in the oil & gas, petrochemical, and power sectors. Strategic differentiation often comes from a company’s ability to offer low-NOx designs, high thermal efficiency, digital integration, and turnkey engineering-procurement-construction (EPC) services.

A major trend shaping the competitive landscape is the integration of automation, digital controls, and IoT-enabled monitoring systems. Companies that embed smart controls, real-time diagnostics, and predictive maintenance capabilities into their heater systems are gaining an edge, particularly in developed markets such as North America, Japan, and Western Europe, where industrial automation is well established.

Vendors are also increasingly offering modular and skid-mounted systems that enable faster installation and easier scalability, an attractive value proposition for operators expanding capacity or replacing aging units.

Product innovation and regulatory compliance are key competitive levers. With growing global emphasis on reducing emissions, top players are investing in low-emission combustion technology, including low-NOx and ultra-low-NOx burners, heat recovery systems, and hybrid (gas-electric) heater configurations. Companies that can align their products with regional environmental regulations, such as the U.S. EPA standards or EU climate goals, are well-positioned to capture new business in retrofitting and greenfield projects alike.

Competition is also intensifying from regional and local manufacturers, particularly in China, India, and Southeast Asia, where cost-sensitive markets are seeking affordable, localized solutions. These regional players often compete on price, delivery timelines, and service availability, putting pressure on global firms to offer customized solutions, lifecycle support, and local partnerships. As a result, many international companies are expanding their manufacturing footprints, service hubs, and distribution networks in high-growth regions to strengthen their market presence and stay competitive.

Key players in the fired heaters industry include AbsolutAire, Inc., Sigma Thermal, Hetsco Inc., Thermax, Exotherm Corporation, TechEngineering Srl, Optimized Process Furnaces, Inc., The G.C. Broach Company, Boustead International Heaters Ltd., and other players.

Recent Development

- In February 2025, Inspectioneering hosted a webinar showcasing advanced convection-section cleaning technologies and tube-temperature monitoring aimed at optimizing fired heater efficiency and reducing emissions through smarter maintenance practices.

- In October 2024, IOCL’s Panipat Refinary has commissioned a DHDT cabin-type fired heater, prefabricated and modular in design, as part of its BS‑VI fuel-upgradation program. Similarly, at the Haldia and Bina refineries, IOCL selected Esteem Projects to supply new vertical cylindrical heaters to meet stricter emission targets under BS‑VI norms. These heaters showcase modular design and low-emission performance.

Segmentation of Fired Heaters Market

-

By Product Type :

- Direct-fired Heaters

- Reformers

- Hydrocrackers

- Gas Oil Hydrocrackers

- Crude Distillation

- Others

- Indirect-fired Heaters

- Direct-fired Heaters

-

By Configuration :

- Vertical Cylindrical

- Horizontal Cylindrical

- Cabin Type

-

By Heating Capacity :

- Up to 10 MMBtu/hr

- 11 to 50 MMBtu/hr

- Above 50 MMBtu/hr

-

By End-Use Sector :

- Chemicals

- Petrochemicals

- Power

- Oil & Gas

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the Global Fired Heaters Market size in 2025?

The fired heaters market is valued at USD 1.3 billion in 2025.

Who are the Major Players Operating in the Fired Heaters Market?

Prominent players in the market include AbsolutAire, Inc., Sigma Thermal, Hetsco Inc., Thermax, and Exotherm Corporation.

What is the Estimated Valuation of the Fired Heaters Market by 2035?

The market is expected to reach a valuation of USD 2.3 billion by 2035.

What value CAGR is the Fired Heaters Market Exhibit Over the Last Five Years?

The growth rate of the fired heaters market is 4.8% from 2020 to 2024.

Author:

Shubham Patidar

Editor:

Naved Ahmed