Landfill Gas Market Outlook (2025 to 2035)

The global landfill gas market is expected to reach USD 4,106 million by 2035, up from USD 1,706 million in 2024. During the forecast period (2025 to 2035), the industry is projected to grow at a CAGR of 8.3%, driven by strict emission legislation, increasing demand for renewable energy, and the growing amount of waste in cities.

The favorable policy, the ability to produce energy on a scalable basis, and technological improvements in gas recovery interventions are enabling the increased viability of LFG projects, leading to a high rate of adoption in municipal, industrial, and utility-scale operations in international markets.

What are the drivers of the landfill gas market?

Landfill gas capture systems are gaining importance due to stringent environmental regulations that primarily focus on reducing methane emissions. North American and European governments are implementing restrictions by legislating and providing tax credits, subsidies and carbon-offset benefits. Such a policy environment strengthens the incentives for city and non-state operators to install gas recovery facilities in a manner that enables them to achieve compliance and sustainability targets.

A gas from landfills is a renewable energy source capable of providing grid stability and supplementing intermittent sources such as wind and solar. Utilities and independent power producers are seeking LFG as a combined heat and power (CHP) source, grid injection, as well as vehicle fuel. Its reliability and scalability also make it useful in long-term energy diversification plans.

Due to rapid urbanization, the amount of solid waste is rising, which widens the landfill sites and consequently increases the availability of methane. The combination of this dynamism and gas collection, purification, and monitoring technologies advances the commercial viability of LFG projects. This is due to the greater efficiency of the system, automation, and reduced operational costs, thus opening up for use even in more economies, especially developing ones.

What are the regional trends of the landfill gas market?

The primary segment leader in the study of landfill gas is North America, with its well-established regulation systems, well-developed waste management industry, and well-invested renewable energy projects. There has been a rapid adoption in states with large emission reduction goals, supported primarily by incentives and projects from the U.S. Environmental Protection Agency's LFG energy efforts. Canada is also widening biogas applications using provincial policies.

Europe is a close follower, with the countries of Western Europe, such as the UK, Germany, and France, focusing on the mitigation of methane by EU climate directives. Landfill gas recovery and use are also increasing throughout the region, thanks to the support of feed-in tariffs, carbon pricing, and circular economy policies. In Eastern Europe, there is a gradual improvement in waste management systems, which is slowly catching up.

The Asia Pacific region is rapidly becoming a hub of high growth, particularly in China and Japan, where government reforms in waste-to-energy are being implemented. Early-stage South Asia and Southeast Asia are experiencing a boost in foreign development funding. In the meantime, in Latin America, the Middle East and Africa, there is a gradual market penetration, with the majority of activity being pilot-scale and utility-driven.

What are the challenges and restraining factors of the landfill gas market?

The landfill gas industry is characterized by multiple operating, financial, and regulatory impediments, which slow the industry's growth. Large initial periods of capital investment and long payback times discourage small and mid-sized landfill operators from engaging in LFG-to-energy programs. Financing is also made difficult by project-dependent factors, such as the size of the landfill, waste mixture, and uncertainty in gas yield.

There is also a technical barrier in maintaining the same gas quality and flows, which are associated with technical complexities. Fine gas purification systems, as well as monitoring equipment, are also quite costly and very labor-intensive to operate and maintain.

Regulation-wise, the variable application of emission control laws and the absence of common policies in emerging economies lower investor confidence. Moreover, the opportunity cost of renewable energy sources, such as solar and wind, which tend to have quicker returns and less complex retrofits, has posed a challenge to landfill gas projects, making them relatively less favourable to energy developers and utilities.

Country-Wise Insights

United States Leads with Mature Infrastructure and Regulatory Backing

-2025-to-2035.webp)

The U.S. has the world’s most advanced landfill gas management system, supported by a strong policy framework and a highly developed waste treatment infrastructure. The Landfill Methane Outreach Program (LMOP), coordinated by the Environmental Protection Agency, is still leading the trend with more than 500 active landfill gas energy projects. Tax credits and renewable identification numbers (RINs) are also used as a federal stimulus to increase economic viability.

California, Texas, and Pennsylvania are the states that have taken the lead in implementing projects that utilize landfill gas to produce electricity, fuel vehicles, and inject into pipelines. LFG systems are being coupled with combined heat and power (CHP) applications by the utilities and municipalities, which are witnessing a stable volume of methane produced and scalable technology. Waste Management Inc. and Aria Energy are two privately owned companies that dominate the production and management of infrastructure.

In addition, the popularity of renewable natural gas (RNG) in the transportation sector as a decarbonization tool is revving up LFG development. The United States will continue to experience stable growth due to long-term investments in projects, driven by sustainability goals and ESG requirements.

United Kingdom Expands with Decarbonization Targets and Circular Economy Mandates

Ambitious climate targets and a proactive approach to converting waste into energy around the UK play a significant role. Landfill diversion goals and Government-promoted decarbonization policies have created a favorable environment for LFG investments.

Feed-in tariffs and Renewable Obligation Certificates (ROCs), which made the developers profitable, should have subsidized the industry. Notwithstanding the changes happening in support mechanisms, legacy projects are continuing to thrive, and installations being set up are becoming increasingly efficient in terms of gas collection and automation. The well-regulated waste management sector in the UK can also provide efficient long-term gas recovery.

In the UK, landfill gas is increasingly being used for grid injection and biomethane blending, aligning with the country's broader green gas objectives. As the country transitions towards a circular economy model, the LFG sector is well-positioned to complement energy production processes and emissions control.

China Accelerates with Waste Reforms and Industrial Integration

Landfill gas in China is currently experiencing high growth rates, attributed to the country's reforms in waste management, as well as the trend toward low-carbon industrial activities.

Municipalities in major cities, including Beijing, Shanghai, and Guangzhou, are also investing in waste-to-energy (WTE) infrastructure, combining landfill gas systems with larger environmental management programs. LFG is applied in power generation and is progressively used in industrial steam and fuel applications in adjacent industrial plants, which evidences the Chinese efficiency-based implementation strategy.

Chinese companies are also turning to international cooperation and utilizing new technologies for gas purification, as well as compressed and automated systems. The implementation of regulations is also regional, but at the central level, there is greater convergence with climate strategies, thereby ensuring more effective control and investment. China will be one of the major contributors to global landfill gas growth, given the ambitious environmental targets in place.

Category-Wise Analysis

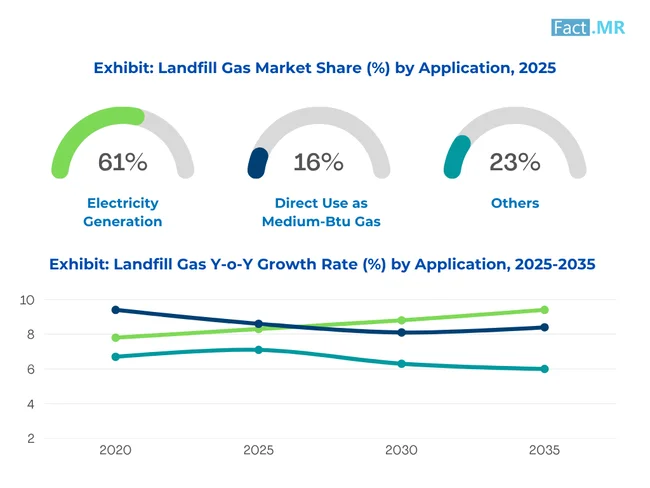

Electricity Generation Dominates Due to Baseload Reliability and Infrastructure Integration

The largest application segment in the landfill gas generation market is electric power, with a significant share due to its compatibility with existing power grids and its stable power output. Unlike solar or wind power, landfill gas provides a more consistent energy flow, making it well-suited for baseload generation. It is preferred due to long-term contracts and grid balancing strategies implemented by municipalities and private operators.

There is also an increased co-location of landfill gas-to-energy projects with landfills, whereby transmission losses are minimized and infrastructure synergies maximized. These systems most commonly use internal combustion engines or turbines to convert methane directly into electricity, which can be used onsite or exported to a grid. The principal adopters, U.S. and European utilities, have been encouraged through renewable portfolio standards at the state level and financial incentives.

In addition, the increasing volume of electricity required by data centers, manufacturing, and municipal infrastructure is also contributing to the strategic role of landfill gas. LFG projects are also considered to offer a two-fold benefit by governments, helping to achieve both waste management and clean energy objectives, which fuels further expansion in this segment globally.

Methane Recovery Leads Owing to Climate Regulations and Energy Value

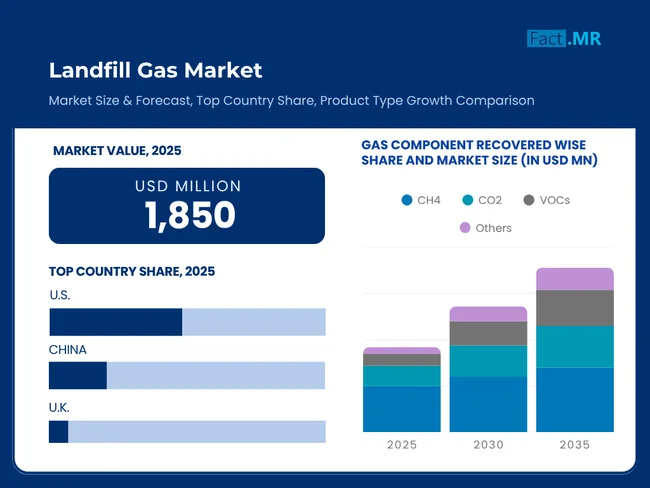

The most important gas recovered from landfills is methane (CH4), which has the highest economic and environmental value. Recovery of methane is receiving a lot of priority from regulatory bodies to reduce climate change due to its high global warming potential.

The extracted methane is used to generate electricity through combustion or converted into renewable natural gas (RNG), making it applicable in various industries. RNG may be injected into natural gas pipelines or directly into vehicles, such as CNG/LNG fleets. This increases the appeal of methane recovery to utilities, fleet operators and decarbonization-seeking large-scale industry users.

Membrane separation, pressure swing adsorption, and cryogenic processes are improving in terms of their technological development and are also becoming more efficient in purifying the methane. Nations such as the U.S., China, and Germany are diving into investing in methane-based LFG projects, making this sector the backbone of commercial feasibility in the landfill gas value chain.

Competitive Analysis

Key players in the landfill gas industry include Waste Management Inc., Tetra Tech Inc., SUEZ, Veolia Environment, Infinis Energy PLC, Highland Energy, Ameresco Inc., Aria Energy Corp, Covanta Holding Corporation, Babcock & Wilcox, Enterprises, Inc., Montauk Renewables Inc., and Quadrogen Power Systems Inc.

The landfill gas market is relatively concentrated, with competition existing in terms of technology, project size, and long-term financing. The major players distinguish themselves by their integrated services, which cover gas collection, purification, energy conversion and emissions monitoring. A key competitive advantage lies in securing public-private partnerships and municipal contracts, particularly in mature markets with favorable regulatory frameworks.

The new competition is implied by the use of modular, mobile or AI-powered LFG systems by companies that shorten setup time and increase predictability in gas yield. Products in renewable natural gas (RNG) applications are gaining traction as demand for clean transportation fuels increases. Local attempts to compete with market participants include regional players that are also becoming increasingly active in the market through local system customization tailored to specific waste characteristics, policy environments, and utility requirements.

Recent Development

- In June 2025, Veolia Environment SA and Waga Energy inaugurated the upgraded Granges-sur-Vologne landfill RNG plant in northeastern France. The renovation increased capacity by 30% to 180 GWh per year and added a second gas purification unit to comply with French biomethane standards. This collaboration expanded Veolia’s global RNG portfolio to ten plants, aiding the EU's decarbonization efforts.

- In April 2025, WM announced the grand opening of four new recycling and renewable natural gas (RNG) facilities across the U.S., part of a $3 billion sustainability investment from 2022 to 2026. The upgrades, including the largest recycling facility near Baltimore and a major RNG facility outside Philadelphia, aimed to enhance landfill gas processing, significantly increasing renewable energy capacity and supporting community energy needs.

Fact.MR has provided detailed information about the price points of key manufacturers in the landfill gas market, positioned across regions, including sales growth, production capacity, and speculative technological expansion, in the recently published report.

Methodology and Industry Tracking Approach

The 2025 landfill gas market report by Fact.MR is based on responses from 6,700 stakeholders across 29 countries, with a minimum of 210 participants per country. Of the total respondents, 58% were end users, including utilities, waste management operators, and municipal bodies. The remaining 42% comprised equipment manufacturers, project developers, consultants, and regulatory authorities.

Insights were gathered between June 2024 and May 2025, emphasizing gas recovery efficiency, technology deployment trends, equipment compatibility, project financing structures, and compliance with evolving environmental regulations. Regional weighting was implemented to ensure balanced representation across all key markets.

More than 190 credible sources were referenced, including technical whitepapers, government reports, environmental policy documents, and audited financial statements.

Fact.MR applied advanced tools such as regression modeling to ensure analytical precision. With continuous industry monitoring since 2018, this report stands as a definitive guide for stakeholders pursuing growth, innovation, and strategic investments in the sector.

Segmentation of Landfill Gas Market

-

By Technology :

- Thermal Technologies

- Combustion

- Gasification

- Pyrolysis

- Biochemical Technologies

- Fermentation

- Anaerobic Digestion

- Mechanical Technologies

- Gas Collection Systems

- Gas Conditioning Equipment

- Thermal Technologies

-

By Gas Component Recovered :

- Methane (CH4)

- Carbon Dioxide (CO2)

- Volatile Organic Compounds (VOCs)

- Others

-

By Application :

- Electricity Generation

- Direct Use as Medium-Btu Gas

- Combined Heat and Power (CHP)

- Vehicle Fuel

- Pipeline Injection

-

By End-Use Industry :

- Utilities and Power Producers

- Industrial Manufacturing

- Commercial Facilities

- Transportation (CNG/LNG vehicles)

- Municipal Operations

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What was the Global Landfill Gas Market Size Reported by Fact.MR for 2025?

The global landfill gas market was valued at USD 1,850 million in 2025.

Who are the Major Players Operating in the Landfill Gas Market?

Prominent players in the market are Waste Management Inc., Tetra Tech Inc., SUEZ, Veolia Environment, among others.

What is the Estimated Valuation of the Landfill Gas Market in 2035?

The market is expected to reach a valuation of USD 4,106 million in 2035.

What Value CAGR did the Landfill Gas Market Exhibit Over the Last Five Years?

The historic growth rate of the landfill gas market was 7.8% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed