Nafion Market Outlook (2025 to 2035)

The global Nafion Market is projected to increase from USD 891.4 million in 2025 to USD 1,537.1 million by 2035, with a CAGR of 5.6%, driven by rising demand for proton exchange membranes in fuel cells, hydrogen electrolyzers, and redox flow batteries. Their use makes them ideal for applications requiring high ionic conductivity, chemical stability, and durability in fuel cells, hydrogen electrolyzers, and redox flow batteries.

-2025-to-2035.webp)

What are the Drivers of the Nafion Market?

The Nafion market is being driven by the growing adoption of clean energy, advancements in industrial technologies, and supportive regulatory frameworks aimed at decarbonization. A primary growth driver is the increasing global emphasis on hydrogen-based energy systems.

Nafion, renowned for its superior proton conductivity and chemical stability, is a crucial component in proton exchange membrane (PEM) fuel cells and water electrolysis technologies, which are central to the hydrogen economy.

As nations roll out hydrogen roadmaps to meet climate targets, demand for PEM electrolyzers has surged in Europe, Japan, and South Korea. For instance, the European Union’s Green Deal and Hydrogen Strategy aim to install at least 40 GW of renewable hydrogen electrolyzers by 2030, boosting Nafion consumption.

In addition to clean energy, the material’s application in the chlor-alkali industry, where it enables safer, mercury-free electrolysis, remains a solid contributor to the product demand. The ongoing transition to sustainable chemical manufacturing processes further supports this trend.

Moreover, Nafion’s role in redox flow batteries and advanced sensors is gaining traction amid growing interest in grid-scale energy storage and precision industrial monitoring. Alongside rising R&D investments and supply chain expansions by major players such as Chemours and Solvay, these factors continue to strengthen the Nafion market’s growth momentum.

What are the Regional Trends of the Nafion Market?

The Nafion market exhibits distinct regional dynamics, shaped by the pace of clean energy adoption, industrial infrastructure, and public investment in hydrogen and electrochemical technologies.

North America, the U.S., continues to be a significant market, driven by rising investments in hydrogen fuel cells and PEM electrolyze installations. The U.S. Department of Energy’s Hydrogen Program and the Inflation Reduction Act (IRA) have catalyzed interest in hydrogen production and storage technologies, where Nafion membranes play a crucial role.

Moreover, demand for sustainable chemical processing and the replacement of asbestos-based diaphragms in chlor-alkali plants further contribute to regional growth.

Europe remains at the forefront of the Nafion market due to ambitious decarbonization targets and strong policy support for green hydrogen. The EU’s Hydrogen Strategy and “Fit for 55” initiative have accelerated the rollout of electrolysis projects across Germany, France, and the Netherlands.

As a result, demand for high-performance ion-exchange membranes used in PEM electrolyzers and fuel cells is surging. Europe is also a hub for advanced battery research, which supports Nafion's use in redox flow batteries and energy storage systems.

Asia-Pacific, led by Japan, China, and South Korea, is witnessing rapid growth. Japan’s Strategic Roadmap for Hydrogen and Fuel Cells and South Korea’s Hydrogen Economy Roadmap are boosting the deployment of fuel cell electric vehicles (FCEVs) and hydrogen refueling stations. In China, the industrial-scale production of green hydrogen, backed by large state-owned enterprises, is driving up demand for high-performance membranes in electrochemical applications.

Additionally, the region’s robust electronics and semiconductor manufacturing base supports the use of Nafion in sensors and specialty coatings.

The rest of the World, including the Middle East and Latin America, is gradually emerging, with early-stage hydrogen infrastructure projects and rising interest in sustainable industrial technologies. Pilot initiatives in countries like Saudi Arabia (e.g., NEOM's green hydrogen plant) suggest potential long-term demand for Nafion membranes as the global hydrogen economy matures.

What are the Challenges and Restraining Factors of the Nafion Market?

Although demand for Nafion is rising in hydrogen technologies and electrochemical applications, several challenges still hinder the market from reaching its full potential.

One of the significant limitations is the high production cost of Nafion membranes. The complex fluoropolymer structure and energy-intensive manufacturing process make it substantially expensive than alternative ion-exchange materials. This cost barrier limits its scalability, particularly for emerging markets or cost-sensitive applications, such as large-scale hydrogen electrolysis, where economic feasibility is crucial.

Another constraint is the limited availability of raw materials used in the production of fluoropolymers. Nafion relies on perfluorinated compounds, which are subject to tight environmental and regulatory scrutiny due to their persistence and potential health risks. Increasing regulatory pressure in regions such as the European Union, which is considering broader restrictions on PFAS (per- and polyfluoroalkyl substances), could affect production capabilities and supply chains.

The market also faces performance trade-offs in high-temperature or long-cycle operations. Although Nafion provides excellent chemical resistance and ionic conductivity, its performance may deteriorate with extended exposure to high temperatures or dry conditions, key factors in high-efficiency fuel cell and electrolyzer operations. This has driven research into alternative or modified membranes that may compete with Nafion in certain use cases.

Furthermore, competition from emerging technologies poses a long-term challenge. Companies and research institutions are investing in next-generation membranes, such as those based on hydrocarbon or composite materials, that offer comparable performance at lower costs and with reduced environmental impact. These alternatives are gaining traction in pilot projects and could potentially displace Nafion in specific applications if scalability and durability improve.

The lack of standardized global hydrogen infrastructure also acts as a bottleneck. Nafion’s demand is closely linked to the pace of fuel cell adoption and electrolyzer deployment. In regions where hydrogen development remains fragmented or delayed due to policy uncertainty or inadequate investment, Nafion market growth may slow.

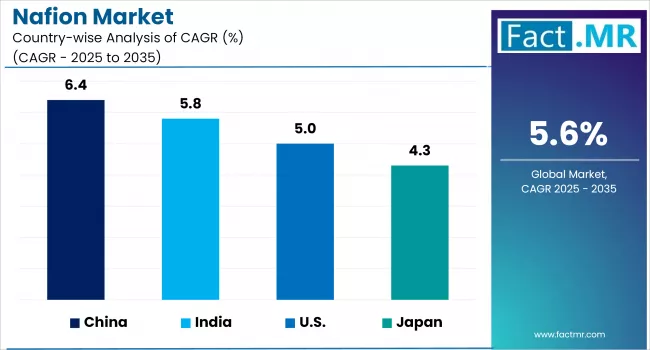

Country-Wise Outlook

U.S. Nafion Market Sees Growth Driven by Clean Energy and Industrial Applications

The U.S. is witnessing a steady increase in Nafion demand, largely driven by national efforts to accelerate the adoption of clean energy and modernize industrial infrastructure. With strong federal support through initiatives like the Inflation Reduction Act and the Department of Energy’s Hydrogen Program, investment in hydrogen production technologies, such as proton exchange membrane (PEM) electrolysis, is growing rapidly. Nafion, a critical component in these systems, is benefiting directly from this momentum.

Beyond hydrogen, the U.S. also relies on Nafion in established sectors such as chlor-alkali production, where it plays a key role in enabling safer, mercury-free electrolysis. Additionally, its application in advanced energy storage, particularly in redox flow batteries, is gaining traction due to the increasing need for grid-scale solutions that support the integration of renewable energy sources.

-2025-to-2035.webp)

Several domestic research institutions and technology companies are also investing in R&D to improve membrane durability and performance, further reinforcing demand. The combination of robust policy backing, a mature chemical processing sector, and emerging clean tech infrastructure positions the U.S. as a significant contributor to growth within the global Nafion market.

China Strengthens Nafion Demand Through Hydrogen and Industrial Growth

China is rapidly emerging as a key growth driver in the global Nafion market, supported by its aggressive push toward hydrogen energy and industrial modernization. As a part of its national decarbonization strategy, China has launched several large-scale projects aimed at expanding hydrogen production capacity through proton exchange membrane (PEM) electrolyzers, where Nafion membranes are a core component.

State-owned energy giants and regional governments are investing heavily in green hydrogen infrastructure, particularly in provinces such as Inner Mongolia, Hebei, and Gansu. These developments are directly increasing the demand for advanced ion-exchange membranes with high chemical resistance and conductivity features that make Nafion a preferred choice.

Beyond energy, China’s massive chlor-alkali industry, which is transitioning from mercury-based to membrane-based technologies, further contributes to the consumption of Nafion. The country also maintains a strong electronics manufacturing base, where Nafion finds use in sensors, fuel cells, and other electrochemical components.

Additionally, Chinese companies are actively investing in domestic research and development (R&D) to reduce their reliance on imports and develop localized alternatives or complementary technologies. These initiatives, paired with supportive government policies and infrastructure investment, position China as a critical player in shaping the future trajectory of Nafion applications across clean energy and industrial sectors.

Japan Expands Nafion Applications Amid Hydrogen Push and Industrial Demand

Japan continues to advance its role in the Nafion market, propelled by the country's strong commitment to hydrogen energy and clean technology.

Under its Strategic Roadmap for Hydrogen and Fuel Cells, Japan is aggressively scaling up the deployment of PEM fuel cells, hydrogen refueling stations, and green hydrogen production facilities, all of which heavily rely on Nafion membranes for their high ion conductivity and chemical durability.

In addition to clean energy, Japan's well-established chemical and electronics industries contribute to consistent demand for Nafion in electrochemical applications such as chlor-alkali processing, specialty sensors, and battery separators. The material’s stability in harsh chemical environments makes it valuable across a range of industrial processes.

Leading Japanese firms are also investing in R&D for advanced membrane technologies, aiming to enhance efficiency and reduce costs in fuel cell systems and electrolyzers.

Furthermore, collaboration between Japanese corporations and international membrane suppliers is facilitating local integration of Nafion-based technologies into automotive and power generation systems.

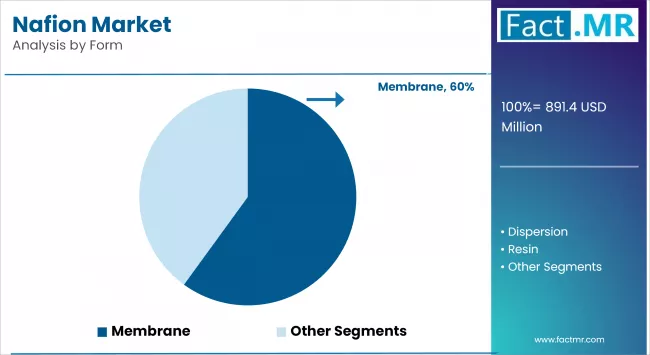

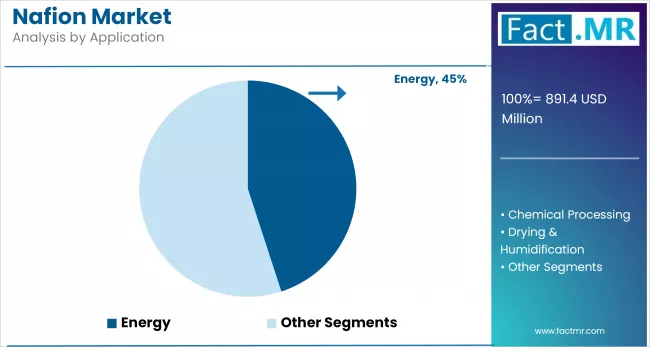

Category-wise Analysis

Membrane to Exhibit Leading by Form

Nafion membranes hold the largest share in the market, primarily due to their vital role in high-efficiency electrochemical systems. These membranes are preferred for their exceptional proton conductivity, chemical stability, and mechanical strength —key characteristics required in demanding applications such as proton exchange membrane (PEM) fuel cells and water electrolysis. Their performance in hydrogen production and utilization systems has made them the industry standard for clean energy projects.

With the global rise in green hydrogen initiatives and decarbonization strategies, governments and corporations are increasingly deploying PEM-based technologies, which heavily rely on Nafion membranes.

In comparison to other forms, such as resins or dispersions, membranes offer the precision and structure required for consistent electrochemical performance in energy systems. Their role is also expanding into redox flow batteries and semiconductor manufacturing, reinforcing their dominance across sectors.

Energy to Exhibit Leading by Application

The energy sector is expected to continue dominating the Nafion demand due to its widespread use in fuel cells, electrolyzers, and stationary energy storage systems. Nafion’s function in enabling efficient hydrogen fuel cells used in fuel cell electric vehicles (FCEVs) and backup power systems is critical as countries commit to net-zero goals. In electrolyzers, Nafion membranes facilitate the separation of hydrogen and oxygen, playing a pivotal role in green hydrogen generation.

Public and private investments in the hydrogen economy bolster this demand. For instance, the U.S. Hydrogen Energy Earthshot, the EU Green Deal, and Japan’s Hydrogen Strategy all emphasize the deployment of PEM electrolyzers, where Nafion is a preferred membrane material.

Competitive Analysis

The Nafion market is becoming increasingly competitive, with a mix of global chemical giants and emerging regional players competing on the basis of product performance, innovation, and application-specific advancements. Leading companies such as The Chemours Company, Solvay SA, AGC Inc., and Dongyue Group Ltd. dominate the global supply of Nafion and related ion-exchange membranes.

These players have established strong manufacturing infrastructure, extensive R&D capabilities, and deep-rooted customer relationships across energy, electronics, and industrial chemical sectors. Their global reach and technical expertise continue to provide a competitive edge, especially in high-growth areas such as fuel cells and hydrogen technologies.

Strategic expansions, partnerships, and product diversification also play a critical role in shaping the Nafion market. Companies like AGC Inc. are broadening their fluoropolymer offerings to serve hydrogen infrastructure and industrial electrolysis applications. Meanwhile, Dongyue Group Ltd. is expanding production to meet the growing demand for PEM systems in China and abroad. These moves enable companies to penetrate new verticals and expand their presence in the fast-growing Asia-Pacific markets, where cost efficiency and local supply are key competitive factors.

Key players in the Nafion industry include The Chemours Company, Solvay SA, AGC Inc., Dongyue Group Ltd., and other regional and emerging manufacturers.

Recent Development

- In May 2025, Chemours partnered with Navin Fluorine (India) to begin manufacturing Opteon two-phase immersion cooling fluid critical for high-powered AI/data-center cooling. This strategic collaboration addresses the growing demand for high-performance, sustainable, and cost-effective cooling solutions for data centers and AI hardware.

- In June 2023, Solvay completed a 20% capacity expansion of its ACORGA® solvent extraction product line at its Mount Pleasant, Tennessee, facility. This expansion enhances Solvay's position in the mining industry, specifically in the production of reagents for copper solvent extraction (SX-EW) processes.

Segmentation of the Nafion Market

-

By Form :

- Membrane

- Resin

- Dispersion

-

By Application :

- Energy

- Fuel Cells

- Hydrogen Production

- Energy Storage

- Chemical Processing

- Chlor Alkali

- Catalysts

- Ion Exchange

- Semiconductors

- Waste Recovery

- Others

- Drying & Humidification

- Single Tubing Systems

- Multi Tubing Systems

- Others

- Energy

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the Global Nafion Market Size in 2025?

The nafion market is valued at USD 891.4 million in 2025.

Who are the Major Players Operating in the Nafion Market?

Prominent players in the nafion market include The Chemours Company, Solvay SA, AGC Inc., Dongyue Group Ltd., and others.

What is the Estimated Valuation of the Nafion Market by 2035?

The nafion market is expected to reach a valuation of USD 1,537.1 million by 2035.

What Value CAGR Did the Nafion Market Exhibit over the Last Five Years?

The historic growth rate of the nafion market was 5.1% from 2020-2024.

Author:

S.N. Jha

Editor:

Naved Ahmed