Metal Finishing Chemicals Market Outlook (2025 to 2035)

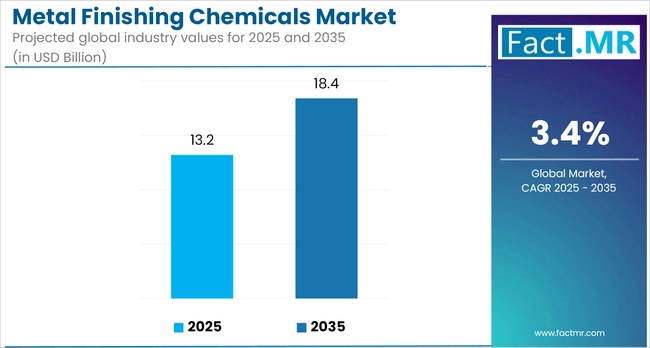

The global metal finishing chemicals market is projected to grow from USD 13,214.8 million in 2025 to USD 18,461.46 million by 2035, with an annual growth rate of 3.4%. Supported by consistent demand across key industries, including automotive, aerospace, electronics, and general manufacturing.

As companies seek to enhance corrosion resistance, extend component lifespan, and improve surface finishes, particularly for lightweight materials and electric vehicle parts, the use of advanced metal finishing solutions is growing.

At the same time, evolving environmental regulations are prompting a shift toward safer, more sustainable formulations, such as chromium-free and cyanide-free alternatives. These regulatory pressures, combined with innovation in application technologies, are expected to support steady market growth over the next decade.

What are the Drivers of the Metal Finishing Chemicals Market?

The metal finishing chemicals market is experiencing consistent growth, driven by increasing demand across key sectors, including automotive, aerospace, electronics, and industrial manufacturing. These chemicals play a crucial role in enhancing corrosion resistance, wear resistance, and the overall surface quality of metal parts used in a wide range of applications.

In the automotive industry, with the shift toward electric and lightweight vehicles, manufacturers are increasingly relying on advanced surface treatment processes to enhance the longevity and performance of components. Similarly, the electronics sector relies on high-precision metal finishing for essential components, such as printed circuit boards, connectors, and semiconductors.

Tighter environmental regulations, especially in North America and Europe, are accelerating the transition toward safer, more sustainable formulations, such as those free from hexavalent chromium and cyanide. Meanwhile, infrastructure expansion and increased industrial activity in emerging economies are adding to the market’s momentum. Together, evolving regulatory frameworks, performance requirements, and technological advancements are shaping the future growth of the metal finishing chemicals industry.

What are the Regional Trends of the Metal Finishing Chemicals Market?

Differences influence regional trends in the metal finishing chemicals market in industrial maturity, regulatory policies, and sector-specific demand across geographies.

In North America, the United States, demand remains strong due to the continued expansion of the automotive, aerospace, and electronics sectors. Growing investment in domestic manufacturing, alongside stricter environmental regulations, is prompting a shift toward safer, high-performance alternatives such as trivalent chromium and phosphate-free solutions. This shift is evident in automotive parts manufacturing and defense-related applications.

Europe maintains steady demand, supported by a strong emphasis on sustainability and strict compliance with REACH directives. Countries like Germany and France are at the forefront of adopting low-VOC and water-based coatings, moving away from hazardous substances. The region’s established automotive and precision engineering sectors remain major consumers of advanced electroplating and conversion coating technologies.

Asia-Pacific leads in growth, with China, India, South Korea, and Southeast Asian nations driving the expansion. China, as a global manufacturing hub, dominates consumption due to high production volumes in the automotive, electronics, and heavy equipment industries. India is witnessing an increased uptake of metal pretreatment and cleaning chemicals, driven by industrial investment and government-backed infrastructure projects.

In Latin America, moderate growth is observed, primarily in Brazil and Mexico. While the automotive and construction sectors are generating demand, broader market advancement is constrained by regulatory inconsistencies and limited access to advanced finishing technologies.

The Middle East and Africa represent emerging opportunities. Countries in the GCC are investing in industrial diversification and infrastructure in sectors such as oil and gas and water treatment, which is driving demand for corrosion-resistant coatings and advanced surface finishing products.

What are the Challenges and Restraining Factors of the Metal Finishing Chemicals Market?

The metal finishing chemicals market is contending with several structural and operational challenges as regulatory, economic, and technological pressures continue to reshape the landscape. A primary concern is the tightening of global environmental and safety regulations, including the phasing out of hazardous substances such as hexavalent chromium and cadmium under frameworks like the European Union’s REACH regulation. Similar regulatory standards are being adopted across North America and Asia, compelling manufacturers to transition to safer chemical alternatives.

This shift often necessitates substantial upgrades to production processes, thereby increasing operational costs. In parallel, volatile raw material prices, including those for nickel, zinc, and specialty acids, are disrupting supply chains and complicating long-term procurement strategies.

The market is also seeing increased competition from cleaner, more efficient surface treatment technologies such as powder coating and physical vapor deposition, which are being adopted by manufacturers seeking to reduce their environmental footprint. These technologies offer a cost-effective alternative, particularly for companies seeking to mitigate the high compliance burden associated with traditional metal finishing chemicals.

Smaller manufacturers, in particular, face challenges in absorbing the capital costs tied to modernization and compliance. Compounding this, a shortage of skilled labor trained to manage complex chemical formulations and processes is placing additional strain on production efficiency and quality control.

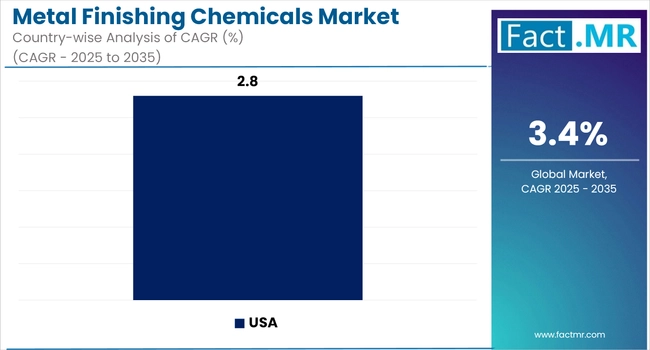

Country-Wise Outlook

| Countries | CAGR (2025 to 2035) |

|---|---|

| United States | 2.8% |

| China | 4.2% |

| Japan | 3.2% |

United States Metal Finishing Chemicals Market Sees Sustained Growth Driven by Regulatory Compliance and Manufacturing Demand

The U.S. metal finishing chemicals market is experiencing steady growth, fueled by consistent demand from key sectors including automotive, aerospace, electronics, and general manufacturing. The need for enhanced corrosion resistance, improved durability, and superior surface aesthetics is driving the adoption of advanced technologies, including trivalent chromium, electroless nickel, and zinc-nickel plating.

Stricter federal and state environmental regulations, overseen by the Environmental Protection Agency (EPA), are prompting a shift toward more eco-friendly formulations. As a result, manufacturers are moving away from traditional solvent-based solutions in favor of water-based and low-VOC alternatives. To remain competitive and compliant, companies are intensifying their investments in R&D and process optimization, with a growing emphasis on sustainable chemistry.

In automotive applications, the push for lightweight and fuel-efficient vehicles, along with the rise of EVs, is increasing the demand for precision-coated metal parts. Aerospace and defense sectors are also focusing on high-performance coatings to protect mission-critical components. Meanwhile, electronics manufacturers are adopting micro-scale plating techniques to enhance electrical performance and extend product lifespans.

Backed by a strong manufacturing ecosystem, advanced infrastructure, and a regulatory environment that encourages innovation, the U.S. remains a key player in the development and adoption of next-generation metal finishing chemical solutions.

China Witnesses Rapid Market Growth, Industrialization, Expanding Automotive And Packaging Sectors, And Rising Investments In Advanced Materials Research

China has established itself as a key player in the metal finishing chemicals market, driven by rapid industrial expansion and robust activity across the automotive, electronics, and heavy machinery sectors. The country's increasing emphasis on scaling up automotive manufacturing and advancing industrial infrastructure has led to a strong uptick in demand for surface treatment solutions.

Supportive government policies and stricter environmental standards are encouraging manufacturers to adopt cleaner, more sustainable metal finishing practices. At the same time, many domestic firms continue to depend on imported technologies due to underinvestment in homegrown R&D, limiting their capacity for innovation.

China’s “Made in China 2025” strategy aims to reduce this dependency by promoting self-sufficiency in critical manufacturing areas, including specialty chemicals. However, issues such as industrial overcapacity and ongoing global trade uncertainties present persistent hurdles for growth.

In parallel, national initiatives like the carbon emissions trading scheme are adding regulatory pressure, encouraging a faster transition toward low-impact, environmentally responsible finishing processes. These trends are expected to shape the next phase of China’s role in the global metal finishing chemicals landscape.

Japan Sees Experiencing Steady Expansion, Supported By The Country’s Advanced Manufacturing Sector.

Japan’s metal finishing chemicals market is experiencing steady growth, driven by increasing demand from the aerospace and automotive sectors. Specifically, the expansion of Japan’s aerospace industry, particularly in the production of aircraft components, has increased the demand for metal finishing chemicals, which are used for high-performance cleaning, corrosion resistance, and surface treatment.

Additionally, government-supported research and development initiatives, along with regulatory backing, have facilitated advancements in chemical formulations designed for precision applications. This has strengthened Japan’s position as a leading player in the metal finishing market, particularly in high-end manufacturing industries where both performance and regulatory compliance are essential.

Category-wise Analysis

Plating chemicals to Exhibit Leading Share Among Product Types

Plating chemicals represent the largest segment within the metal finishing chemicals market, largely due to their wide-ranging applications across industries such as automotive, aerospace, electronics, and heavy machinery, where plating is essential for improving durability, corrosion resistance, and appearance.

Innovations like trivalent chromium and electroless nickel coatings have further boosted demand, thanks to their superior performance, environmental compliance, and ability to extend the lifespan of components. Additionally, tighter regulations focused on surface treatment emissions have driven manufacturers to adopt advanced plating chemicals that not only meet regulatory standards but also ensure operational efficiency.

Electroplating to Exhibit Leading Share Among Processes

Electroplating remains the dominant process in the metal finishing chemicals market due to its broad industrial applications and proven ability to enhance surface properties. It is the go-to method in industries like automotive, electronics, aerospace, and machinery manufacturing, thanks to its effectiveness in improving corrosion resistance, wear durability, electrical conductivity, and visual appeal.

This process is particularly useful for coating metals such as zinc, nickel, chromium, and copper onto substrates like steel and aluminum. For instance, in the electronics industry, electroplating ensures the production of precise, high-performance components with reliable conductivity. In the automotive sector, it helps protect underbody parts and fasteners from rust and wear.

Recent technological advancements, such as pulse plating and automation, have improved both efficiency and consistency while also minimizing chemical waste and reducing energy consumption. Additionally, the growing emphasis on environmentally friendly formulations, including cyanide-free and trivalent chromium baths, is driving further adoption, particularly in regulated markets like North America and Europe.

Zinc to Exhibit Leading Share Among Materials

Zinc continues to dominate the metal finishing chemicals market as the material of choice for coatings. Its prevalence is driven by the combination of corrosion resistance, cost-effectiveness, and regulatory favorability.

In automotive and infrastructure sectors, zinc coatings such as hot-dip galvanizing provide durable protection against rust and weathering, extending asset lifespan and reducing maintenance costs. Innovations in zinc alloy formulations and advanced deposition techniques have further improved coating performance, enabling thinner, more uniform layers that withstand harsh environments.

Additionally, evolving environmental regulations are encouraging the adoption of low-emission zinc processes, reinforcing its position as the leading material for metal treatment applications.

Automotive & Transportation Category to Hold Leading Share in Metal Finishing Chemicals Market

The automotive and transportation sector is expected to maintain its leading position in the metal finishing chemicals market, driven by the industry's demand for high-performance, corrosion-resistant, and durable components. Metal finishing processes such as electroplating, anodizing, and conversion coating are integral in manufacturing parts like engine components, body panels, fasteners, fuel systems, and transmission assemblies.

As vehicle manufacturers prioritize weight reduction and extended product life, surface treatments using specialized chemicals enhance resistance to wear, heat, and environmental degradation. Additionally, the transition toward electric vehicles (EVs) has increased the need for advanced finishing solutions for battery enclosures, electronic connectors, and lightweight aluminum components.

Countries such as Germany, the U.S., Japan, and South Korea, home to major OEMs and tier suppliers, are investing heavily in innovative coatings that meet both functional and regulatory requirements. Simultaneously, emerging markets such as India, Mexico, and Brazil are expanding their automotive production capacity, further driving the consumption of metal finishing chemicals throughout the value chain.

North America holds the Leading Share in the Metal Finishing Chemicals Market

North America continues to lead the metal finishing chemicals market, supported by its advanced manufacturing capabilities and well-established industrial base. The United States serves as a focal point for demand, particularly from the automotive and aerospace sectors, where stringent material and performance requirements drive the adoption of corrosion-resistant coatings, anodizing solutions, and electroplating treatments. Investment in clean production processes and compliance with environmental regulations further encourages the use of advanced chemical finishes.

In addition to conventional industries, growth in electronics and electric vehicles has increased demand for precision surface treatments and conductive coatings. Canada is also investing in surface-finishing technologies within its metal fabrication and machinery industries, strengthening the regional market.

Furthermore, North America’s leading chemicals and equipment suppliers are expanding R&D efforts, focusing on eco-friendly formulations and chrome-free alternatives to satisfy regulatory expectations and customer demand. Together, these factors ensure the region remains at the forefront of metal finishing chemistry innovation.

Competitive Analysis

The global metal finishing chemicals market is characterized by a dynamic and competitive landscape, where established multinationals operate alongside agile regional players. Major corporations like DuPont, BASF SE, and Atotech lead the market with a strong emphasis on sustainable and regulatory-compliant product innovation. Their portfolios increasingly feature chrome-free and eco-conscious solutions, catering to high-demand industries such as automotive, aerospace, and electronics.

Mid-tier companies, including A Brite Company, Advanced Chemical Company, and McGean-Rohco Inc., play a vital role in specialized segments. These firms focus on tailored formulations for metal plating, surface cleaning, and treatment applications. Meanwhile, firms such as PciChemicals.com and KCH Services Inc. distinguish themselves by offering end-to-end chemical processing systems and integrated engineering services to support complex industrial needs.

Emerging companies such as Coral, Elements Plc, and Wuhan Jadechem International Trade Co., Ltd. are rapidly expanding in growth markets across Asia and Latin America. These firms compete on pricing, local responsiveness, and their ability to adapt to regional requirements, which helps them gain traction in competitive territories.

Market dynamics continue to evolve with increased investment in green chemistry, process automation, and the development of multifunctional coatings. As sustainability and efficiency become top priorities, companies across all tiers are engaging in innovation and strategic partnerships to meet rising industry standards and customer expectations.

Recent Development

- In March 2025, IFS Coatings received specification approval from General Motors for coatings used on underhood and underbody components. This reflects growing demand in the automotive sector for advanced, durable treatments suitable for harsh operating environments.

- In February 2025, Ronatec established a new warehouse in Hermosillo, Mexico, to support its electroless nickel solutions. This strategic move improves service speed and logistical support for North American clients.

Segmentation of Metal Finishing Chemicals Market

-

By Product Type :

- Plating Chemicals

- Cleaning Chemicals

- Conversion Coating Chemicals

- Others

-

By Process :

- Pre-treatment

- Electroplating

- Electro-less Plating

- De-greasing

- Polishing

- Etching

- Cleaning

- Chemical Conversion

- Others

-

By Material :

- Aluminium

- Chromium

- Nickel

- Zinc

- Gold

- Silver

- Copper

- Others

-

By End-Use Industry :

- Electrical & Electronics

- Automotive & Transportation

- Industrial Machinery

- Building & Construction

- Aerospace

- Jewellery

- Others

-

By Region :

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- MEA

- Frequently Asked Questions -

What is the Global Metal Finishing Chemicals Market Size in 2025?

The metal finishing chemicals market is valued at USD 13,214.8 million in 2025.

Who are the Major Players Operating in the Metal Finishing Chemicals Market?

Prominent players in the metal finishing chemicals market include KCH Services Inc., Advanced Chemical Company, DuPont, Atotech, BASF SE, and others.

What is the Estimated Valuation of the Metal Finishing Chemicals Market by 2035?

The metal finishing chemicals market is expected to reach a valuation of USD 18,461.46 million by 2035.

What Value CAGR Did the Metal Finishing Chemicals Market Exhibit over the Last Five Years?

The historic growth rate of the metal finishing chemicals market was 2.5% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed