Agricultural Tractors Market Outlook (2025 to 2035)

The agricultural tractors market is valued at USD 75.15 billion in 2025. As per Fact.MR analysis, the agricultural tractors will grow at a CAGR of 6% and reach USD 134.58 billion by 2035.

The agricultural tractors industry experienced renewed momentum in 2024, driven by increasing demand for tech-integrated tractors and upgrades in production and automation. Fact.MR analysis found that while the first half of the year was marked by cautious dealer movement and surplus inventory in key regions, the latter half saw a significant rebound in procurement, especially in South Asia and Latin America. This was especially evident in South Asia and Latin America, where increased acreage and labor shortages accelerated tractor and mechanization adoption [Source: FAO], [Source: World Bank].

North America was stable, with demand revolving around emissions-conformity upgrades and premature take-up of autonomous-ready platforms. Western Europe was, by contrast, characterized by uneven performance, owing to realignments of subsidies and changing environmental regulation. On the other hand, increased mechanization in Southeast Asia and Sub-Saharan Africa drove first-time tractor ownership by large numbers, backed by OEM-led finance programs [Source: OECD], [Source: FAO].

Forward-looking, Fact.MR believes 2025 will be the starting point for a tech-backed growth cycle that will be fueled by telematics, automation, and electrification innovations. Telematics, electrification pilot projects, and semi-autonomous technologies are going to redesign mid-range tractor demand.

The decade will see the trend reverse to sustainable, digitally upgraded equipment as governments will focus on productivity and climate-sensitive agriculture. Emerging sectors will be the driver of future growth, with OEMs concentrating on flexible platforms that are appropriate for fragmented landholding patterns as well as changing crop economics [Source: FAO], [Source: World Bank].

Key Metrics

| Metric | Value |

|---|---|

| Estimated Global Size in 2025 | USD 75.15 Billion |

| Projected Global Size in 2035 | USD 134.58 Billion |

| CAGR (2025 to 2035) | 6% |

Fact.MR Survey Results: Industry Dynamics Based on Stakeholder Perspectives

(Surveyed Q4 2024, n=500 stakeholder participants evenly distributed across OEMs, dealers, agronomists, and large-scale farm operators in South Asia, Eastern Europe, Latin America, and sub-Saharan Africa)

Key Priorities of Stakeholders

- Mid-Range Digital Tractors: 62% of OEMs identified rising demand for 50-90 HP tractors with GPS and telematics, particularly in mid-acreage farms.

- Precision Autonomy: 58% of dealers stated autonomous steering and GPS guidance are now standard expectations for large-acreage users.

- Service Accessibility: 66% of end users prioritized bundled repair and maintenance services due to rural infrastructure limitations.

Regional Variance:

- South Asia: 71% of OEMs observed peak demand for tech-integrated, mid-range models.

- Eastern Europe: 63% of dealers emphasized automation as critical to operational efficiency.

- Latin America & sub-Saharan Africa: 68% of farmers prioritized reliable after-sales support.

Financing Models & Affordability Factors

Flexible Ownership Trends:

- 70% of dealers noted growing demand for leasing, government loans, and subscription-based access.

- 61% of end users expressed affordability constraints, making flexible financing essential in rural regions.

Regional Differences:

- South Asia: 67% of farmers relied on subsidized or state-guaranteed financing.

- Eastern Europe: 54% of dealers partnered with agri-fintech for pay-as-you-use models.

- Africa: 73% of smallholders showed strong interest in co-ownership or pooled leasing models.

Adoption of Advanced Technologies

- Electrification Pipeline: 55% of OEMs plan to launch electric or hybrid tractors by 2027, with early pilots underway in India and Kenya.

- Supply Chain Barriers: 64% of manufacturers cited cost and battery availability as major hurdles.

- Agronomist Input: 59% tied tractor usage to crop resilience under climate variability, citing increased yield stability through mechanization.

Material Preferences & Sustainability Trends

Consensus:

- 65% of stakeholders continued using conventional diesel-powered models but favored digitization for sustainability gains.

Regional Variance:

- South Asia: 60% of dealers reported demand for fuel-efficient systems and alternate engine tuning.

- Latin America: 57% of users explored dual-fuel options to reduce long-term emissions.

- Eastern Europe: 61% supported EU-aligned emissions compliance but demanded subsidies for hybrid models.

Pain Points in the Value Chain

OEMs:

- South Asia: 58% cited battery shortages and emissions compliance costs.

- Eastern Europe: 53% flagged delays in GPS module imports.

- Africa: 61% of OEMs noted limited access to certified local assembly partners.

Dealers:

- South Asia: 64% struggled with rising input costs due to currency fluctuations.

- Latin America: 59% highlighted long lead times from regional warehouses.

- Eastern Europe: 66% of dealers cited labor and technician skill shortages.

End Users (Farm Operators):

- South Asia: 47% reported downtime due to poor access to servicing.

- Africa: 52% faced difficulty sourcing replacement parts.

- Eastern Europe: 60% lacked technical support for digital tractor systems.

Future Investment Priorities

Alignment:

- 68% of global OEMs plan to invest in electrification, digital precision systems, and rural servicing hubs.

Divergence:

- South Asia: 63% focused on low-emission engines for mid-range tractors.

- Eastern Europe: 58% prioritized digital field optimization and fuel management.

- Africa & Latin America: 54% allocated capital to mobile servicing and telematics-integrated tractors.

Regulatory Impact

- South Asia: 69% of OEMs cited evolving emissions standards as a key influence on product design.

- Eastern Europe: 74% of stakeholders aligned their offerings with EU Stage V compliance.

- Africa & Latin America: Only 38% reported direct regulatory influence but emphasized the importance of government subsidies for technology adoption.

Conclusion: Variance vs. Consensus

High Consensus:

Stakeholders agree on the importance of mid-horsepower, digitally equipped tractors with flexible financing and bundled service offerings.

Key Regional Variances:

- South Asia: Focus on affordability and emissions compliance.

- Eastern Europe: Prioritization of automation and digital optimization.

- Africa & Latin America: Emphasis on access to services and flexible ownership models.

Strategic Insight:

- A one-size-fits-all approach will not succeed. Regional tractor strategies must balance digital integration, emissions readiness, and financing access to maximize industry growth.

- To access detailed regional survey breakdowns and strategic tractor adoption forecasts, contact Fact.MR for the full stakeholder intelligence report.

Impact of Government Regulation

| Country/Region | Policy & Regulatory Impact |

|---|---|

| India | The government promotes tractor adoption through subsidy schemes under the Sub-Mission on Agricultural Mechanization (SMAM). Emissions compliance is moving toward Bharat Stage TREM-IV norms [Source: Ministry of Agriculture & Farmers Welfare, India]. |

| Pakistan | Agricultural mechanization is subsidized through provincial programs. However, no centralized emissions or safety certification exists for tractor manufacturers [Source: FAO, Pakistan]. |

| Bangladesh | Tractors receive import duty waivers under the National Agriculture Policy, but there's no strict certification for emissions or safety. The local assembly is encouraged through tax incentives. |

| Poland | Must comply with EU Regulation 167/2013 (Mother Regulation) covering emissions (Stage V), braking, lighting, and driver safety. CE marking is mandatory for access. |

| Romania | Follows EU compliance standards for all imported or locally manufactured tractors. Subsidies under the National Rural Development Programme encourage digital and energy-efficient models. |

| Ukraine | While EU-aligned safety and emissions norms are being adopted, the region still allows older, non-compliant imports. No unified certification system, but reforms are ongoing under EU trade agreements. |

| Brazil | Implements PROCONVE MAR-I (equivalent to Euro Stage IIIA) for agricultural machinery. Inmetro certification is required for tractors sold domestically. The government offers low-interest credit lines. |

| Argentina | Tractors must comply with IRAM standards and safety regulations. Agricultural credit is tied to energy efficiency under Law 27.640, promoting agro-industrial modernization. |

| Mexico | Requires compliance with NOM (Normas Oficiales Mexicanas) safety standards. Emissions regulation is less stringent than in the EU but is evolving. Import duties are waived under agricultural development programs. |

| Kenya | The government supports imports through the Mechanization Services Strategy. No mandatory emissions certification yet. The focus is on increasing access via subsidies and tax reliefs for farm machinery. |

| Nigeria | National policies promote local assembly and tractorization under the Agricultural Promotion Policy. No enforced certification exists; however, OEMs follow voluntary quality standards. |

| South Africa | Follows SANS (South African National Standards) for tractor safety and performance. Emissions regulations are voluntary, but certification is required for finance-backed procurement programs. |

Market Analysis

The industry is entering a decade of steady, tech-enabled growth driven by rising mechanization across emerging economies and growing demand for precision farming. Electrification, telematics, and automation are reshaping equipment preferences, favoring OEMs with flexible, mid-range portfolios. Smaller farmers and regions lacking subsidy support may struggle to keep pace with this transition.

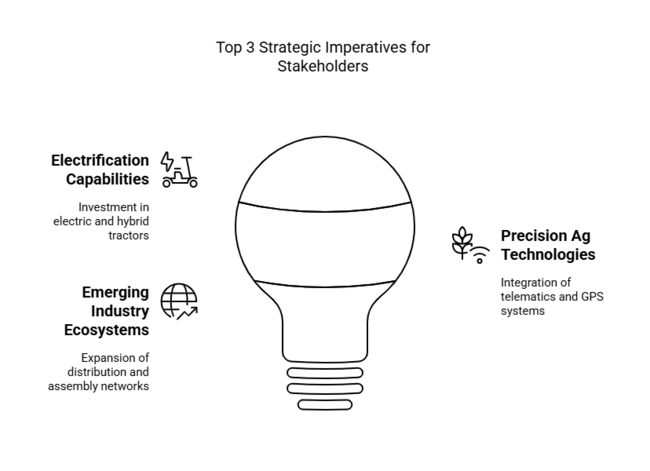

Top 3 Strategic Imperatives for Stakeholders

Expand Electrification Capabilities

Executives should prioritize investment in electric and hybrid tractor platforms, especially for low-to-mid horsepower ranges, to meet rising demand in environmentally regulated and fuel-sensitive regions.

Integrate Precision Ag Technologies

Align product development with farm digitization trends by embedding telematics, GPS guidance, and autonomous-ready systems into mainstream tractor models to stay competitive with evolving farmer expectations.

Strengthen Emerging Industry Ecosystems

Build or expand localized distribution networks, financing partnerships, and assembly capacity in South Asia, Africa, and Latin America to capture first-time buyers and accelerate volume growth.

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability & Impact |

|---|---|

| Regulatory Compliance Costs- Stricter emissions and safety regulations may increase engineering costs and limit product flexibility for OEMs. | High Probability, High Impact |

| Supply Chain Disruptions- Semiconductor shortages, shipping delays, or geopolitical instability could slow tractor deliveries and raise input costs. | Medium Probability, High Impact |

| Slow Adoption in Price-Sensitive Regions- High upfront costs and limited digital literacy may restrict the uptake of tech-enabled tractors in lower-income industries. | Medium Probability, Medium Impact |

Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Evaluate Electrification Readiness | Run feasibility on localized battery sourcing and charging infrastructure support. |

| Accelerate Product-Market Fit | Initiate OEM feedback loop on hybrid and autonomous tractor feature demand. |

| Strengthen Aftermarket Access | Launch aftermarket channel partner incentive pilot in high-growth rural zones. |

For the Boardroom

To stay ahead, companies must immediately realign product development around mid-range electrification and embedded precision technologies while deepening partnerships in emerging regions where first-time tractor adoption is accelerating. This intelligence signals a shift from pure volume growth to value-driven innovation, requiring faster iteration cycles and region-specific go-to-market strategies. Investing now in scalable tech platforms, localized assembly, and digital support infrastructure will be critical to capturing long-term share as the competitive landscape tilts toward efficiency, autonomy, and sustainability.

Segment-wise Analysis

By Engine Power

The below 40 HP segment will have a growth rate of 5.4% CAGR between 2025 and 2035. The segment is mainly catering to smallholder farmers who need compact, low-cost tractors for common farming operations like tillage and transport.

The industry for these tractors is robust in areas with small-scale farming operations, particularly in South Asia, Sub-Saharan Africa, and Latin America. Government subsidies as well as affordable financing are also fueling adoption.

Ease of use and compact size, along with reduced maintenance expenses, make them a popular option among farmers with small landholdings. Their capabilities are, however, limited compared to more powerful models.

By Driveline Type

The 2WD segment is estimated to expand at a CAGR of 5.7% during 2025 to 2035. The segment continues to be in demand in areas where the terrain is flat since 2WD tractors are cost-effective and easy to use, hence well-suited for small and medium farms.

2WD tractors find wide application in areas such as Sub-Saharan Africa, Southeast Asia (Vietnam, Thailand, etc.), and South America (Brazil, Argentina, etc.). They cost less as well as are easy to maintain, which makes them a viable choice for poorer smallholder farmers.

But the segment's progress will be limited in more mechanized agricultural areas, like regions of North America and Western Europe, where 4WD tractors provide improved traction and performance in different terrain conditions.

Country-wise Insights

U.S.

The U.S. is projected to expand at a CAGR of 5.8% from 2025 to 2035, driven by large-scale mechanized farming and growing investments in precision agriculture, particularly in the Midwest, where corn, soybean, and wheat are major crops.

There is sustained demand in the Midwest for high-horsepower tractors, where large-acreage farms are the norm. OEMs are concentrating on designing autonomous as well as GPS-equipped tractor models to assist farmers in lowering labor expenses as well as maximizing yield efficiency per acre [Source: USDA Economic Research Service].

State and national incentives for climate-resilient farming methods and investment in sustainable farming, like subsidies and tax relief, have stepped up the transition to low-emission and hybrid tractors. Mid-sized farm operators in the southern and central U.S. are increasingly opting for leasing models and bundled packages of services, making high-end machinery more affordable.

UK

The UK is expected to grow at a CAGR of 4.9% from 2025 to 2035, supported by the shift towards sustainable farming practices and the adoption of digital solutions following Brexit aimed at improving food system resilience.

Medium-horsepower tractors between 70-100 HP are seeing strong demand, especially in arable regions like East Anglia and the Midlands. The demand for intelligent farming equipment is driving investments in GPS guidance and variable-rate application systems faster.

The UK government's Environmental Land Management Scheme (ELMS) is encouraging the adoption of low-emission farm machinery. OEMs with telematics-enabled tractors as well as Stage V emission compliance standards are becoming popular among big agribusinesses [Source: UK Government].

France

France is expected to grow at a CAGR of 5.2% during 2025-2035 on the back of modernization in viticulture, dairy, and cereal crop industries in Nouvelle-Aquitaine, Brittany, and the Grand Est.

Farmers are increasingly turning to 60-100 HP tractors for mixed farming purposes such as livestock and arable farming, particularly in areas like East Anglia. Demand is highest in telematics and data-driven agronomy models, especially in regions where precision irrigation is followed.

France's CAP Strategic Plan emphasizes emissions cuts and productivity improvements, further spurring demand for hybrid and electric tractors to meet EU environmental targets. Local OEMs are also introducing Stage V emissions compliance models, featuring AI-predictive maintenance and configuring tractor performance.

Germany

Germany is projected to expand at the CAGR rate of 5.4% during the period between 2025 and 2035 through the strong utilization of automation and electrification technologies in agricultural systems in Bavaria, Lower Saxony, and North Rhine-Westphalia.

High-acreage cereal and dairy operations in regions like Bavaria and Lower Saxony are fueling demand for 90-150 HP tractors. OEMs are targeting autonomous-ready versions and battery-electric pilot versions for Germany's strict Stage V emission rules.

Government incentives under the Climate Action Programme and the initiative for digital farming equipment are driving up demand for smart tractors. There is an increasing demand for models with ISOBUS compatibility and cloud-connected performance monitoring, as reported by dealers.

Italy

Italy is expected to expand at a CAGR of 5.1% during 2025-2035, spurred by the growth of mechanized agriculture in southern Italy and vineyard and olive farm modernization in central Italy.

Tractors in the 50-80 HP category dominate the industry, particularly compact tractors for hill farming and orchard farming. Italian farmers are purchasing low-emission, high-performance tractors with narrow bodies and smart control systems.

Government stimulus through the National Recovery and Resilience Plan (PNRR) and CAP subsidies are driving sales of precision agriculture-compatible tractors. Electrification as well as GPS-enabled operations are gaining traction in value crops areas.

South Korea

South Korea is expected to expand at a CAGR of 4.3% during 2025-2035, driven by rural automation programs and government incentives for upgrading small and mid-scale agricultural farms.

There is high demand for sub-50 HP compact tractors, especially for rice farming and greenhouse cultivation in Gangwon, Jeolla, and Gyeongsang provinces. Convenience in maneuverability and compact design are key drivers of purchases.

The government of South Korea is increasing subsidies on smart farming gear, boosting the sales of tractors with self-steering and remote diagnosis. Local brands are focusing on hybrid powertrain models and intuitive telematics interfaces.

Japan

Japan is projected to develop at a CAGR of 4.2% during the period 2025-2035, spurred by a fast-growing aging farming community and universal acceptance of robotics in agriculture.

Farmers prefer compact, autonomous-ready tractors of 20-60 HP, suitable for terraced rice paddies and fragmented landholdings. Industry players are introducing AI-based controls to support elderly operators with minimum physical intervention.

Government schemes such as the Smart Agriculture Demonstration Project are promoting the adoption of GPS-guided and low-emission tractors. Japanese original equipment manufacturers connectivity for remote monitoring and field data analysis.

China

China is expected to grow at a CAGR of 6.7% from 2025 to 2035, driven by swift mechanization in rural regions and national emphasis on food security and digital agriculture.

Strong demand exists for 100+ HP tractors in big farm tracts of Heilongjiang and Xinjiang provinces, although smaller tractors under 50 HP continue to be in favor in the provinces of southern China. Automation is gaining pace in high-yielding grain areas.

The subsidy programs under the Agricultural Mechanization Promotion Law by the government of China are fueling sales. Domestic participants are introducing product lines with Stage IV engines and AI-based smart farming platforms.

Australia & New Zealand

New Zealand and Australia are predicted to grow at a CAGR of 5.6% during 2025-2035 with technological upgradation in broadacre agriculture and animal husbandry systems.

Tractors in the 120-180 HP range are in demand for large farms in New South Wales, Victoria, and Canterbury. GPS-enabled, variable-rate control systems are standard among high-income farming operations.

Both governments offer rebate schemes for low-emission machinery, pushing the adoption of battery-electric and hybrid tractors. Regional dealers note growing interest in autonomous and satellite-linked precision farming models.

Market Share Analysis

John Deere: 20-25%

John Deere will hold the lead spot through the spotlighting of AI and autonomous tractor growth. Dominant exposure in Europe as well as North America will spur development, with its pioneering of precision farming retaining its dominance.

Mahindra & Mahindra: 15-20%

Mahindra & Mahindra is leader in India and is growing fast in Africa. The firm's value tractors are helping it grow well in the industry, and it wants to be a leader in emerging industries with higher exports.

CNH Industrial (Case IH, New Holland): 12-18%

CNH Industrial will emphasize its positions in Europe and the Americas, leading the charge in electric tractor technology. The drive of the company toward sustainable solutions will continue to fuel growth through its portfolio of diversified brands.

Kubota: 10-15%

Kubota is set to expand in Southeast Asia with an increased demand for compact tractors. Its growth in the U.S., combined with technological advancements in small as well as medium-sized farm equipment, will drive its growth over this period.

AGCO (Massey Ferguson, Fendt, Valtra): 8-12%

AGCO will have a strong concentration in the upper-end tractor category, with a continued emphasis in hydrogen-powered tractors. Investment in technology areas like precision farm solutions will provide it with support to establish higher visibility in older and newer agrarian areas.

Sonalika (International Tractors Ltd.): 5-10%

Sonalika is growing fast in price-sensitive industries such as India and Africa. As exports grow, the company's emphasis on cheap yet dependable tractors put it in a position for sustained growth in these industries.

Other Key Players

- TAFE Motors and Tractors Ltd. (Tractor and Farm Equipment Limited)

- Lamborghini Trattori (Argo Tractors)

- Caterpillar Inc.

- Zetor Tractors a.s.

- Dongfeng Agricultural Machinery .

- JCB

- Foton Lovol International Heavy Industry Co., Ltd.

- Mitsubishi Mahindra Agricultural Machinery Co. Ltd.

- Bharat Earth Movers Limited (BEML)

- Escorts Limited

Segmentation

-

By Engine Power :

- Less than 40 HP

- 41 to 100 HP

- More than 100 HP

-

By Driveline Type :

- 2WD (Two-Wheel Drive)

- 4WD (Four-Wheel Drive)

-

By Region :

- North America

- Latin America

- Western Europe

- South Asia & Pacific

- East Asia

- Middle East

- Africa

- Frequently Asked Questions -

What factors are driving the growth of the agricultural tractor industry?

Technological advancements, automation demand, and the need for efficient farming are key growth drivers.

Which regions are seeing the highest adoption of agricultural tractors?

North America, Europe, and parts of Asia, particularly India and China, are adopting agricultural tractors at a high rate.

How are agricultural tractors evolving to meet sustainability goals?

Manufacturers are incorporating electric, hybrid models, and energy-efficient technologies to enhance sustainability.

What technological innovations are impacting agricultural tractor design?

GPS guidance, autonomous driving, and IoT integration are transforming tractor functionality and efficiency.

What are the challenges faced by companies in the agricultural tractor industry?

Companies face challenges with raw material cost fluctuations, high capital investment, and evolving regulations.

Author:

Shubham Patidar

Editor:

Naved Ahmed