Greaseproof Paper Market Outlook (2025 to 2035)

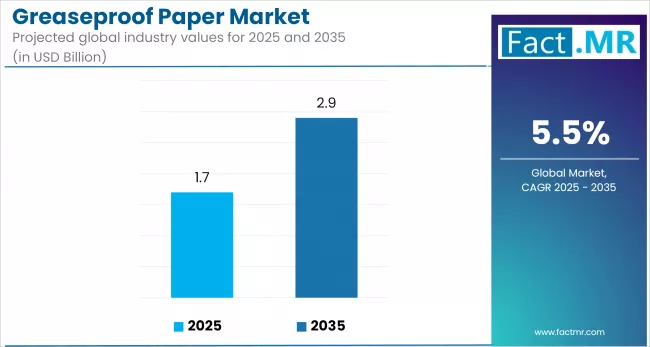

The global greaseproof paper market is expected to increase from USD 1.7 billion in 2025 to USD 2.9 billion by 2035, with a CAGR of 5.5% during the forecast period, driven by rising demand for sustainable, oil-resistant packaging across bakery, foodservice, and takeaway sectors.

Bans on plastic and rising consumer demand for eco-friendly materials are accelerating the shift to paper-based solutions, particularly in Europe and North America.

What are the Drivers of the Greaseproof Paper Market?

The greaseproof paper market is gaining momentum, primarily driven by the global shift toward sustainable packaging and the growing demand for oil-resistant materials in the food industry. Regulatory bans on single-use plastics in regions such as Europe and North America have accelerated the adoption of biodegradable and compostable alternatives, positioning greaseproof paper as a viable solution for eco-conscious brands.

The rapid growth of food delivery services, quick-service restaurants, and on-the-go food consumption has further increased the need for functional, hygienic, and visually appealing packaging. In the bakery and confectionery sectors, greaseproof paper is widely used for wrapping pastries, chocolates, and baked goods, driven by a growing interest in artisanal and premium offerings.

Emerging markets in Asia-Pacific and Latin America are also contributing to market expansion, driven by urbanization, rising disposable incomes, and the growth of organized retail. Manufacturers are developing advanced greaseproof paper variants, including unbleached, chlorine-free, and fluorocarbon-free options, to meet evolving consumer and regulatory demands. These innovations improve safety, support sustainability goals, and help brands stand out in the market.

What are the Regional Trends of the Greaseproof Paper Market?

The greaseproof paper market exhibits distinct regional patterns shaped by local regulations, consumer behavior, and levels of industrialization.

Europe continues to lead global demand, supported by stringent environmental regulations and a strong preference for sustainable packaging. Countries like Germany, France, and the UK are at the forefront, with the widespread use of greaseproof paper in bakeries, food service, and organic food packaging. The region’s ban on certain plastic food wraps and its commitment to the EU Green Deal has further encouraged the shift toward compostable and recyclable paper alternatives.

North America follows closely, driven by rising consumer interest in eco-friendly packaging and a booming food service sector. In the U.S., the use of greaseproof paper is rising across quick-service restaurants, artisanal bakeries, and meal delivery services. Growing focus on food safety and the clean-label trend is driving demand for unbleached and fluorocarbon-free options.

In the Asia-Pacific region, rapid urbanization, the expansion of middle-class populations, and the rise of organized retail are driving demand for functional and affordable food packaging. Countries such as China, India, and Indonesia are experiencing a rising demand for fast food, baked goods, and convenience foods, which are core applications for greaseproof paper. While sustainability awareness is still developing, increasing pressure to cut plastic waste is creating new opportunities for paper-based alternatives.

Latin America is witnessing a gradual increase in urban centers, where the food delivery and retail bakery segments are expanding. Brazil and Mexico are among the active markets, supported by local manufacturing and rising demand for flexible, food-safe packaging.

In the Middle East & Africa, adoption remains limited but is expected to grow alongside rising food imports, bakery product consumption, and hospitality sector development. Markets such as the UAE and South Africa are showing an early interest in sustainable packaging solutions, including greaseproof paper, in high-end food retail and tourism-related sectors.

What are the Challenges and Restraining Factors of the Greaseproof Paper Market?

One of the primary concerns is cost competitiveness. Compared to conventional plastic and wax-coated packaging, greaseproof paper, especially in its unbleached or fluorocarbon-free forms, can be expensive to produce. This cost difference becomes a barrier for small and mid-sized food businesses in price-sensitive markets where budget constraints often override sustainability considerations.

Limited barrier properties also present a challenge. While greaseproof paper performs well against oil and moisture, it lacks high gas and vapor barrier characteristics offered by multilayer films or foil laminates. This restricts its use in packaging applications that require extended shelf life or advanced protection, such as frozen foods or products with high fat content.

Raw material availability and quality fluctuations in sustainably sourced pulp can impact production consistency and pricing. As demand for environmentally friendly paper products rises, competition for certified wood pulp is intensifying, creating supply chain pressures for manufacturers.

In emerging markets, low awareness and weak infrastructure for composting or recycling paper-based materials further restrain growth. Without adequate waste management systems, the environmental benefits of greaseproof paper are not fully realized, which can discourage adoption among regulators and consumers.

Moreover, technical limitations in printing and customization can be a drawback for brand owners seeking high-impact packaging design. Paper's lower resistance to heat and moisture during certain printing or converting processes may limit its use in some high-volume, visually intensive applications.

Country-Wise Outlook

U.S. Greaseproof Paper Market Advances with Regulatory Support and Packaging Innovation

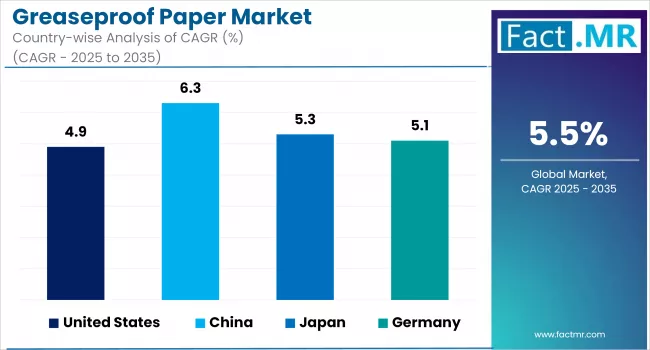

The United States' greaseproof paper market is experiencing steady growth, driven by shifting regulations, evolving consumer preferences, and the expansion of the food service sector. Increasing environmental regulations and state-level mandates promoting compostable and PFAS-free packaging are encouraging quick-service restaurants and food delivery platforms to adopt grease-resistant paper alternatives over traditional plastics. The rise in home baking and retail demand for eco-friendly kitchen essentials has further accelerated usage in household applications.

Manufacturers are responding with innovations such as unbleached, fluorocarbon-free variants and enhanced coatings that offer better grease and moisture resistance while meeting safety standards. Custom-printed greaseproof paper is also gaining popularity among restaurants and cafes as a branding tool, reflecting broader trends in premium packaging and consumer engagement.

While the market continues to face limitations in barrier performance under high-heat or moisture-heavy conditions, ongoing investment in material technology is helping address these constraints. Overall, the U.S. remains a key driver of innovation and adoption in the global greaseproof paper landscape.

China’s Greaseproof Paper Market Gains Momentum Amid Sustainability Push

China’s greaseproof paper market is gaining significant traction, driven by the country’s rapidly expanding food delivery industry, increasing environmental regulations, and a nationwide effort to reduce plastic waste. As urban populations grow and digital food platforms scale rapidly, the need for safe, oil-resistant, and convenient food packaging continues to rise.

Government policies promoting biodegradable materials have encouraged both domestic and international food service chains to adopt greaseproof paper for wrapping snacks, baked goods, and takeaway meals. Manufacturers are also shifting toward PFAS-free and fluorocarbon-free alternatives to meet evolving safety and compliance standards.

China’s large-scale paper production infrastructure allows for cost-effective, high-volume output, positioning the country as both a key consumer and exporter of greaseproof packaging materials. Additionally, increasing interest in eco-friendly solutions among Chinese consumers is reinforcing demand for compostable and unbleached variants.

Japan Drives Innovation in Greaseproof Paper with Quality and Safety Focus

Japan’s greaseproof paper market is advancing through a combination of consumer preferences, regulatory measures, and manufacturing excellence. High standards for food safety and hygiene in both domestic households and food service outlets are reinforcing demand for grease-resistant, PFAS-free packaging solutions. The popularity of takeout, convenience foods, and premium bakery products has led to the increased use of greaseproof paper liners and wrappers.

Manufacturers in Japan are responding by introducing unbleached, chlorine-free, and fluorocarbon-free variants that align with health regulations and consumer expectations. They are also investing in advanced coating technologies such as silicone and nano-cellulose layers to enhance oil and moisture resistance without compromising recyclability or compostability.

Leading Japanese firms, such as Mitsubishi Paper, Oji Paper, and Nippon Paper Industries, are expanding their product lines to support eco-conscious packaging trends. Custom printing and branding for cafes and bakeries have become common, reflecting a shift toward value-added, premium packaging experiences.

Overall, Japan remains at the forefront of greening the greaseproof paper industry, combining high-performance materials with strict quality standards and sustainability commitments.

Category-wise Analysis

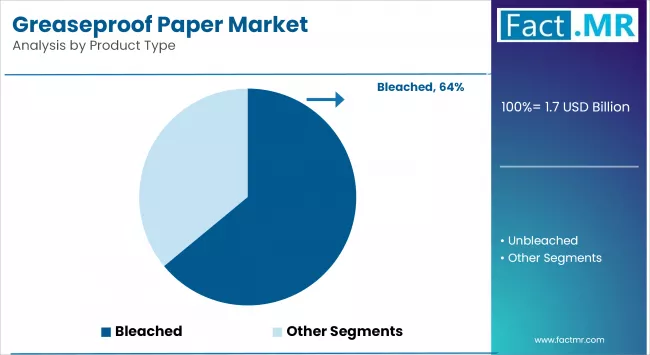

Bleached greaseproof paper to Exhibit Leading Share by Product Type

Bleached greaseproof paper continues to lead the market by product type, favored for its smooth finish, high printability, and consistent visual appeal, qualities that make it widely preferred in retail food packaging and branded applications. It is extensively used by bakeries, fast-food chains, and confectionery brands for wrapping items like sandwiches, pastries, and sweets, where clean presentation and product visibility are critical to consumer perception.

The bright, white surface of bleached paper enhances branding through high-quality custom printing, enabling clear logos, promotional graphics, and ingredient labeling important in competitive food service environments. Despite the rise in demand for unbleached and eco-labeled alternatives, bleached variants remain in demand due to their familiarity, versatility, and availability across both industrial and retail channels.

In emerging economies, where sustainability standards are still evolving, bleached greaseproof paper remains the standard choice due to its cost-efficiency and broad acceptance. Additionally, technological advancements in chlorine-free and oxygen-bleached processing are helping reduce the environmental impact traditionally associated with whitening treatments, making modern bleached options aligned with global sustainability goals.

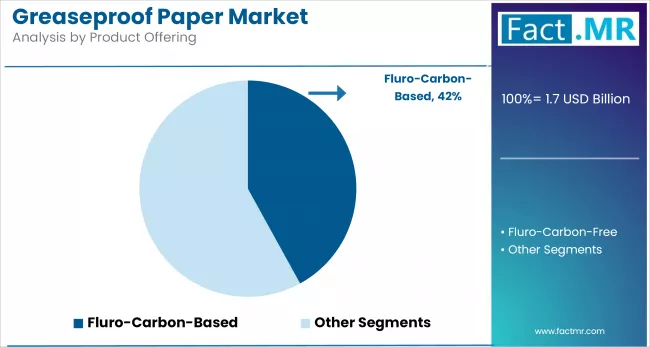

Fluro-Carbon-Free to Exhibit Leading Share by Product Offering

Fluorocarbon-free greaseproof paper is poised to capture a leading share of the market, driven by rising regulatory scrutiny and growing consumer awareness of the health and environmental risks associated with per- and polyfluoroalkyl substances (PFAS). As governments worldwide tighten restrictions on PFAS in food-contact materials in regions such as the European Union, Canada, and U.S. states, demand is shifting rapidly toward safer, compliant alternatives.

Food service operators, bakery chains, and packaged food brands are increasingly adopting fluorocarbon-free paper to align with evolving safety standards and clean-label packaging trends. This product segment is also benefiting from strong uptake among organic and natural food producers, who require packaging that reflects their sustainability positioning and avoids chemical additives.

Manufacturers are responding with advanced formulations that use alternative barrier coatings such as silicon, clay, and biodegradable biopolymer blends. These innovations provide effective grease and moisture resistance without compromising compostability or recyclability, which are critical factors in both regulatory approval and brand differentiation.

40-80 GSM to Exhibit Leading Share by Weight

Greaseproof paper in the 40-80 GSM range is expected to dominate the market by weight category due to its ideal balance of durability, flexibility, and cost-effectiveness. This weight range is widely used across bakery, food service, and retail packaging applications where moderate barrier strength and easy handling are required.

Products in this GSM category offer sufficient resistance to oil and moisture while remaining lightweight enough for efficient wrapping, folding, and storage. Bakeries commonly use 40-60 GSM sheets for lining trays and wrapping pastries, while quick-service restaurants favor 60-80 GSM paper for sandwich wraps, burger liners, and takeaway applications that demand both strength and grease holdout.

In addition to functional benefits, papers within this weight range are also cost-efficient and compatible with a variety of printing techniques, making them a preferred choice for branded and custom packaging. Their widespread availability and suitability for automated converting processes further support their continued use in large-scale food packaging operations.

Food Packaging to Exhibit Leading Share by Application

Food packaging remains the primary application segment for greaseproof paper, accounting for the majority of its global consumption. Its widespread use is driven by increasing demand for sustainable, oil-resistant materials across fast food, bakery, confectionery, and ready-to-eat meal segments.

Quick-service restaurants and food delivery platforms rely heavily on greaseproof paper for wrapping burgers, sandwiches, fries, and fried snacks due to its ability to maintain product integrity and minimize leakage. In the bakery sector, it is used extensively to line baking trays, wrap pastries, and package artisanal bread, where both hygiene and presentation are critical.

Confectionery manufacturers also use greaseproof paper to wrap chocolates and candy, where oil migration needs to be controlled. The shift away from plastic and wax-coated paper toward compostable and PFAS-free options has further increased the appeal of greaseproof paper in retail food packaging.

Additionally, the rise in pre-packed and grab-and-go food formats in urban markets, combined with regulatory support for biodegradable packaging, continues to fuel growth. Food processors and retailers are increasingly choosing greaseproof paper for primary and secondary packaging, especially when looking to meet sustainability goals without compromising product protection or branding flexibility.

Fast Foods to Hold Leading Share in Greaseproof Paper Market by End-Use

Fast food remains the largest end-use segment for greaseproof paper, driven by the growing demand for takeaway, drive-thru, and delivery services worldwide. Used extensively for wrapping burgers, sandwiches, and fried items, greaseproof paper offers essential oil resistance, hygiene, and convenience.

Quick-service restaurants are adopting branded, PFAS-free, and recyclable paper to meet both regulatory requirements and consumer expectations for sustainable packaging. As global fast food chains expand, especially in urban and emerging markets, the need for functional, eco-friendly wrapping solutions continues to rise, securing the sector’s dominant share in the greaseproof paper market.

Europe holds the Leading Share in the Greaseproof Paper Market

Europe holds the leading share in the greaseproof paper market, driven by strict environmental regulations, advanced recycling infrastructure, and high consumer demand for sustainable packaging. Countries like Germany, France, and the UK have widely adopted greaseproof paper in the food service and bakery sectors due to EU bans on single-use plastics and growing restrictions on PFAS.

Local manufacturers are expanding production of unbleached, chlorine-free, and fluorocarbon-free variants to meet regulatory and market expectations. With a strong base in premium baked goods and custom-branded packaging, Europe remains a key driver of innovation and supply in the global greaseproof paper industry.

Competitive Analysis

The greaseproof paper market is highly competitive, with key players including Nordic Paper, Ahlstrom-Munksjö, Delfortgroup, Metsä Group, and Domtar Corporation leading through innovation, sustainability, and strong global distribution. These companies are investing in PFAS-free and recyclable solutions to meet evolving regulatory and consumer demands.

Regional manufacturers such as Pudumjee Paper Products, KRPA Paper Inc., and Fujian Naoshan Paper Industry Group are expanding their presence in Asia and Europe with cost-effective, high-volume offerings. Niche players like The Griff Network and VICAT Cortec Corporation serve specialized applications, including industrial and medical packaging.

With increasing focus on eco-friendly materials, printability, and product safety, companies are enhancing R&D and forming strategic partnerships to maintain a competitive edge in a rapidly shifting packaging landscape.

Recent Development

- In 2023, Nordic Paper acquired a pulp production facility in Sweden to secure raw material supply and strengthen greaseproof paper production capacity.

- In 2024, Ahlstrom-Munksjö expanded its European footprint by acquiring a specialty paper mill with the strategic goal of increasing the output of non-stick, eco-friendly packaging. This move aligns with the company's emphasis on sustainable specialty materials and innovation in fiber-based packaging.

Segmentation of Greaseproof Paper Market

-

By Product Type :

- Bleached

- Unbleached

-

By Product Offering :

- Fluro-Carbon-Based

- Fluro-Carbon-Free

-

By Weight :

- <40 GSM

- 40-80 GSM

- >80 GSM

-

By Application :

- Baking/Cooking

- Food Packaging

- Paper Bags

- Wrapping Paper

- Laminating Base Paper

- Microflute Paper

- Clamshells

- Others

-

By End Use :

- Confectionary

- Poultry

- Fresh Produce

- Fast Foods

- Others

-

By Region :

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- MEA

- Frequently Asked Questions -

What is the Global Greaseproof Paper Market Size in 2025?

The greaseproof paper market is valued at USD 1.7 billion in 2025.

Who are the Major Players Operating in the Greaseproof Paper Market?

Prominent players in the greaseproof paper market include Nordic Paper, Ahlstrom-Munksjö, Delfortgroup, Dispapali, Domtar Corporation, and others.

What is the Estimated Valuation of the Greaseproof Paper Market by 2035?

The greaseproof paper market is expected to reach a valuation of USD 2.9 billion by 2035.

What Value CAGR Did the Greaseproof Paper Market Exhibit over the Last Five Years?

The historic growth rate of the greaseproof paper market was 3.5% from 2020-2024.

Author:

S.N. Jha

Editor:

Naved Ahmed