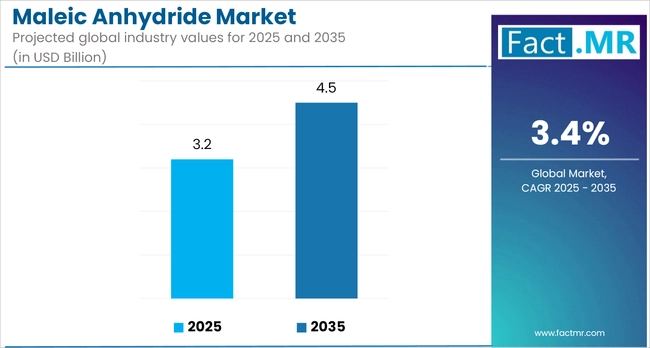

Maleic Anhydride Market Outlook (2025 to 2035)

The global maleic anhydride market is projected to increase from USD 3.2 billion in 2025 to USD 4.5 billion by 2035, with an annual growth rate of 3.4%, driven by rising demand for unsaturated polyester resins (UPRs) and 1,4-butanediol (BDO) across the construction, automotive, and industrial coatings sectors.

With the increasing shift toward lightweight materials and corrosion-resistant composites, the role of maleic anhydride as a key chemical intermediate continues to gain strategic importance in global manufacturing ecosystems.

What are the Drivers of Maleic Anhydride Market?

The global maleic anhydride market is experiencing steady growth, primarily driven by increasing demand from key end-use industries, including construction, automotive, and packaging. One of the major growth drivers is the increasing consumption of unsaturated polyester resins (UPRs), where maleic anhydride serves as a key raw material. These resins are extensively used in lightweight composite materials, which are gaining popularity in automotive and infrastructure applications due to their durability and corrosion resistance.

Additionally, the growing production of 1,4-butanediol (BDO), used in high-performance plastics, elastomers, and as a solvent, is further fueling demand. Urbanization and infrastructure development in emerging economies, particularly in the Asia-Pacific and Latin America regions, are also contributing to the higher consumption of adhesives, coatings, and construction chemicals derived from maleic anhydride.

Moreover, increasing focus on sustainability has prompted investments in bio-based production technologies, aligning with stricter environmental regulations and shifting consumer preferences. Collectively, these factors are positioning maleic anhydride as a critical material in multiple high-growth industrial applications.

What are the Regional Trends of Maleic Anhydride Market?

The maleic anhydride market exhibits diverse regional dynamics, influenced by industrial demand, feedstock availability, and regulatory frameworks.

The Asia-Pacific region is currently the most prominent, driven by strong demand in countries such as China, India, and South Korea. This growth is supported by the expansion of end-use sectors, including construction, automotive, and electronics. China, in particular, is a major producer and consumer, benefiting from integrated petrochemical operations and rising consumption of unsaturated polyester resins (UPR) and 1,4-butanediol (BDO). India’s growing infrastructure and plastics industries are also fueling the uptake of maleic anhydride derivatives.

North America maintains a steady demand, largely centered in the United States. The region benefits from access to cost-effective natural gas-based feedstocks, such as n-butane, which gives producers a competitive edge. Applications in agriculture, coatings, and automotive parts primarily drive the U.S. market. Additionally, domestic investment in renewable chemical alternatives could gradually reshape demand patterns.

Europe, while mature, is experiencing modest growth. Environmental regulations and a strong push for sustainable production practices are influencing market strategies. Countries like Germany, France, and Italy continue to rely on maleic anhydride in resin production for automotive, marine, and industrial coatings. However, competition from bio-based alternatives and high energy costs are pressing concerns for producers.

Latin America shows emerging potential, with Brazil and Mexico witnessing increased industrial activity and infrastructure development. The use of UPR in construction and composite materials is growing gradually, with maleic anhydride consumption in the region also increasing.

In the Middle East and Africa, market development is at an earlier stage but is supported by investments in petrochemical infrastructure. The region’s access to abundant feedstock and growing focus on diversifying beyond oil are expected to create new growth avenues for maleic anhydride applications in the near future.

Overall, regional trends reflect a mix of mature demand, feedstock advantages, and evolving regulatory and sustainability pressures that continue to shape the global maleic anhydride market.

What are the Challenges and Restraining Factors of Maleic Anhydride Market?

The maleic anhydride market faces structural and operational challenges that could impede its growth trajectory across key regions. One of the foremost constraints is the volatility in raw material prices, particularly n-butane and benzene, which are crucial feedstocks for maleic anhydride production. Fluctuations in global oil and gas prices directly impact production costs and margins, making it challenging for manufacturers to maintain stable pricing and secure long-term contracts.

Environmental and regulatory pressures are also intensifying. In regions such as Europe and North America, stricter emission norms and sustainability mandates are compelling producers to adopt cleaner technologies. However, transitioning to low-emission or bio-based production routes often involves high capital investment and longer approval timelines. This creates a barrier for small and mid-sized manufacturers that may lack the resources for large-scale modernization.

Health and safety concerns related to the handling and storage of maleic anhydride, a reactive and irritant chemical, further complicate logistics and regulatory compliance, especially in densely populated or heavily regulated markets.

Market saturation in mature regions is another challenge. In the U.S. and parts of Europe, demand for maleic anhydride in applications such as unsaturated polyester resins has plateaued, with limited room for expansion. In these areas, competition from substitutes such as bio-based succinic acid and other eco-friendly intermediates is gradually gaining traction, particularly among environmentally conscious manufacturers.

Lastly, global supply chain disruptions triggered by geopolitical tensions, trade policy shifts, and port delays have impacted the timely delivery of raw materials and finished products. This has compelled producers to reassess their sourcing strategies and consider regional diversification to mitigate risks.

Collectively, these factors underscore the importance of innovation, regulatory foresight, and operational resilience for companies aiming to remain competitive in the global maleic anhydride market.

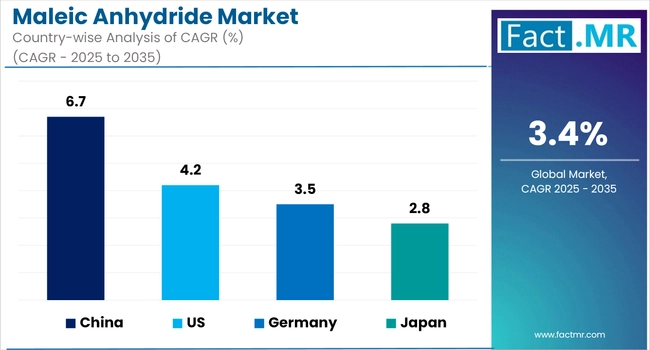

Country-Wise Outlook

United States Maleic Anhydride Market Sees Growth Primarily Fueled by Rising Demand for Sustainable and High-Performance Materials Across Industries

The United States maleic anhydride market is experiencing sustained growth, largely driven by increasing demand from key downstream industries, including construction, automotive, and marine manufacturing. The increased consumption of unsaturated polyester resins (UPR), which are extensively used in reinforced plastics, coatings, and fiberglass, is a major factor. The surge in infrastructure projects and commercial construction elevated UPR usage, thereby driving the demand for maleic anhydride as a core feedstock.

Additionally, the automotive sector’s focus on producing lightweight, fuel-efficient vehicles has accelerated the adoption of composite materials made from UPRs and other thermosetting polymers. Maleic anhydride plays a crucial role in these formulations, providing the mechanical strength and chemical resistance necessary for vehicle components, such as bumpers, panels, and internal parts.

The market is also benefiting from advancements in production processes, particularly the shift toward n-butane-based oxidation routes, which offer improved yields and cost efficiency compared to traditional benzene-based methods. This transition is enabling U.S.-based manufacturers to optimize operational margins and effectively meet growing domestic demand.

Moreover, the push for localized supply chains and strategic stockpiling of chemical intermediates post-pandemic has encouraged regional production expansion, supported by regulatory incentives for chemical manufacturing in select states. Collectively, these factors underscore the strengthening trajectory of the maleic anhydride market in the USA, positioning it as a key hub for both production and consumption over the next decade.

China Witnesses Propelled By Its Expansive Industrial Base and Increasing Demand Across Key Sectors Such as Automotive, Construction, and Electronics

China's maleic anhydride market is experiencing dynamic growth, driven by its extensive industrial base and rising demand across key sectors, including automotive, construction, and electronics. The material is integral to the production of unsaturated polyester resins (UPR) and 1,4-butanediol (BDO), which are essential for manufacturing reinforced plastics, coatings, and synthetic fibers.

Recent years have seen a noticeable shift toward industrial consolidation. Large-scale producers have expanded capacity, while smaller, less competitive players have exited the market. This trend reflects the broader push toward efficiency and economies of scale in China’s chemical manufacturing landscape. Major investments such as those by Puyang Shengyuan and other integrated producers are reshaping regional production capabilities and supporting a vertically integrated supply chain.

However, the rapid expansion has introduced challenges, particularly in terms of overcapacity and underutilization. New MA-BDO integrated projects have added output, but downstream demand has not always kept pace. This mismatch has led to intensified price competition and margin pressures, prompting manufacturers to aggressively explore export markets.

At the same time, China is advancing its sustainability and environmental compliance frameworks. These efforts are prompting MA producers to upgrade technology and adopt cleaner production processes, which may increase operational costs but align with long-term policy goals.

Overall, China remains a critical force in the global maleic anhydride market, driven by industrial scale, technological investments, and evolving environmental standards. Future growth will depend on striking a balance between capacity expansion and stable demand, while also advancing production efficiency.

Japan is evolving rapidly, fueled by industrial modernization

Japan’s maleic anhydride market is evolving rapidly, fueled by industrial modernization and strong demand from the automotive and electronics industries. Manufacturers have ramped up R&D efforts, particularly focusing on bio-based variants and digitalized production methods, to improve sustainability and competitiveness. In 2023, unsaturated polyester resins remained the dominant application, while 1,4-butanediol showed the fastest growth, reflecting diversified end-use.

Imports have also increased, with over 4,700 tonnes sourced in 2023 from suppliers like South Korea and Malaysia. On the export side, volumes increased by 15% in 2022, with China emerging as the primary destination, underscoring strong regional trade integration. As Japan advances with environmental regulations and industrial innovation, the maleic anhydride sector is poised for steady growth.

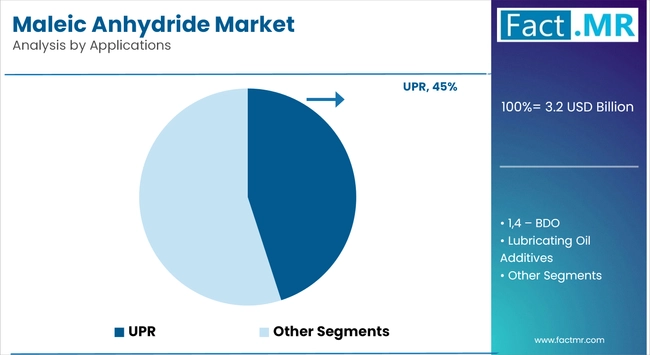

Category-wise Analysis

Lubricating Oil Additives to Exhibit Leading Share Among Application

Lubricating oil additives continue to dominate the maleic anhydride market, driven by their essential role in enhancing lubricant performance. These additives are widely used to improve oxidation resistance, dispersancy, and acidity control in engine oils, industrial lubricants, and metalworking fluids. For instance, products like polyisobutylene succinimide (PIBSI) and succinic esters derived from maleic anhydride are industry standards for tackling soot and sludge in modern diesel engines and to protect high-performance gear and hydraulic systems.

This leadership is further supported by increasing demand from the automotive and heavy machinery sectors, where superior engine protection and extended drain intervals are critical. In industrial applications, maleic-derived additives help maintain machinery performance under high-temperature and high-pressure conditions, reducing downtime and maintenance costs. Additionally, as equipment manufacturers and regulators push for improved fuel economy and lower emissions, the use of advanced lubricating additives has become standard practice.

Technological progress in additive formulation, such as tailoring molecular structures for specific applications, also adds value. These innovations not only enhance lubricant lifespan but also support sustainability by enabling longer oil change intervals and lowering waste. As such, the lubricating oil segment is expected to remain the primary driver of maleic anhydride consumption, supported by its enduring value across a wide range of demanding applications.

n-butane Category to Hold Leading Share in Maleic Anhydride Market by Raw Material

The n‑butane category serves as the primary feedstock for maleic anhydride production, and its dominance is well‑justified on multiple fronts. From an operational standpoint, n‑butane offers a highly efficient catalytic conversion process: one ton of n‑butane typically yields one ton of maleic anhydride, whereas benzene-based methods are costlier and less efficient.

Economically, n-butane enjoys an edge because its price remains lower than that of benzene, and its processing generates fewer hazardous by-products, aligning with tighter environmental regulations.

Additionally, n-butane is deeply integrated into modern petrochemical infrastructure. Refineries often incorporate n-butane oxidation units that co-generate maleic anhydride, along with other valuable by-products, thereby enhancing overall energy and resource efficiency. As stricter benzene controls come into effect, n‑butane’s environmental compliance and economic advantages ensure it remains the preferred raw material for maleic anhydride production.

North America Hold Leading Share in Maleic Anhydride Market

A combination of advanced production infrastructure, diversified industrial demand, and consistent investment in high-performance chemical technologies underpins North America's position in the maleic anhydride market. The region benefits from a mature chemical manufacturing sector, particularly in the United States, where maleic anhydride is widely used in the production of unsaturated polyester resins (UPR), coatings, and lubricating oil additives.

In the USA, demand is largely driven by applications in the construction and automotive industries. Maleic anhydride-based resins are used in fiberglass-reinforced plastics for construction panels, automotive body parts, and marine components. The growing focus on lightweight and durable composite materials has bolstered consumption. Similarly, the rise in electric vehicle (EV) adoption has spurred demand for high-performance resins and specialty chemicals, further expanding the market.

Mexico is emerging as a growth hub within the region, supported by its expanding automotive manufacturing base and increasing consumption of synthetic lubricants. Local demand for maleic anhydride in additive formulations is growing steadily, as OEMs and aftermarket suppliers shift toward performance-enhancing and emissions-reducing lubricants.

Additionally, North America maintains a competitive edge due to its focus on n-butane-based maleic anhydride production. This route offers greater efficiency and environmental benefits compared to older benzene-based processes. Continuous investments in process optimization and sustainability, especially among USA producers, support long-term cost competitiveness and regulatory compliance.

In summary, North America’s leadership in the maleic anhydride market is supported by robust industrial demand, especially in construction, automotive, and lubrication sectors, as well as technological innovation and supply chain integration. The region remains strategically positioned for sustained growth amid evolving global industrial trends.

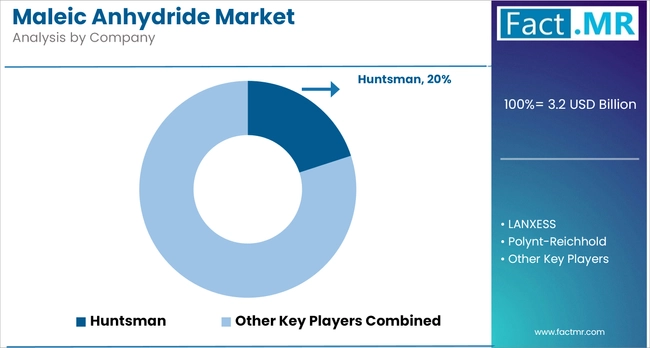

Competitive Analysis

Key players in the maleic anhydride market are advancing the industry through a mix of strategic initiatives, including product innovation, capacity expansions, and geographic diversification. Companies such as Huntsman Corporation and LANXESS AG are expanding their portfolios to meet demand in high-performance applications, including unsaturated polyester resins, lubricating oil additives, and automotive coatings.

In Asia, firms such as Nippon Shokubai Co., Ltd. and Mitsubishi Chemical Corporation are capitalizing on the growing demand for lightweight composites and reinforced materials, particularly in the electronics and infrastructure sectors. Ashland Inc. continues to serve niche markets in North America, offering customized formulations for marine and industrial uses.

Meanwhile, CEPSA and Thirumalai Chemicals Ltd. are expanding their export capacities to strengthen their foothold in emerging markets across Latin America, Africa, and Southeast Asia. Companies such as DSM N.V. are focusing on sustainable chemistry, integrating maleic anhydride into eco-friendly polymers aligned with circular economy goals. These players collectively shape market dynamics by responding to both industrial demand and environmental imperatives.

Recent Development

- In 2025, Huntsman Corporation concluded its strategic review of its European Maleic Anhydride operations and will proceed with the closure of its manufacturing facility in Moers, Germany. The shutdown is expected to be finalized by the end of the current quarter. In 2024, this segment posted an adjusted EBITDA loss of roughly USD 10 million. Moving forward, Huntsman plans to supply its European customers from its existing facilities in Pensacola, Florida, and Geismar, Louisiana. As a result of the closure, the company anticipates recording a one-time, non-cash asset impairment charge of approximately USD 75 million in the second quarter of 2025.

- In 2024, Thirumalai introduced an eco-friendly maleic anhydride grade for the coatings industry, offering up to 30% improved adhesion and reduced emissions during application.

Segmentation of Maleic Anhydride Market

-

By Raw Material :

- n-butane

- Benzene

-

By Application :

- UPR

- 1,4 - BDO

- Lubricating Oil Additives

- Copolymers

- Others

-

By Region :

- North America

- Latin America

- Europe

- Asia Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the Global Maleic Anhydride Market Size in 2025?

The maleic anhydride market is valued at USD 3.2 billion in 2025.

Who are the Major Players Operating in the Maleic Anhydride Market?

Prominent players in the maleic anhydride market include Huntsman Corporation, LANXESS AG, Nippon Shokubai Co., Ltd., Mitsubishi Chemical Corporation, Ashland Inc., and among others.

What is the Estimated Valuation of the Maleic Anhydride Market by 2035?

The maleic anhydride market is expected to reach a valuation of USD 4.5 billion by 2035.

What Value CAGR Did the Maleic Anhydride Market Exhibit over the Last Five Years?

The historic growth rate of the maleic anhydride market was 4.0% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed