Gas Detection Equipment Market Outlook (2025 to 2035)

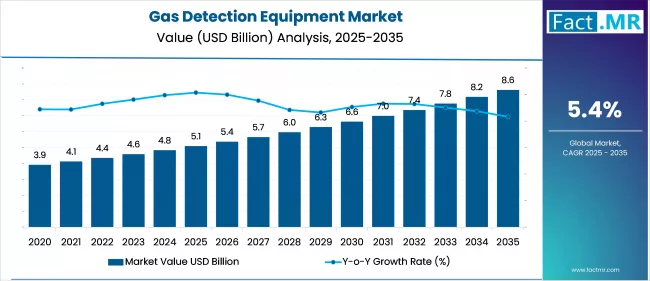

The global gas detection equipment market is projected to increase from USD 5.1 billion in 2025 to USD 8.6 billion by 2035, with a CAGR of 5.4% during the forecast period. Growth is driven by rising industrialization and the expansion of hazardous workplaces. Stringent government safety regulations are compelling industries to adopt advanced gas detection systems.

What are the Drivers of Gas Detection Equipment Market?

The gas detection equipment market is witnessing robust growth, primarily driven by stringent regulatory frameworks and heightened safety standards across industrial sectors. Governments and regulatory bodies such as OSHA, ATEX, and the European Commission have enforced strict guidelines mandating the use of gas detection systems in facilities handling toxic, flammable, or oxygen-depleting gases.

These regulations are particularly rigorous in sectors such as oil & gas, chemicals, and mining, where worker safety and accident prevention are of critical importance. The increasing frequency of gas-related industrial incidents has further emphasized the importance of such equipment, prompting organizations to adopt it early to ensure compliance and avoid operational liabilities.

Technological advancements are playing a transformative role in the evolution of gas detection equipment. Innovations such as laser-based sensors, infrared spectroscopy, and wireless, IoT-enabled devices are enhancing the precision, durability, and connectivity of gas detectors.

Integration with smart systems and cloud-based platforms enables real-time data collection, predictive maintenance, and remote monitoring, making the systems more intelligent and efficient. These advancements not only improve safety outcomes but also reduce downtime and operational costs, making them attractive investments for industries undergoing digital transformation.

Growing environmental concerns and global efforts to reduce greenhouse gas emissions are accelerating the adoption of gas detection systems. Industries are under pressure to monitor emissions and leaks of harmful gases, such as methane and carbon dioxide, from both regulatory and sustainability perspectives.

The demand for continuous emissions monitoring, especially in power plants, refineries, and landfill sites, is creating new market opportunities. Combined with the expansion of smart infrastructure and smart cities, where gas monitoring is integrated into building management systems, the gas detection equipment market is poised for sustained growth in the coming years.

What are the Regional Trends of Gas Detection Equipment Market?

The North American gas detection equipment market is characterized by its maturity, regulatory stringency, and high technological adoption. The U.S. and Canada have established comprehensive safety frameworks led by organizations such as OSHA, NFPA, and EPA, which mandate the use of gas detection systems in hazardous environments. Industries such as oil & gas, chemicals, and manufacturing dominate demand, especially for both fixed and portable detectors.

Moreover, the region is a leader in integrating smart technologies, such as wireless connectivity, IoT, and AI, into gas monitoring systems, enabling real-time detection and predictive maintenance. This advanced technological landscape continues to strengthen North America's global market position.

In Europe, the market is driven by stringent environmental and occupational safety regulations enforced by entities such as the European Union under ATEX, REACH, and the Industrial Emissions Directive (IED). Countries like Germany, the U.K., France, and the Netherlands have a strong focus on minimizing workplace hazards and reducing industrial emissions.

European industries are among the early adopters of cutting-edge gas detection technologies, particularly in sectors such as energy, wastewater management, and manufacturing. With rising awareness of carbon neutrality and climate commitments, the region is also experiencing a growing demand for emission monitoring equipment to track gases such as methane and CO₂, which further stimulates market growth.

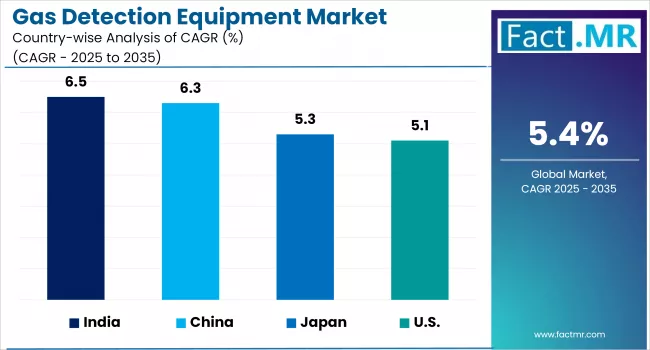

Asia Pacific region is emerging as the fastest-growing market due to its rapid industrialization, expanding energy infrastructure, and increasing emphasis on worker safety. Major economies such as China, India, Japan, and South Korea are experiencing strong growth in process industries, construction, and urban infrastructure, all of which necessitate effective gas detection solutions.

Although regulatory enforcement varies across countries, increasing government focus on workplace safety and environmental protection is improving adoption rates. Moreover, the region is witnessing growing interest in portable and wireless gas detectors, especially in confined spaces and construction zones, as industries modernize and safety awareness increases.

In the Middle East, the gas detection market is developing steadily, fueled primarily by the oil & gas, mining, and utility sectors. In the Middle East, countries such as Saudi Arabia, the UAE, and Qatar are investing in petrochemical and energy infrastructure, where fixed and portable detectors are crucial for leak detection and worker safety.

What are the Challenges and Restraining Factors of Gas Detection Equipment Market?

One of the primary restraints is the high upfront cost of advanced gas detection systems. Sophisticated equipment, especially that with smart features such as real-time monitoring, wireless connectivity, and multi-gas detection, can be prohibitively expensive for small and medium-sized enterprises (SMEs) to adopt. Additionally, ongoing maintenance, calibration, and sensor replacement costs can further strain operational budgets, particularly in price-sensitive markets. This cost barrier often leads to delayed or partial implementation, particularly in developing regions.

Another major restraint is the lack of uniform regulatory enforcement in developing economies. While developed countries have well-established occupational health and safety regulations mandating gas detection systems in hazardous environments, many developing nations either lack such regulations or fail to enforce them effectively.

This leads to inconsistent adoption across industries, despite the presence of similar risks. In some regions, limited awareness of gas hazards and insufficient government oversight result in industries not prioritizing the installation of gas detection equipment, thereby slowing market penetration.

Technical challenges also pose significant obstacles to market growth. Despite improvements in sensor technologies, gas detection systems can suffer from false alarms, sensor drift, or failure under extreme environmental conditions such as high humidity, corrosive atmospheres, or fluctuating temperatures. These limitations may reduce the reliability of detection systems in critical situations. Additionally, the complexity of integrating these systems into existing industrial automation and monitoring platforms can deter end-users who lack the necessary technical expertise or resources for customization.

A shortage of skilled personnel trained to install, operate, and maintain gas detection equipment is a persistent issue, especially in emerging markets. Without adequate training, workers may misinterpret warnings, neglect necessary maintenance, or misuse the devices, compromising safety and reducing the effectiveness of the investment. This skills gap can limit the widespread deployment and long-term performance of gas detection systems.

Country-Wise Outlook

U.S. Gas Detection Equipment Market sees Growth Driven by Strict Regulatory Environment

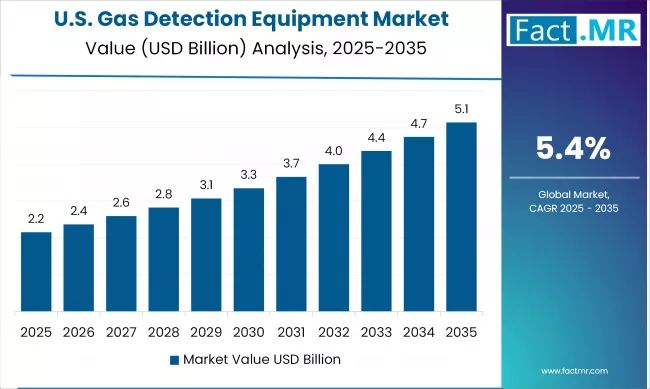

The gas detection equipment market in the U.S. is experiencing strong and consistent growth, driven by a combination of strict regulatory compliance, technological innovation, and rising industrial safety demands. Federal regulations from agencies such as the Occupational Safety and Health Administration (OSHA), the Environmental Protection Agency (EPA), and the Department of Energy are key in enforcing the use of gas detection systems across hazardous work environments.

One of the main driving factors is the strict regulatory environment. U.S. industries, particularly those in oil & gas, chemical processing, and mining, are required to implement comprehensive gas monitoring systems to detect hazardous gases such as methane, carbon monoxide, hydrogen sulfide, and VOCs.

In 2023 and 2024, government-led initiatives focusing on methane leak detection and emissions monitoring have gained traction, encouraging further adoption of advanced detection technologies. These include funding for energy infrastructure upgrades, as well as policy mandates aligned with the Biden administration's climate goals, pushing industries to prioritize emission control and workplace safety.

Another critical growth factor is the rapid adoption of portable and smart gas detection devices. Portable gas detectors are the fastest-growing product category in the U.S., driven by the need for flexible and real-time monitoring in confined spaces, remote worksites, and emergency response scenarios.

The integration of IoT, wireless connectivity, and AI-based analytics in these devices enables predictive maintenance and real-time alerts, which improve safety and operational efficiency. Moreover, advances in semiconductor-based and electrochemical sensor technologies are making gas detectors more reliable, durable, and responsive, further boosting the gas detection equipment market.

China witnesses Rapid Market Growth Backed by Rapid Industrialization

China’s gas detection equipment market is expanding faster, driven by strong industrial growth and rising safety standards. The key driver behind this growth is the rapid industrialization and infrastructure development, particularly in the energy, chemicals, and construction sectors.

China’s push for modernization in petrochemical plants, LNG terminals, and heavy industries has created persistent demand for advanced gas monitoring technologies. Moreover, government-led industrial safety initiatives, including the 2014 Work Safety Law and emissions control plans, have increased mandatory usage of gas detection systems in high-risk environments.

Another pivotal factor is technological innovation and local manufacturing momentum. Chinese and international OEMs are forging partnerships to introduce IoT-enabled, AI-powered detectors tailored for domestic applications. Players such as Teledyne, Siemens, Honeywell, ABB, and local firms are launching cost-effective, purpose-built solutions that comply with global standards, supporting both large-scale plants and SME requirements.

Environmental and ESG pressures are driving organizations to enhance their monitoring of greenhouse and toxic emissions. As China prioritizes cleaner air under its national policies, continuous emissions monitoring systems (CEMS) and methane leak detection equipment are being increasingly implemented in industrial sites. Consequently, demand extends beyond traditional workplace safety to encompass environmental compliance, reinforcing the market’s double-digit growth trajectory.

Japan sees Precision Manufacturing Fuels Demand for Ultra-Pure Piping

The growth of the gas detection market in Japan is driven by stringent workplace safety and environmental regulations enforced by Japanese authorities. Regulatory bodies require gas monitoring in industries such as oil & gas, chemicals, and manufacturing, ensuring compliance with national safety standards. Rising awareness of indoor air quality and emissions has increased adoption in healthcare, residential spaces, and smart building applications. This regulatory and environmental impetus is encouraging companies to invest in reliable detection technologies.

Technological innovation is also enabling market expansion. Japan’s advanced industrial ecosystem has fostered the development and deployment of IoT-enabled, wireless, and AI-integrated gas detection solutions. Local and global manufacturers, including ABB, Honeywell, and Siemens, are introducing sensor systems tailored for Japan’s high standards and operational needs. Furthermore, advancements in sensor technology, such as semiconductor and infrared sensors, offer higher accuracy, improved durability, and reduced maintenance, making adoption more viable for end-users.

Emerging demand in portable detectors complements fixed installations. With portable devices recognized as the fastest-growing segment, Japan’s workforce in sectors like construction, confined-space operations, and emergency response is increasingly relying on mobile monitoring. Combined with broader industrial automation trends and a focus on ESG compliance, the market is well-positioned for sustained double-digit growth through 2030.

Category-wise Analysis

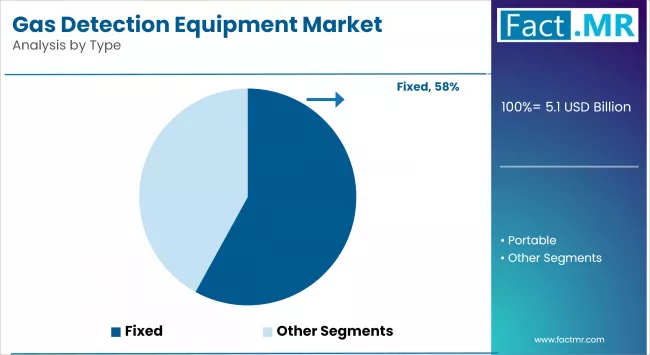

Fixed Gas Detection Systems to Exhibit Leading by Type

Fixed gas detection systems dominate the global gas detection equipment market, holding the largest revenue share. These systems are widely used in industrial facilities such as oil & gas plants, chemical manufacturing units, refineries, and wastewater treatment facilities, where continuous and real-time monitoring is critical for detecting hazardous gas leaks.

The dominance of fixed systems is primarily driven by their high reliability, ability to cover large areas, and integration with automated safety systems such as alarms, ventilation controls, and emergency shutdowns. Regulatory requirements across many countries also mandate the installation of fixed detectors in high-risk zones, reinforcing their widespread adoption.

Portable gas detectors are the fastest-growing segment driven by the increasing need for mobility, flexibility, and personal safety in field operations and confined spaces. Workers widely use portable detectors in various sectors, including construction, mining, firefighting, utilities, and emergency response, where fixed systems are not feasible. Technological advancements, including compact designs, multi-gas sensing capabilities, wireless connectivity, real-time data transmission, and integration with mobile apps, have significantly enhanced the usability and appeal of portable detectors.

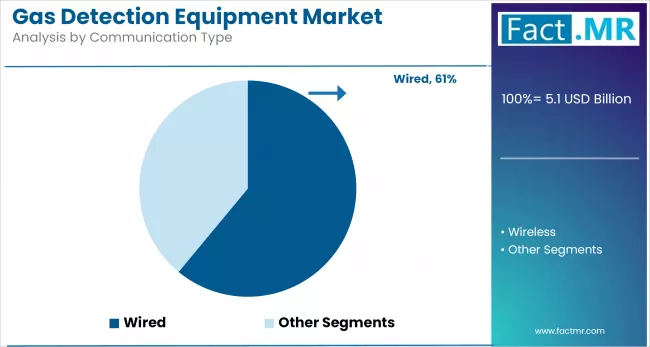

Wired to Exhibit Leading by Communication Type

Wired communication systems hold the largest market share, driven by their reliability, minimal signal interference, and stable data transmission, especially in hazardous or industrial environments. These systems are preferred in legacy setups and large-scale facilities where infrastructure already supports physical wiring, providing consistent performance for monitoring and control applications over extended periods.

Wireless communication is the fastest-growing segment, driven by the need for flexible, scalable, and easy-to-install solutions. Advancements in IoT, along with decreasing costs of wireless technologies, are enabling real-time monitoring in remote or difficult-to-wire locations. Industries seeking digital transformation and reduced installation costs are increasingly turning to wireless systems for improved operational agility.

Oxygen Gas Detection to Exhibit Leading by Gas Type

The toxic gas detection segment currently dominates the gas detection equipment market. Strict occupational health and safety regulations and the high risk of exposure to toxic gases in industrial processes drive the dominance of this segment. Toxic gases are often colorless and odorless, posing serious health hazards even at low concentrations. As a result, industrial facilities are increasingly deploying fixed and portable toxic gas detectors to ensure real-time monitoring and compliance with safety standards, making this the most widely adopted gas type in the market.

The oxygen gas detection segment is expected to register the fastest growth over the forecast period. Oxygen detectors are crucial in environments where oxygen levels can either fall below safe thresholds (causing asphyxiation) or rise to dangerously high levels (increasing flammability risks).

This is particularly important in confined spaces, such as tunnels, tanks, and underground facilities, where oxygen depletion is a common concern. The increasing use of personal safety devices by workers, along with stricter safety protocols in industries such as pharmaceuticals, water treatment, food processing, and laboratory research, is driving the demand for oxygen monitoring equipment.

Electrochemical to Exhibit Leading by Sensor Technology

Electrochemical sensors dominate the sensor technology market due to their high sensitivity, selectivity, and suitability for detecting toxic gases such as CO and H₂S in industrial environments. These sensors are widely used across oil & gas, wastewater, and manufacturing industries for their accuracy, compact design, and lower power consumption, making them a reliable choice for continuous gas monitoring applications.

The infrared sensor segment is experiencing the fastest growth, propelled by its non-contact detection capabilities and durability in harsh conditions. Infrared sensors are being increasingly deployed in high-risk and explosive environments, particularly for detecting hydrocarbon gases. Their long lifespan, resistance to poisoning, and low maintenance requirements make them ideal for critical applications requiring dependable, real-time monitoring.

Oil & Gas to Exhibit Leading by End-Use

The oil & gas industry holds the dominant share in the gas detection equipment market. This segment’s leadership is driven by the inherently hazardous nature of oil and gas exploration, refining, and distribution processes, which involve the frequent handling of combustible and toxic gases such as methane (CH₄), hydrogen sulfide (H₂S), and volatile organic compounds (VOCs).

Strict safety regulations imposed by agencies like OSHA and API, along with increasing emphasis on leak detection and emissions monitoring, have compelled oil & gas companies to install both fixed and portable gas detectors across upstream, midstream, and downstream operations.

The water & wastewater industry is emerging as the fastest-growing end-use segment in the gas detection equipment market. This growth is largely attributed to the increasing need to monitor toxic gases, such as chlorine (Cl₂), hydrogen sulfide (H₂S), ammonia (NH₃), and methane (CH₄), during water treatment, sludge processing, and sewage handling. The sector is increasingly adopting gas detection systems to comply with environmental regulations and protect workers operating in confined spaces, such as sewers and tanks.

Competitive Analysis

The gas detection equipment market is becoming increasingly competitive, with a mix of global industry leaders and regional players competing on the basis of technology, product innovation, pricing, and service capabilities.

Technological innovation is a key differentiator in this market. Leading players are investing heavily in the development of smart, connected detection systems integrated with IoT, AI, real-time data analytics, and cloud platforms. These advancements enhance system reliability, facilitate remote monitoring, and minimize false alarms.

Companies are also focusing on miniaturized sensors, multi-gas detection capabilities, and enhanced battery life to meet the evolving needs of field personnel and mobile users. For example, MSA Safety has introduced Bluetooth-enabled portable detectors, while Honeywell offers wireless area monitoring systems and cloud-linked safety platforms.

Strategic partnerships, acquisitions, and geographic expansion are crucial to a company's competitive positioning. Firms are increasingly acquiring niche sensor manufacturers or software developers to expand their technological edge. For instance, Fortive (the parent company of Industrial Scientific) has been actively acquiring complementary safety and industrial automation businesses. Moreover, global players are targeting the Asia Pacific and Latin America for market expansion, leveraging regional partnerships to tap into fast-growing industries such as manufacturing, chemicals, and water treatment.

Regional players and emerging startups, particularly in Asia, are introducing cost-effective, localized solutions that are tailored to regional regulatory needs and pricing sensitivities. While they may lack the global reach of larger firms, these companies often compete effectively in price-sensitive markets by offering simpler, rugged designs and after-sales support. The competitive landscape is expected to become more dynamic as regulatory pressures, ESG goals, and industrial safety demands drive further innovation, collaboration, and consolidation across the sector.

Key players in the gas detection equipment industry are MSA Safety Incorporated, Opgal, Drägerwerk AG & Co. KGaA, Teledyne Technologies Inc., Emerson Electric Co., Halma plc, Honeywell International Inc., Danfoss A/S, Riken Keiki Co., Ltd., Sensidyne, LP, Testo SE & Co KGaA, Fortive Corporation, Inficon Holding AG, Trolex Ltd., ESP Safety Inc., and other players.

Recent Development

- In June 2025, Teledyne Gas & Flame Detection released the PS DUO, a portable, ATEX/IECEx-certified device capable of simultaneously detecting two gases (e.g., CO + H₂S, NH₃ + SO₂). Its ergonomic, rugged design and two-year battery life target field workers in high-risk industrial environments.

- In May 2025, Honeywell introduced a Thermal Conductivity-based Hydrogen Leak Detector capable of detecting leaks as small as 50 ppm. The sensor operates without recalibration for up to 10 years, marking a major leap in efficiency and hydrogen safety.

Segmentation of Gas Detection Equipment Market

-

By Type :

- Fixed

- Portable

-

By End-Use Industry :

- Oil & Gas

- Government & Military

- Manufacturing

- Chemicals & Petrochemicals

- Water & Wastewater

- Metal & Mining

- Utilities

-

By Communication Type :

- Wired

- Wireless

-

By Gas Type :

- Combustible

- Toxic

- Oxygen

- Dedicated

-

By Sensor Technology :

- Electrochemical

- Infrared

- Metal Oxide

- Catalytic

- Zirconia

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the Global Gas Detection Equipment Market size in 2025?

The gas detection equipment market is valued at USD 5.1 billion in 2025.

Who are the Major Players Operating in the Gas Detection Equipment Market?

Prominent players in the market include MSA Safety Incorporated, Opgal, Drägerwerk AG & Co. KGaA, Teledyne Technologies Inc., and Emerson Electric Co.

What is the Estimated Valuation of the Gas Detection Equipment Market by 2035?

The market is expected to reach a valuation of USD 8.6 billion by 2035.

What value CAGR is the Gas Detection Equipment Market Exhibit Over the Last Five Years?

The growth rate of the gas detection equipment market is 4.9% from 2020 to 2024.

Author:

Shubham Patidar

Editor:

Naved Ahmed