Sawn Timber Market Outlook (2025 to 2035)

The global sawn timber market is projected to reach USD 882.2 billion by 2035, up from USD 531 billion in 2024. During the forecast period (2025 to 2035), the industry is projected to grow at a CAGR of 4.8%. The demand of high-strength but eco-certified wood in the construction, furniture and engineered wood is on the increase, leading to the market.

It is highly usable for precision joinery or modular design due to its uniform grain, workability, and structural strength. Its increasing popularity in the export markets, as well as use in sustainable forestry programs, further adds to its attractiveness. With a trend towards building resistant and carbon-efficient structures, the sawn timber industry is expected to continue rising through the applications of residential and commercial enterprises worldwide.

What are the drivers of the Sawn Timber Market?

The sawn timber market is enjoying a stable growth on the back of the increasing demand for eco-certified, dimensionally stable, as well as high-performance wood products by the global construction industry. Since the industry is going modular and precision engineered building systems, sawn timber with its high strength to weight ratio, fin grain and work ability are becoming part of structural and interior uses.

Market penetration is being improved through increasing use of mass timber formats, including CLT (Cross-Laminated Timber) and Glulam, in mid-rise and commercial project types.

Rightfully, regulatory focus on sustainable forestry and carbon-free materials is also contributing to an increase in demand, and even certifications like FSC and PEFC are having an effect on procurement requirements in numerous markets worldwide. At the same time, value-added operations, such as lifecycle-optimized wood for use as decking, cladding, and joinery, are gaining traction in both developed and emerging economies.

Differentiation in the market is further augmented by the use of technology in sawmilling, which introduces tailored cuts and finishes that suit the technical requirements of a project. The combination of these trends makes the future of the sawn timber market strong, particularly in terms of environmentally friendly innovation and cost-effective delivery services in construction.

What are the regional trends of the Sawn Timber Market?

A dynamic interplay between construction demand, sustainability requirements, and technology integration is evident in the regional landscape of the sawn timber market. Markets in North American markets are experiencing solid support for prefabricated wooden housing and mass timber construction, especially in the U.S and Canada. Government incentives for green building and increased interest in cross-laminated timber (CLT) building systems are driving up the demand for precision-cut sawn timber products.

The Asia Pacific region is experiencing booming growth driven by urbanization, infrastructural development, and the transition to modular construction, which is evident in countries such as China, India, and Indonesia.

The markets in Latin America and the Middle East and Africa, which show consistency in demand for sawn timber, include surging housing construction, export-based forestry projects, and government housing programs.

What are the challenges and restraining factors of the Sawn Timber Market?

The sawn timber market faces several structural and operational limitations that hinder steady growth and quality assurance. Variability of the timber properties is one of the fundamental problems. These variances affect strength, dimensional stability, finish, among others, leaving doubt in structural and interior applications.

Another key issue is standardization, and in this regard, international trade faces certain problems, such as grading systems, treatment requirements, and compliance norms, which present a barrier to easy market access. In developing countries, due to poor technologies in terms of high kiln-drying and mechanized sawmilling, the waste of material is high, and the competitiveness of the goods is restricted.

Stringent environmental policies aimed at curbing deforestation, carbon emissions, and sourcing using certified means mandate environmentally friendly forest management. Yet, the coincidence of certification requirements with effectiveness and traceability remains challenging, especially in the case of smaller mills.

Scalability is also not possible due to the fragmented nature of the market, which is home to several local market players with limited access to automated processing and digital quality testing systems. This subdivision limits access to high-value export chains, indicating the necessity to modernize, consolidate, and coordinate industry standards.

Country-Wise Insights

Canada leads in sustainable, export-driven sawn timber production

-2025-to-2035.webp)

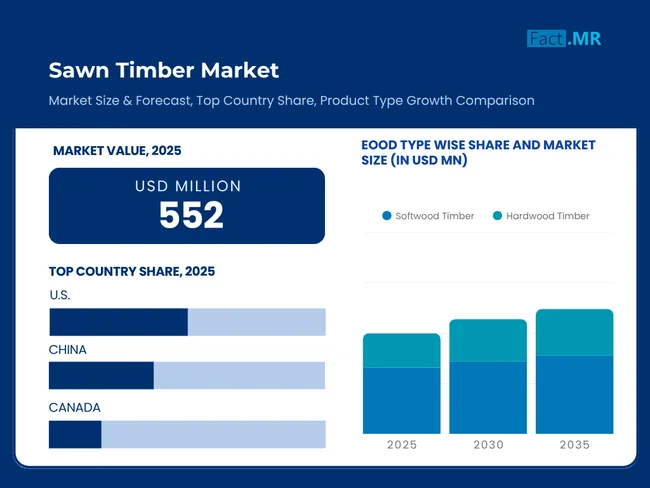

The sawn timber market in Canada is characterized by a high degree of export focus, environmentally sustainable forest management, and an increased use of mass timber in construction within the country. Canada is the world's largest exporter of sawn wood, with the majority of its supply going to key global markets such as the U.S., China, and Japan.

Major producers are the provinces of British Columbia and Quebec, which utilize well-developed sawmilling capacity facilities with long-standing supply sources of conifers. Regulatory conformity, as demonstrated by FSC/PEFC levels, will ensure entry into high-end markets where stringent requirements are placed on the environmental component.

Domestically, there is an increase in interest in pre-fabricated wooden houses and multi-story timber buildings, which is driving the demand for high-grade dimensionally stable sawn timber. Cross-laminated timber (CLT) and Glulam are being rapidly used in the construction of public infrastructure and institutional buildings, with strong provincial support for carbon-neutral construction materials.

Policies that advocate the conservation of biodiversity and have a positive impact on wildfire are shaping long-term harvesting plans that guarantee a stable market and sound preservation of ecological balance. All these factors make Canada a leader in terms of high-performance and sustainable sawn timber production.

Russia expands timber exports, navigating sanctions and modernization challenges

The environment in the Russian sawn timber industry has been described as a huge resource, with extensive forests, high production capabilities, and changing export sales. Russia has an extraordinary timber reserve that spans more than 800 million hectares, making it one of the largest in the world. It is therefore able to sustain its top global status as an exporter of sawn wood.

Most of the exports are concentrated towards China, the Middle East, and a few European markets and softwood species such as spruce, pine or fir species prevail in the trade relations.

The factories are located in the areas of Siberia and the Northwest under the influence of huge mechanized sawmills and the growth of rail and port services. Geopolitical factors and sanctions, however, have shifted part of export volumes in Western Europe back to Asia and the CIS world. Domestic demand is also increasing due to higher interest in affordable housing and the use of wood in construction.

Major challenges in the industry, despite its magnitude, include a low take-up of certification, outdated methods of processing in smaller mills, and environmental concerns related to logging. Sustainability, related to the development of modern sawmilling technology and adherence to sustainability benchmarks, is considered key to maintaining global competitiveness in the Russian sawn timber sector.

Sweden leads in sustainable, high-tech sawn timber exports

The Swedish sawn timber market is characterized by a very strong tradition in sustainable forestry, well-developed processing technologies, and a high quality of export infrastructure. Sweden is regarded as one of the largest wood producers and exporters of sawn softwood in Europe, with the country covering almost 70 percent of its forest area. Promising markets include the United Kingdom, Germany, and North Africa, which are facilitated by efficient maritime logistics and strong trade relations.

Forestry in Sweden is well-regulated in terms of environmental and biodiversity, with high standards certified by FSC and PEFC. The nation is also a pioneer in digital forest mapping, automated sawmilling, and the utilization of AI-based control systems to ensure evenness, minimize waste, and optimize yield.

Category-Wise Analysis

Softwood timber dominates structural markets with sustainable versatility

The use of softwood timber has remained dominant in the global sawn timber products market due to its extensive applications in the structural, industrial, and packaging sectors. The softwood is the material of choice for use in framing, as well as for any roof truss, beams, pallets, and formwork, due to species such as Pine, Spruce, and Fir that provide high strength-to-weight ratios, dimensional stability, and cost-effectiveness in the construction and logistics industries.

Softwood timber is being dried and sawn with high precision to increase homogeneity and reduce warping, making it better suited for the engineered wood industry, such as CLT and Glulam. Automation through innovations in grading and moisture control is already attempting to standardize the quality of products, especially in high-volume items.

As governments increasingly favor the use of low-carbon building materials, softwood is a valuable contributor to ecological construction. It can be large and environmentally friendly, and therefore it will continue to exert leadership in the wider sawn timber industry.

Sawn timber drives sustainable growth in global construction infrastructure

The most active sawn timber consumers are in the construction and infrastructure segment, where sawn timber is being used due to the demand of sustainable products, cost-effective and high-performing building materials globally. Sawn softwood, mostly pine and spruce, is most commonly used within a structural structure, roof truss, beams and formwork systems because of its desirable strength weight ratio and ability to be machined.

In high-rise commercial and public infrastructure, including in North America and Europe, where building decarbonization has been prioritized in carbon neutrality developments, CLT (Cross-Laminated Timber) and Glulam engineered timber formats are gaining maturity rapidly.

Building codes and green building rating systems are also lending credence to the continued importance of sawn timber in low-carbon construction, with several cities and countries requiring wood in their publicly funded housing and other buildings.

The demand is further being escalated by the prefabrication and modular building trends, which utilize dimensionally stable, kiln-dried, and precision-sawn timber components. Timber is being used in non-residential construction through enhanced fire-rated treatments and certified sourcing.

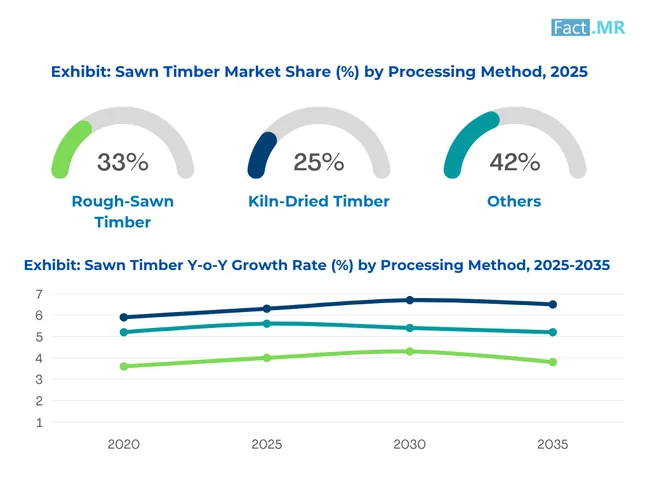

Kiln-dried timber ensures stability, quality, and export readiness

The kiln-dried timber sector is also becoming an important value-added proposition in the sawn timber industry due to its more stable dimensions, lower moisture levels, and high resistance to warping and fungal decay. The segment is gaining popularity in all aspects of construction, furniture and interior uses where narrow tolerances and repetitive performance are needed.

In the manufacturing and construction industry, Builders and manufacturers are focusing more of their resources on utilizing kiln-dried timber in framing, joinery, cabinetry, and flooring, where regulating shrinkage levels and maintaining surface quality is paramount. The process of kiln drying speeds up the seasoning process, retaining structural integrity as opposed to air-dried products, which makes it ideal for time-sensitive and quality-sensitive projects.

New kiln systems that adapt to temperature and humidity conditions are being used to optimize the drying process and increase production rates without compromising the quality of the wood. Phytosanitary compliance and increased pest resistance are also driving the segment's popularity in export markets.

Competitive Analysis

Key players in the sawn timber industry include West Fraser Timber Co Ltd, Canfor Corporation, Weyerhaeuser Company, Stora Enso Oyj, Interfor Corporation, UPM-Kymmene Oyj, Sierra Pacific Industries and Moelven Industrier ASA.

The sawn timber market is growing as a result of increased demand for sustainable building materials, engineered wood products, and low-carbon infrastructure. Green buildings are also finding timber an essential ingredient in achieving a strength-to-weight ratio and aesthetic beauty, combined with a low carbon footprint, making timber a building material of choice. The promotion of renewable materials and net-zero goals, supported by policies, is driving the transition in both residential and commercial areas.

Product consistency and waste reduction is the reasons why companies have invested in precision sawmilling, automation of kiln-drying and AI-based grading systems. Emerging strong is the trend to certified timber, panelized structures and other applications of modular construction. Investments made in cross-laminated timber (CLT), Glulam and logistics export are changing supply balances throughout the world.

Recent Development

- In March 2025, Kronospan, one of the world's leading producers of wood-based products, is pleased to announce the acquisition of the Sebes plant from ZG Timber, a subsidiary of the Ziegler Group. The initiative will contribute towards increased supply of high-quality sawn wood in furniture and construction applications, and augment growth in the market in Europe, where there is increased demand to use sustainable materials.

- In January 2023, Stora Enso, a large forest products company, revealed that it will invest 1 billion euros to build a cross-laminated timber (CLT) production line in Finland. This relocation will go in line with the trend market shift towards sawn wooden products that are eco-friendly, especially those meant to be used in residential and commercial building projects.

Fact.MR has provided detailed information about the price points of key manufacturers of the Sawn Timber Market positioned across regions, sales growth, production capacity, and speculative production expansion, in the recently published report.

Methodology and Industry Tracking Approach

In preparation for the 2025 global sawn timber market report, Fact.MR conducted a survey that covered 10800 market players in 30 countries, with each market having at least 300 respondents. About two-thirds of the respondents were direct market participants, including timber processors, sawmill operators, construction contractors, and manufacturers of wood products.

The third of them were value chain experts, including procurement chiefs, sustainability, forestry consultants, and trade controllers. The study period covered from June 2025 to May 2026, and the data collected during this period included information on market drivers, production trends, trade trends, investment trends, environmental restrictions, and technological gaps.

Responses were weighted according to the volumes of timber production, the distribution of forest cover, and consumption levels in regions. The study has analyzed more than 280 documents, including government policies, import-export data, sustainability publications, academic papers, and audits of timber certification systems.

Advanced tools of quantitative analysis were employed, including time-series modeling and cluster regression, to provide a relevant and accurate interpretation of structural and market-level variables. This all-around technique enabled the report to provide region-based information and futuristic outlooks within the global sawn timber value chain.

With Fact.MR monitoring consumer behavior, product efficacy, industry trends, and market opportunities since 2018, this report is becoming an authoritative source of information that stakeholders can rely on.

Segmentation of Sawn Timber Market

-

By Wood Type :

- Softwood Timber

- Hardwood Timber

-

By Processing Method :

- Rough-Sawn Timber

- Dressed Timber (Planed)

- Kiln-Dried Timber

- Pressure-Treated Timber

-

By Application :

- Construction & Infrastructure

- Residential

- Commercial

- Industrial Buildings

- Furniture & Joinery

- Packaging & Pallets

- Decking & Fencing

- Others

- Construction & Infrastructure

-

By End-Use Industry :

- Construction

- Furniture Manufacturing

- Logistics & Packaging

- DIY & Home Improvement

- Marine & Transport Structures

-

By Distribution Channel :

- Direct Sales (Mills to B2B buyers)

- Retail Distribution (Lumberyards, Hardware Stores)

- E-Commerce & Online Platforms

- Wholesale Distributors

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What was the Global Sawn Timber Size Reported by Fact.MR for 2025?

The Global Sawn Timber Market was valued at USD 552 Million in 2025.

Who are the Major Players Operating in the Sawn Timber Market?

Prominent players in the market are West Fraser Timber Co Ltd, Canfor Corporation, Weyerhaeuser Company, Stora Enso Oyj, Interfor Corporation, Sierra Pacific Industries, and Moelven Industrier ASA among others.

What is the Estimated Valuation of the Sawn Timber in 2035?

The market is expected to reach a valuation of USD 882.2 Million in 2035.

What Value CAGR did the Sawn Timber Market Exhibit Over the Last Five Years?

The historic growth rate of the Sawn Timber Market was 3.8% from 2020 to 2024.

Author:

Shubham Patidar

Editor:

Naved Ahmed