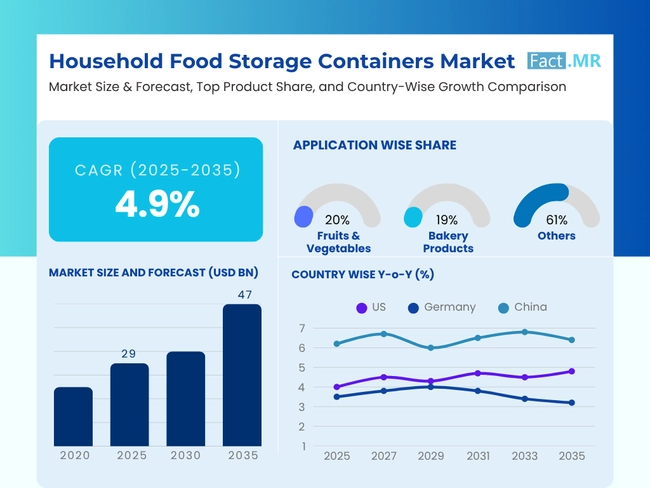

- Base Value(2025): 29 Bn

- Forecast Value (2035): 47 Bn

- CAGR (2035): 4.9%

Household Food Storage Container Market Outlook (2025 to 2035)

The global household food storage container market is expected to reach USD 47 billion by 2035, up from USD 28 billion in 2024. During the forecast period 2025 to 2035, the industry is projected to expand at a CAGR of 4.9%. Lifestyle changes and a focus on safe microwave systems, as well as airtight and BPA-free options, are contributing to the growth of the market size for this industry.

The household food storage containers market has been experiencing several major trends, driven by the need for the highest level of functionality, sustainability, and visual appeal. Currently, buyers who prioritize better health opt for containers made of BPA-free plastic, glass, or steel. These buyers want safer use, the ability to use it in a microwave, and reusability.

Health concerns and environmental considerations have led buyers to prefer biodegradable or recyclable containers. These trends are changing how products are made, what materials are used to make them, and how they are sold in both rich and poor countries.

What are the drivers of the Household food storage container Market?

Modern families are increasingly drawn to methods that make life easier and faster, which is why food storage containers are in high demand. These containers help pack food in advance, can be stacked, and prevent leaks, all in a way that fits into a busy life. They also help reduce waste by keeping food fresher for longer, resulting in less food being thrown away. Health-minded buyers look for safe ways to store the foods they put in these containers, and prefer to bundle up foods in containers that can be used in the microwave and cleaned often.

There is also a trend towards putting foods in containers that are safe to use in the microwave and easy to clean. These current needs in storage containers align with what people want in kitchen items, prioritizing health and safety for the user. As manufacturers address diverse demands across global regions, they are blending affordability with ethical production, creating a competitive edge in offering storage solutions that appeal to both practical needs and environmental values.

What are the regional trends of the household food storage container market?

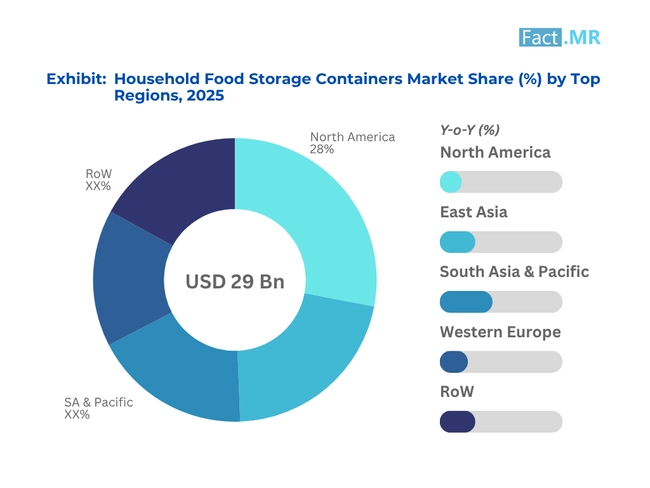

The regional trends of the household food storage container market indicate variations in lifestyle, stage of urbanization, consumer awareness, and maturity of the infrastructure. The North American market is undergoing a transition to high-performance containers to meet demand.

The growth in popularity of health food practices, such as meal prepping, portioning, and clean eating, has led to increased demand for stackable, leak-proof, and microwave-friendly containers. Consumers in the USA and Canada are adopting non-toxic materials and modular designs, as these individuals have a culture of proper refrigeration and waste minimization.

In Europe, sustainability and household efficiency are driving growth. Nations like Germany, France, and Sweden are also experiencing a growing trend of switching to glass and stainless-steel containers, which echoes the demands of customers who desire long-lasting materials and a design that complements contemporary kitchens. Recyclable and reusable products will align with regional environmental responsibility and help reduce plastic waste. Small kitchen spaces and compact living are also promoting multifunctional and space-saving container formats.

In the Asia-Pacific region, the market is growing due to rapid urbanization and shifting food habits. As more people form nuclear families and spend money on attending to work, consumers in countries such as China, India, and Indonesia are demanding flexible packages that aid in storage, reheating food, and portability.

Intelligent, segmented containers are generating a lot of excitement because they conform to the lunch schedule of the schools and offices. The market demand is also being strengthened by the increase in middle-class consumption and the modernization of lifestyles, particularly in urban Tier 1 and Tier 2 cities.

In Latin America, the trend of prioritizing household organization and affordable kitchen solutions is also influencing demand. The adoption of plastic and hybrid containers, which offer competitive pricing while performing well, is particularly notable in countries such as Brazil, Chile, and Mexico. There has been an increasing tendency towards airtight containers that help manage tropical humidity and minimize the spoilage of essential foodstuffs, such as grains and legumes.

Urban retail development, along with the increasing awareness of products in online markets and supermarkets, drives market growth in the Middle East and Africa. The state of premiumization will be evident in Gulf cities, where demand exists for designer glassware sets and imported kitchenware. Inexpensive and useful features prevail in other areas of the region, where families have adopted hard plastic containers to store goods in bulk and utilize them on a daily basis.

What are the challenges and restraining factors of the household food storage container market?

The market for household food storage containers is characterized by significant structural and behavioral constraints that question the feasibility of similar adoption, innovation, and scale-up. Standardization of product quality and material safety (regional/manufacturer) is one of the most long-term issues.

Plastic, glass, or hybrid container products tend to differ significantly in durability, thermal tolerance, and food-grade properties. This discrepancy draws reluctance in the mind of the consumer especially those who are health conscious to buy the product because they are not sure it is safe to use it under different conditions of use like when it is frozen, when it is microwaved, or when it is stored a long time.

Another obstacle is the lack of information concerning safe storage methods and material use. Scores of households still resort to using inappropriate containers to store foodstuffs without understanding the long-term health effects. Misuse may be caused by the lack of labeling and instructional design (hot food stored in low-grade plastics, repetitive use of containers that are not intended to be used in the long term).

Country-Wise Insights

USA Market Favors Safe, Stackable, Aesthetic, And Multifunctional Storage Containers

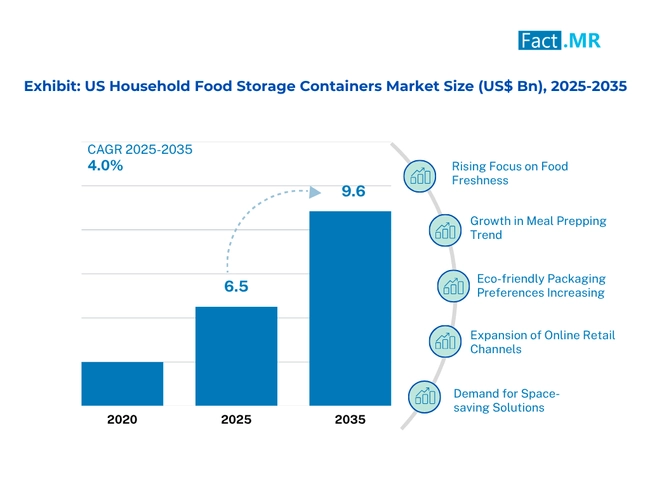

The household food storage container market in the USA is also characterized by the increasing demand for containers that serve multiple functions and are designed to support contemporary food storage and consumption patterns. Customers are increasingly interested in purchasing BPA-free containers that are microwave- and dishwasher-safe, particularly those made from borosilicate and high-grade polymers.

The clarity of federal agencies like the FDA has enabled a steady environment to incentivize the development of new product lines built around material safety and food contact standards, allowing manufacturers to continue investing in products that are end-of-life, premium, serviceable, or recyclable.

In Northeast and West Coast states, where green living and a modern approach to design are top buying motivators, suppliers are introducing uncomplicated, reusable forms that suit modern kitchen design trends. Conversely, the Midwest and Southern markets are experiencing a stable demand for value-based bulk storage services that accommodate large households and long-term preservation in pantries.

The American market is becoming increasingly segmented, with diversified products that integrate safety, functionality, and fit into consumers' lifestyles, in response to the further convergence of consumer interests in health, beauty, and convenient operational models.

China Drives Demand For Safe, Compact, And Digitally-Driven Storage Containers

A higher rate of urbanization, a changing food safety consciousness, and a growing transition towards organized kitchen supplies characterize China's Household food storage containers market. The need for multi-functional and space-saving containers is increasing at an alarming rate due to the growing population of small-scale family living in urban areas and the rising popularity of batch cooking, school lunch packing, and online grocery delivery services.

Cities in Tier 1, such as Beijing, Shanghai, and Shenzhen, are already experiencing demand for minimalist and durable containers, with lifestyle upgrades and the adoption of smart kitchen tools being prominent. On the contrary, Tier 2 and 3 cities are experiencing increased demand for economically priced bulk container sets capable of accommodating a family-sized food requirement, particularly for dry grains, spices, and diets.

Container innovation at scale is being spurred by the emergence of domestic e-commerce platforms, where top Chinese brands are selling bundles of hand-selected kitchenware items, and the trend towards localization of product design. A combination of safety-related issues, online retailing convenience and penetration, as well as customer demand, is shaping the Chinese market pattern, establishing significant traction on both the mass-market and premium sides of the container market.

Germany Prioritizes Eco-Friendly, Durable, And Design-Forward Food Storage Container Solutions

An increasing focus on customer concerns regarding material safety, ecological responsibility, and the integration of design and functionality in products characterizes the German household food storage containers industry. By embedding plastic reduction policies and retail practices, manufacturers follow EU standards and introduce compostable and recyclable materials of strict food-contact quality. Regulatory conformity to the German Packaging Act of 2021 (VerpackG) and consumer awareness of the risks associated with microplastics are also key for governments to drive innovation away from single-use plastics and towards new, high-durability alternatives.

Urban homeowners in Western and Southern Germany are driving demand for design-forward, space-effective container systems that can integrate with built-in refrigeration and smart pantry infrastructures. In the meantime, Central and Eastern Germany, which are family-oriented areas, are observing a long-term demand for high-scale storage mediums that support dry foods and pantry consolidation.

Manufacturers are also including QR-coded labels and transparent labels in their packaging to indicate compliance with health and sustainability standards. Led by a proactive regulatory environment, environmental education, and consumer sophistication, the German market is shifting towards premium, sustainability-conscious storage, offering utility, safety, and durability.

Category-Wise Analysis

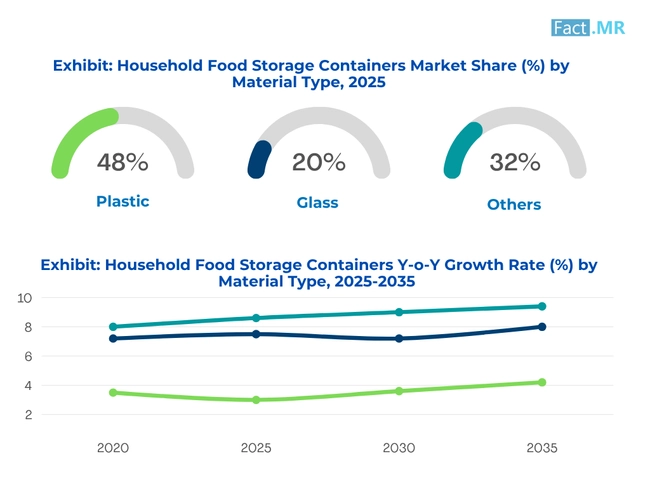

Plastic containers offer affordability, durability, and convenience for daily kitchen use

With low-cost purchasing options, portability, and versatility, the plastic container type is optimal for food preservation. Storage containers made of plastics offer multi-functional shapes to accommodate different storage, which come in various sizes and often include stackable designs and airtight lids. Due to increasing concerns about health issues, versions without BPA are gaining more popularity. Their enduring strength alongside resilience to breakage makes them ideal for daily use foods as well as easy-to-clean items.

Trends towards sustainability are also being met with reusable and recyclable alternatives offered by plastics. They have been integrated into modern kitchens, where leftovers or perishables are stored, as they are suitable for dry goods due to their efficiency and ease of use. Plastic containers allow for balanced storage alongside new improvements that offer better sealing, transparency for visibility, and modularity.

Microwave-safe containers ensure safe reheating and simplify modern meal routines

In streamlined lifestyles, microwavable containers emerge as multipurpose tools to streamline both food storage and reheating. The most common materials used for microwave-safe containers are plastics, which are BPA-free, silicone, and borosilicate glass. These do not warp or chemically leach due to high temperature exposure.

Venting lids that are microwave-safe aid in mess prevention both during and after use of the microwave. Along with serving and storing, these products also assist in cooking, making them multifunctional, which is appealing to busy individuals. Reducing the amount of washing up required helps promote good sanitary practices. With growing interest in meal prepping comes the need for safe and flexible receptacles that seamlessly integrate into daily kitchen routines, catering to convenience.

Special containers keep produce fresh, reducing waste and preserving nutrition

Fruits and vegetables should be kept in well-fitting boxes that keep them fresh longer, slow down rotting, and preserve their nutrients. More and more boxes with built-in fresh air ducts, moisture seals, and various components are used to make them last longer. Clear containers make it easy to see what’s inside and prevent rotting food from being eaten first.

This helps to cut waste. Most boxes are designed for use in the fridge and can be stacked to save space. People who buy fresh fruits and vegetables often make up the majority of buyers. These boxes help us eat healthy, prepare meals, and follow rules for keeping food fresh. They also help us to be good to the earth every day.

Competitive Analysis

Key players in the household food storage container industry include Sealed Air Corporation, Tupperware, Newell Brands, Owens-Illinois, Sonoco, Ardagh Group, Berry Global, Silgan Plastic, Alcan Packaging, Anchor Glass, Caraway, and Yeti.

The market is experiencing an increase due to rising demand for sustainable home storage solutions, food safety guarantees, and well-planned kitchens. The role of properly designed containers in extending the shelf life of food, reducing waste, and streamlining the food preparation process is gaining prominence as households become more space- and health-conscious. The manufacturers are investing in multi-compartment packs that meet modern use standards, tempered glass figures, and plastic that is long-lasting yet free of BPA.

Regionally spread production centers and quality control systems, driven by automation, have also made it possible to achieve better consistency and faster product delivery. The market is becoming increasingly competitive, with a preference for brands that combine innovation with functional relevance, as consumer expectations for design, hygiene, and environmental responsibility continue to rise.

Recent Development

- In October 2024, YETI just launched food storage containers - move over Rubbermaid. This launch aligns with the market’s demand for durable, eco-friendly, and versatile storage solutions for residential and commercial kitchens.

- In August 2024, Sealed Air introduces BUBBLE WRAP ® brand Ready-To-Roll Embossed Paper, combining the proven effectiveness of BUBBLE WRAP® brand cushioning with curbside-recyclable embossed paper. This innovation aligns with the market's demand for durable, eco-friendly, and versatile storage and packaging solutions for residential and commercial kitchens.

Fact.MR has provided detailed information about the price points of key manufacturers in the Household Food Storage Container Market, positioned across regions, including sales growth, production capacity, and speculative technological expansion, in the recently published report.

Methodology and Industry Tracking Approach

The 2025 global household food storage container market report surveyed 10,000 stakeholders across 30 countries, with a minimum of 300 respondents per national market. Approximately 65% of respondents were end users or stakeholders who interact with consumers, including retail buyers, professionals in home organization, and consumers of kitchenware. The remaining 35% consisted of industry professionals, including supply chain managers, product developers, packaging engineers, and brand strategists.

Consumer behavioral trends, including major shifts in material adoption, price alterations, brand loyalty, and unmet product needs, along with changing retail patterns, were presented in the data recorded between June 2025 and May 2026. To ensure that representative views were obtained, the survey responses were carefully weighted to align with regional income distribution, urbanization factor, market maturity, and population density.

The research utilised over 250 sources, including supply chain audits, sustainability declarations, trade journals, product specifications, and package law amendments. Further statistical analysis was performed using advanced statistical techniques, including regression modeling, cross-tabulations, and cluster analysis, to provide both qualitative and quantitative insights into the association between demographic factors, usage habits, and preferred materials.

To provide producers, distributors, and policy advocates working in the kitchenware and home storage ecosystem with a comprehensive understanding of both mass-market and luxury segments across plastic, glass, and hybrid storage containers, this approach was developed.

Segmentation of Household food storage container Market

-

By Material Type :

- Plastic Containers

- Paper Board

- Glass Containers

- Metal Containers

- Silicone and Composite Containers

- Biodegradable and Eco-friendly Containers

-

By Product Type :

- Bottle Jars

- Cans

- Boxes

- Cups & Tube

- Bags & Pouches

-

By Functionality :

- Microwave-safe Containers

- Freezer-safe Containers

- Dishwasher-compatible Containers

- Leak-proof/Airtight Containers

- Stackable and Modular Containers

- Smart Containers

-

By Distribution Channel :

- Supermarkets/Hypermarkets

- Specialty Homeware Stores

- Online/E-commerce Platforms

- Direct-to-Consumer (D2C) Brands

- Wholesale/Bulk Retailers

-

By End User :

- Individual Households

- Multi-member/Joint Families

- Working Professionals

- Students and Hostellers

- Meal Kit and Food Delivery Subscribers

-

By Application :

- Fruits & Vegetables

- Meat Processed Products

- Dairy Goods

- Grain Mill Products

- Bakery Products

- Others

-

By Region :

- North America

- Latin America

- Western Europe

- South Asia

- East Asia

- Eastern Europe

- Middle East & Africa

- Frequently Asked Questions -

What was the Global household food storage container market Size Reported by Fact.MR for 2025?

The Global Feed Micronutrients Market was valued at USD 29 Billion in 2025.

Who are the Major Players Operating in the household food storage container market?

Prominent players in the market are Sealed Air Corporation, Tupperware, Newell Brands, Owens-Illinois, Sonoco, Ardagh Group, and Yeti among others.

What is the Estimated Valuation of the household food storage container market in 2035?

The market is expected to reach a valuation of USD 47 Billion in 2035.

What Value CAGR did the household food storage container market Exhibit Over the Last Five Years?

The historic growth rate of the Feed Micronutrients Market was 3.9% from 2020 to 2024.