Knee Cartilage Repair Market Outlook (2025 to 2035)

The knee cartilage repair market is valued at USD 4.52 billion in 2025. As per Fact.MR analysis, the global industry will grow at a CAGR of 5% and reach USD 7.36 billion by 2035.

In 2024, the industry of cartilage repair in knees saw consistent forward momentum, partly fueled by surging cases of joint diseases, greater awareness towards early treatment options, and an increase in novel surgical technologies. Advances in fields like 3D bioprinting and biomaterials started gaining greater commercial acceptance in 2024, paving the way for a more individualized and structurally similar grafting.

Looking ahead to 2025, the sector is likely to see faster growth as healthcare providers increasingly embrace precision medicine and biologically augmented cartilage reconstruction methods. The use of robotics, newer imaging modalities, and AI-assisted diagnostics is also further optimizing surgical planning and postoperative results. Increasing R&D investment and favorable reimbursement policies in many countries are also likely to improve accessibility and affordability, drive patient reach, and confirm global adoption patterns.

| Metric | Value |

|---|---|

| Industry Value (2025E) | USD 4.52 billion |

| Industry Value (2035F) | USD 7.36 billion |

| CAGR (2025 to 2035) | 5% |

Market Analysis

The knee cartilage repair industry will expand steadily till 2035, fueled by the increasing incidence of osteoarthritis, sports injury, and advancements in regenerative medicine technologies. Ongoing innovation in 3D bioprinting and minimally invasive surgery is enhancing clinical efficacy and stimulating uptake. Individuals looking for long-term mobility solutions and medtech companies investing in biologics will gain the most. At the same time, high costs of surgery and a lack of trained staff could slow access in low-income areas.

Top 3 Strategic Imperatives for Stakeholders

Invest in Advanced Regenerative Technologies

Companies must invest in the next generation of regenerative treatments, such as stem cell therapy, 3D bioprinting, and bioengineered scaffolds, to increase treatment effectiveness and gain competitive differentiation.

Align Offerings with Aging Population and Sports Medicine Trends

Stakeholders need to adjust their product portfolios and services to meet the growing prevalence of age-related degeneration of the joints and high-performance sports injury, with an emphasis on minimally invasive and patient-specific treatment options.

Consolidate Strategic Partnerships and International Distribution Channels

For effective scaling, firms need to seek collaborations with orthopedic clinics, sports rehabilitation facilities, and distributors, deepen R&D partnerships, and contemplate mergers or acquisitions for access to emerging sectors and new technologies.

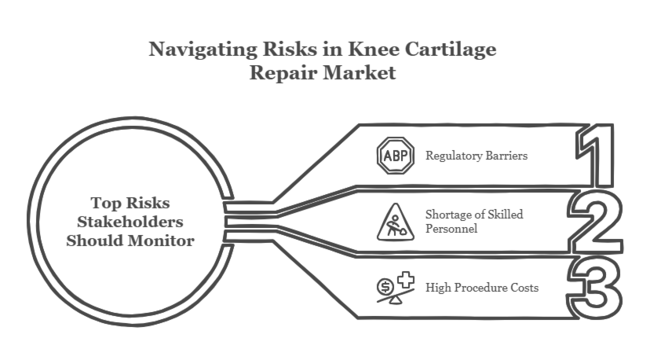

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability - Impact |

|---|---|

| Regulatory Barriers for Advanced Therapies - Strict approval processes for biologics and novel implants can disrupt the commercialization and restrict sector access. | Medium Probability - High Impact |

| Shortage of Skilled Orthopedic Surgeons and Technicians - Inadequate supply of trained personnel can limit procedural volume and impact treatment quality. | High Probability - Medium Impact |

| High Procedure Costs Constrained Patient Adoption in Price-Sensitive Regions - Costly surgical procedures might discourage patients, particularly in emerging economies with restricted insurance coverage. | High Probability - High Impact |

1-Year Executive Watch-List

| Priority | Immediate Action |

|---|---|

| Evaluate Emerging Regenerative Technologies | Conduct a targeted feasibility study on combining stem cell therapy and 3D bioprinting with product pipelines, with a focus on regulatory feasibility and commercial scale. |

| Expand Skilled Workforce Pipeline | Collaborate with leading medical centers to introduce focused training for surgeons and technicians in advanced cartilage repair procedures. |

| Strengthen Global Access and Affordability Strategy | Form regional distribution partnerships and implement tiered pricing or co-pay models to enhance access in price-sensitive areas. |

For the Boardroom

To stay ahead, companies must focus on scalable innovation and industry-driven strategies. This intelligence highlights the pressing need to invest in regenerative technologies and state-of-the-art cartilage restoration methods that cater to changing patient populations and clinical needs. Businesses must realign their R&D pipelines to stem cell technology and bioprinting, coupled with bridging the talent gap through systematic clinical training.

Additionally, widening availability through localized distribution and cost-efficient pricing models will be crucial in unlocking growth in under-penetrated sectors. In the coming years, board attention needs to be directed towards developing robust, technology-enabled orthopedic portfolios that foresee regulatory changes and patient-focused models of care.

Segment-Wise Analysis

By Treatment Modality

Autologous Chondrocyte Implantation is predicted to be the most profitable area in the field of knee cartilage repair over 2025 to 2035. The approach provides a biologically based, long-term result using an individual's cultured cartilage cells, with less risk of immune rejection and maximized integration into native tissue. Growing clinical choice of regenerative and less invasive procedures, paired with solid reimbursement support within advanced sectors, is propelling the adoption of ACI.

Supported by strong clinical evidence and positive patient-reported outcomes, ACI is set to witness a consistent adoption in both primary and revision repair procedures.

The autologous chondrocyte implantation segment will register a CAGR of 6.2% between 2025 and 2035, ahead of other modalities in terms of revenue growth and volume of procedures.

By Cartilage Type

Hyaline cartilage is expected to be the most profitable cartilage type segment in the knee cartilage repair industry between 2025 and 2035. This is mainly because of its essential biomechanical function in load-bearing joints such as the knee, where it offers low-friction articulation and mechanical shock absorption. Hyaline cartilage damage is commonly linked with degenerative diseases like osteoarthritis and traumatic injuries, and hence it is a significant clinical target for repair and regenerative treatments.

Hyaline cartilage is increasingly addressed in advanced procedures like autologous chondrocyte implantation and osteochondral grafting, where maintaining or reconstructing its structural integrity is the main principle for securing long-lasting results.

The hyaline cartilage repair surgeries will grow at a CAGR of 5.7% from 2025 through 2035, surpassing fibrocartilage both in clinical need and commercial potential.

By End User Segment

Hospitals are expected to continue as the most profitable end-user industry for knee cartilage repair treatments between 2025 and 2035. As institutions of advanced orthopedic treatment, hospitals provide comprehensive diagnostic and surgical facilities, multidisciplinary specialists, and post-operative rehabilitation care, all of which are necessary for sophisticated procedures like autologous chondrocyte implantation, osteochondral grafting, and microfracture surgery.

The growing incidence of osteoarthritis and trauma knee injuries is compelling patient preference towards better-served hospital settings that can provide high-quality, standardized outcomes.

As the number of orthopedic admissions increases steadily, particularly among aging populations and sports-injury patients, the hospital segment will have a CAGR of 5.9% from 2025 to 2035.

Country-Wise Analysis

United States

The United States continues to remain the global leader in the knee cartilage repair sector because of its strong orthopedic infrastructure, high incidence of sports injuries, and obesity-related joint conditions. Stepped-up uptake of minimally invasive cartilage repair technologies and a boom in outpatient arthroscopic procedures are driving growth. In addition, favorable reimbursement paradigms and large federal and private investments in cartilage regeneration research are pushing the boundaries of technology.

USA surgeons increasingly turn to autologous chondrocyte implantation and 3D bioprinting for individualized cartilage reconstruction. Both NIH and industry funds often support clinical trials, and it's driving ongoing innovation in this area.

Fact.MR opines that the CAGR of United States will be 5.6% from 2025 to 2035.

India

India's cartilage repair industry for knees is rapidly evolving, fueled by growing health awareness of the joints and a sharp increase in road traffic injuries. While cost consciousness continues to be a limitation, the spread of multi-specialty hospitals and orthopedic specialty centers is facilitating greater utilization of repair treatments.

Additionally, India is emerging as a major destination for affordable regenerative orthopedic treatments, drawing in medical tourists. Local manufacturers are collaborating with research and development institutions to develop cost-effective scaffolds and implants jointly and to localize innovation. An aging population and an increase in sports injuries among young urbanites are supporting the long-term demand forecast.

Fact.MR forecasts that the CAGR of India will be 5.3% from 2025 to 2035.

China

China is becoming a key growth driver in the knee cartilage repair sector, driven by a huge aging population and increasing orthopedic procedure volumes. As the Chinese government is emphasizing the modernization of healthcare with the Healthy China 2030 plan, hospitals are upgrading quickly to provide sophisticated surgical procedures. Public-private collaborations are financing research into biomaterials and cell-based cartilage therapy.

Western medtech players, in turn, are forging strategic partnerships with Chinese distributors to localize and speed up industry penetration. Increasing insurance coverage and government investment in tertiary hospitals are also widening the treatment base. Fact.MR projects that the CAGR of China will be 5.4% from 2025 to 2035.

United Kingdom

The UK sector for knee cartilage repair is being transformed by NHS investments in orthopedic care pathways and the nation's leadership in regenerative medicine research. Clinical uptake of autologous chondrocyte implantation and cell-based resurfacing is increasing, especially among younger patients who want to avoid total knee replacement.

The availability of advanced biobank networks and stem cell laboratories facilitates innovation. In spite of the economic pressure on the NHS, partnerships with university hospitals are also making it easier to access state-of-the-art methods.

Cartilage repair medical tourism from Europe is also gaining speed in light of the reduced waiting lists. Fact.MR opines that the CAGR of United Kingdom will be 5.1% from 2025 to 2035.

Germany

Germany is ahead of the game when it comes to cartilage repair technology, bolstered by globally renowned research facilities, highly accurate medtech production, and abundant orthopedic surgeons. It is one of the front runners in integrating tissue engineering and 3D printing into cartilage repair regimes. Subsidized by governments and led by universities, large-scale training is ongoing in the field of minimally invasive treatment modalities.

Cross-border alliances with Nordic biotech companies are introducing new scaffolds in the industry. And Germany's aged but healthy populace is progressively deciding on regenerative treatments in order to maintain mobility and avoid knee arthroplasty. Fact.MR is of the opinion that Germany's CAGR will be 5.5% from 2025 to 2035.

South Korea

South Korea's knee cartilage repair sector is thriving because of its sophisticated healthcare infrastructure and heavy government investment in regenerative medicine. The nation boasts some of Asia's leading orthopedic hospitals, which are early movers in cell-based cartilage therapies and personalized implants. Surgeons are working closely with biotech companies to engineer scaffold-free technologies and next-generation hydrogel matrices.

The Hallyu or Korean Wave, as well as an extensive health and fitness culture, are increasing the demand for joint care services among millennials and Gen Z. South Korea also exports regenerative cartilage technology into ASEAN countries.Fact.MR forecasts that the CAGR of South Korea will be 5.4% from 2025 to 2035.

Japan

Japan's knee cartilage repair industry is fueled by demographic aging, with a pressing need for joint preservation methods. The nation's long-standing expertise in minimally invasive surgery and biomaterials research is facilitating innovation in cartilage resurfacing. Autologous treatments and tissue engineering are being quickly adopted clinically, aided by regulatory fast-tracks under Japan's regenerative medicine law. The government is also investing in wearable tech integration to track joint recovery after surgery.

As osteoarthritis becomes more prevalent, national payers are now covering increasingly broader ranges of cartilage operations to stem long-term arthroplasty expenditure. Fact.MR opines that the CAGR of Japan will be 5.2% from 2025 to 2035.

France

France's knee cartilage repair environment is strengthened by its dense network of clinical trials and rising public-private funding for orthopedic innovation. France's patient-focused approach to care is spurring demand for regenerative approaches that postpone knee replacement. French hospitals are rolling out hybrid procedures combining autologous cell therapy with innovative polymer scaffolds.

Orthopedic clusters in the region are encouraging the integration of medtech startups with academic researchers. An increase in sports activity across all age ranges is driving a consistent flow of younger patients for early-stage cartilage procedures. Fact.MR forecasts that the CAGR of France will be 5.1% from 2025 to 2035.

Italy

Italy's cartilage repair environment for knees is advancing with the adoption of increased arthroscopic techniques and the further integration of outpatient joint treatment. Orthopedic wards in Italy are increasingly embracing biomimetic scaffolds and composite implants to treat severe cartilage defects. Public health programs are emphasizing early joint condition diagnosis through screening schemes.

Youth sports-related knee injury and degeneration due to aging are both contributing to the procedure numbers. Hospitals and foreign companies are collaborating on R&D, which is introducing new cell-source resurfacing technology to Italian clinics. Fact.MR opines that the CAGR of Italy will be 5.2% from 2025 to 2035.

Australia-New Zealand

Australia and New Zealand are experiencing increased orthopedic demand, particularly with rising life expectancy and a highly active older population. Incentives for minimally invasive procedures by the government and coverage of cartilage repair under private insurance programs are fueling growth.

The sports medicine industry within the region is booming, driving demand for early intervention procedures like microfracture and chondroplasty. Joint registries and electronic patient tracking are allowing evidence-based improvement in surgical results, making the region a testing ground for clinical innovation. Fact.MR forecasts that the CAGR of both areas will be 5.3% from 2025 to 2035.

FACT.MR Survey Results: Knee Cartilage Repair Industry Dynamics Based on Stakeholder Perspectives

(Surveyed Q4 2024, n=450 stakeholder participants evenly distributed across orthopedic surgeons, hospital procurement heads, sports medicine specialists, and medical device manufacturers in the USA, Western Europe, Japan, and South Korea)

Key Priorities of Stakeholders

- Recovery Time of Patients: 85% of international respondents cited "reducing recovery time" as the key driver of product adoption.

- Biocompatibility: 72% cited biocompatible biomaterials (e.g., hydrogels, collagen scaffolds) as essential for sustainability.

Regional Dispersion

- USA: 66% concerned with arthroscopic repair avenues enabling outpatient intervention, compared with 38% in Japan.

- Western Europe: 81% prioritized regenerative treatment modalities (e.g., ACI, MACI) consistent with country-specific reimbursement plans.

- Japan/South Korea: 59% gave preference to minimally invasive methods because of the age-old populations and surgeons' availability, compared to 33% in the USA.

Use of Advanced Regenerative Methods

High Variance

- US: 54% of orthopedic surgeons used scaffold-based cartilage implants, particularly in metropolitan trauma units.

- Western Europe: 49% used autologous chondrocyte implantation (ACI), with Germany (63%) registering the highest utilization because of advantageous insurance policies.

- Japan: As few as 27% utilized high-end biologics due to costs and lagging regulatory clearances.

- South Korea: 40% adopted stem cell-based treatment, primarily in Seoul-area private specialty clinics.

ROI Perception

- 69% of USA specialists graded high-tech interventions as "cost-effective" among active patients under age 50, while just 29% in Japan perceived long-term value from high-end procedures.

Material and Product Preferences

Consensus

- Synthetic-Organic Hybrid Scaffolds: Most preferred by 62% worldwide because of their structural integrity and reduced rejection rates.

Variance

- Western Europe: 53% chose bioengineered matrices (e.g., hyaluronic acid-based) because of strict MDR requirements.

- Japan/South Korea: 45% chose biodegradable polymers (e.g., PGA/PLA) to reduce follow-up procedures.

- USA: 67% chose allografts and hydrogels for flexibility and reduced rehab time.

Price Sensitivity

Shared Concerns

- 84% listed the expense of procedures (ranging USD 12,000-USD 35,000 per knee) as the primary deterrent to mass adoption.

Regional Differences

- USA/Western Europe: 59% would pay 20% more for solutions with documented results (e.g., second-look arthroscopy outcomes).

- Japan/South Korea: 76% highlighted the need for value-based pricing, with a high interest in bundled care packages under USD 8,000.

- South Korea: 43% favored national reimbursement-backed alternatives, compared to just 17% in the USA, where private insurance is prevalent.

Pain Points in the Value Chain

Manufacturers

- USA: 52% mentioned long FDA approval times for new implants.

- Western Europe: 47% complained of high costs of post-MDR compliance (e.g., documentation, testing).

- Japan: 61% experienced slow industry entry due to conservative clinical uptake and physician training deficiencies.

Distributors

- USA: 66% experienced stockout problems as a result of global supply chain vulnerability.

- Western Europe: 51% mentioned the challenge of demand forecasting in decentralized healthcare systems.

- Japan/South Korea: 63% grappled with surgeon resistance to newer regenerative solutions.

End-Users (Hospitals & Clinics)

- USA: 48% mentioned that lengthy rehab periods impacted patient satisfaction and throughput.

- Western Europe: 42% grappled with uniform surgical outcomes within hospitals.

- Japan: 57% mentioned lack of specialized rehab facilities as a major challenge.

Priorities for Future Investment

Alignment

- 71% of manufacturers surveyed intend to boost R&D investment in next-generation cell therapies and biofabrication.

Divergence

- USA: 64% look to digital surgery support tools (e.g., AR-based planning) for accurate repair.

- Western Europe: 58% look to incorporate smart biomaterials that respond to load stress.

- Japan/South Korea: 50% intend to invest in day-care procedure kits to minimize hospital stays.

Regulatory Impact

- USA: 67% said changing CMS coverage decisions (e.g., for outpatient orthopedic surgeries) had a major influence on purchasing priorities.

- Western Europe: 79% named MDR (Medical Device Regulation) as a decisive filter, inducing movement towards fewer, but compliant, vendors.

- Japan/South Korea: Just 35% believed existing regulations influenced demand due to delayed enforcement and patient preference for existing systems.

Conclusion: Variance vs. Consensus

- High Consensus: Recovery time, biocompatibility, and cost control predominate stakeholder priorities across the globe.

Key Variances:

- USA: Outpatient arthroscopy and high-tech-driven adoption.

- Western Europe: Intense focus on regulatory convergence and long-term regenerative advantages.

- Asia (Japan/South Korea): Cost efficiency, minimally invasive approaches, and compact models.

Strategic Insight:

- Regional tailoring is what it takes to succeed in the knee cartilage repair ecosystem: digital add-ons in the US, bioresponsive scaffolds in Europe, and cheap kits in Asia.

Government Regulations

| Country | Impact of Regulations and Mandatory Certifications |

|---|---|

| United States | FDA clearance (through 510(k) or PMA) is required for knee cartilage repair devices and implants. The FDA Center for Devices and Radiological Health (CDRH) has stringent safety, biocompatibility, and clinical trial regulations. [Source: FDA] |

| India | Knee implants are governed under the Medical Devices Rules, 2017, and need CDSCO (Central Drugs Standard Control Organization) clearance. India has also regulated the prices of knee implants to make them affordable. [Source: CDSCO, NPPA] |

| China | Medical devices need to obtain NMPA (National Medical Products Administration) approval. Class III devices such as cartilage repair implants require a lot of clinical data. New reforms also target localization of production. [Source: NMPA] |

| United Kingdom | After Brexit, devices need UKCA marking. Knee implant safety, efficacy, and post-industry surveillance are regulated by the Medicines and Healthcare products Regulatory Agency (MHRA). [Source: MHRA] |

| Germany | Subject to EU MDR (Medical Device Regulation) with CE marking and conformity assessment requirements for knee cartilage repair devices. Clinical evidence and biocompatibility testing are required. [Source: European Commission] |

| South Korea | Devices must be approved by the MFDS (Ministry of Food and Drug Safety). Korea is also subject to GMP compliance and post-industry surveillance for orthopedic implants. [Source: MFDS] |

| Japan | PMDA (Agency for Pharmaceuticals and Medical Devices) requires rigorous clinical testing and quality testing for orthopedic devices in the Pharmaceuticals and Medical Devices Act. [Source: PMDA] |

| France | Knee cartilage devices need CE marking under EU MDR, with oversight by ANSM (National Agency for the Safety of Medicines). Extra scrutiny is applied to the biomaterials utilized. [Source: ANSM, EU Commission] |

| Italy | CE marking is required as a regulation by the EU MDR. Distribution and clinical use of knee repair products, particularly those that use biologics, are under the jurisdiction of the Ministry of Health. [Source: Italian Ministry of Health] |

| Australia-New Zealand | The products need to be registered with the TGA (Therapeutic Goods Administration) and fulfill ARTG registration criteria. New Zealand demands a WAND notification. Post-industry surveillance is prioritized in both countries for high-risk implants. [Source: TGA, Medsafe] |

Competitive Landscap

The knee cartilage repair industry is moderately consolidated, with some leading companies and a few new entrants, all of which provide constant innovation and competition.

The leading players in this industry compete by incessantly innovating regenerative technology, biologics, and minimally invasive treatments. They also engage in strategic alliances, acquisitions, and expansion into regions to achieve competitive advantage.

Smith+Nephew acquired CartiHeal for USD 330 million in January 2024. CartiHeal created Agili-C, a revolutionary implant for knee cartilage defect repair. This acquisition expands Smith+Nephew's sports medicine offerings and its regenerative technologies portfolio.

In June 2024, Askel Healthcare announced clinical trial results of its COPLA® knee cartilage implant during the 9th Joint Preservation Congress in Warsaw. The results revealed promising cartilage regeneration potential, placing COPLA as a viable emerging option in knee repair.

Market Share Analysis

Zimmer Biomet (25%)

Zimmer Biomet is a global leader in musculoskeletal healthcare with expertise in cartilage repair solutions. They have BioCartilage® Extracellular Matrix, which is a micronized cartilage scaffold, and CartiLife®, an autologous chondrocyte implantation (ACI) product. Their cutting-edge biologics and surgical solutions aim to restore joint function through minimally invasive procedures.

Stryker Corporation (20%)

Stryker is a leading medical technology company with advanced cartilage repair solutions like the TruFit® BGS Plug for osteochondral defects and BioCartilage® (in collaboration with Arthrex). Their offerings range from bone graft substitutes and 3D-printed implants to furthering patient outcomes in joint preservation.

Smith & Nephew (18%)

Smith & Nephew is focused on regenerative medicine and advanced wound care, with significant presence in cartilage repair via MACI (Matrix-Induced Autologous Chondrocyte Implantation). Their ORIGIN® and COBLATION® technologies enable minimally invasive cartilage restoration. The company makes significant investments in biologics and stem cell therapies, positioning itself as a leading innovator in knee repair solutions.

DePuy Synthes (Johnson & Johnson) (15%)

A Johnson & Johnson subsidiary, DePuy Synthes provides TruFit® Bone Graft Substitute and synthetic cartilage implants for knee reconstruction. Their cartilage restoration technologies supplement their trauma and joint reconstruction expertise.

Vericel Corporation (10%)

Vericel is a leader in cell-based treatments, with MACI® (autologous cultured chondrocytes) being its lead product for cartilage regeneration. It concentrates on individualized regenerative medicine, utilizing cells derived from the patient to enhance the natural regeneration of cartilage. Vericel's solid clinical results and FDA clearances position it as a dominant niche company in complex orthopedic therapies.

Arthrex, Inc. (8%)

Arthrex is well-known for its minimally invasive orthopedic surgical solutions, such as the BioCartilage® Extracellular Matrix for cartilage repair. Their ArthroFlex® scaffold and PRP (Platelet-Rich Plasma) systems facilitate enhanced tissue regeneration. With a focused emphasis on sports medicine, Arthrex's surgeon-centric innovations spearhead its success in the cartilage repair business.

Other Key Players

- TiGenix NV (Takeda)

- ISTO Biologics

- MEDIPOST

- B. Braun Melsungen AG

- Osiris Therapeutics, Inc.

- Histogenics Corporation

- Anika Therapeutics

- Collagen Matrix, Inc.

- Arthrosurface

- Regentis Biomaterials

Segmentation

Segmentation by Treatment Modality:

- Arthroscopic Chondroplasty

- Autologous Chondrocyte Implantation

- Osteochondral Grafts Transplantation

- Cell-based Cartilage Resurfacing

- Implants Transplant

- Microfracture

Segmentation by Cartilage Type:

- Fibrocartilage

- Hyaline Cartilage

Segmentation by End User:

- Hospitals

- Specialty Clinics

- Ambulatory Surgery Centers

- Others

Segmentation by Region:

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- Middle East and Africa (MEA)

- Frequently Asked Questions -

What are the key drivers leading the industry for knee cartilage repair?

Increased sports injuries, aging demographics, and the need for minimally invasive procedures are speeding up industry growth.

Are there significant technological leaps in this sector?

Yes, technologies such as 3D bioprinting, stem cell therapy, and bioengineered implants are revolutionizing treatments.

Which areas are seeing the highest adoption of knee cartilage repair solutions?

North America and Europe are in the lead in terms of adoption, but Asia-Pacific is witnessing accelerating growth as healthcare infrastructure improves.

How are companies maintaining competitiveness in this industry?

Top companies invest in R&D, strategic acquisitions, and collaborations to increase their regenerative therapy offerings.

What are the most pressing challenges this industry faces at present?

High procedure fees, regulatory difficulties, and insufficient long-term clinical data remain challenges.

Author:

Md Sanaullah

Editor:

Anushree Karale