Railcar Spill Containment Market Outlook (2025 to 2035)

The global railcar spill containment market is projected to increase from USD 26.3 billion in 2025 to USD 42.8 billion by 2035, with a CAGR of 5.0%, driven by stringent environmental regulations to ensure compliance and prevent costly penalties. The increasing transport of hazardous materials via rail is driving the need for effective spill containment solutions to mitigate environmental and safety risks.

-2025-to-2035.webp)

What are the Drivers of Railcar Spill Containment Market?

The railcar spill containment market is experiencing robust growth, primarily due to the increasing stringency of environmental and safety regulations worldwide. Regulatory bodies such as the U.S. Environmental Protection Agency (EPA), Transport Canada, and European environmental authorities have enforced strict rules for the handling and transport of hazardous materials by rail.

These regulations require the use of spill containment systems at railcar loading and unloading stations to prevent soil and water contamination. As environmental compliance becomes a top priority for industries, investments in spill containment infrastructure are surging to avoid legal penalties and environmental liabilities.

Another key driver is the growing volume of hazardous materials transported via rail, including crude oil, chemicals, fertilizers, and industrial solvents. Rail transport is widely used for its cost efficiency and ability to handle bulk loads over long distances, particularly in the energy, chemical, and manufacturing sectors.

However, this increased reliance on rail logistics also amplifies the risk of spills and leaks. As a result, there is a rising demand for effective and durable spill containment systems to mitigate these risks and ensure operational safety during transit, loading, and unloading processes.

Technological advancements are also accelerating railcar spill containment market growth. Modern containment systems are being designed with advanced materials, such as corrosion-resistant polymers and high-strength composites, which offer improved durability and environmental performance.

The market is being bolstered by corporate sustainability initiatives and ESG commitments, especially among large logistics and chemical companies. As organizations strive to reduce their environmental footprint and align with global sustainability goals, spill containment solutions are viewed as essential infrastructure.

Furthermore, developing nations are rapidly expanding their rail infrastructure to support industrialization, and new terminals require containment systems that are compliant with regulations. Together, these factors are shaping a favorable environment for the continued expansion of the railcar spill containment market in both developed and emerging economies.

What are the Regional Trends of Railcar Spill Containment Market?

The U.S. and Canada hold the dominant share in the global market due to their well-established rail transport network, high volumes of hazardous materials shipment, and strict environmental compliance standards. Regulatory frameworks, such as the U.S. EPA’s Spill Prevention, Control, and Countermeasure (SPCC) rule and Transport Canada's safety standards, drive the mandatory adoption of containment systems.

Moreover, frequent investments in upgrading oil and chemical rail terminals further support the demand for advanced containment technologies in the region.

In Europe, the market is driven by the European Union’s strong environmental regulations and commitment to sustainability. Countries like Germany, the Netherlands, and France are leading adopters of eco-friendly spill containment systems.

The emphasis on reducing soil and groundwater pollution, coupled with growing concerns about the safety of transporting hazardous chemicals and fuels by rail, is encouraging the use of compliant spill control infrastructure. Moreover, Europe's focus on digitization is promoting the adoption of smart containment systems with remote monitoring capabilities.

The Asia Pacific is emerging as the fastest-growing regional market, driven by rapid industrialization, increased cross-border trade, and the expansion of rail infrastructure in countries such as China, India, Indonesia, and Vietnam. Governments in this region are investing heavily in rail freight networks and logistics hubs, particularly to support the chemical, petrochemical, and energy sectors.

As regulatory frameworks become more aligned with global environmental standards, industries are increasingly adopting spill containment systems to meet compliance requirements and attract foreign investment.

In the Middle East & Africa (MEA), market growth is moderate but gaining momentum due to increasing awareness about environmental protection and the modernization of transportation infrastructure.

In the Middle East, countries such as Saudi Arabia and the UAE are enhancing their industrial and logistics capacities, creating new opportunities for spill containment solutions, particularly in oil and gas transportation by rail. However, the market here is still in its early stages of development compared to other regions.

What are the Challenges and Restraining Factors of Railcar Spill Containment Market?

One of the primary restraints is the high initial cost of installing and maintaining advanced spill containment systems. These systems often require durable materials, site-specific engineering, and specialized installation, all of which can be costly, especially for small and mid-sized operators.

Moreover, smart containment technologies that incorporate sensors and monitoring systems involve added costs for integration, staff training, and ongoing maintenance, which may deter adoption in price-sensitive markets.

Another major challenge is the lack of regulatory uniformity across regions. While countries like the U.S., Canada, and members of the European Union have well-defined and enforced environmental protection laws, several developing nations still lack strict or clearly defined standards for railcar spill containment. This inconsistency in enforcement hinders adoption in emerging economies, even as hazardous materials are being transported in increasing volumes.

Operational limitations and site constraints also pose challenges to the market. Rail terminals located in densely populated or geographically constrained areas may face difficulties in retrofitting existing infrastructure with spill containment systems. Issues such as drainage design, space availability, and disruption of daily operations during installation often discourage implementation.

In some cases, older infrastructure may require costly upgrades before containment systems can be installed, further complicating the process.

Low awareness and limited technical expertise, especially in developing regions, hinder the market growth. Many logistics companies and terminal operators may not be fully informed about the environmental risks, compliance requirements, or long-term cost benefits of railcar spill containment. This knowledge gap results in underinvestment and missed opportunities for enhancing safety and sustainability.

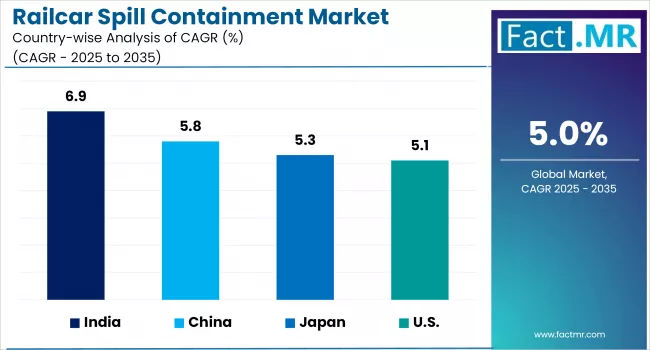

Country-Wise Outlook

U.S. Railcar Spill Containment Market sees Growth Driven by Stringent Regulatory Standards

The U.S. railcar spill containment market is experiencing steady and sustained growth, primarily driven by stringent environmental regulations and an increase in hazardous materials transported by rail. Regulatory agencies such as the U.S. Environmental Protection Agency (EPA) and the Occupational Safety and Health Administration (OSHA) have implemented comprehensive guidelines, including the Spill Prevention, Control, and Countermeasure (SPCC) rule.

These regulations require rail operators and freight terminals to adopt robust spill containment systems to prevent soil and water contamination. As regulatory scrutiny intensifies, more companies are investing in durable and compliant containment infrastructure to avoid penalties and ensure environmental protection.

Another major driver of growth is the high volume of hazardous freight moved by rail across the country. With over 140,000 miles of rail network, the U.S. has one of the most extensive and heavily used rail systems globally, transporting large volumes of crude oil, chemicals, fertilizers, and industrial solvents.

The increasing reliance on rail for these materials inherently raises the risk of spills, leaks, and accidents. To mitigate these risks, companies are deploying spill containment systems at rail yards, loading and unloading stations, and storage terminals, further expanding the market.

-2025-to-2035.webp)

Technological advancements are also playing a critical role in shaping the U.S. market. Companies are increasingly adopting smart spill containment systems that feature real-time monitoring, automated leak detection, and IoT-enabled sensors. These innovations enhance safety, reduce manual labor, and help companies meet compliance requirements more efficiently.

China witnesses Rapid Market Growth Backed by Rapid Industrialization

The railcar spill containment market in China is experiencing rapid expansion, driven by industrialization, infrastructure investment, and increasing environmental standards. China's industrial boom, especially in petrochemicals, chemicals, and energy, has led to increased use of rail to carry bulk hazardous materials. This growth has intensified the need for spill containment systems at terminals and on rail networks to reduce environmental risks.

Furthermore, the nation’s evolving regulatory framework and environmental policies are playing a significant role. New laws around spill prevention and water contamination are enforcing stricter standards. Along with rising public and corporate environmental responsibility, there is a strong demand for advanced solutions, including high-performance containment materials and IoT-based leak detection systems.

China is among the fastest-growing regional markets, with double-digit or high single-digit growth rates, driven by infrastructure investment, regulatory modernization, and the expansion of industrial logistics across freight transport.

Japan sees Strict Environmental Standards Fuels Demand for Railcar Spill Containment

The adoption of advanced containment systems in Japan is being driven by a combination of moderate regulatory tightness, growing environmental consciousness, and steady industrial activity. Although Japan’s environmental standards have long been rigorous, particularly concerning water and soil protection, the demand for additional spill-containment infrastructure is primarily concentrated in the petrochemical and heavy-chemicals sectors, where safety and compliance are paramount.

A shift is also occurring in containment technology. Japanese operators are increasingly upgrading to custom-engineered track pans and containment berms, which are tailored to meet the requirements of specific rail terminals and types of hazardous cargo. This innovation is supported by notable R&D investments, in line with global trends toward more resilient, corrosion-resistant materials and intelligent monitoring systems.

Japan’s market expansion will be characterized by steady, low- to mid-single-digit growth, as awareness of environmental risks increases and older rail infrastructure is incrementally retrofitted. However, compared to the more aggressive expansion seen in China and other Asian Pacific nations, Japan remains a mature market, oriented toward modernization and optimization rather than rapid capacity buildup.

Category-wise Analysis

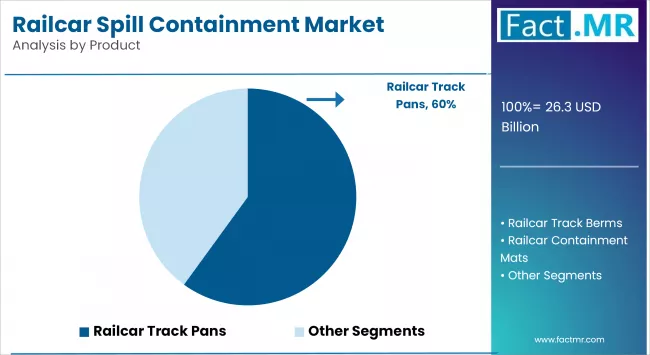

Railcar to Exhibit Leading by Product

The railcar track pans segment holds the largest market share, driven by their use in rail terminals, chemical loading stations, and freight yards, where they are utilized for their high containment capacity, durability, and ease of installation.

These systems are typically constructed from heavy-duty materials, including polyethylene, steel, or fiberglass. They are designed to collect and contain spills from valves, hoses, and tank car fittings during loading and unloading operations. Moreover, regulatory compliance with SPCC and EPA spill control standards continues to drive investments in robust track pan systems.

The railcar containment mats segment is projected to be the fastest-growing over the forecast period. These mats offer a more portable and cost-effective solution for temporary or mobile containment applications. They are especially suited for short-term spill control, emergency response, or smaller operations that do not require permanent infrastructure.

Advancements in material science, such as the use of chemical-resistant and UV-stabilized fabrics, are enhancing the performance and reusability of containment mats. Their quick deployment, lightweight design, and ability to be used across multiple locations make them attractive for industries with dynamic operational needs. Growth is further accelerated by increasing awareness among small and mid-sized logistics firms seeking affordable, regulation-compliant containment solutions without the cost or complexity of permanent systems.

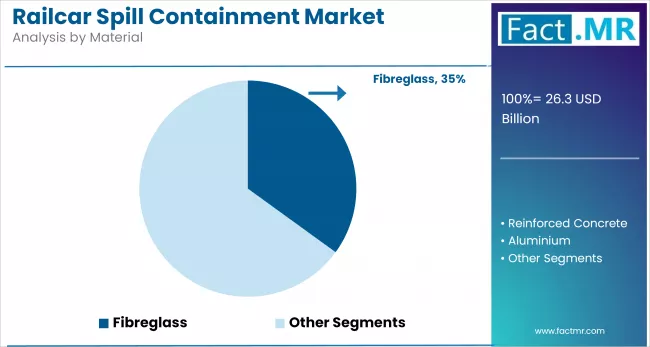

Stainless Steel to Exhibit Leading by Material

Polyethylene is the dominant material segment, accounting for the largest market share. This dominance is largely attributed to polyethylene’s excellent chemical resistance, lightweight nature, and cost-effectiveness. It is widely used in manufacturing track pans, berms, and spill pallets due to its high durability, corrosion resistance, and ability to withstand a wide range of hazardous substances, including acids, solvents, and petroleum-based liquids.

Polyethylene systems are also easier to install and maintain compared to heavier alternatives, such as reinforced concrete or metal. Its compatibility with modular designs and regulatory compliance requirements, especially in the oil & gas and chemical sectors, further strengthens its position as the leading material in spill containment applications.

Stainless steel is the fastest-growing material segment, driven by rising demand for high-strength, long-life, and high-performance containment systems in heavy industrial applications.

Stainless steel offers superior durability, load-bearing capacity, and resistance to extreme temperatures and corrosive chemicals, making it ideal for permanent installations at major rail terminals, refineries, and chemical processing facilities.

Oil & Gas to Exhibit Leading by End-Use Industry

The oil & gas industry represents the dominant end-use segment due to the high volume of crude oil, refined petroleum products, and other hazardous liquids transported via rail across long distances. The industry’s stringent safety and environmental standards necessitate the use of robust containment systems to prevent accidental leaks and spills during loading and unloading operations.

Regulatory mandates, such as the U.S. EPA's SPCC rule and equivalent standards in Canada and Europe, have further accelerated the adoption of railcar containment solutions in oil terminals and refineries.

The petrochemical industry is expected to be the fastest-growing end-use segment, fueled by global expansion in chemical manufacturing and rising cross-border rail transport of liquid chemicals and hazardous compounds. As the demand for plastics, solvents, and industrial chemicals increases, particularly in the Asia-Pacific and Middle East regions, so does the risk of railcar-related spills.

Petrochemical plants are increasingly installing containment systems to comply with environmental regulations, reduce liability, and ensure safe handling of aggressive chemicals. Moreover, advancements in material-resistant containment technologies and the growing number of specialized rail terminals serving petrochemical clusters are driving rapid growth in this segment.

Competitive Analysis

The railcar spill containment market is becoming increasingly competitive, with a mix of well-established players and emerging companies competing on innovation, regulatory compliance, and cost-efficiency. Companies offer a range of solutions, including track pans, berms, mats, and modular containment systems tailored for the oil & gas, chemical, and transportation industries. Their continued investment in product development and customization keeps them at the forefront of the market.

Product innovation and material advancements are key areas of competition. Leading players are focusing on developing high-performance containment systems using advanced materials such as UV-resistant polyethylene, stainless steel, and composite polymers. Moreover, the integration of smart technologies, such as IoT-based sensors, real-time leak detection, and remote monitoring systems, is helping manufacturers differentiate themselves in the market. These smart containment systems are particularly appealing in high-risk environments where quick response and data tracking are essential for regulatory compliance and operational safety.

Strategic collaborations and mergers & acquisitions are shaping the competitive dynamics of the market. For example, Eagle Manufacturing’s acquisition by Justrite Safety Group expanded its reach in industrial safety solutions, while partnerships between containment product suppliers and chemical or logistics firms are improving on-site implementation and service offerings. Such moves allow companies to enhance their technological capabilities, streamline supply chains, and enter new markets more effectively.

Key players in the railcar spill containment industry include Eagle Manufacturing, Enpac, Complete Environmental Products, The Century Group, Ultra Tech International, Safe Rack, Basic Concepts Inc., Pactec, Safe Harbor Access Systems, Polystar Containment, Aldon Company Inc., GEI Works, Clean It Up, and other notable companies.

Recent Development

- In March 2025, SafeRack, a leading provider of loading racks and safety solutions, completed a comprehensive installation at a railcar loading terminal. The project involved integrating spill containment track pans with gangways and safety cages, significantly enhancing both operational efficiency and worker safety while ensuring compliance with stringent environmental and occupational safety standards such as those set by the EPA and OSHA.

(Source: https://saferack.com/installations/spill-containment-gangway-platformom)

Segmentation of Railcar Spill Containment Market

By Product :

- Railcar Track Pans

- Railcar Track Berms

- Railcar Containment Mats

By Material :

- Fibreglass

- Reinforced Concrete

- Aluminium

- Stainless Steel

- Galvanised Steel

- Polyethylene

- Poly Vinyl Chloride

By End-Use Industry :

- Power Plants

- Oil & Gas Industries

- Petrochemical Industries

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the Global Railcar Spill Containment Market size in 2025?

The railcar spill containment market is valued at USD 26.3 billion in 2025.

Who are the Major Players Operating in the Railcar Spill Containment Market?

Prominent players in the market include Eagle Manufacturing, Enpac, Complete Environmental Product, The Century Group, and Ultra Tech International.

What is the Estimated Valuation of the Railcar Spill Containment Market by 2035?

The market is expected to reach a valuation of USD 42.8 billion by 2035.

What Value CAGR Did the Railcar Spill Containment Market Exhibit Over the Last Five Years?

The growth rate of the railcar spill containment market is 4.2% from 2020-2024.

Author:

Shubham Patidar

Editor:

Naved Ahmed