Packaging Coating Market Outlook (2025 to 2035)

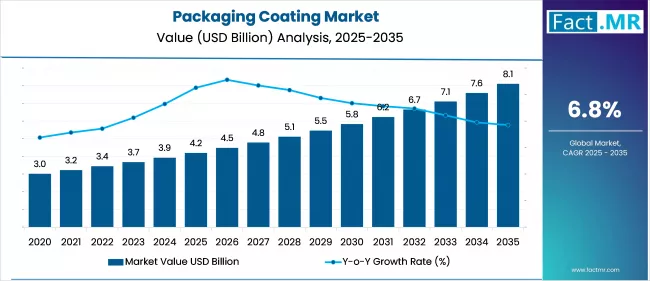

The global packaging coating market is projected to increase from USD 4.2 billion in 2025 to USD 8.1 billion by 2035, with a CAGR of 6.8%, driven by increasing demand for sustainable, high-performance packaging solutions fueled by e-commerce expansion, regulatory compliance, and technological advancements. Their use makes them ideal for enhancing durability, visual appeal, and barrier protection across a wide range of consumer goods and industrial packaging applications.

What are the Drivers of Packaging Coating Market?

The packaging coatings market is witnessing robust growth, primarily driven by rising sustainability demands and stringent global regulations. As governments across regions implement bans on harmful substances like PFAS, VOCs, and BPA, manufacturers are increasingly shifting towards eco-friendly, recyclable, and biodegradable coating solutions.

These regulatory pressures are driving innovation in the development of water-based, solvent-free, and plant-based coatings that meet both environmental standards and functional performance requirements. The emphasis on circular economy principles is further reinforcing the demand for sustainable packaging coatings across industries.

The booming e-commerce and online retail industry, which has amplified the need for durable and protective packaging solutions, is driving market growth. As products are transported over longer distances, coatings that enhance barrier properties, resist abrasion, and ensure visual integrity have become increasingly essential.

Consumer expectations regarding aesthetics and unboxing experiences are increasing, prompting brands to adopt coatings that offer premium finishes, including gloss, matte, metallic, and soft-touch effects. These visual and tactile enhancements not only protect the packaging but also serve as tools for brand differentiation in a crowded marketplace.

The market is also benefiting from rapid technological advancements in coating materials and application techniques. Innovations such as UV-curable, nano-engineered, and antimicrobial coatings are enhancing packaging functionality by providing extended shelf life, microbial protection, and improved print adhesion. The increasing adoption of smart and interactive packaging technologies, enabled by coatings that are compatible with QR codes, sensors, and traceability features, is further contributing to the market's evolution, particularly in sectors such as food, beverages, and healthcare.

Furthermore, the rising consumption of packaged foods, pharmaceuticals, and personal care products is expanding the addressable market for high-performance packaging coatings. These coatings play a critical role in maintaining hygiene, ensuring tamper-evident packaging, and preventing contamination, factors that are especially important in the healthcare and food industries.

What are the Regional Trends of Packaging Coating Market?

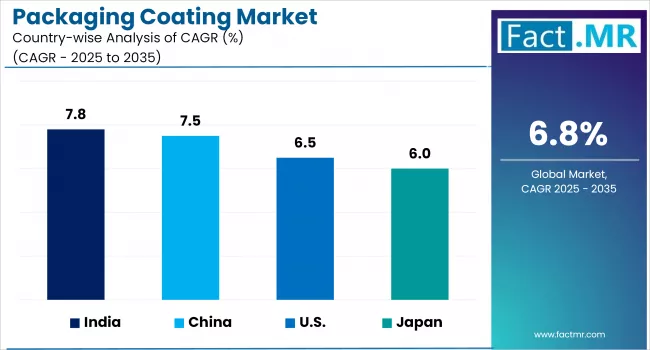

Asia Pacific region currently leads the global packaging coatings market and is projected to maintain its dominance over the forecast period. Rapid industrialization, urbanization, and a growing middle-class population have increased the consumption of packaged goods, especially in countries like China, India, and Southeast Asian nations.

The boom in e-commerce and food delivery services is also driving demand for durable, protective, and high-barrier coatings. Moreover, increasing regulatory emphasis on sustainable packaging and reduced VOC emissions is encouraging the adoption of eco-friendly water-based and UV-curable coatings, further stimulating packaging coating market growth across the region.

In North America, the market is being propelled by strong demand across the food, beverage, personal care, and pharmaceutical sectors. Consumers are increasingly seeking sustainable, safe, and visually appealing packaging solutions, leading to the rise of solvent-free, BPA-free, and functional coatings that ensure product integrity and compliance with environmental regulations. Moreover, the rapid expansion of e-commerce logistics in the U.S. and Canada has fueled demand for coatings that provide enhanced protection during shipping, alongside premium aesthetics that enrich the consumer unboxing experience.

Europe is another key market, characterized by its stringent environmental and chemical regulations, including REACH compliance and bans on certain single-use plastics and toxic substances. These frameworks have accelerated innovation in sustainable coating technologies, such as bio-based, recyclable, and waterborne coatings.

The Middle East and Southeast Asia regions are emerging as promising markets, driven by increasing urbanization, growth in fast-moving consumer goods (FMCG), and rising disposable incomes. UAE is witnessing growing adoption of packaged foods and beverages, which is positively impacting the demand for advanced packaging coatings. However, challenges such as infrastructure limitations, economic instability, and limited regulatory enforcement in some areas may temper the growth pace.

What are the Challenges and Restraining Factors of Packaging Coating Market?

The packaging coatings market faces several restraints and challenges that may limit its growth, despite rising global demand. One of the most significant challenges is stringent environmental regulations surrounding the use of certain chemicals such as volatile organic compounds (VOCs), bisphenol A (BPA), and per- and polyfluoroalkyl substances (PFAS). These substances are commonly used in traditional coatings due to their durability and chemical resistance; however, regulatory restrictions, particularly in North America and Europe, are pressuring manufacturers to reformulate their products.

Another key restraint is the high cost of advanced and sustainable coatings. While water-based, UV-curable, and bio-based coatings offer environmental and performance benefits, they are often more expensive than conventional solvent-based alternatives. This can be a deterrent for small and medium-sized manufacturers, especially in cost-sensitive or developing markets.

Moreover, the specialized equipment and technologies needed for the application of some high-performance coatings may further increase production costs and limit adoption in regions with underdeveloped industrial infrastructure.

Technical challenges related to performance trade-offs also pose barriers. For example, while water-based and solvent-free coatings are eco-friendly, they may offer lower moisture or chemical resistance compared to traditional coatings, particularly in high-humidity or high-temperature environments. Achieving the right balance between sustainability, durability, and functionality remains a challenge for formulators, particularly in applications that require a long shelf life and high barrier performance.

Raw material price volatility, driven by global supply chain disruptions, geopolitical tensions, and fluctuating crude oil prices, has had a direct impact on coating production costs. Many packaging coatings are derived from petrochemicals, making them susceptible to swings in oil prices. This uncertainty affects manufacturers' pricing strategies and profit margins, particularly when long-term contracts are in place with packaging suppliers or consumer goods companies.

Country-Wise Outlook

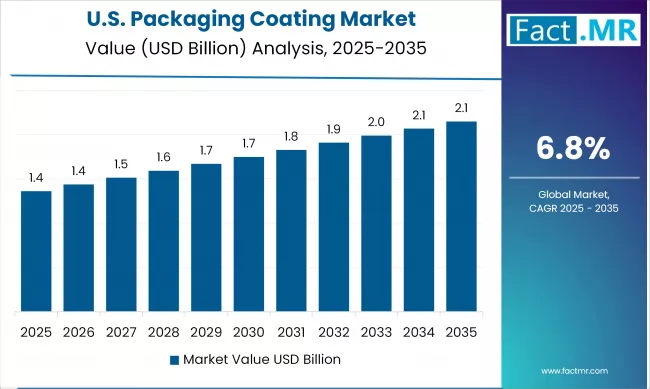

The U.S. Packaging Coating Market sees Growth Driven by Rise In E-Commerce and Direct-To-Consumer Distribution Models

The U.S. packaging coatings market is experiencing steady growth, driven by robust demand from key end-use sectors such as food and beverages, pharmaceuticals, and personal care. Packaging coatings are increasingly valued for their ability to enhance durability and provide effective barriers against moisture and oxygen. These features are crucial for improving product safety and shelf life, especially in industries where maintaining product integrity and meeting regulatory standards is essential.

A significant factor propelling the U.S. market is the continued rise in e-commerce and direct-to-consumer distribution models, which demand advanced packaging solutions that are both protective and aesthetically appealing.

Coatings that offer abrasion resistance, grease barriers, and premium visual finishes are being adopted more widely as brands seek to enhance the customer unboxing experience and reduce product damage during transit. The food and beverage industry, in particular, remains a dominant force, as coated packaging is essential to preserve freshness and comply with FDA food contact standards.

Moreover, consumer-driven trends, stringent environmental regulations and sustainability initiatives are shaping the future of packaging coatings in the U.S. The Environmental Protection Agency (EPA) and other regulatory bodies are enforcing strict limits on the use of volatile organic compounds (VOCs), PFAS, and BPA in packaging materials. This has accelerated the adoption of low-VOC, water-based, UV-curable, and solvent-free coatings that offer improved environmental profiles without compromising performance.

Furthermore, the U.S. market is benefiting from strong investments in manufacturing infrastructure and technological innovation. Advanced coating technologies, such as antimicrobial, smart, and high-barrier formulations, are gaining traction, especially in applications that require extended shelf life, tamper evidence, and traceability. With a well-established industrial base, growing consumer awareness, and strong regulatory oversight, the U.S. packaging coatings market is poised for long-term, innovation-driven growth.

China witnesses Rapid Market Growth Backed by Rapid Industrialization and Urbanization

The packaging coatings market in China is experiencing growth, largely propelled by rapid industrialization, urbanization, and a burgeoning middle-class consumer base. As the global manufacturing hub for packaging materials, ranging from cans and cartons to flexible plastics, China’s coatings industry is scaling to meet increasing demand, especially in the food, beverage, and personal care sectors.

The rise of e-commerce, where China accounts for over 50% of the world’s online retail sales, has increased the need for durable and visually appealing packaging coatings to support safe transit and enhance brand presentation.

Environmental regulations also play a critical role in shaping market growth. The Chinese government’s initiatives to reduce VOC emissions and plastic waste have driven manufacturers to adopt eco-friendly water-based and UV-curable coatings, aligning with global and domestic sustainability goals. This clean-technology shift is fostering innovation while helping domestic and international producers remain compliant and competitive.

Government support, via subsidies, tax incentives, and infrastructure investment, along with continued investment by global players like AkzoNobel, PPG, and local Chinese firms, is accelerating capacity expansion and R&D in advanced coating technologies. These factors combined suggest that China's packaging coatings sector is set for sustained, innovation-led growth over the next decade.

Japan Sees Rising Demand for High-Quality, Sustainable Packaging Solutions

The Japan’s packaging coatings market is experiencing steady, innovation-driven growth, propelled by rising demand for high-quality, sustainable solutions. This growth is supported by multiple structural and strategic drivers. Japan’s strong regulatory emphasis on low-VOC, biodegradable, and mono-material packaging, evident in recent policies and recycling standards, encourages widespread adoption of advanced coating formulations.

Likewise, the country’s sophisticated e-commerce ecosystem and booming packaged food and pharmaceutical industries require coatings that balance functionality, like barrier performance and chemical resistance, with aesthetic appeal.

Japan’s global leadership in high-precision and smart packaging technologies, including nanocoatings and sensor-compatible surfaces, further underpins market growth. As domestic and international players, including AkzoNobel, Nippon Paint, and Kansai Paint, invest in R&D and line expansions, Japan’s packaging coatings market is well-positioned for sustained growth in the mid-to-high single digits over the coming decade.

Category-wise Analysis

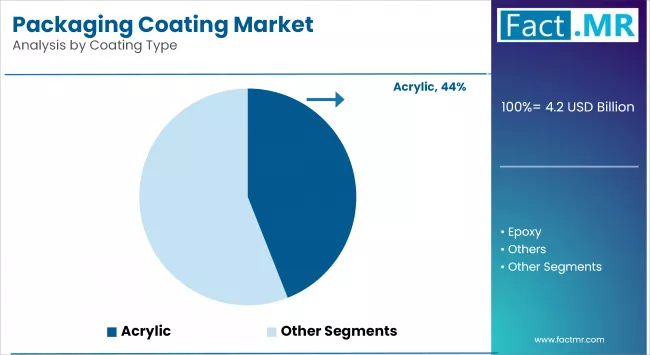

Acrylic to exhibit Leading by Coating Type

The acrylic coatings segment currently dominates the packaging coating market due to their excellent adhesion, transparency, chemical resistance, and cost-effectiveness across diverse packaging substrates, including metal, plastic, and paperboard.

They are commonly used in food and beverage packaging, personal care products, and pharmaceutical applications due to their ability to offer a glossy finish, durability, and resistance to environmental factors such as UV radiation and moisture. The increasing demand for aesthetically appealing and long-lasting packaging, particularly in the consumer goods sector, is a major driver sustaining the dominance of the acrylic segment.

The fluoropolymer coatings segment is expected to grow at the fastest CAGR over the forecast period. This growth is driven by their superior barrier properties, including high resistance to heat, chemicals, and moisture, making them ideal for high-performance applications in the pharmaceutical, medical device, and critical diagnostic packaging sectors.

As the need for highly sterile, contamination-resistant, and thermally stable packaging increases, especially in advanced healthcare and biotechnology applications, fluoropolymer coatings are gaining traction. Their rising use in specialty and high-value packaging, along with innovations in environmentally friendly fluoropolymer formulations, is propelling this segment’s accelerated growth.

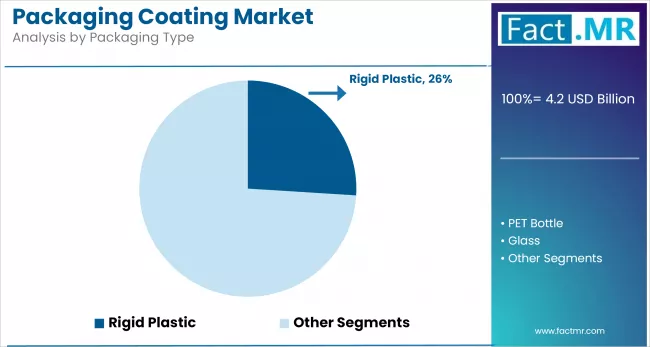

Rigid Plastic to Exhibit Leading by Packaging Type

The rigid plastic segment holds the dominant share in the packaging coating market. Rigid plastic packaging, including containers, jars, and trays, is widely used across food, beverage, pharmaceutical, and personal care industries due to its durability, lightweight nature, and cost-effectiveness.

The versatility of rigid plastics in both primary and secondary packaging, coupled with consumer preference for tamper-resistant and visually appealing packages, has sustained the dominance of this segment. Moreover, advancements in recyclable and BPA-free rigid plastics have further reinforced their market position, especially amid increasing environmental scrutiny.

The flexible plastic segment is projected to be the fastest-growing over the forecast period. This growth is driven by the rising adoption of flexible packaging formats such as pouches, wraps, and films across various industries, particularly in food, snacks, pharmaceuticals, and e-commerce shipments. Flexible plastics are valued for their lightweight, cost-efficient, and space-saving attributes. The shift toward convenience packaging, along with consumer demand for resealable, single-use, and sustainable options, is accelerating the demand for high-performance coatings in flexible packaging formats.

Roll Coating to Exhibit Leading by Technology

The roll coating segment holds the largest share in the packaging coating market, driven by its efficiency, cost-effectiveness, and ability to deliver uniform coating thickness on large surface areas. It is widely adopted in high-volume packaging operations, particularly for applications requiring consistent barrier properties and aesthetic finishes across food, beverage, and consumer goods packaging. This method supports a wide range of substrates and coating types, making it ideal for both functional and decorative packaging needs.

The spray coating segment is expected to witness the highest CAGR over the forecast period due to its ability to apply coatings on complex shapes, irregular surfaces, and high-precision applications. This technology is gaining popularity in specialized packaging sectors such as pharmaceuticals, electronics, and luxury goods, where precision, flexibility, and minimal material waste are critical. Advancements in spray systems, including electrostatic and automated spray technologies, are further enhancing the speed, efficiency, and adoption of this method.

Food & Beverage to Exhibit Leading by End-Use

The food & beverage segment holds the dominant share, accounting for the highest demand globally. This dominance is driven by the need for high-barrier, moisture-resistant, and food-safe coatings that preserve freshness, prevent contamination, and extend the shelf life of perishable products. Moreover, the increasing consumption of packaged and ready-to-eat foods, coupled with the expansion of cold-chain logistics and convenience-oriented packaging, continues to fuel strong demand for packaging coatings in this sector.

The semiconductor & electronics segment is expected to register the fastest CAGR over the forecast period. As electronic components become smaller and more sensitive to environmental factors, the need for highly specialized packaging coatings that offer superior barrier protection against moisture, static, and chemical exposure has grown significantly. These coatings help ensure the integrity of delicate circuits, microchips, and semiconductors during transport and storage.

With the rapid expansion of electronics manufacturing, particularly in the Asia Pacific and North America, and growing trends such as 5G deployment, electric vehicles (EVs), and IoT devices, the demand for high-performance, anti-corrosive, and thermally stable coatings in electronics packaging is expected to surge significantly.

Competitive Analysis

The packaging coatings market is becoming moderately competitive, with a mix of both global players and regional manufacturers. Companies compete based on product performance, innovation, regulatory compliance, sustainability, and pricing. Established players have strong global distribution networks, robust R&D capabilities, and a wide range of product portfolios catering to food, beverage, pharmaceutical, personal care, and industrial packaging sectors.

Innovation and sustainability are central to competitive strategy. Companies are heavily investing in the development of eco-friendly, low-VOC, BPA-free, and recyclable coatings, responding to tightening environmental regulations and rising consumer awareness. For example, AkzoNobel and PPG have introduced waterborne and UV-curable coatings that reduce environmental impact while maintaining durability and aesthetic appeal. These innovations give companies a competitive edge, particularly in markets like Europe and North America, where regulatory compliance is stringent and customer preferences are shifting toward sustainable packaging.

Strategic collaborations, mergers, and acquisitions are also shaping the competitive landscape. For instance, in recent years, PPG Industries expanded its market reach by acquiring specialty coating firms to enhance its position in the packaging segment.

Smaller regional players, especially in emerging markets like India, China, and Brazil, offer cost-competitive alternatives and are gaining traction through localized product offerings and faster delivery timelines. However, they often face challenges in meeting international regulatory standards and scaling up production. As a result, global giants continue to hold a competitive advantage through their technological capabilities, regulatory know-how, and broader customer base. Overall, the competitive landscape of the packaging coatings market is dynamic, innovation-driven, and increasingly influenced by sustainability trends and global regulatory developments.

Key players in the market are Axalta Coating System, DuPont, Solvay S.A, Nippon Paint, Kansai Paints, Evonik Industries, BASF SE, and other players.

Recent Development

- In July 2025, Dow introduced INNATE TF 220, a recyclable resin designed for BOPE (biaxially-oriented polyethylene) films used in flexible packaging. This innovation enhances recyclability and performance while reducing manufacturing waste.

- In June 2024, Sonoco agreed to acquire Eviosys, forming the world’s largest platform for metal food can and aerosol packaging. This integration strengthens Sonoco’s technical and commercial presence in can coatings.

Segmentation of the Packaging Coating Market

-

By Coating Type :

- Acrylic

- Epoxy

- Fluoropolymer

- Plastisol Polyurethane

- Others

-

By Packaging Type :

- Rigid Plastic Packaging Can

- PET Bottle

- Glass Flexible Plastic

- Rigid Plastic

- Liquid Carton

- Others

-

By Technology :

- Coil Sheet Coating

- Roll Coating

- Spray Coating

-

By End Use Industry :

- Food & Beverage

- Consumer Product

- Chemical

- Paints & Coatings

- Industrial Product

- Semiconductor & Electronics

- Others

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the Global Packaging Coating Market size in 2025?

The packaging coating market is valued at USD 4.2 billion in 2025.

Who are the Major Players Operating in the Packaging Coating Market?

Prominent players in the market include Axalta Coating System, DuPont, Solvay S.A, Nippon Paint, and Kansai Paints.

What is the Estimated Valuation of the Packaging Coating Market by 2035?

The market is expected to reach a valuation of USD 8.1 billion by 2035.

What value CAGR is the Packaging Coating Market Exhibit During the Last Five Years?

The growth rate of the packaging coating market is 6.1% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed