Bentonite Market Outlook (2025 to 2035)

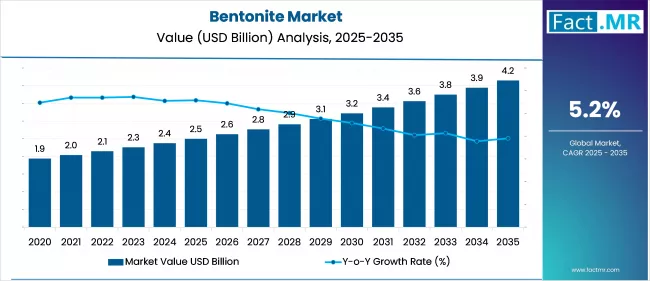

The global bentonite market is projected to increase from USD 2.5 billion in 2025 to USD 4.3 billion by 2035, with a CAGR of 5.2%, driven by increased demand in the construction, iron ore pelletizing, oil and gas, wastewater treatment, and foundry industries. Their use makes them ideal for binding, sealing, and lubricating applications across various industries, including mining, construction, and drilling.

What are the Drivers of the Bentonite Market?

The market is driven by the increasing demand for bentonite in various industrial and environmental applications. It is being used in the construction industry for slurry walls, tunneling, and foundation sealing due to its remarkable sealing and swelling properties in large infrastructure projects in Asia, the Middle East, and North America.

The steel industry serves as a key growth driver, utilizing bentonite as a crucial binder in the iron ore pelletizing process, which is essential to steel production. As the world's crude steel production, especially in India and Southeast Asia, recovers, demand for bentonite for pelletizing is expected to remain high. Bentonite-based drilling fluids are highly valued in the oil and gas sector for their ability to stabilize boreholes and control pressure, effectively meeting demand amid rising shale and offshore exploration activities.

Stricter environmental regulations are also promoting its use in landfill liners, wastewater treatment, and soil sealing, as businesses seek cost-effective and ecologically friendly methods to contain waste. The agricultural industry is also driving market expansion because bentonite is used as a carrier for fertilizers and pesticides, particularly in arid areas where moisture retention is crucial.

What are the Regional Trends of the Bentonite Market?

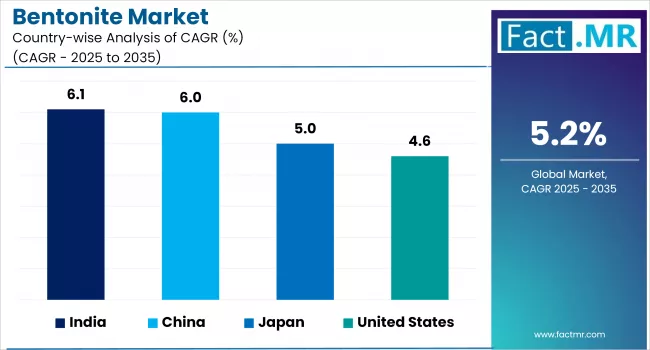

A wide range of regional factors, such as end-use sector demand, regulatory frameworks, mineral reserves, and industrial priorities, influence the global bentonite market. The Asia-Pacific region continues to lead the world in consumption due to its extensive infrastructure development, rapid industrialization, and expanding energy projects. China, India, and Indonesia are primarily to blame for this expansion, with India emerging as a key hub for both production and end-use.

Large amounts of calcium and sodium bentonite are found in India in states like Gujarat and Rajasthan. These minerals are used domestically in construction, iron ore pelletizing, and civil engineering. China's growing demand for bentonite is also a result of the nation's massive steel production, urbanization, and environmental restoration initiatives, which are funded by government-sponsored pollution control programs.

North America, led by the U.S., continues to be one of the world's largest producers and exporters of bentonite. The majority of the country's bentonite sodium bentonite, which is widely used in drilling fluids, foundry molds, and geosynthetic clay liners (GCLs), is produced in Wyoming alone. Strong demand from the oil and gas sector, especially in shale-rich basins like the Permian and Bakken, continues to support market stability. Additionally, the region's focus on environmental compliance has increased the use of landfill lining, groundwater protection, and sealing in the management of municipal and industrial waste.

Europe's top producers and consumers of bentonite are Germany, Turkey, and Greece. Germany and Turkey, in particular, have developed robust value chains that are utilized in metal casting, wastewater treatment, and tunneling projects.

Due to the EU's regulations, which strongly emphasize waste containment and circular economy practices, as well as the growing use of environmentally friendly building materials, bentonite is also gaining popularity in Western and Central Europe. Furthermore, ongoing investments in green infrastructure and water management initiatives are creating new opportunities for bentonite applications in the region.

The Middle East & Africa (MEA) region is a frontier with substantial growth potential. Countries such as South Africa, the United Arab Emirates, and Saudi Arabia are experiencing a surge in demand for bentonite due to their emphasis on water infrastructure, smart city initiatives, and urban development.

The use of bentonite in drilling fluids, tunnel boring, and foundation sealing is growing as a result of major infrastructure projects like NEOM in Saudi Arabia and ongoing metro developments in Dubai. As awareness of environmental protection and water conservation grows, bentonite is being increasingly used in Africa for landfill containment, managing mining tailings, and agricultural purposes.

Although the Latin American market is smaller overall, it is growing steadily in countries such as Argentina, Chile, Brazil, and Mexico. In Brazil, bentonite is primarily used for oilfield services and iron ore pelletizing; however, in Mexico, its applications in civil engineering, agricultural soil treatment, and cosmetics manufacturing are expanding. Bentonite consumption is expected to increase gradually over the next decade due to the region's expanding industrial base, favorable government policies, and rising foreign investment in mining and infrastructure.

What are the Challenges and Restraining Factors of the Bentonite Market?

Some operational and structural problems may limit the potential for long-term growth in the bentonite market. The reliance on dependable raw material quality and accessibility is one of the primary problems arising from the geographical concentration of bentonite mining in regions such as China, India, and the U.S. (Wyoming).

Changes in ore quality and mining disruptions, caused by land-use conflicts or environmental restrictions, can impact price and supply stability. Additionally, bentonite is logistically challenging to transport due to its bulk density and the high cost of long-distance shipping, especially in markets that are remote or export-oriented.

Increasingly strict environmental regulations relating to mining operations in North America and Europe are driving up compliance costs for producers. Additionally, the need for bentonite may be reduced in some use cases due to the availability of substitutes, such as synthetic binders in foundry applications or polymer-based sealing systems in construction.

Some developing regions may have limited market penetration due to a lack of technical know-how for specialized applications (like drilling mud formulations or geosynthetic clay liners) and a lack of awareness about the material's industrial versatility. These factors, along with the unpredictable demand from cyclical industries like construction and oil and gas, make the bentonite market vulnerable to broader economic fluctuations.

Country-Wise Outlook

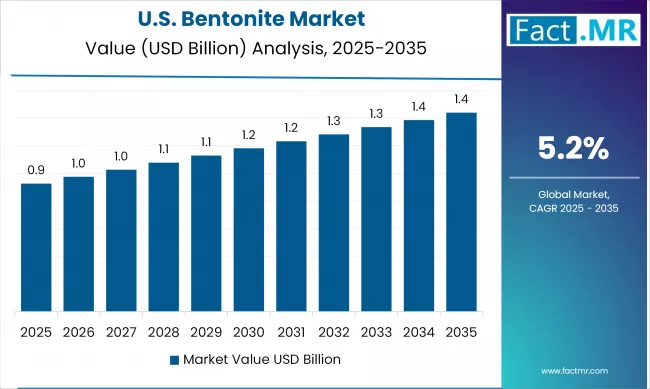

Bentonite Demand in the U.S. Strengthens Amid Industrial Recovery and Environmental Focus

The U.S. bentonite market is steadily growing due to the foundry, oil and gas, and construction sectors. The U.S. benefits from having large, superior reserves that support both exports and domestic consumption, as it is one of the world's top producers of deposits in the Fort Benton Formation of Wyoming.

Growing rig activity in North Dakota, New Mexico, and Texas is contributing to the maintenance of volume requirements for the substance, which is widely used in drilling muds for shale gas and oil exploration. The construction industry also utilizes bentonite in geotechnical engineering projects, including slurry walls and waterproofing systems for tunnels, subways, and basements.

Environmental applications are also growing as a result of stricter EPA regulations on the containment of hazardous waste in landfill liners and groundwater protection systems. Bentonite is also used as a binding agent in the iron ore pelletizing process. While demand from the iron and steel sector is smaller compared to Asia, it remains steady and reliable.

Large producers, such as Amcol Corporation (now part of Minerals Technologies Inc.), Black Hills Bentonite, and Bentonite Performance Minerals LLC, are expanding their product lines to meet evolving technical standards and client-specific performance requirements.

China’s Bentonite Market Expands on Industrial Output and Infrastructure Investment

China is a significant producer and consumer of bentonite, with vast reserves located in provinces such as Inner Mongolia, Xinjiang, and Shandong. These reserves accommodate a variety of uses in waste containment, drilling, steel production, and construction.

Bentonite is being used in slurry walls, foundation sealing, and waterproofing solutions as a result of the nation's drive to modernize its urban infrastructure, which includes high-speed rail networks, subways, and tunnels. In the meantime, bentonite is used as a pelletizing agent for iron ore sintering in China's rapidly growing iron and steel sector, which continues to rank among the largest in the world, thereby significantly increasing demand.

Opportunities for bentonite-based drilling fluids are emerging in the energy sector due to increased shale gas exploration and geothermal drilling activity. Additionally, the use of bentonite in wastewater treatment, groundwater barriers, and landfill liners has been promoted by growing environmental awareness as well as pressure from national policies like the Soil Pollution Prevention and Control Action Plan. To meet the demands of both domestic and export markets, particularly in Southeast Asia and Africa, domestic producers such as Zhejiang Fenghong New Material, Ningcheng Tianyu, and Shanxi Longyuan are expanding their operations and investing in product innovation.

Japan's Bentonite Market Grows Modestly Amid Technological Applications and Environmental Standards

Because bentonite is used in high-precision applications in industrial manufacturing, civil engineering, and construction, its demand in Japan is steady. The nation imports and processes premium bentonite mainly for geotechnical engineering projects, such as seawalls, subways, underground storage facilities, and earthquake-resistant infrastructure, despite not having as large bentonite reserves as other world leaders. Due to Japan's stringent building regulations and vulnerability to natural disasters, bentonite is often used in waterproofing and slurry trenching applications to ensure long-term structural stability.

In keeping with its solid foundation in the production of advanced materials, electronics, and automobiles, the nation also uses bentonite in ceramics, foundry operations, and specialty absorbents. The use of bentonite for waste containment systems, landfill liners, and soil sealing has steadily increased, coinciding with environmental regulations under the Soil Contamination Countermeasures Act, particularly in areas surrounding urban and industrial zones.

Prominent domestic firms, such as Suzuki Co., HOEI Mining Co., Ltd., and KUNIMINE INDUSTRIES CO., LTD., specialize in premium processed bentonite products designed for Japan's quality-conscious industrial applications. Additionally, government-funded research into low-impact building materials and partnerships with academic institutions continue to foster innovation in formulations based on bentonite.

Category-wise Analysis

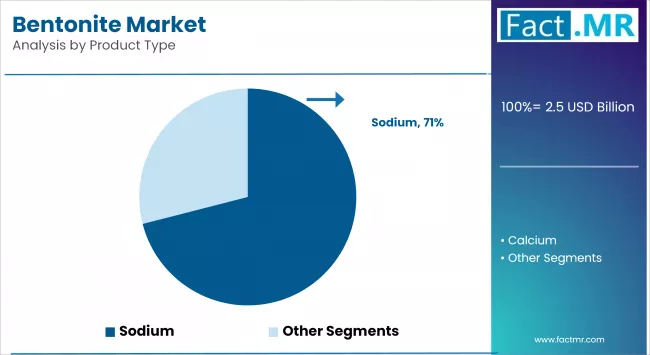

Sodium to Exhibit Leading by Product Type

Sodium bentonite dominates the bentonite market, accounting for the largest share due to its superior swelling capacity, high viscosity, and excellent water absorption properties. These qualities make it ideal for use in drilling fluids, sealants, foundry sand binders, and environmental liners. Its ability to form impermeable barriers also supports widespread use in geosynthetic clay liners for waste containment. With strong production hubs in the U.S. and India, sodium bentonite continues to drive consistent demand across multiple industrial sectors.

Calcium bentonite is a steadily growing segment, driven by its use in absorbents, pet litter, and cosmetic and pharmaceutical applications. While it does not swell as much as sodium bentonite, its high absorption and detoxification properties make it suitable for products requiring moisture control and purification. The increasing demand for natural and non-toxic ingredients in the wellness and skincare sectors, along with their industrial applications, is helping calcium bentonite gain traction, particularly in Europe and North America.

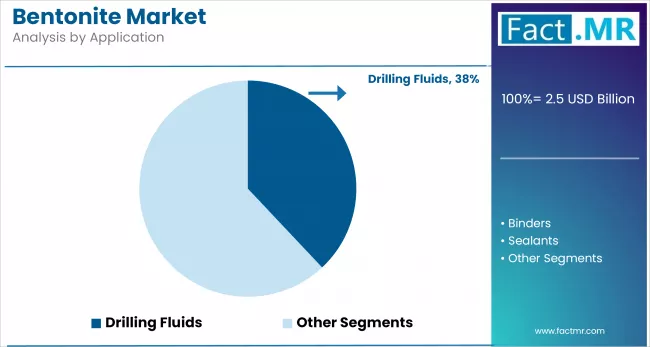

Drilling Fluids to Exhibit Leading by Application

Drilling fluids dominate the bentonite market, accounting for the largest share due to their critical role in oil and gas exploration. Bentonite’s ability to stabilize boreholes, cool drill bits, and control formation pressures makes it essential in both onshore and offshore drilling operations. Its superior viscosity and swelling properties enable efficient cuttings removal and wellbore integrity. With global drilling activities on the rise, particularly in shale and deepwater projects, the demand for high-performance bentonite-based drilling fluids continues to grow significantly.

Sealants are a steadily growing segment, driven by increasing use in construction, environmental containment, and infrastructure development. Bentonite's ability to form impermeable barriers makes it ideal for sealing landfills, ponds, dams, and tunnels. Its application in geosynthetic clay liners for waste containment is expanding as environmental regulations tighten worldwide. Additionally, demand from foundation waterproofing and underground structures is contributing to the segment’s growth, especially in urban areas with high infrastructure activity and environmental sustainability goals.

Oil to Exhibit Leading by End-use

The oil industry dominates the bentonite market, accounting for the largest share due to its extensive use in drilling operations. Bentonite is a key component in drilling muds, where it stabilizes boreholes, cools drill bits, and prevents formation fluids from entering the well. With increasing global exploration activities, particularly in shale and offshore drilling, the demand for reliable, high-performance bentonite is on the rise. Its critical function in ensuring operational efficiency and safety cements its position as a primary end-use segment.

The construction industry is a steadily growing segment, driven by rising infrastructure development and the increasing use of bentonite in tunneling, foundation sealing, and waterproofing. Its swelling and sealing properties make it ideal for forming impermeable barriers in geotechnical and civil engineering projects. Additionally, its use in slurry walls, diaphragm walls, and landfill liners is expanding, particularly in urban infrastructure and environmentally sensitive construction zones, further boosting its demand within the construction sector.

Asia Pacific Holds Leading Share in the Bentonite Market

Asia-Pacific remains the largest regional market for bentonite, supported by strong demand from the infrastructure, foundry, and iron ore pelletizing industries. India and China lead regional consumption, driven by rapid urbanization, industrialization, and large-scale steel production. India, both a top producer and consumer, with applications spanning oil well drilling, construction, agriculture, and environmental remediation. The region also benefits from low-cost labor, abundant raw materials, and expanding domestic manufacturing, positioning it as a strategic hub for both supply and consumption.

Competitive Analysis

The global bentonite market is witnessing intensifying competition, with a mix of multinational corporations, regionally specialized producers, and emerging eco-focused companies addressing a wide range of industrial applications.

This competitive landscape is largely shaped by innovation in processing technology, product purity, and performance optimization across sectors like oil and gas, foundry, construction, pharmaceuticals, and personal care. Companies offering tailored bentonite grades, sustainable sourcing practices, and value-added services such as technical support and supply chain integration are gaining a distinct competitive edge in the global market.

Companies like Wyo-Ben Inc., Black Hills Bentonite LLC, and Kutch Minerals have built strong reputations in supplying high-quality sodium and calcium bentonite, with a focus on reliability, consistent performance, and compliance with API and ISO standards. In parallel, specialty manufacturers, including CETCO (a Minerals Technologies brand), Polymer Drilling Systems Co., Inc. (PDS), and Charles B. Chrystal Co., Inc., are developing performance-enhanced formulations targeting niche markets such as geosynthetic clay liners, tunneling, and water well drilling.

In the Middle East and Asia, companies like Delmon Group of Companies and Kunimine Industries Co., Ltd. are gaining ground by serving region-specific demand in oilfield services, construction, and environmental remediation, often with competitive pricing and local technical support. Meanwhile, major service providers like Halliburton Co. are vertically integrating bentonite sourcing within their broader oil and gas operations, ensuring supply chain control and cost efficiency in drilling applications.

As global environmental regulations tighten and industries shift toward sustainable construction and waste management practices, companies are investing in mining efficiency, purification technologies, and research and development to differentiate themselves in this maturing yet essential market.

Key players in the global bentonite industry include Clariant AG, Minerals Technologies Inc., Ashapura Group, Imerys S.A. (formerly Amcol), Wyo-Ben Inc., and Bentonite Performance Minerals LLC (a Halliburton subsidiary).

Recent Development

- In June 2024, Clariant AG, a global specialty chemical company, showcased its latest bentonite-based offerings for metal casting at China’s Metal China 2024 show in Shanghai, highlighting a commitment to innovation and sustainable solutions within the foundry industry..

- In November 2023, Wyo-Ben Inc., a major producer of bentonite products, acquired the bentonite operations of M-I Swaco, a division of Schlumberger, located in Greybull, Wyoming. This acquisition significantly increased Wyo-Ben's production scale and strengthened its position in the bentonite industry.

Segmentation of the Bentonite Market

-

By Product Type :

- Sodium

- Calcium

-

By Application :

- Drilling Fluids

- Binders

- Sealants

- Absorbents

- Clarification Agents

- Others

-

By End-use :

- Oil

- Foundry

- Construction

- Food

- Pharmaceuticals

- Others

-

By Region :

- North America

- Latin America

- Europe

- APAC

- MEA

- Frequently Asked Questions -

What is the Global Bentonite Market Size in 2025?

The bentonite market is valued at USD 2.5 billion in 2025.

Who are the Major Players Operating in the Bentonite Market?

Prominent players in the bentonite market include Clariant AG, Black Hills Bentonite LLC, Kutch Minerals, Mineral Technologies Inc., Kemira OYJ, CETCO, Ashapura Group of Companies, and others.

What is the Estimated Valuation of the Bentonite Market by 2035?

The bentonite market is expected to reach a valuation of USD 4.3 billion by 2035.

What Value CAGR Did the Bentonite Market Exhibit over the Last Five Years?

The historic growth rate of the bentonite market was 4.8% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed