- Base Value(2025): 1854 Mn

- Forecast Value (2035): 2615 Mn

- CAGR (2035): 3.5%

Perchloroethylene Market Outlook (2025 to 2035)

The perchloroethylene market is valued at USD 1,854 million in 2025. As per Fact.MR's analysis, the market will grow at a CAGR of 3.5% and reach USD 2,615 million by 2035.

In 2024, the industry continued to grow, driven largely by its increased demand for dry cleaning applications. The compound's superior solvency and recyclability made it the go-to solvent for dry cleaning businesses.

The virgin form of the solvent was preferred due to its high-quality cleaning results, ability to rapidly dissolve stains and soiling from a wide range of fabrics, and efficient performance in dry cleaning machines.

Consumer demand for dry cleaning services rose as busy lifestyles and increasing disposable incomes supported higher spending on laundry services. Further the industry obtained advantages from the dry cleaning sector consistently growing. With more consumers opting for professional laundry services, the demand for effective and eco-friendly cleaning agents has increased steadily.

Looking ahead to 2025 and beyond, the industry will be sustained and, as a result, remain buoyant by the growth performance of the dry cleaning and laundry services sector. Changes could occur due to increasing awareness to environmental and health impacts that bring an inclination towards greener alternatives in the long term and, arguably, change dynamics in the industry.

Healthy future prospects for the CAGR of 4 percent will support steady long-term growth during the forecast period, especially if demand for dry cleaning remains high.

Key Metrics

| Metric | Value |

|---|---|

| Estimated Global Size in 2025 | USD 1,854 Million |

| Projected Global Size in 2035 | USD 2,615 Million |

| CAGR (2025 to 2035) | 3.5% |

Fact.MR Survey Results: Global Perchloroethylene Market Dynamics Based on Stakeholder Perspectives

(Surveyed Q4 2024, n=450 stakeholder participants evenly distributed across manufacturers, distributors, dry cleaning service providers, and regulatory bodies in the U.S., Western Europe, Japan, and South Korea)

Key Priorities of Stakeholders

- Regulatory Compliance: 84% of stakeholders globally identified compliance with environmental regulations as a "critical" priority. Stricter standards on chemical usage, waste management, and emissions are driving the demand for sustainable alternatives.

- Efficiency and Cost Reduction: 72% of stakeholders highlighted the need for more cost-effective chemical solutions to maintain operational efficiency and profit margins. With increasing competition in the dry cleaning sector, companies are focusing on improving resource efficiency and reducing operational costs.

Regional Variance:

- U.S.: 70% emphasized the growing importance of developing eco-friendly substitutes due to mounting environmental concerns and stricter state-level regulations.

- Western Europe: 88% prioritized sustainability, particularly the use of recyclable and biodegradable alternatives, driven by the EU’s stringent regulations on chemical disposal and carbon footprint.

- Japan/South Korea: 62% focused on reducing space and energy consumption in dry cleaning operations, with increasing demand for energy-efficient systems and smaller chemical usage due to high real estate costs.

Adoption of Sustainable Alternatives and Technological Advancements

High Variance:

- U.S.: 57% of dry cleaning service providers have begun experimenting with sustainable cleaning agents, such as liquid carbon dioxide and silicone-based solutions. The shift is largely driven by local regulatory pressure and consumer demand for eco-friendly options.

- Western Europe: 65% of stakeholders use advanced filtration and water-recycling systems to complement their use of conventional solvents, which is expected to decrease reliance on traditional chemicals.

- Japan: Only 30% of dry cleaners have started integrating alternative solvents, primarily due to cost concerns and the high initial investment required for new technologies.

Convergent and Divergent Perspectives on ROI:

- 71% of U.S. stakeholders consider the switch to eco-friendly alternatives to be "worth the investment" for long-term sustainability and regulatory compliance. In comparison, 40% in Japan still prefer traditional methods due to perceived cost-effectiveness.

Material Preferences and Chemical Alternatives

Consensus:

- Solvent-based cleaning remains the most preferred method for dry cleaning, selected by 66% of stakeholders globally due to its proven effectiveness in stain removal and fabric care.

Regional Variance:

- Western Europe: 58% of stakeholders have begun exploring alternatives, with 45% opting for more sustainable options such as wet cleaning or CO2-based solvents, driven by environmental regulations and shifting consumer preferences.

- U.S.: 72% of stakeholders still rely on traditional solvents, but 40% in California have started exploring alternative cleaning methods as state regulations around chemical emissions become more stringent.

- Japan/South Korea: 50% of dry cleaners are testing hybrid systems combining conventional and biodegradable options to balance performance and environmental impact.

Price Sensitivity and Economic Challenges

Shared Challenges:

- 88% of stakeholders cited rising material costs (solvents and alternative cleaning agents) as a significant challenge. Increased raw material costs, particularly for eco-friendly alternatives, are putting pressure on profit margins in the dry cleaning industry.

Regional Differences:

- U.S.: 64% of stakeholders would be willing to pay a 15-20% premium for eco-friendly chemical solutions, while 40% are still hesitant, focusing on cost control due to competitive pricing pressures.

- Western Europe: 75% are willing to pay a premium for green solutions, reflecting the region’s strong commitment to sustainability and regulatory compliance.

- Japan/South Korea: 55% prefer low-cost alternatives, especially in smaller businesses, where upfront investments in sustainable technologies are harder to justify.

Pain Points in the Value Chain

Manufacturers:

- U.S.: 60% cited challenges with fluctuating raw material prices for both traditional and alternative chemicals, affecting production timelines.

- Western Europe: 53% struggled with sourcing sustainable materials that meet regulatory standards, which delays product development and increases costs.

- Japan: 50% faced difficulties in meeting demand due to a lack of local production capabilities for sustainable chemicals.

Distributors:

- U.S.: 67% faced delays in delivery from international suppliers of alternative solvents.

- Western Europe: 55% cited logistical challenges in distributing eco-friendly chemicals due to complex regulatory approvals.

- Japan/South Korea: 58% highlighted the lack of a consistent supply of green alternatives, impacting their ability to meet demand.

End-Users (Dry Cleaners):

- U.S.: 45% cited high maintenance costs associated with eco-friendly systems as a significant issue.

- Western Europe: 39% noted that adapting to new chemical solutions has resulted in higher operational costs.

- Japan: 55% expressed concerns over the complexity and training requirements associated with new technologies and green solutions.

Future Investment Priorities

Alignment:

- 70% of global manufacturers plan to invest in research and development of sustainable chemical solutions over the next 2-3 years.

Divergence:

- U.S.: 63% are focusing on improving the performance and cost-effectiveness of sustainable solvents, while Western Europe (70%) is prioritizing the development of green technologies and reducing the carbon footprint of their operations.

- Japan/South Korea: 58% are investing in hybrid systems that combine traditional and alternative chemicals to balance performance and environmental impact.

Regulatory Impact

- U.S.: 68% of stakeholders stated that state-level regulations on chemical emissions, such as California’s Proposition 65, significantly impacted their purchasing and operational decisions.

- Western Europe: 80% viewed the EU’s Green Deal and chemicals strategy as both a challenge and an opportunity to innovate and grow within the green chemicals sector.

- Japan/South Korea: 38% felt that local regulations had a minimal effect on their purchasing behavior, with most stakeholders noting the lack of strong enforcement in these regions.

Conclusion: Variance vs. Consensus

High Consensus:

- Environmental compliance, cost reduction, and material efficiency are common priorities for stakeholders worldwide.

Key Variances:

- U.S.: Focus on integrating eco-friendly alternatives while balancing costs.

- Western Europe: Strong leadership in sustainability, prioritizing green solutions.

- Asia (Japan/South Korea): Preference for hybrid models that combine cost efficiency with environmental considerations.

Strategic Insight:

A "one-size-fits-all" approach will not succeed. Regional adaptations (e.g., sustainability in Europe, cost-efficiency in Asia, regulatory compliance in the U.S.) are necessary to capture share effectively.

For a deeper understanding of industry trends and actionable insights, connect with Fact.MR today and refine your strategy for the evolving global perchloroethylene landscape.

Impact of Government Regulations

| Country | Impact of Policies and Government Regulations |

|---|---|

| United States | State-Level Regulations: Various states, particularly California, have stringent regulations around chemical emissions, including Proposition 65, which requires warnings about harmful substances. EPA Regulations: The U.S. Environmental Protection Agency (EPA) enforces regulations regarding the safe disposal and handling of certain solvents, leading to increased scrutiny of their use in industries like dry cleaning. Mandatory Certifications: Companies must ensure compliance with EPA’s Toxic Substances Control Act (TSCA) for chemical safety, as well as adhere to local state-level air quality standards. |

| European Union | EU Green Deal: The European Union's Green Deal and its related REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) regulations are pushing for a shift towards more sustainable chemical alternatives, impacting solvent usage. Carbon Footprint Regulations: The EU is implementing stricter rules on the carbon footprint of manufacturing processes, which may increase costs for businesses relying on certain chemical substances. Mandatory Certifications: Companies operating in the EU need to comply with REACH for chemical registrations and obtain CE marking for products to meet safety and environmental standards. |

| Japan | Chemical Control Laws: Japan enforces the Chemical Substances Control Law (CSCL), which mandates the proper handling, usage, and disposal of hazardous chemicals. Environmental Regulations: There are stringent rules around air pollution and water discharge, pushing for the reduction of harmful chemical usage in industries like dry cleaning. Mandatory Certifications: Companies must adhere to Japan's Industrial Safety and Health Act, ensuring safety standards for the use of hazardous chemicals and obtaining necessary safety certifications. |

| South Korea | National Chemical Control Act: South Korea regulates the use of chemicals through the Chemical Control Act, which requires businesses to monitor hazardous substances and reduce exposure to harmful materials. Regulation on Waste and Emissions: There are specific regulations regarding the disposal of chemicals and the reduction of emissions from industrial processes, particularly in the dry cleaning sector. Mandatory Certifications: Companies need to ensure compliance with K-REACH (Korea REACH), which mandates chemical substance registration, and ISO 14001 for environmental management practices. |

| China | Regulations on Chemical Safety: China has introduced policies to regulate chemicals in industrial applications, with an emphasis on improving environmental safety. The Environmental Protection Law requires companies to reduce their usage of hazardous substances. Air Quality Regulations: China enforces strict regulations around air pollution, which impacts the use of volatile organic compounds (VOCs) in various industries. Mandatory Certifications: Companies must comply with the China Compulsory Certification (CCC) for chemical safety and obtain necessary environmental permits for handling certain substances. |

| Australia | National Industrial Chemicals Notification and Assessment Scheme (NICNAS): Australia regulates industrial chemicals under NICNAS, which requires businesses to assess and report the chemicals they use. Environmental Regulations: Similar to other regions, Australia is pushing for more sustainable practices, with new regulations aimed at reducing VOC emissions from dry cleaning and industrial sectors. Mandatory Certifications: Companies need to comply with AS/NZS ISO 14001 for environmental management systems and Workplace Health and Safety Regulations to ensure safe chemical handling. |

Market Analysis

The industry is set for steady growth, driven by rising demand in dry cleaning applications due to its efficient solvency and superior cleaning performance.

As the dry cleaning and laundry services sector expands, businesses using traditional solvents will continue to benefit.

However, increasing environmental concerns may push for more sustainable alternatives in the long run. Companies that adapt to eco-friendly solutions will be better positioned to thrive as industry dynamics evolve.

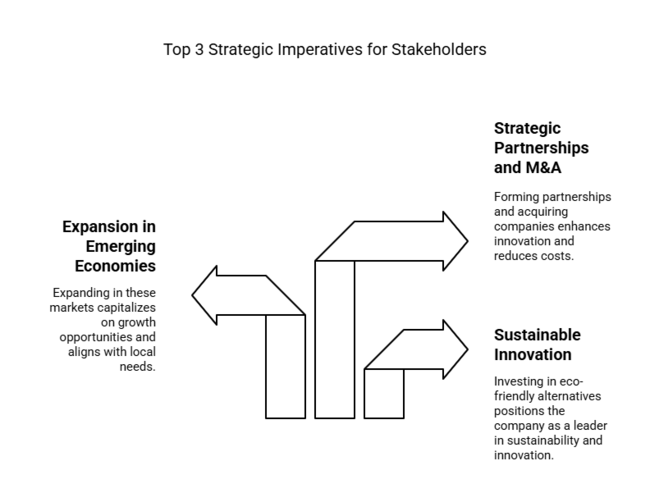

Top 3 Strategic Imperatives for Stakeholders

Sustainable Innovation

Executives should invest in research and development of eco-friendly alternatives to traditional solvents to stay ahead of regulatory trends and consumer demand for greener solutions. Developing sustainable cleaning chemicals can help mitigate the risk of environmental backlash while positioning the company as a leader in innovation.

Expansion in Emerging Economies

Focus on expanding the footprint in emerging economies where dry cleaning and laundry services are rapidly growing due to rising disposable income and urbanization. Align product offerings with the specific needs of these economies, including addressing local regulatory and environmental concerns.

Strategic Partnerships and M&A

Explore partnerships with technology companies and invest in mergers and acquisitions that allow for greater innovation in chemical processes and sustainability. Strengthening ties with key distributors and expanding production capacity can help meet growing demand and reduce operational costs, ensuring long-term competitiveness.

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability & Impact |

|---|---|

| Regulatory Changes - The potential for significant shifts in environmental laws, chemical usage regulations, and industry standards. The risk includes heightened compliance costs, operational disruptions, or product reengineering to meet evolving legal frameworks. | High Probability, High Impact |

| Shift to Eco-friendly Alternatives - The growing trend towards sustainable and biodegradable chemicals in dry cleaning and industrial cleaning sectors could reduce demand for traditional solvents. Companies will need to adapt to this shift, investing in green alternatives and improving environmental profiles to remain competitive. | Medium Probability, High Impact |

| Economic Downturn Impacting Consumer Spending - A global or regional economic slowdown could reduce consumer spending on dry cleaning services, directly affecting demand for conventional cleaning solvents. Companies need to monitor economic trends closely to adjust pricing strategies and maintain industry stability during lean periods. | Medium Probability, Medium Impact |

Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Sustainable Alternative Development | Run feasibility studies on sustainable and biodegradable chemical alternatives to conventional solvents. Conduct research to assess consumer and regulatory demand for green alternatives and evaluate potential suppliers. |

| Regulatory Compliance Strategy | Initiate proactive engagement with policymakers to track upcoming regulatory changes affecting solvent use. Prepare for compliance with stricter environmental regulations by planning necessary product adjustments and certifications. |

| Economic Impact Monitoring | Monitor global economic indicators and consumer behavior to assess potential impacts on dry cleaning demand. Adjust pricing models and marketing strategies to maintain stability in case of economic downturns or fluctuations. |

For the Boardroom

To stay competitive and mitigate risks, companies must prioritize investment in sustainable alternatives, prepare for stricter environmental regulations, and shift consumer preferences toward greener solutions. Proactively engaging with policymakers and tracking regulatory developments will ensure smooth compliance while diversifying sourcing strategies can mitigate supply chain risks.

Additionally, closely monitoring economic trends and adjusting pricing and service offerings will help maintain stability amid potential downturns. This intelligence should prompt the client to accelerate innovation in eco-friendly solutions, strengthen partnerships with key stakeholders, and align their product development roadmap with both regulatory and industry shifts, ensuring long-term growth and resilience.

Segment-wise Analysis

By Application

Hydrofluorocarbon (HFC) production is expected to grow at 3.8% CAGR from 2025 to 2035, driven by the need for refrigerants in air conditioning and refrigeration. As an intermediate, certain chemical compounds play a crucial role in the synthesis of HFCs, where they act as key feedstocks for producing refrigerants and refrigerant blends. In 2019, HFC applications accounted for nearly three-quarters of global solvent consumption.

Despite growing regulatory pressure on HFCs due to environmental concerns, the demand for refrigerants in emerging regions and the increasing use of air conditioning systems continue to support this segment's growth. However, future expansion may face challenges as more sustainable alternatives such as hydrofluoroolefins (HFOs) gain traction.

By Grade

The fluorocarbon grade segment, where specific chemicals are used as feedstocks for producing refrigerants and other fluorinated compounds, is expected to grow at 3.9% CAGR from 2025 to 2035. This segment benefits from strong demand for refrigeration, air conditioning, and industrial processes.

Fluorocarbon-grade solvents play a critical role in the production of hydrofluorocarbons (HFCs) and other fluorinated chemicals. These chemicals are essential for cooling systems worldwide.

However, the growth of this segment is being challenged by the rising adoption of eco-friendly refrigerants such as HFOs. Despite this, the ongoing industrial demand, particularly in emerging regions, will continue to support growth in the fluorocarbon grade segment.

By Function

The isomerization and reforming segment, used primarily in the chemical industry for refining purposes, is anticipated to grow at a 3.0% CAGR from 2025 to 2035.

Certain solvents act as stabilizers in specific chemical processes, particularly in petroleum refining and polymer production. Their stability and effectiveness in high-temperature processes make them essential for refining crude oil and natural gas.

While this segment’s growth is steady, it faces competition from other solvents and increasing environmental regulations. The industry will likely continue to see demand from established refining sectors, though innovation in sustainable solvents will be key to the future of this application.

Country-wise Insights

U.S.

The U.S. is expected to grow at a 3.2% CAGR from 2025 to 2035, slightly below the global average due to increasing regulatory restrictions. The EPA has tightened regulations on volatile organic compounds (VOCs), prompting shifts towards alternative solvents in dry cleaning applications.

However, demand remains robust in industrial applications, particularly for metal degreasing and automotive industries. These sectors continue to rely on high-efficiency solvents for precision cleaning.

Regulatory pressures like VOC restrictions may impact future demand, but industrial usage in sectors like aerospace and heavy machinery will support steady growth. Companies must focus on compliance and innovative solutions for continued success.

UK

The UK is projected to grow at 3.1% CAGR from 2025 to 2035, driven by sustainability regulations. Post-Brexit REACH compliance and environmental initiatives are pushing businesses towards eco-friendly alternatives in dry cleaning.

Nevertheless, industrial applications such as metal degreasing and cleaning for automotive and electronics sectors will continue to show stable demand. Given the push for low-VOC solvents, businesses should focus on innovative solutions and maintaining compliance with environmental regulations to stay competitive.

France

France is expected to grow at 3.0% CAGR from 2025 to 2035, driven by increasing demand for sustainable solutions and strict environmental regulations. The push for green chemistry and compliance with REACH is encouraging businesses to explore alternatives.

However, industrial applications such as automotive and precision cleaning will continue to support demand. The need for high-efficiency solvents in specialized manufacturing remains strong. Companies must focus on eco-friendly innovations and ensure alignment with France’s environmental policies to remain competitive in the long term.

Germany

Germany is set to grow at 3.3% CAGR from 2025 to 2035, supported by strong demand from industrial sectors and environmental regulations. The country’s focus on sustainability and the circular economy is pushing companies toward eco-friendly solvents.

Despite these challenges, the automotive and electronics industries continue to use high-efficiency solvents for cleaning. Companies must comply with REACH regulations and invest in green chemistry to maintain their competitive edge while meeting sustainability goals.

Italy

Italy’s demand is expected to grow at 3.0% CAGR from 2025 to 2035, with steady industrial applications in metal degreasing and specialized manufacturing. EU regulations are encouraging the adoption of eco-friendly alternatives, which could impact solvent usage in dry cleaning.

Nevertheless, the automotive and machinery industries will remain strong drivers of demand. Italy's industries continue to require high-efficiency solvents for cleaning and precision applications. To succeed, companies must focus on sustainable alternatives and ensure compliance with the EU’s environmental policies to stay competitive in this evolving sector.

South Korea

South Korea is expected to grow at 3.4% CAGR from 2025 to 2035, driven by automation and industrial applications. The country's electronics and automotive industries continue to use high-efficiency solvents for precision cleaning.

Regulatory changes regarding chemical safety are shaping demand, but industrial applications remain heavily reliant on these solvents. Robotic and IoT advancements also continue to drive innovation in manufacturing processes. The adoption of new technologies and compliance with K-REACH and other green chemistry regulations will drive growth.

Japan

Japan is projected to grow at 2.8% CAGR from 2025 to 2035, influenced by a slower shift towards automation and evolving regulations. Despite regulatory pressures to reduce VOCs, industrial sectors like electronics and automotive manufacturing still heavily rely on high-efficiency solvents.

However, small-scale farming and the preference for cost-effective solutions may limit growth in certain segments.

The growth will benefit from continued industrial demand but must navigate stricter environmental regulations and cost challenges. Companies must innovate with eco-friendly alternatives and comply with local regulatory requirements.

China

China is projected to grow at 4.0% CAGR from 2025 to 2035, driven by rapid industrialization and a growing demand for high-efficiency solvents. The automotive, aerospace, and electronics sectors are major consumers in China, where precision cleaning is crucial.

Regulations on hazardous chemicals are tightening, but industrial growth continues to drive demand for these solvents in sectors like metal degreasing. To succeed, companies must focus on compliance with China's Chemical Safety Law and invest in environmentally friendly solutions and sustainable chemical handling technologies.

Market Share Analysis

Occidental Petroleum (OxyChem): 28-33%

OxyChem is expected to maintain its leadership but face slight share erosion due to the accelerated dry-cleaning phase-outs in North America. In 2025, the company will focus on carbon capture integration at its Louisiana plant to reduce Perc production emissions. A new metal-degreasing-grade Perc formulation is under development to cater to aerospace demand.

Dow Chemical: 22-27%

Dow is projected to gain a share in 2025 with its "Green Perc” initiative, replacing traditional solvent processes with bio-based, chlorinated alternatives in Europe. Its Texas plant will pilot AI-driven distillation optimization, cutting energy use by 15%. Regulatory filings suggest Dow may acquire a smaller solvent recycler to bolster closed-loop systems.

PPG Industries: 11-14%

PPG’s 2025 strategy focuses on high-purity Perc for electronics cleaning, targeting semiconductor clients in Taiwan and South Korea. A joint venture with SK Materials is expected to secure the lithium battery supply chain demand. PPG will also debut a low-residue Perc variant specifically for precision aerospace applications. The company is investing in an electrochemical Perc synth.

Kanto Denka Kogyo: 9-13%

Kanto Denka will expand its Osaka facility’s output by 20% in 2025 to meet surging Asian demand for metal fabrication solvents. The company is testing a new stabilizer formula aimed at extending Perc's shelf life and addressing logistics challenges in Southeast Asia.

Gujarat Fluorochemicals Ltd (GFL): 7-10%

GFL’s 2025 growth will be driven by its new Mumbai export hub, targeting Middle Eastern and African markets. The company is investing in electrochemical Perc synthesis to decrease its reliance on ethylene feedstocks. A long-term contract with India’s defense sector for aerospace-grade Perc is being negotiated.

Solvay SA: 4-6%

Solvay’s European Perc sales will decline further in 2025 due to the EU’s proposed 2026 dry-cleaning ban. However, its Airbus contract for flame-retardant Perc formulations will offset losses. Solvay plans to divest two aging Perc plants and focus on specialty applications.

Others (Tokuyama, AkzoNobel, Befar Group): 9-14%

- Tokuyama: Will launch a Prec recycling consortium with Panasonic and Sony to recover Perc from electronics waste.

- AkzoNobel: Shifts entirely to industrial-grade Perc after exiting consumer industries. Testing solvent recovery drones for offshore metal cleaning.

- Befar Group: China’s new environmental rules may force temporary plant closures; however, Befar’s coal-based Perc process could lower costs if approved.

Key Companies

- Dow Chemical Company

- BASF SE

- Honeywell International Inc.

- ExxonMobil Chemical Company

- LyondellBasell Industries N.V.

- Solvay SA

- Shin-Etsu Chemical Co., Ltd.

- The Chemours Company

- Mitsui Chemicals, Inc.

- AkzoNobel N.V.

- INEOS Group

- Zhejiang Materials Industry Group Co., Ltd.

- Arkema SA.

- Aditya Birla Chemicals

- Kureha Corporation

- Reliance Industries Limited

- AGC Inc.

- Befar Group

- INOVYN ChlorVinyls Limited

- Kanto Denka Kogyo Co., Ltd.

- Occidental Chemical

- Olin Corporation

- Spolchemie

- SRF Limited

- Westlake Chemical Corporation

- PPG Industries

Perchloroethylene Market Segmentation

By Function :

By function, the industry is segmented into intermediate, solvent, isomerization & reforming, and others.

By Grade :

In terms of grade, the industry is segmented into fluorocarbon grade, degreasing & general purpose, industrial grade, and others.

By Application :

Based on application, the industry is segmented into hydrofluorocarbon, dry cleaning, metal cleaning & degreasing, isomerization & reforming, and others.

By Region :

The industry is segmented by region into North America, Latin America, Western Europe, South Asia & Pacific, East Asia, Middle East, and Africa.

- Frequently Asked Questions -

What are the primary uses of perchloroethylene?

It is primarily used as a solvent in dry cleaning and metal cleaning, as well as as an intermediate in the production of hydrofluorocarbons.

How does the demand for perchloroethylene vary by region?

Demand for this chemical varies based on regional industries, with the U.S. focusing on dry cleaning and industrial uses and Europe emphasizing sustainability.

What factors are driving the growth of perchloroethylene consumption?

Growth is driven by its versatile applications in various industries, along with increasing regulatory focus on cleaning agents and sustainability.

Are there any environmental concerns associated with perchloroethylene?

Yes, it is a volatile organic compound (VOC) linked to environmental concerns like water and soil contamination.

What are the key challenges in the production of this industry?

Challenges include rising raw material costs, stringent environmental regulations, and the growing demand for eco-friendly alternatives.