Chillers Market Outlook (2025 to 2035)

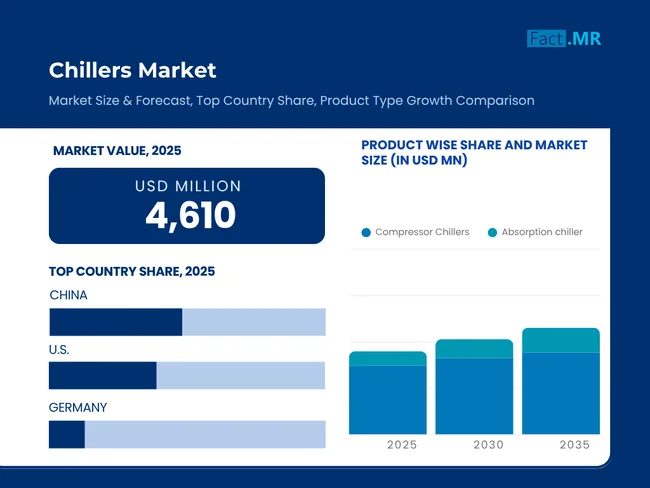

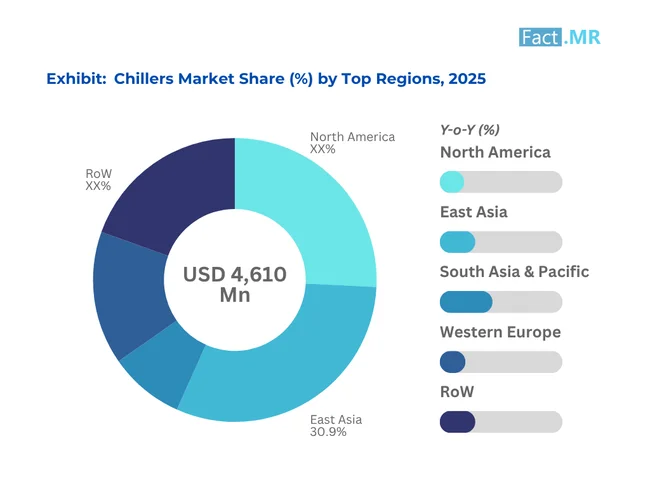

The global chillers market is expected to reach USD 6,256.3 million by 2035, up from USD 4,610.3 million in 2025, reflecting a projected CAGR of 3.1% over the forecast period.

The increased need for precise temperature adjustments in data centers, hospitals, and high-reliability production remains a driving force behind the liberalization of chillers. Nonetheless, regulatory pressure in terms of refrigerant use and the overall energy efficiency of the life cycle is changing procurement trends and the architecture (of systems) in all end-use sectors.

What is driving demand for chillers globally?

The use of chillers has become necessary to provide centralized cooling of temperature-sensitive systems. Chilled water systems, at commercial scales, are being pursued for their ability to deliver space- and scale-efficient solutions across various sectors, from corporate offices to hospitality and data centers.

The higher capacity and the capacity to resist loads in industrial sectors, on its part, has increased the demand of water-cooled and screw- type chillers, mainly in the chemical, food and beverage, plastics and automotive industries wherein per ton of cooling capacity is less expensive to install compared with the installed capacity of other chillers.

At the same time, a limited set of refrigerants is about to change, due to the relaxation of refrigerant rules under the Kigali Arrangement and local phase-out plans (e.g., the India HCFC Phaseout Management Plan and the U.S. AIM Act).

Manufacturers have responded by integrating variable-speed compressor technologies, adaptive control logic, and modularity to meet both regulatory and cost-effectiveness requirements.

What are the regional dynamics of the Chillers Market?

Methodical retrofit activity dominates commercial HVAC in North America. Industrial adoption is fragmented and constrained due to capital budgeting cycles and regional climate zoning codes; industrial adoption is slowly moving away from fragmentation.

Europe has long been a leader in the deployment of centrifugal and scroll chillers in public infrastructure and district cooling operations. The building sector has been pushed with the Energy Performance of Buildings Directive (EPBD), further ensuring enforcement of F-gas regulations to limit the use of high-GWP refrigerants.

Construction in China and manufacturing capacity in India, Vietnam, and Thailand. Newly built data centers in Singapore and Japan, along with augmented procurement, have somewhat supported demand for scroll and modular air-cooled chillers. Backing the procurement, while not directly, government programs such as India’s Cooling Action Plan, as well as China’s promotion of green industrial parks, add to the procurement support.

What are the challenges and restraining factors of Chillers Market?

Capital cost remains the most constraining factor, particularly for centrifugal and absorption chillers, which require higher upfront investment and larger installation infrastructure. GWP compliance also necessitates regular retrofitting and cyclical replacement of coolants, further increasing the lifecycle costs.

Operational risks arise from under-performance under part-load conditions due to fixed-speed compressors, which have made part-load performance a concern in variable-load applications, such as data centers and hospitals, where demand rates fluctuate unpredictably.

Lastly, unresolved standardization issues persist in emerging economies, particularly regarding the integration of building codes, access to refrigerants, and post-installation support infrastructure. Several developing markets continue to address this lack of servicing expertise and spare part incompatibility.

Country-Wise Outlook

United States enforces low-GWP transition through regulatory compliance and federal grants.

-2025-to-2035.webp)

Relying on the EPA SNAP Rule 23 and AIM Act mandates, manufacturers and institutional buyers in the United States hastened the transition toward chillers utilizing R-454B, R-1234ze(E), and R-513A. Federal procurement is giving preference to products conforming to AHRI 550/590 standards and ASHRAE 90.1 energy codes. Here, hybrid chiller integration is further aided while capital barriers are reduced through cooling-as-a-service contracts in municipal facilities.

Germany reinforces the water-cooled segment through industrialized decarburization targets

Under its National Industrial Strategy 2030, Germany's chiller market is driven by the decarbonization of industrial process heat. The chemical and discrete manufacturing sectors are investing in screw and absorption chillers with thermal energy recovery units. In urban areas, the low noise and compactness of the system are enforced under zoning constraints, and the increasing use of R717 (ammonia) is observed due to its zero-GWP and non-flammable properties, notwithstanding concerns about toxicity.

Scroll and screw chillers are supported in China for installation under smart factory policies

In support of the "Made in China 2025" industrial upgrade plan, the PRC government provides subsidies toward setting up high-efficiency cooling systems. In manufacturing hubs, chillers with R410A and R448A are specified, whereas Tier 1 city projects require a greater number of modular air-cooled systems. The Ministry of Ecology and Environment in China is experimenting with refrigerant recovery zones to prevent illegal emission of refrigerants, bringing the secondary market into compliance.

Category-Wise Analysis

Scroll and screw chillers continue to dominate mid- to high-capacity usage

Scroll chillers are generally preferred for commercial buildings and small data centers because they are small with high partial-load COPs. However, screw chillers are primarily used in industrial operations that require continuous operation at high thermal loads, particularly in applications such as food processing, chemical production, and plastics manufacturing.

Demand centered between the 50–150 ton segment

The cooling capacity range of 50 to 150 tons remains the core demand band, accounting for the majority of installations across hospitals, hotels, and commercial buildings. Larger systems (greater than 150 tons) are typically deployed in heavy process industries or centralized utilities. Below 30 tons, packaged air conditioners remain more prevalent than chillers.

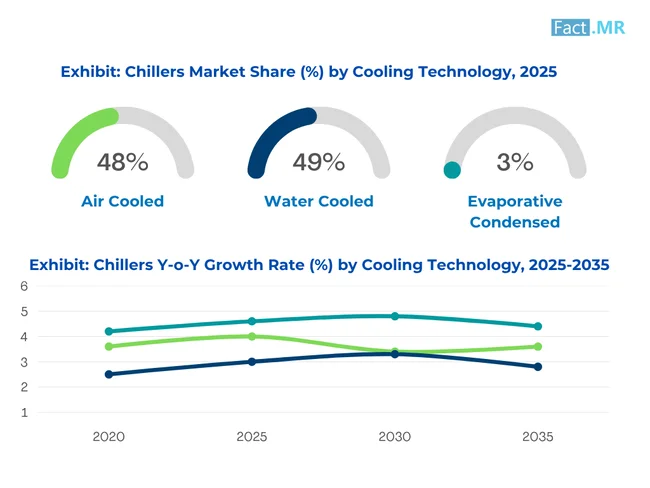

Water-cooled systems remain dominant, but air-cooled systems are gaining in urban settings

Water-cooled types are more efficient, particularly in systems characterized by low ambient temperatures and those with high load variations. Air-cooled systems are, however, gaining popularity in crowded urban areas and for retrofit solutions, as they are easier to site and require reduced initial infrastructure requirements.

Competitive Analysis

The chillers market is a highly concentrated industry, where world-leading companies account for more than 60 percent of the value. The most important competitive levers present are refrigerant flexibility, energy efficiency, adaptive control algorithms and modularity.

Technology platforms are also being perfected that enable multi-refrigerant compatibility, enabling end-user operators to choose in line with changing F-gas regulations. Large manufacturers have developed designs for compressors that offer variable-speed and magnetic bearing solutions to improve partial-load efficiency.

Strategic differentiation is also visible in after-sales support networks. OEMs with predictive maintenance services and real-time performance dashboards are gaining share in the institutional segment. In cost-sensitive sectors, value engineering and lower service cost per hour continue to shape procurement decisions.

To reduce lead time and comply with regional codes, firms are implementing regional assembly and custom configuration across the board to optimize costs. For example, production lines in the U.S. are optimized using AHRI-registered scroll units, whereas European production is ramping up based on ammonia-based large-tonnage systems.

The current consolidation of HVAC companies has also led to the standardization of products across different parts of the globe. Nevertheless, there is a risk of price erosion, particularly in markets such as South Asia and Latin America, where the second-tier would compete on a volume basis without much differentiation in terms of technology.

Major players in the chillers industry include Carrier, Trane Technologies, Johnson Controls, Daikin Industries, LG Electronics, Mitsubishi Electric, GEA Group, Blue Star Ltd., MTA SpA, and Smart Chiller Group.

Recent Development

- January 2025 - Daikin released the VRX-series scroll chiller, featuring a built-in inverter compressor and multi-refrigerant control of R-32 and R-1234yf.

- August 2024 -Johnson Controls announced a collaboration with the U.S. DOE to pilot the ultra-low GWP centrifugal chillers under real-time load conditions.

Methodology and Industry Tracking Approach

Fact.MR conducted a comprehensive 12-month study (June 2024 to May 2025) across 19 countries, combining demand-side and supply-side data. Over 6,300 respondents participated, including facilities engineers, HVAC planners, procurement directors, and maintenance specialists from sectors such as data centers, chemical plants, hospitals, and automotive factories.

Primary research focused on evaluating:

- Cooling system replacement cycles

- Refrigerant migration timelines

- Energy usage patterns under partial-load conditions

- Control system compatibility with Building Management Systems (BMS)

Secondary validation was carried out through:

- Compliance data from the EPA (U.S.), the EU F-Gas Regulation, India’s Ozone Cell, and national building codes

- Energy efficiency guidelines from ASHRAE, AHRI, and Eurovent Certification

- Supplier-level analysis from OEM annual reports and verified performance data sheets

Technology benchmarking was performed across six compressor architectures, comparing system COPs, operating costs, and refrigerant transitions. Chillers using R290, R717, and R1234ze(E) were examined for lifecycle costs and safety trade-offs.

Since 2016, Fact.MR has tracked the chillers market under its broader Industrial HVAC & Building Utilities Program, focusing on equipment lifecycle analysis, refrigerant regulation response, and capacity deployment across smart infrastructure projects.

Segmentation of Chillers Market

-

By Product :

- Compressor Chillers

- Screw

- Centrifugal

- Scroll

- Reciprocating

- Absorption Chillers

- Compressor Chillers

-

By Capacity :

- Up to 30 Ton

- 30 – 50 Ton

- 50 – 70 Ton

- 70 – 100 Ton

- 100 – 150 Ton

- Above 150 Ton

-

By Cooling Technology :

- Air Cooled

- Water Cooled

- Evaporative Condensed

-

By Coolant Type :

- R134A

- R744

- R717

- HCFC (R22, R123, R124, R151)

- HCS (R600A, R290)

- R407C

- R404A

- R410A

- R448A

- R449A

- Others

-

By End Use Sector :

- Commercial

- Corporate Offices

- Data Centers

- Hospitality

- Industrial

- Chemical & Petrochemical

- Healthcare

- Plastics & Polymers

- Food & Beverage

- Oil & Gas

- Energy & Power

- Automotive

- Discreet Manufacturing

- Commercial

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the expected market size of chillers in 2025?

The market is estimated to reach USD 4,610.3 billion by 2025.

What is the forecasted valuation by 2035?

The global chillers market is projected to reach USD 6,256.3 billion by 2035.

Who are the key manufacturers in this market?

Major players include Trane, Carrier, Johnson Controls, Daikin, Mitsubishi Electric, LG, Blue Star, Midea, and GEA Group.

Which cooling capacity segment dominates demand?

Chillers within the 50–150 ton range account for the majority of commercial and institutional installations.

Author:

Shubham Patidar

Editor:

Naved Ahmed