Dust Extraction System Market Outlook (2025 to 2035)

The global dust extraction system market is projected to be valued at USD 7.8 billion by 2025. As per Fact.MR analysis predicts that the dust extraction system will grow at a CAGR of 6.1% and reach USD 14.1 billion by 2035.

In 2024, the dust extraction system industry experienced a phase of calibrated recovery, influenced by fragmented industrial operations across high-emission sectors. As analyzed by Fact.MR, temporary slowdowns in the global manufacturing value chain mainly affected construction and metal-working clusters in Southeast Asia and Eastern Europe, restraining volume growth.

Simultaneously, due to hygiene and compliance pressures in post-pandemic facility audits, the food processing and pharmaceutical industries have shown a steady rate of adoption for mobile and centralized extraction units.

An uptick in fine particulate matter regulation enforcement by national environmental agencies catalyzed replacement demand for outdated systems, especially in European Union and North American factories. However, hesitancy in capital expenditure among small and mid-sized firms stalled large-scale retrofits, leading to uneven penetration of HEPA-based extractors and wet scrubbers.

In 2025, Fact.MR believes that the very dynamics of the environment will enter a safer and more stable expansion phase, bolstered by industrial automation upgrades and the tightening of occupational safety standards in the Global South.

Multi-stage filtration systems, which were once a niche, are set to gain standardization status in heavy industries. The demand will broaden as OEMs integrate smarter filtration controls, enabling predictive maintenance and compliance tracking with Fact.MR is projecting a CAGR of 6.1%, and the value pool is expected to expand confidently from USD 7.8 billion in 2025 to USD 14.1 billion by 2035.

Key Metrics

| Metric | Value |

|---|---|

| Estimated Size in 2025 | USD 7.8 Billion |

| Projected Size in 2035 | USD 14.1 Billion |

| CAGR (2025 to 2035) | 6.1% |

Fact.MR Survey Results: Market Dynamics Based on Stakeholder Perspectives

(Surveyed Q4 2024, n=500 stakeholder participants evenly distributed across manufacturers, distributors, and end-users in the USA, Western Europe, Japan, and South Korea)

Key Priorities of Stakeholders

- Compliance with Environmental Regulations: 80% of stakeholders globally identified compliance with increasing air quality regulations as a "critical" priority.

- Energy Efficiency: 75% highlighted the need for energy-efficient systems to reduce operational costs over time.

Regional Variance:

- USA: 72% emphasized the importance of automation (IoT, predictive maintenance) to enhance operational efficiency and reduce manual labor costs.

- Western Europe: 85% considered sustainability in material selection (recyclable, low-carbon footprint), with a strong push towards eco-friendly solutions.

- Japan/South Korea: 60% highlighted the need for compact, high-performance extraction systems due to space constraints in urban facilities.

Embracing Advanced Technologies

High Variance:

- USA: 52% of manufacturers have adopted IoT-enabled extraction systems for real-time monitoring, driven by high demand in the manufacturing and pharmaceutical sectors.

- Western Europe: 48% of countries have implemented automated filter cleaning and maintenance systems, with Germany (61%) leading the way due to its stringent EU air quality regulations.

- Japan/South Korea: Only 30% have implemented advanced technologies, attributing slow adoption to high upfront costs and a smaller scale of operations.

Convergent and Divergent Perspectives on ROI:

- USA: 67% of stakeholders considered automation in extraction systems to be "worth the investment," whereas only 39% in Japan reported similar satisfaction with advanced technology.

Material Preferences

Consensus:

- Steel: Selected by 68% overall for its durability and resistance to wear and tear, especially in high-traffic industrial environments.

Variance:

- Western Europe: 54% preferred stainless steel with corrosion-resistant coatings due to strict regulatory compliance demands and sustainability focus.

- Japan/South Korea: 45% selected hybrid materials (steel-aluminum blends) to balance cost with resistance to corrosion in high-moisture environments.

- USA: 70% preferred steel due to its proven longevity, though there was a slight uptick (15%) in interest for lightweight aluminum options in the Pacific Northwest.

Price Sensitivity

Shared Challenges:

- Rising Raw Material Costs: 80% of stakeholders cited increasing steel and aluminum prices as a major concern.

Regional Differences:

- USA/Western Europe: 55% of stakeholders were willing to pay a 10-15% premium for energy-efficient systems and advanced automation features.

- Japan/South Korea: 65% favored cost-effective models under USD 5,000, with minimal interest in premium, feature-heavy systems.

- South Korea: 40% expressed a preference for leasing options to help manage upfront costs, compared to 20% in the USA

Pain Points in the Value Chain

Manufacturers:

- USA: 60% of manufacturers reported challenges with labor shortages, particularly in the assembly and maintenance sectors.

- Western Europe: 55% highlighted the complexity of adhering to stringent EU environmental regulations, such as CE certification.

- Japan: 58% struggled with slow demand from traditional industries that rely on older dust collection technologies.

Distributors:

- USA: 65% cited delays in inventory due to reliance on overseas suppliers, leading to supply chain bottlenecks.

- Western Europe: 50% mentioned pressure from lower-cost competitors, particularly from Eastern Europe.

- Japan/South Korea: 60% struggled with logistical challenges in rural locations, limiting the efficient distribution of large extraction systems.

End-Users:

- USA: 47% cited high maintenance costs as a significant issue with existing systems.

- Western Europe: 40% reported difficulties in retrofitting older buildings with modern extraction technology.

- Japan: 52% cited limited technical support for advanced systems as a primary challenge.

Future Investment Priorities

Alignment:

- 72% of global manufacturers plan to invest in R&D for automation, smart filters, and energy-efficient technologies.

Divergence:

- USA: 58% intend to focus on developing modular systems for varied industrial applications, such as combined filtration and fume extraction.

- Western Europe: 63% of stakeholders are prioritizing sustainable production methods, including green steel and low-carbon materials.

- Japan and South Korea: 48% are focusing on compact, space-saving systems to meet the growing demand in urban areas.

Regulatory Impact

- USA: 70% of USA stakeholders viewed state-level air quality regulations (e.g., California's Proposition 65) as a significant factor in equipment purchase decisions.

- Western Europe: 82% of stakeholders felt the EU's tighter environmental standards would be a growth driver for premium filtration equipment, particularly in industries such as food and pharmaceuticals.

- Japan/South Korea: 40% noted that local air quality regulations have a relatively minor influence on purchasing decisions, citing less stringent enforcement compared to Western regions.

Conclusion: Variance vs. Consensus

- High Consensus: Global stakeholders are united in their concerns regarding air quality regulations, energy efficiency, and the rising costs of raw materials.

Key Variances:

- USA: Emphasis on automation and modularity versus Japan/South Korea's focus on cost control and space efficiency.

- Western Europe: Leadership in sustainability and regulatory compliance, compared to Asia's focus on hybrid material solutions.

Strategic Insight:

- A one-size-fits-all approach will not succeed in the global landscape. Regional differentiation (e.g., automation in the USA, sustainability in Europe, compact designs in Asia) will be crucial for success.

Impact of Government Regulation

| Country | Impact of Policies and Government Regulations |

|---|---|

| United States |

|

| Western Europe |

|

| Japan |

|

| South Korea |

|

| China |

|

| Australia |

|

Market Analysis

The dust extraction system industry is set to grow steadily through 2035, driven by stricter workplace air quality regulations and rising automation in manufacturing environments. Fact.MR analysis found that companies investing in smart, high-efficiency filtration systems will gain a competitive advantage, especially in the metal, construction, and pharmaceutical sectors. Conversely, legacy equipment manufacturers and low-cost suppliers without compliance-ready offerings risk losing relevance as global environmental standards tighten.

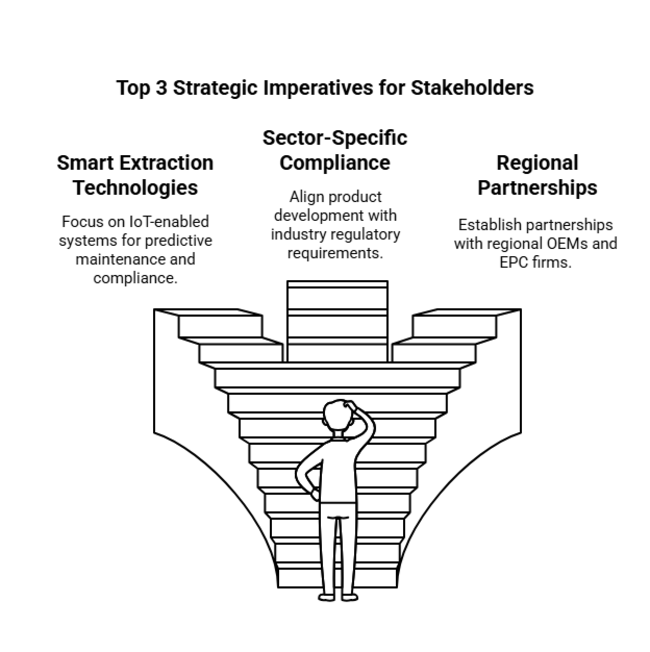

Top 3 Strategic Imperatives for Stakeholders

Accelerate Investment in Smart Extraction Technologies

Executives should prioritize CAPEX allocation toward IoT-enabled collection systems that offer predictive maintenance, energy optimization, and real-time compliance tracking to meet evolving occupational safety mandates.

Align Offerings with Sector-Specific Compliance Demands

Product development must align with distinct regulatory requirements in target industries-such as HEPA filtration in pharmaceuticals and wet scrubbers in metal processing-to ensure long-term procurement eligibility and reduce certification delays.

Forge Regional OEM and EPC Partnerships

To scale distribution and service networks, companies should establish joint ventures or technical licensing deals with regional equipment manufacturers and engineering-procurement-construction (EPC) firms in emerging industries where industrial build-outs are accelerating.

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability & Impact |

|---|---|

| Delayed Regulatory Enforcement in Emerging Economies- Inconsistency in dust emission enforcement across South Asia, Africa, and parts of Latin America may stall adoption, giving room for non-compliant, low-cost alternatives to persist. | Medium Probability, High Impact |

| Volatility in Raw Material Prices for Filtration Components- Frequent fluctuations in the prices of stainless steel, aluminum, and synthetic polymers used in filters and housings can erode manufacturer margins and disrupt pricing strategies. | High Probability, Medium Impact |

| Slow Adoption of Automation in Legacy-Heavy Industrial Clusters - Industries such as mining and lumber in less digitized regions may resist upgrades, limiting the addressable demand for smart or centralized collection systems. | Medium Probability, High Impact |

Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Invest in Smart Filtration Systems | Run feasibility on IoT-enabled filtration components to enhance energy efficiency and predictive maintenance capabilities. |

| Strengthen Regulatory Compliance Offerings | Initiate a compliance audit for products across key sectors (e.g., pharma, metal, food) to ensure adherence to new regulations. |

| Expand Regional Distribution Network | Launch a regional partnership program to onboard local OEMs and EPC firms in emerging industries like Southeast Asia and Latin America. |

For the Boardroom

To stay ahead, companies must prioritize investment in smart filtration technologies and regulatory-compliant solutions. Immediate steps should include sourcing IoT-enabled components to meet the increasing demand for predictive maintenance and energy efficiency. Simultaneously, the client should conduct a thorough compliance audit to ensure offerings meet the latest sector-specific regulations, particularly in the food, pharma, and metal industries.

Expanding partnerships with regional OEMs and EPC firms in emerging regions like Southeast Asia will position the company to capitalize on the growing industrialization in these areas. This intelligence should shift the client's roadmap toward proactive product innovation, compliance readiness, and strategic regional expansion to secure long-term growth and leadership.

Segment-wise Analysis

By Product Type

Bag filters remain one of the largest and most widely adopted dust extraction solutions in various industries. The increasing focus on air quality standards and workplace safety regulations such as OSHA is driving their growth. With a CAGR of 4.2%, bag filters will continue to dominate, offering a cost-effective solution for large-scale operations.

The demand is particularly robust in industries like mining, construction, and textiles, where particulate matter poses significant health risks. This segment’s growth is also buoyed by technological advancements improving filtration efficiency and reducing maintenance costs. Moreover, bag filters are highly scalable, making them suitable for a range of applications.

By System Type

Chip extractors, commonly used in metalworking industries to capture chips and fine particles during machining, are expected to grow at a CAGR of 4.1%. As industries prioritize automation and operational efficiency, the demand for chip extractors continues to rise.

These systems are crucial for maintaining clean, safe environments by effectively removing metal chips and dust generated in processes like cutting, grinding, and turning. The automotive and manufacturing sectors, in particular, are ramping up production due to increasing global demand, which further drives the need for chip extraction systems. This trend is expected to sustain growth in the chip extractor segment over the forecast period.

By End-Use Industry

The lumber industry remains a significant end-user of dust collection technologies due to the high levels of dust generated during woodworking operations. This segment is expected to grow at a CAGR of 4.1% as more stringent health and safety regulations are introduced worldwide. Dust generated from wood processing not only poses respiratory risks but also creates fire hazards, thus driving the adoption of advanced dust control technologies.

The increasing focus on workplace safety and air quality in lumber mills and sawmills is propelling the demand for more efficient collection solutions. Additionally, innovations in filtration technologies tailored to wood dust will further bolster industry growth.

By Dust Type

Blowers with dust collection technologies are projected to grow at a CAGR of 3.7%. These systems are essential in industrial environments where high-efficiency airflow is needed to capture large volumes of dust. Industries such as woodworking, construction, and metalworking benefit significantly from blowers integrated with dust collection capabilities.

The growing focus on improving air quality and reducing airborne particulate matter in industrial settings is driving the demand for these systems. As companies continue to prioritize worker safety and environmental compliance, the adoption of blowers with dust extraction features is expected to increase, supporting steady growth in this segment.

Country-wise Insights

USA

The USA is forecast to grow at a CAGR of 6.5% from 2025 to 2035. This growth is driven by stringent OSHA regulations, which mandate clean air standards in manufacturing and construction sectors.

The USA is also benefiting from increasing automation as industries invest in advanced filtration systems. The adoption of IoT and energy-efficient solutions is a significant driver in sectors such as mining and food processing.

Rising environmental concerns and state-level regulations like California's Proposition 65 are pushing for better dust control systems. This is particularly evident in industries with high dust exposure, like mining and agriculture, making the USA a key adopter of dust collection technologies.

UK

The UK is projected to grow at a CAGR of 5.8% from 2025 to 2035. Strong regulatory frameworks, such as the EU Industrial Emissions Directive, are pushing industries to adopt more efficient dust control systems to reduce air pollution.

The UK government’s push towards green industrial policies and carbon-free production is fostering demand for sustainable, energy-efficient filtration solutions, particularly in manufacturing and construction.

Technological advancements, including IoT-based dust control systems, are gaining traction across various sectors. Companies are increasingly investing in automation to enhance workplace health and safety, further driving demand for these systems.

France

France is set to grow at a CAGR of 6.2% from 2025 to 2035, driven by EU regulatory compliance. The Eco-Design Directive encourages the adoption of energy-efficient dust collection technologies across industrial sectors.

The industry is also influenced by France's emphasis on sustainable practices, particularly in the manufacturing and food processing industries. Regulations like the EU Green Deal are further pushing the demand for low-emission systems.

Automation and IoT integration are expected to grow in France as industries demand higher-performance systems. These advancements in technology are crucial for maintaining air quality standards in compliance with labor safety regulations.

Germany

Germany is projected to grow at a CAGR of 6.3% from 2025 to 2035, fueled by strict EU air quality regulations. The EU Industrial Emissions Directive has driven companies to improve filtration systems across industrial sectors.

With a focus on worker safety and health, German industries are prioritizing advanced dust control systems. Compliance with both CE certification and EU safety standards is becoming more critical in sectors like automotive and manufacturing.

Germany’s strong focus on sustainability and technological innovation is driving a shift toward automation and energy-efficient systems. IoT-based systems are also gaining adoption, improving operational efficiency in high-dust environments like factories.

Italy

Italy is expected to grow at a CAGR of 5.6% from 2025 to 2035, driven by Italy's EU compliance and increasing emphasis on industrial safety. Regulations like the EU Industrial Emissions Directive are pushing industries to adopt more advanced dust control solutions.

The industry is also influenced by Italy’s manufacturing and construction sectors, which are major contributors to dust emissions. Companies are increasingly investing in energy-efficient and automated solutions to meet environmental standards.

Italy is also witnessing rising demand for IoT-enabled and smart dust collection solutions. These innovations are crucial for sectors like automotive and food processing, where air quality and worker safety are high priorities.

South Korea

South Korea is projected to grow at a CAGR of 5.4% from 2025 to 2035. Government regulations, including those from the KOSHA, are pushing industries toward better dust management solutions to ensure workplace safety.

With South Korea’s emphasis on automation in industrial processes, demand for advanced dust control systems, including those with IoT capabilities, is growing. Sectors like electronics and automotive manufacturing are particularly invested in these technologies.

South Korea also faces challenges related to space efficiency due to high urbanization, prompting interest in compact dust extraction solutions. As a result, demand for space-saving, energy-efficient systems is on the rise.

Japan

Japan is forecast to grow at a CAGR of 5.2% from 2025 to 2035. Japan's regulatory focus on worker safety and environmental protection is encouraging industries to invest in advanced filtration systems.

Despite Japan’s traditionally lower adoption of automation in smaller industrial setups, there is increasing interest in smart filtration solutions in larger industrial sectors, particularly in the automotive and electronics industries.

Japan’s cost-sensitive industry is leading to the adoption of hybrid materials and more compact designs. This trend is especially seen in the food processing and pharmaceutical sectors, which require efficient yet affordable solutions.

China

China is expected to grow at a CAGR of 6.0% from 2025 to 2035. With its focus on industrial growth and air quality standards, China is rapidly adopting advanced filtration technologies to comply with national environmental regulations.

The government’s push towards green manufacturing and air pollution control is encouraging industries to invest in energy-efficient filtration solutions. Additionally, China’s manufacturing sector remains a key driver of demand for these solutions.

Chinese industries are increasingly adopting automation and smart technologies, including IoT-based filtration systems. As industrial automation rises, the demand for more sophisticated dust control solutions is also expected to increase.

Market Share Analysis

Donaldson Company, Inc.: 15-20%

Donaldson will continue its dominance in industrial filtration, backed by robust R&D in dust extraction technologies and an expanding presence in emerging regions. By 2025, the company will focus on innovations in sustainable filtration solutions, driving significant growth, especially in industries like manufacturing and automotive. Strong growth in emerging economies, particularly in Asia-Pacific and Latin America, will enhance its share in the coming years.

Nederman Holding AB: 12-18%

Nederman will expand its share with strategic acquisitions, such as the 2024 acquisition of Keller Lufttechnik, which bolsters its position in industrial air filtration. The company will be able to remain an industry leader in Europe with its eco-friendly solutions for dust control. Its emphasis on incorporating new, energy-saving technologies in industries such as autos and chemical production will also drive its growth, especially in North America and Europe.

Camfil AB: 10-15%

Camfil will have a robust presence, fueled by its advanced-efficiency air filtration equipment and expanding demand within industries such as healthcare and manufacturing. By 2025, the firm will emphasize building its clean air solutions portfolio and taking advantage of the mounting regulations governing air quality. With tremendous expansion anticipated in North America and Europe, Camfil's commitment to environmental stewardship will set it up for long-term growth.

Parker Hannifin Corporation: 8-12%

Parker Hannifin will see moderate growth in the dust collection industry, driven by its adoption of IoT technologies into filtration systems. The company will emphasize automation and energy efficiency, particularly in Industry 4.0-practicing industries. The development of Parker's presence in new regions like Asia and South America will also drive its growth in the coming decade.

WAMGROUP S.p.A.: 7-10%

WAMGROUP will continue to be a dominant force in bulk material handling and dust control solutions, especially in food, cement, and chemical production industries. The company's dominance in these industries, combined with the growing regulations on air quality and environmental protection, will propel its growth. Its expansion into emerging industries, particularly in Asia and the Middle East, will reinforce its position, guaranteeing a consistent rise in the next few years.

AAF International (Daikin): 6-9%

The AAF International, under the Daikin umbrella, will utilize its knowledge and expertise in air filtration systems to further consolidate its gains in the industry. The company will be leveraged by stringent international air quality legislation and the growing requirements for energy-efficient systems in various industries such as industrial manufacturing.

AAF would expand its products and service range to include environmentally-friendly and high-performance products by 2025, thus consolidating its position in the European, North American, and Asia-Pacific regions.

Other Key Players

- Robert Bosch GmbH

- Thermax Limited

- Hocker Polytechnik GmbH

- DELTA NEU S.A.S

- EnviPro Engineering Pvt. Ltd

- Envirosystems Manufacturing, LLC

- Eurovac

- Fercell Engineering Limited

- Cleantek

- ESTA Apparatebau GmbH & Co. KG

- BWF Envirotech

- Filtermist International Limited

- Sly Inc.

- Airflow Systems, Inc.

- Dustcontrol Ltd.

- Flex Kleen

- Schenck Process

- TiTan Technologies

- Kelin Environmental Protection Equipment Co., Ltd.

- RoboVent Products, Inc.

Dust Extraction System Market Segmentation

By Product Type:

- Bag Filters

- Cartridge

- Vacuum

- Cyclone

- Suction Benches

- Wet Scrubbers

- Media Blasting Rooms

- Rotary

- Other

By System Type:

- Chip Extractors

- Fine Dust Extractors

- Vacuum Extractors

- Power Tool Extractors

- Air Filters

- HEPA Filters

By End-Use Industry:

- Lumber

- Food & Beverage

- Paper & Printing

- Plastic & Rubber

- Mining, Quarrying, and Oil & Gas

- Chemicals

- Construction

- Metal

- Textile

- Miscellaneous Industries

By Dust Type:

- Blowers with Dust Extraction

- Wet Extractors

- Dry Extractors

By Region:

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- Middle East & Africa

- Frequently Asked Questions -

What are the key factors driving the growth of dust extraction systems in industrial settings?

The key factors driving growth include stricter environmental regulations, increased focus on worker health and safety, and advancements in filtration technology.

How does the implementation of government regulations impact the adoption of dust extraction systems?

Government regulations, such as air quality standards and safety protocols, compel industries to adopt more efficient dust extraction systems to comply with legal requirements.

Which product types in the dust extraction system are expected to experience significant demand in the coming years?

Product types such as bag filters, cartridge systems, and vacuum extractors are expected to see significant demand in the dust extraction system due to their efficiency and widespread use across industries.

What industries are the largest users of dust extraction systems globally?

Industries like woodworking, metalworking, mining, and chemicals are the largest users of dust extraction systems due to the hazardous nature of dust in these sectors.

How do technological advancements influence the performance and efficiency of dust extraction systems?

Technological advancements, such as automation, IoT integration, and improved filtration materials, significantly enhance the performance, efficiency, and energy savings of dust extraction systems.

Author:

Shubham Patidar

Editor:

Naved Ahmed