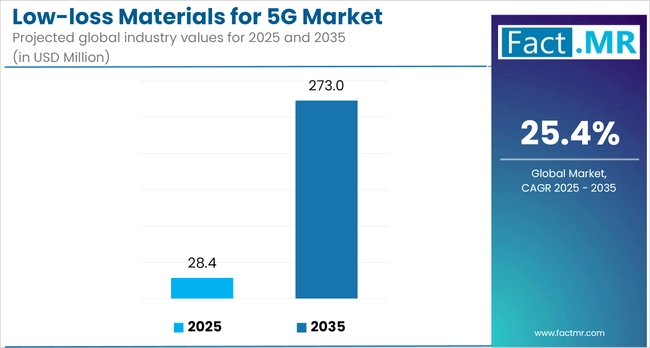

- Base Value(2025): 28.4 Mn

- Forecast Value (2035): 273.1 Mn

- CAGR (2035): %

Low-loss Materials for 5G Market Outlook (2025 to 2035)

The global Low-loss Materials for 5G market is projected to increase from USD 28.4 million in 2025 to USD 273.1 million by 2035, with an annual growth rate of 25.4%, driven by the global rollout of high-frequency 5G networks.

As demand rises for faster, reliable connectivity, materials with excellent dielectric properties, such as PTFE laminates, LCPs, and modified polyimides, are being widely adopted in antennas, base stations, and high-frequency PCBs.

Low Loss Materials For 5g Market | Source: Fact.MR

These materials reduce signal loss, enhance thermal stability, and support efficient performance in RF front-end modules and 5G devices. Growth is especially strong in regions such as the USA, China, and South Korea, where telecom and electronics manufacturers are investing heavily in next-generation infrastructure. The rise of applications such as autonomous vehicles and industrial IoT is further driving demand across various industries.

What are the Drivers of the Low-loss Materials for the 5G Market?

The expansion of the 5G market, which relies on low-loss materials, is driven by the surging need for faster data transmission, reduced signal loss, and superior performance of next-generation communication infrastructures. Since 5G networks operate at higher frequencies, particularly millimeter waves, materials in substrates, PCBs, and antenna radomes should exhibit low dielectric loss, high thermal stability, and high signal integrity.

Important sources of innovation include material innovations, such as PTFE composites, liquid crystal polymers (LCP), and ceramics. These enable achieving lower insertion losses and reduced electromagnetic interference in smaller and higher-frequency 5G modules. Additionally, increased spending on 5G base station infrastructure and small cell deployment is exacerbating the shortage of these materials.

The combination of 5G and IoT, smart mobility, and industrial automation opens up new areas of application, which also increases the demand for low-loss materials. Telecom equipment OEMs are constantly exploring performance limits, resulting in high mileage for the market in both developed and emerging economies.

What are the Regional Trends of the Low-loss Materials for the 5G Market?

The regional dynamics of the low-loss materials for the 5G market reflect the pace of 5G infrastructure deployment and advancements in telecommunications manufacturing across key global economies.

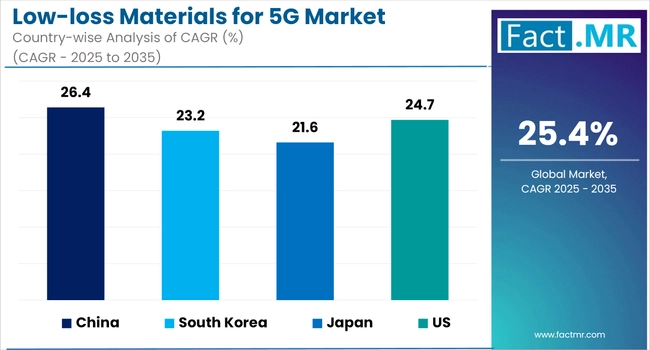

Asia-Pacific leads the market, with China, South Korea, and Japan at the forefront due to strong investments in 5G networks, robust electronics manufacturing, and the presence of major OEMs such as Huawei, Samsung, and Murata. China’s aggressive rollout of 5G base stations and high-frequency antenna modules is a primary driver of demand for low-loss laminates and substrates. North America, particularly the United States, follows closely, driven by large-scale 5G infrastructure projects, R&D investments, and defense-related communications upgrades.

The region benefits from a strong presence of technology leaders, including Qualcomm, Cisco, and Rogers Corporation, which are driving innovation in advanced PCB and antenna materials. In Europe, countries such as Germany and the UK are gradually expanding their 5G networks, supported by regulatory initiatives and increased demand from the automotive and industrial sectors. Emerging markets in Latin America and the Middle East and Africa are in earlier stages of adoption; however, increasing investments in telecom infrastructure, particularly in urban centers, are expected to create new growth opportunities for high-performance materials over the coming years.

What are the Challenges and Restraining Factors of the Low-loss Materials for the 5G Market?

The low-loss materials for the 5G market face challenges that may hinder their long-term growth and scalability across global markets. One of the primary obstacles is the high cost of advanced raw materials such as polytetrafluoroethylene (PTFE), liquid crystal polymer (LCP), and ceramic-filled laminates. These materials, while offering superior dielectric performance, come at a higher price point than conventional alternatives, which can limit their adoption particularly in cost-sensitive applications or emerging economies where budget constraints are tighter.

Manufacturing complexity is another barrier. Producing low-loss materials suitable for high-frequency 5G applications requires precision engineering and strict quality control, leading to longer production cycles and higher defect rates. This raises operational costs and limits output, especially for small- to mid-sized suppliers without advanced infrastructure.

Thermal and mechanical limitations also present challenges. Many low-loss materials struggle with dimensional stability and heat resistance when exposed to the high-power requirements of next-generation 5G base stations and antennas. This can compromise performance and reliability, especially in harsh environments or high-density installations.

Additionally, supply chain disruptions, particularly for specialty chemicals and rare-earth elements, pose risks. Many of these inputs are sourced from limited geographic regions, making the market vulnerable to geopolitical tensions and trade restrictions. The lack of diversified sourcing increases price volatility and delays.

Finally, standardization and qualification timelines remain lengthy. New materials must undergo extensive validation processes to meet the stringent reliability and performance standards required in telecommunications infrastructure. This slows the commercialization of next-generation solutions and deters innovation.

Collectively, these challenges emphasize the need for collaborative efforts among manufacturers, network providers, and regulators to reduce costs, streamline production, and support material innovation that meets the technical and economic demands of a global 5G rollout.

Country-Wise Outlook

Low Loss Materials For 5g Market Cagr Analysis By Country | Source: Fact.MR

United States Low-loss Materials for 5G Market Sees Growth Driven by Accelerating Investments in 5G Infrastructure

The United States' low-loss materials for the 5G market are witnessing strong growth, driven by accelerating investments in 5G infrastructure and the increasing deployment of high-frequency applications such as millimeter-wave (mmWave) networks.

As telecom operators expand their 5G coverage, the demand for materials that enable minimal signal attenuation and high-speed data transmission is surging. Industries like consumer electronics, automotive, and aerospace are adopting advanced substrates such as PTFE, LCP, and ceramic-filled composites to meet the stringent performance and thermal stability requirements of next-generation devices and antennas.

Additionally, the proliferation of IoT devices and smart infrastructure is reinforcing the need for low-dielectric-loss materials to maintain signal integrity in compact, high-frequency environments. With strong support from federal initiatives and private sector R&D, the U.S. is positioning itself as a leading hub for innovation and commercialization in this evolving segment of the 5G supply chain.

China witnesses a Combination of Domestic Policies, Technological Advancements, and Shifting Export Dynamics.

China witnesses a surge in the adoption of low-loss materials for 5G, driven by its aggressive rollout of next-generation telecommunications infrastructure. As the world’s largest 5G market by number of base stations and users, China is scaling up deployment of mmWave and sub-6 GHz networks, which require materials with excellent dielectric properties to ensure minimal signal degradation.

Major Chinese manufacturers are heavily investing in the research and domestic production of advanced materials, such as PTFE composites, liquid crystal polymers (LCP), and ceramic-filled laminates, to reduce their dependency on imports and strengthen supply chain resilience.

Additionally, the growth of 5G-enabled technologies such as autonomous vehicles, industrial automation, and smart cities is further driving demand for high-frequency, thermally stable, and low-dielectric-loss substrates across electronics and antenna design applications. Supported by government incentives and strategic industrial policies, China is positioning itself as a dominant force in the global low-loss materials market.

Japan Sees Strong Emphasis on Innovation and Quality in the Development of Low-Loss Materials For 5G.

Japan sees a strong emphasis on innovation and quality in the development of low-loss materials for 5G, positioning the country as a key contributor to advanced telecommunications infrastructure. Japanese manufacturers are leveraging their expertise in high-performance polymers, ceramics, and laminates to produce substrates that meet the strict dielectric requirements essential for high-frequency signal transmission.

With companies such as Panasonic, Toray, and Mitsubishi Chemical investing in research and development, Japan is focused on enhancing materials like liquid crystal polymers (LCP) and polyimides that support mmWave applications. Additionally, the country’s push for 5G rollout across industrial and urban zones, supported by government initiatives and smart city projects, continues to drive demand for materials that enable reliable, high-speed connectivity with minimal signal loss.

Category-wise Analysis

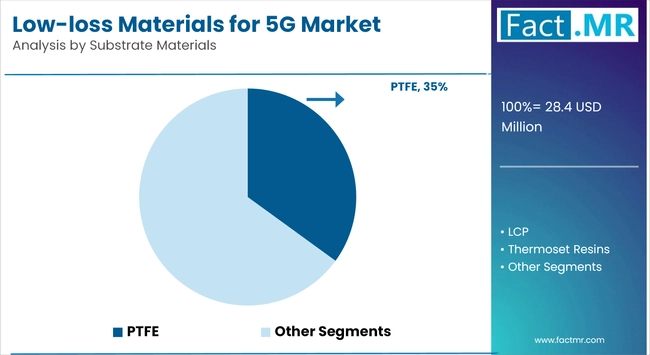

Substrate Materials to Exhibit Leading Share Among Material Types

Substrate materials are expected to hold the leading share among material types in the low-loss materials for the 5G market, driven by their critical role in high-frequency signal transmission.

Low Loss Materials For 5g Market Analysis By Substrate Materials | Source: Fact.MR

As 5G technology demands higher data rates and minimal signal attenuation, the need for advanced substrate materials such as PTFE (polytetrafluoroethylene), LCP (liquid crystal polymer), and polyimide has intensified.

These materials offer low dielectric constants and reduced dissipation factors, making them ideal for applications in 5G base stations, antennas, and RF modules. The growing deployment of small cells and mmWave infrastructure globally further underscores the dominance of substrates, as they provide the foundation for reliable and efficient signal performance in complex, high-speed communication systems.

Sub-6 GHz 5G to Exhibit Leading Share Among Frequency

Sub-6 GHz 5G is anticipated to account for the leading share among frequency segments in the low-loss materials market, owing to its widespread deployment and balanced performance characteristics.

Unlike mmWave frequencies, Sub-6 GHz offers broader coverage, better penetration through obstacles, and lower latency, making it a practical choice for early and large-scale 5G rollouts. This frequency range is being widely adopted across urban, suburban, and rural environments, particularly in markets like China, the United States, and parts of Europe.

As a result, the demand for low-loss materials optimized for Sub-6 GHz applications such as circuit boards, antennas, and filter components is rising steadily. The segment’s dominance is further reinforced by continued investment in nationwide 5G infrastructure and upgrades to existing LTE networks.

Smartphones to Exhibit Leading Share Among End Use

Smartphones are expected to hold the leading share among end-use segments in the low-loss materials for 5G market. This dominance is driven by the massive global demand for 5G-enabled mobile devices, as consumers increasingly prioritize high-speed connectivity, low latency, and enhanced user experiences.

Leading smartphone manufacturers such as Apple, Samsung, Xiaomi, and Huawei are integrating advanced materials to support higher frequency performance, improved thermal management, and efficient signal transmission.

The transition to 5G has intensified the need for low-loss substrates, antenna materials, and printed circuit boards that can accommodate dense component placement and maintain signal integrity. With the smartphone sector at the forefront of 5G adoption, its continued growth is set to influence material innovation and market expansion.

East Asia holds the Leading Share in the Low-loss Materials for 5G Market

East Asia continues to dominate the low-loss materials for 5G market, driven by aggressive 5G infrastructure rollouts, advanced semiconductor manufacturing capabilities, and government-backed digital transformation initiatives.

China remains at the forefront, supported by its expansive telecom ecosystem and strategic investments under initiatives like Made in China 2025. Japan and South Korea also contribute, leveraging their strengths in electronics and mobile device production to increase demand for high-performance substrates and laminates essential to 5G hardware.

The region’s integrated supply chains and focus on next-generation connectivity make it a pivotal hub for low-loss material innovation and deployment. With strong industrial backing and consistent demand from smartphone, automotive, and network equipment sectors, East Asia is expected to retain its leadership position in the global 5G materials landscape over the coming years.

Competitive Analysis

Low Loss Materials For 5g Market Analysis By Company | Source: Fact.MR

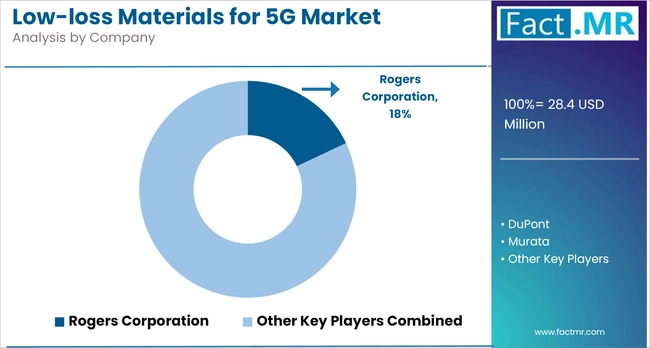

Key players in the low-loss materials for 5G market, including Rogers Corporation, DuPont, Sartomer (Arkema), AGC Chemicals, Toray Industries, Mitsubishi Gas Chemical, JSR Corporation, Hitachi Chemical, SABIC, Solvay, Kyocera, and Sumitomo Bakelite, play a pivotal role in driving innovation, scalability, and commercial adoption of next-generation materials.

These companies are heavily investing in R&D to develop advanced substrates, laminates, and resins with improved dielectric properties, thermal stability, and signal integrity critical for supporting high-frequency 5G applications. Strategic collaborations, product launches, and expansion of manufacturing capabilities are common approaches employed by these industry leaders to meet the growing global demand.

Their expertise in specialty chemicals and materials engineering positions them as key enablers in the evolution of 5G infrastructure, mobile devices, and connected technologies.

Recent Development

- In September 2023, Shin‑Etsu Chemical is advancing its Qromis Substrate Technology (QST) for GaN power devices. While focused on power electronics, this development in low-loss substrates could be leveraged for high-performance 5G components.

- In June 2023, Doosan Corporation Electro-Materials showcased its advanced 5G connectivity solutions at the IMS 2023 Microwave/RF Exhibition in North America. The company introduced a portfolio of next-generation materials and mmWave antenna technologies, developed in collaboration with Movandi’s BeamX beamforming platform. These solutions are designed to enhance performance in small cells and wireless repeaters, offering an integrated approach to signal processing critical to the deployment and scalability of 5G infrastructure.

Segmentation of Low-loss Materials for 5G Market

-

By Material Type :

- Substrate Materials

- Organic Materials

- PTFE

- LCP

- Thermoset Resins

- PPO

- PPS

- Polyimide

- Others

- Inorganic Materials

- Glass

- Ceramic & LTCC

- HTCC

- Others

- Organic Materials

- Package Materials

- EMC / MUF

- EMI Shielding with Inks

- Advanced Package Materials (SiP, AiP)

- Substrate Materials

-

By Frequency :

- Sub-6 GHz 5G

- mmWave 5G

-

By End Use :

- Smartphones

- Infrastructure

- Customer Premise Equipment (CPE)

-

By Region :

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- Middle East & Africa