Medical Plastics Market Outlook (2025 to 2035)

The medical plastics market is valued at USD 25 billion in 2025. As per Fact.MR’s analysis, the medical plastics industry will grow at a CAGR of 5% and will reach USD 40.7 billion by 2035.

In 2024, the medical plastics market saw a significant increase in growth due to sustained demand for affordable, high-performance materials in diagnostic equipment, surgical devices, and disposable consumables.

The trend toward outpatient treatment and home health management spurred the use of portable, lightweight medical devices, many of which depend significantly on advanced polymer applications. Sustainability trends also started influencing production, with producers investing in recyclable and biocompatible plastics to meet regulatory changes and environmental objectives.

Moving forward to 2025, the industry is set for continued growth as public and private healthcare systems accelerate efforts to upgrade infrastructure and minimize cross-contamination risks. Increasing global healthcare expenditure, along with a strong emphasis on infection prevention, will continue to drive the importance of medical-grade plastics.

Moreover, advances in polymer science and medical 3D printing technology are likely to provide new opportunities for product innovation and application-specific customization.

| Metric | Value |

|---|---|

| Industry Value (2025E) | USD 25 billion |

| Industry Value (2035F) | USD 40.7 billion |

| CAGR (2025 to 2035) | 5% |

Market Analysis

The medical plastics industry is experiencing a consistent growth path due to increasing demand for lightweight, sterilizable, and durable materials in surgical, diagnostic, and home healthcare uses. Increased hygiene awareness and expanding healthcare spending are driving adoption, particularly in single-use and disposable medical devices. Advanced polymers and recyclable material manufacturers are likely to gain the most, while legacy providers of glass and metal medical components could be losing relevance.

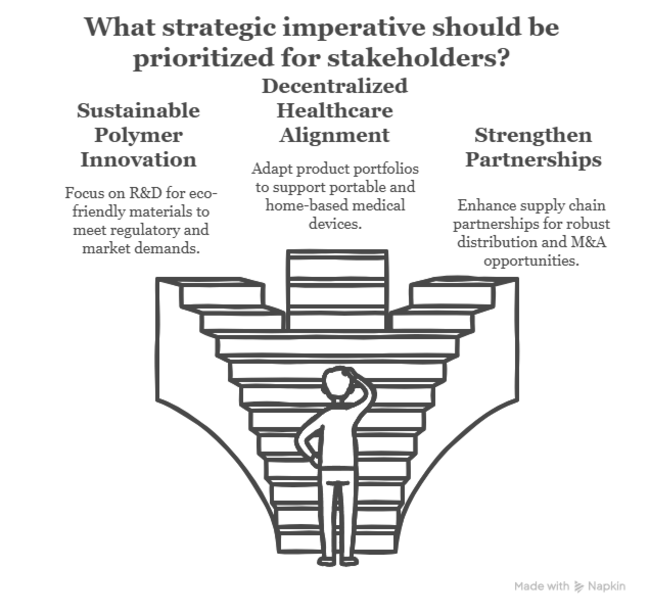

Top 3 Strategic Imperatives for Stakeholders

Invest in Sustainable Polymer Innovation

Top-level executives must make R&D allocations for recyclable, biocompatible, and antimicrobial plastics to meet changing regulatory requirements and increasing orders for environmentally friendly medical products.

Align Product Portfolios with Decentralized Healthcare Trends

Align products with portable and home-based medical devices by incorporating light, sterilizable materials to address outpatient care and distant diagnostics.

Strengthen Strategic Partnerships Throughout Supply Chains

Partner with healthcare professionals, logistics companies, and raw material vendors to obtain robust distribution channels and pursue M&A opportunities that increase production capacity and geographic reach.

Top 3 Risks Stakeholders Should Monitor

| Risk | Assessment (Probability - Impact) |

|---|---|

| Geopolitical Instability Disrupting Raw Material Supply Chains - Trade restrictions and ongoing conflicts have the ability to slow down polymer sourcing, thereby affecting production timelines and expenses. | High Probability - High Impact |

| Regulatory Shifts Towards Biodegradable Plastics - Sudden implementation of environmental regulations may make traditional plastics obsolete, necessitating expensive portfolio realignment. | Medium Probability - High Impact |

| Crude Oil Price Volatility Impacts on Polymer Prices - The up-and-down motion of crude oil prices straight affects plastic resin prices, cutting manufacturer margins. | High Probability - Medium to High Impact |

1-Year Executive Watch-List

| Priority | Immediate Action |

|---|---|

| Accelerate Transition to Sustainable Materials | Perform in-depth feasibility studies for blending bio-based and recyclable medical-grade polymers |

| Deepen OEM Integration | Create a continuous OEM feedback system to co-develop next-generation polymer-based medical components |

| Bolster Regional Manufacturing Resilience | Implement targeted incentive schemes to onboard strategic local partners and expand distributed production networks |

For the Boardroom

To stay ahead, companies must strategically invest in sustainable polymer innovations and deepen their relationships with OEMs to co-design next-generation medical devices. This will help them not only keep pace with increasing demand for eco-friendly materials but also position themselves in line with changing healthcare trends towards decentralized, home-based care.

With regulatory pressures mounting and consumer expectations shifting, companies need to focus on creating robust, local supply chains to insulate themselves against risks and scale up operations. This intelligence should have a direct impact on your roadmap by speeding up R&D in green materials, increasing manufacturing capacity, and strengthening partnerships along the value chain.

Segment-Wise Analysis

By Type

According to analysis, High Performance Plastics (HPP) is the most profitable segment for 2025 to 2035. This is because they are more durable, resistant to chemicals, and can sustain harsh conditions, which are a requirement for life-critical medical applications such as surgical implants, diagnostic equipment, and drug delivery systems.

The market for HPP is anticipated to develop at a better-than-average rate due to technological innovations in the field of healthcare, rising healthcare spending, and growing demand for sophisticated medical gear.

The segment is expected to at a CAGR of 6.6% over the forecast period, leveraging the current trend towards precision, safety, and performance in medical device production.

By Application

According to the analysis, Medical Components is the most profitable segment for 2025 to 2035. The continued evolution of medical technology, especially in diagnostic and therapeutic devices, has raised the demand for specialist medical components immensely.

These components, such as sensors, connectors, and housings for vital devices, form the backbone of the increasing trend towards minimally invasive procedures, telemedicine, and personalized care. As these technologies develop, the need for accurate, reliable, and biocompatible parts will keep on increasing, and this segment will remain extremely profitable.

This category will grow at a CAGR of 5.5% during the forecast period, as the complexity and miniaturization of medical products increase.

Country-Wise Analysis

United States

The United States is a dominant power in the global medical plastics market, thanks to its highly developed healthcare system and heavy investments in medical technology. With a well-developed healthcare infrastructure, the USA experiences high demand for medical plastics in a variety of applications, such as components for medical devices, packaging, and diagnostic equipment.

In the USA, there is also a strong emphasis on sustainable development in medical plastics production, with increased application of recyclable and biocompatible materials. In addition, the ongoing innovation of cutting-edge technologies such as 3D printing and personalized medicine encourages innovation in the medical plastics industry. Fact.MR opines that the CAGR of the United States is 5.3% from 2025 to 2035.

India

India's healthcare plastic industry is growing tremendously on account of India's exploding healthcare market and escalating demands for economical, throw-away type of medical goods. Following growth of the middle-class sector and broader healthcare coverage and availability of the medical service industry, the usage of such plastic health materials like syringes, IV pouches, and diagnostics hardware skyrocketed.

Besides this, India's booming medical device manufacturing industry takes advantage of the low-cost yet high-quality medical plastics, generating tremendous opportunities for both local and foreign players.Market growth is also substantiated by an increasing awareness of hygiene and infection control procedures. Fact.MR is of the opinion that the CAGR of India is 5.1% from 2025 to 2035.

China

China's healthcare plastics market is growing at a very fast rate with its huge population, aging population, and increasing healthcare infrastructure. The nation has witnessed a substantial increase in demand for medical plastics, especially in diagnostic device components, packaging, and surgical devices. The healthcare reforms and medical technology investments of the Chinese government are at the core of the market growth.

With the rising demand for medical devices, including ventilators, dialysis equipment, and diagnostic devices, comes the demand for advanced materials, high-performance plastics in particular, which provide increased durability, chemical resistance, and ease of sterilization. Fact.MR projects that the CAGR of China is 5.2% from 2025 to 2035.

United Kingdom

The medical plastics market in the United Kingdom is experiencing consistent growth due to the country's robust healthcare infrastructure and increased demand for disposable medical products. The UK is a key contributor to the European medical device market, and demand for medical plastics is found across a spectrum of applications such as surgical devices, diagnostic equipment, packaging, and sterilization items.

With an aging population comes greater healthcare requirements, and the need for durable and safe medical devices increases, driving the application of high-performance plastics in the manufacture of these devices. Fact.MR opines that the CAGR of the United Kingdom is 5.0% from 2025 to 2035.

Germany

Germany is among Europe's most significant markets for medical plastics, backed by the country's advanced healthcare infrastructure and dominance in manufacturing medical devices. The demand for medical plastics in the country stems from its well-established healthcare system, an ageing population, and the growing rate of chronic illnesses, which call for innovative medical solutions.

Germany's robust manufacturing sector, especially in the area of medical devices such as diagnostic imaging, surgical devices, and implants, is one of the main drivers of demand for high-performance plastics. The requirement of precision, safety, and performance by the healthcare sector creates a strong demand for innovative plastic material. Fact.MR projects that the CAGR of Germany is 5.1% from 2025 to 2035.

South Korea

South Korea's medical plastics industry is dominated by innovation and speedy technological uptake with high priority to high-quality medical devices and packaging materials. The advanced healthcare system as well as emphasis on technological innovation in medical devices make South Korea a leading force in the world medical plastics industry.

South Korea's healthcare industry is enriched by advanced research and development in materials science that makes possible the application of sophisticated plastics in diagnostic, therapeutic, and surgical contexts. In addition, the government initiative for upgrading healthcare infrastructure and investment in medical technologies leads to the increasing need for specialty medical plastics. Fact.MR is of the opinion that the CAGR of South Korea is 5.0% from 2025 to 2035.

Japan

Japan is likely to experience steady growth in its medical plastics market due to its aging population, which boosts the need for medical devices and healthcare solutions. The aging population and high level of healthcare standards in the country drive the demand for sophisticated medical products, such as diagnostic equipment, surgical instruments, and drug delivery systems, all of which are highly dependent on medical plastics.

The nation's close attention to R&D in medical materials, especially for high-performance and bio-compatible plastics, makes it a pioneer in the industry. With ongoing investments in medical infrastructure, the demand for medical plastics in Japan is likely to grow steadily. Fact.MR forecasts that the CAGR of Japan is 5.2% from 2025 to 2035.

France

France's medical plastics market is backed by a developed healthcare system, aging population, and increasing medical device demand by the country. The demand for sophisticated medical plastics is growing driven by the developing chronic disease pattern and demand for minimally invasive treatments.

France is the largest healthcare market in Europe, and the increasing use of new medical technologies has driven the need for specialized medical plastics. France's government has also invested heavily in healthcare facilities, which have boosted the consumption and production of medical devices.

As one of the prominent players in the European Union, France gains the advantage of strong trade, thus increasing its foothold in the international market of medical plastics. Fact.MR opines that the CAGR of France is 5.1% from 2025 to 2035.

Italy

Italy's medical plastics sector is developing in a sustained manner, helped by the manufacturing capabilities and healthcare-oriented sector in Italy. Italy's requirement for high-quality and low-cost medical equipment and medical packing materials drives demand for medical plastics.

Patient safety orientation by the healthcare sector along with increasing demographics of elderly patients are boosting demand for disposable healthcare products such as syringes, catheters, and diagnostics equipment.

Besides this, Italy is also gaining momentum as a location for the manufacturers of medical devices, enhancing demand for expert materials in the production of these devices. Fact.MR projects that the CAGR of Italy is 5.0% from 2025 to 2035.

Australia-New Zealand

Australia and New Zealand are also experiencing strong expansion in the medical plastics market as demand for high-quality health products continues to grow, coupled with an aging population that is spreading rapidly.

With both nations investing in enhancing healthcare infrastructure and increasing access to healthcare services, demand for medical plastics, most notably in devices and packaging, will grow. The emphasis on well-being and health, in combination with the embrace of latest medical technologies, is driving growth in this area.

With robust healthcare infrastructures and increasing awareness of the necessity for infection control, the medical plastics market in Australia and New Zealand will grow at a very high rate. Fact.MR is of the opinion that the CAGR of Australia-New Zealand is 5.1% from 2025 to 2035.

Fact.MR Survey Results: Medical Plastics Industry Dynamics based on Stakeholder Perspectives

(Surveyed Q4 2024, n=450 stakeholder participants evenly distributed across manufacturers, distributors, healthcare providers, and end-users in the USA, Western Europe, Japan, and South Korea)

Key Priorities of Stakeholders

Global Priorities

- Regulatory Compliance: 80% of the respondents worldwide listed compliance with medical device regulations (e.g., FDA, CE marking) as a "critical" priority.

- Biocompatibility and Safety: 74% saw reducing risk of adverse reactions in patients through the use of biocompatible materials as essential.

- Cost Efficiency: 70% pointed towards cost-effective manufacturing as essential for medical devices and packaging in order to provide competitive prices.

Regional Variance:

- USA: 72% emphasized regulatory compliance and risk management, prompted by strict FDA regulations.

- Western Europe: 78% emphasized sustainability (e.g., biodegradable plastics, recyclability) as an increasing priority, prompted by EU legislation.

- Japan/South Korea: 65% emphasized product integrity and low toxicity to meet patient safety demands in advanced treatments.

Adopting Advanced Technologies

High Variance

- USA: 56% of producers are incorporating advanced polymer technologies (e.g., biodegradable plastics, antimicrobial coatings) for medical use.

- Western Europe: 62% apply 3D printing and customization technologies in prosthetics and surgical implants, with Germany at 68% adoption.

- Japan: 32% have embraced automated injection molding systems for precision, but only 19% are investing in bioplastics.

- South Korea: 48% are using AI for quality control and accuracy in the manufacture of medical plastics.

Convergent and Divergent Views on ROI:

- USA: 68% see automation and advanced materials technologies as enhancing ROI through greater efficiency and patient outcomes.

- Japan: Just 40% see advanced material investments as worthwhile, prioritizing cost-saving options for medical devices.

Material Preferences

Consensus:

- Polyethylene (PE) and Polypropylene (PP): 68% chose these materials in general because of their biocompatibility, low toxicity, and cost-effectiveness, especially in drug delivery systems and packaging.

Regional Variance:

- Western Europe: 56% chose PVC because of its versatility and cost-effectiveness in different medical devices, as opposed to 38% worldwide.

- Japan/South Korea: 42% chose hybrid materials (e.g., PE-PET blends) to balance cost and functionality for medical device packaging.

- USA: 63% remained adhered to polypropylene and polyethylene, while 22% inclined towards bio-based plastics in environmentally conscious segments.

Price Sensitivity

Shared Challenges:

- Material Costs: 85% named increased raw material costs (e.g., polyethylene up 22%, bioplastics up 18%) as a major challenge for manufacturers.

Regional Differences:

- USA/Western Europe: 58% are willing to pay 10-15% premium for biodegradable or environmentally friendly plastic materials.

- Japan/South Korea: 72% are concerned with minimizing production costs, with 60% of stakeholders being interested in low-cost options below USD 3 per unit.

- South Korea: 40% favor leasing arrangements or co-ownership of material sourcing to balance high initial expenses, versus 20% in the USA.

Pain Points in the Value Chain

Manufacturers:

- USA: 62% reported difficulty in material availability, especially high-volume plastic grades for medical devices.

- Western Europe: 54% reported regulatory complexity (e.g., the need for CE certification) as a market entry obstacle.

- Japan: 58% mentioned difficulty with long approval processes of new medical plastics according to local requirements.

Distributors:

- USA: 70% mentioned delays in supply chains because of the world shortage of certain polymers.

- Western Europe: 45% mentioned competition from low-cost vendors outside the EU.

- Japan/South Korea: 60% mentioned difficulty in transporting to rural healthcare centers.

End-Users (Healthcare Providers/Medical Institutions):

- USA: 40% mentioned "high procurement costs" as a prime concern, especially in budget-strapped hospitals.

- Western Europe: 38% lamented regulatory delays in bringing new plastic-based medical devices into healthcare streams.

- Japan: 50% complained of the unavailability of certain high-performance plastics for specialized medical applications.

Future Investment Priorities

Alignment:

- 75% of world manufacturers intend to invest in green plastic technologies (e.g., bioplastics, recyclable plastics) for medical devices.

Divergence:

- USA: 59% of manufacturers intend to prioritize automation technologies (e.g., robotic injection molding), while 45% are considering alternatives such as smart polymers for wound healing.

- Western Europe: 63% are concentrating on maximizing the use of renewable plastics for medical packaging and minimizing carbon emissions during production.

- Japan/South Korea: 52% are investing in the development of hybrid materials for packaging and medical products, weighing cost vs. performance.

Regulatory Impact

- USA: 72% indicated new FDA regulations, specifically those on environmental sustainability (e.g., phasing out some plastics), are causing disruptions in the acquisition of materials for medical use.

- Western Europe: 80% of stakeholders saw the EU's Green Deal and sustainable packaging regulation as medical plastics growth drivers, with a focus on carbon footprint reduction and recyclability.

- Japan/South Korea: Only 30% said strict national laws had a significant influence on buying decisions, pointing out relatively easy enforcement compared to Western norms.

Conclusion: Variance vs. Consensus

High Consensus

- Global stakeholders concur on the paramount importance of regulatory compliance, material biocompatibility, and cost control along the medical plastics value chain. Sustainability, particularly recyclability and carbon footprint minimization, is becoming all-important to everyone.

Key Variances:

- USA: Emphasis on automation and use of high-tech materials to deliver better patient care versus Japan/South Korea: Emphasis on cost-efficient, lower-tech solutions.

- Western Europe: Unambiguously leadership in sustainability and the use of green materials over the more pragmatic hybrid material preference in Asia.

Strategic Insight:

- Stakeholders have to factor in regional regulatory landscapes and cost structures, fostering innovations such as bioplastics in the West and hybrid materials and cost-saving alternatives in Asia.

Government Regulations

| Country | Government Regulations & Policies Impacting the Market |

|---|---|

| USA | FDA Regulations: The FDA has rigorous standards for medical device approval, especially material safety, biocompatibility, and performance. |

| India | Regulatory Development: Medical devices are regulated by the CDSCO (Central Drugs Standard Control Organization), and new regulations are being enforced to guarantee device safety and efficacy. |

| China | Regulatory Oversight: Medical device approval is regulated by NMPA (National Medical Products Administration). |

| UK | Regulatory Compliance: Post-Brexit, the UK operates under its own medical device rules following the EU's MDR (Medical Device Regulation). |

| Germany | EU MDR Implementation: Being a member of the EU, Germany adheres to the Medical Device Regulation (MDR), which requires strict quality control, post-market surveillance, and clinical evaluation. |

| South Korea | Regulatory Framework: The KFDA (Korea Food and Drug Administration) regulates medical device approval, imposing stringent standards for safety and quality. |

| Japan | PMDA Oversight: Pharmaceuticals and Medical Devices Agency (PMDA) regulates standards and ensures that the devices are compliant with safety, efficacy, and quality standards. |

| France | EU MDR Standards: As a member state of the EU, France operates under the Medical Device Regulation (MDR) that focuses on safety, quality, and post-market surveillance. |

| Italy | EU Compliance: Italy conforms to the EU's Medical Device Regulations (MDR) focusing on device safety, biocompatibility, and patient protection. |

| Australia-New Zealand | TGA (Australia) and Medsafe (NZ) Regulation: Both nations maintain strict oversight of medical device approval, with an emphasis on safety and performance. Medsafe in New Zealand also undertakes the same processes. |

Competitive Landscape

The medical plastics industry remains fragmented, with numerous regional and global players competing across various segments. Companies are adopting strategies such as product innovation, strategic partnerships, and mergers and acquisitions to strengthen their market positions.

Leading companies in the medical plastics sector are focusing on pricing strategies, technological innovation, and expanding their global presence. They are investing in research and development to introduce advanced materials that meet the evolving needs of the healthcare industry.

In 2024, Amcor, an Australian packaging giant, announced plans to acquire Berry Global Group in a scrip merger valued at USD 8.4 billion. This acquisition aims to establish Amcor as the world's largest plastic packaging company, enhancing its presence in North America, Western Europe, and emerging markets. The deal is expected to create significant cost and scale benefits, with Berry shareholders receiving 7.25 Amcor shares per Berry share.

UFP Technologies, a USA-based company, has been actively expanding its medical manufacturing capabilities. In 2024, the company acquired several firms, including Marble Medical and Welch Fluorocarbon, to enhance its product portfolio and international footprint. These acquisitions align with UFP's strategy to focus on the medical sector, which now accounts for over 90% of its revenue.

Market Share Analysis

Dow Inc.- ~15-20%

A global market leader in medical-grade plastics, Dow offers silicones, polyethylene (PE), and polypropylene (PP) for uses such as IV devices, syringes, and surgical drapes. Its DOW™ Medical Grade Silicones play a pivotal role in implantable devices with regard to biocompatibility and endurance.

BASF SE- ~12-16%

BASF provides high-performance polymers such as Ultramid® (PA), Ultradur® (PBT), and Ecoflex® (biodegradable plastics), which are used extensively in medical packaging, drug delivery systems, and surgical instruments. Its Ultrasim® simulation tool is used to optimize plastic part designs for FDA/EU compliance.

SABIC- ~10-14%

SABIC's expertise lies in high-temperature thermoplastics like ULTEM™ (PEI) and LEXAN™ (PC) that find applications in sterilizable surgical instruments, imaging devices, and breathing masks. Its TRUCIRCLE portfolio comprises certified recycled plastics for eco-friendly medical solutions.

DuPont de Nemours, Inc.- ~8-12%

DuPont leads in medical packaging (Tyvek®) and high-purity plastics for catheters and wearables. Its Zytel® (PA) and Crastin® (PBT) resins are utilized in load-bearing implantable devices. The Liveo™ silicone solutions of the company are essential in minimally invasive surgery tools and wearable drug pumps.

Celanese Corporation- ~6-9%

Celanese is a significant provider of engineering plastics, such as POM (acetal), PEEK, and PVDF, which find applications in orthopedic implants, dental equipment, and fluid management systems. Its Zenite® LCP facilitates miniaturization of intricate surgical components.

Arkema Group- ~5-8%

Arkema's Pebax® elastomers find extensive applications in balloon catheters, endotracheal tubes, and prosthetics because of their flexibility and resistance to fatigue. Its Kynar® PVDF is critical for chemical-resistant laboratory equipment and filtration membranes.

Other Key Players

- Covestro AG

- Evonik Industries AG

- Eastman Chemical Company

- Solvay S.A.

- LG Chem

- Mitsubishi Chemical Group

- Toray Industries

- Victrex plc

- Ensinger GmbH

- Röchling Group

- Tekni-Plex

- Trinseo

- PolyOne Corporation (Avient)

- EMS-Grivory

Segmentation

Segmentation by Type:

- Standard Plastics

- Engineering Plastics

- High Performance Plastics (HPP)

- Silicone

- Others

Segmentation by Application:

- Medical Device Packaging

- Medical Components

- Orthopedic Implant Packaging

- Orthopedic Soft Goods

- Wound Care

- Cleanroom Supplies

- BioPharm Devices

- Mobility Aids

- Sterilization & Infection Prevention

- Tooth Implants

- Denture Base Materials

- Others

Segmentation by Region:

- North America

- Latin America

- Europe

- East Asia

- South Asia

- Oceania

- Middle East and Africa (MEA)

- Frequently Asked Questions -

What are the most important trends that are determining the medical plastics market in 2024?

In 2024, innovation in the medical plastics market is being driven by sustainability, automation, and high-performance materials, with emphasis on lowering environmental footprints and enhancing performance.

How is the COVID-19 pandemic changing the demand for medical plastics?

The pandemic has created a greater need for disposable medical devices, which has driven the consumption of medical plastics, particularly for PPE, ventilators, and hygiene products.

Which are the regions that are driving the uptake of advanced medical plastic technologies?

The USA, Western Europe, and Japan are leading the uptake of advanced medical plastic technologies, with a particular focus on automation, sustainability, and material innovation.

What are the issues confronting firms in the medical plastics industry?

Increased raw material prices, regulatory requirements, and the need to innovate while remaining cost-effective continue to be the major issues confronting industry players.

How are government regulations affecting the application of medical plastics?

More stringent regulations on sustainability and product safety, especially in Europe and North America, are compelling firms to create environmentally friendly and compliant medical plastics solutions.

Author:

Md Sanaullah

Editor:

Anushree Karale