Portable Ultrasound Equipment Market Outlook (2025 to 2035)

The global portable ultrasound equipment market is projected to be valued at USD 2.42 billion by 2025. As per Fact.MR’s analysis, the industry will grow at a CAGR of 6.8% and reach USD 4.68 billion by 2035. The rising prevalence of cardiovascular diseases and surging demand for point-of-care diagnostics are driving the adoption of portable ultrasound equipment in cardiovascular applications.

In 2024, the portable ultrasound devices sector experienced significant growth, driven by increased interest in point-of-care diagnosis and a growing focus on non-invasive and real-time imaging solutions. Clinical uptake accelerated in emergency care departments, outpatient facilities, and rural healthcare settings, where the availability and prompt diagnosis became even more crucial.

As the industry enters 2025, it is poised for growth at an accelerating pace, as global healthcare systems intensify their focus on early disease diagnosis and patient-centric care models. The intersection of portable design advancements, growing geriatric populations, and increasing chronic disease burdens, like cardiovascular disease and endocrine disorders, is generating fertile ground for mass deployment.

| Metric | Value |

|---|---|

| Industry Value (2025E) | USD 2.42 billion |

| Industry Value (2035F) | USD 4.68 billion |

| CAGR (2025 to 2035) | 6.8% |

Market Analysis

The point-of-care ultrasound equipment industry is on a solid growth path, driven by escalating demand for real-time, non-invasive diagnostic imaging with escalating rates of chronic disease and aging populations.

The key drivers are advances in AI-driven imaging, increased use in emergency care, and increased access to remote or underserved locations. Healthcare providers, diagnostic facilities, and patients requiring fast, point-of-care imaging will benefit most, whereas conventional, cumbersome imaging systems might see declining demand.

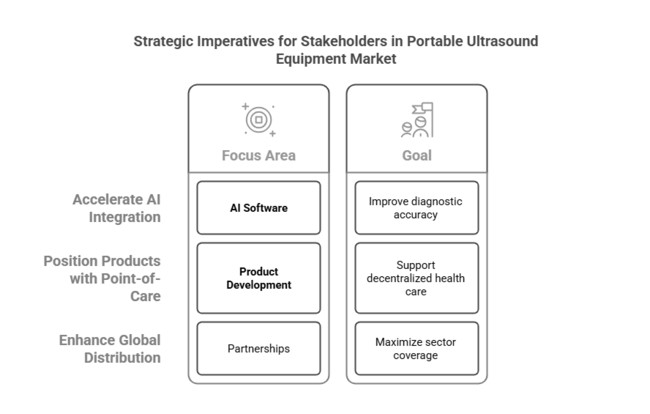

Top 3 Strategic Imperatives for Stakeholders

Speed Up AI Integration and Software Improvement

Investors should make AI-driven imaging software a top priority to increase diagnostic accuracy, automate image review, and lower clinician burden, making equipment more appealing to high-volume health care environments.

Position Products with Point-of-Care and Remote Care Models

Companies need to design product development and service delivery in a way that supports the quick transition to decentralized health care by developing small, simple-to-use devices that can be used for home care, rural clinics, and emergency use.

Enhance Global Distribution and Strategic Partnerships

In order to achieve maximum sector coverage and scalability, stakeholders must prioritize establishing partnerships with telehealth platforms, hospital networks, and regional distributors, as well as pursuing targeted M&A to enhance R&D capabilities and geographic reach.

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability - Impact |

|---|---|

| Delays in Device Approvals by Regulation - Longer approval processes or changing standards of compliance could delay product introductions and prolong sector entry. | Medium - High |

| Excessive Price of Sophisticated Technologies Constraining Use in Low-Income Areas - Affordability is still a hurdle, especially among developing countries with limited healthcare budgets. | High - Medium |

| Challenges to Data Privacy and Security in AI-Incorporated Devices - Growing cloud-based diagnostics reliance creates concerns regarding patient data security and cybersecurity risks. | Medium - High |

1-Year Executive Watch-List

| Priority | Immediate Action |

|---|---|

| Enhance AI-Powered Diagnostic Features | Establish strategic collaborations for co-development and integration of AI algorithms within imaging platforms. |

| Improve Accessibility in Emerging Economies | Conduct an industry viability study for cost-reduced models specific to underserved areas. |

| Bolster Regulatory Agility | Create a regulatory intelligence unit to actively respond to changing global compliance regimes. |

For the Boardroom

To stay ahead, companies will have to focus on the coming together of portability, accuracy, and digital integration within ultrasound diagnostics. Such intelligence points toward a pressing need to rebuild roadmaps toward AI-infused point-of-care image solutions for urban hospitals as well as for rural geographies.

Organizations need to accelerate R&D spending into adaptive, miniaturized systems and intensify partnerships with telemedicine platforms in order to increase reach. Futuristic companies will also anticipate regulatory changes and build security-by-design mechanisms into AI systems to ensure clinical trust. This strategic move is necessary not only for competitiveness but also for leadership in the next generation of diagnostic care.

Fact.MR Survey Results: Portable Ultrasound Equipment Industry Dynamics Based on Stakeholder Perspectives

(Surveyed Q4 2024, n=450 stakeholder participants evenly distributed across manufacturers, distributors, hospitals, diagnostic centers, and ambulatory care centers in the USA, Western Europe, Japan, and South Korea)

Stakeholder Main Priorities

- Regulative Compliance: 78% of stakeholders worldwide rated compliance with medical device rules (e.g., FDA, CE) as a "critical" priority for sustaining industry access.

- Ease of Use and Portability: 71% prioritized lightweight and small size to improve mobility within point-of-care environments.

Regional Difference:

- USA: 65% expressed advanced wireless connectivity (e.g., integration with cloud storage) as a high priority, versus Japan's 40%.

- Western Europe: 83% ranked sustainability (e.g., recyclable components, energy-efficient equipment) as a top consideration for investments in the future.

- Japan/South Korea: 58% emphasized high-definition imaging capabilities due to the growing need for diagnostic precision.

Adopting Advanced Technologies

High Variance

- USA: 63% of healthcare providers have embraced AI-enabled portable ultrasound equipment, especially in the emergency department and telemedicine programs.

- Western Europe: 47% have installed wireless ultrasound systems, and Germany (58%) has done so as a result of government incentives for digital health.

- Japan: Only 25% of small clinics employ advanced features such as AI or cloud connectivity since costs are still a barrier.

- South Korea: 40% have implemented IoT-enabled devices for remote monitoring, especially in rural regions where access to healthcare specialists is low.

Convergent and Divergent Views on ROI

- USA: 72% of stakeholders feel that investment in AI-enabled ultrasound machines promises long-term cost savings and effectiveness.

- Japan: 50% are still inclined towards conventional, non-digital systems, as ROI on high-end technology is seen to be delayed.

Material Preferences

Consensus:

- Plastic & Composite Materials: Selected by 66% worldwide owing to portability and affordability, particularly for handheld and mobile devices.

Variance:

- Western Europe: 52% opt for metal-alloy casings (e.g., aluminum) due to requirements for durability and sustainability in environmentally aware regions.

- Japan/South Korea: 45% adopt hybrid materials for a compromise between durability and light weight, especially for miniaturized, handheld products.

- USA: 70% remain with top-grade plastic composites due to their cost-effectiveness and simplicity of maintenance.

Price Sensitivity

Shared Challenges:

- 85% mentioned increasing production and component prices (e.g., semiconductors, battery technology) as a primary concern impacting pricing strategies.

Regional Differences:

- USA/Western Europe: 64% would pay a 15-20% premium for products with advanced AI features and wireless connectivity.

- Japan/South Korea: 70% are interested in cost-effective, entry-level models (below USD 5,000), with little interest in premium features.

- South Korea: 50% opt for leasing arrangements to cover upfront expenses compared with only 20% in the USA.

Pain Points in the Value Chain

Manufacturers:

- USA: 58% of the manufacturing companies identify difficulties in semiconductor shortages affecting production timelines for high-end devices.

- Western Europe: 42% cite the regulatory complexity of securing CE certification as a region entry barrier.

- Japan: 53% have problems with inadequate adoption of new technology in small clinics because of very high upfront costs.

Distributors:

- USA: 63% experience delays in logistics and deliveries of key components from foreign suppliers.

- Western Europe: 45% mention intense competition from low-cost providers, especially from Eastern Europe and Asia.

- Japan/South Korea: 58% have problems with rural transportation logistics, particularly in mountainous areas.

End Users (Hospitals/Clinics):

- USA: 49% say that the technical complexity of new ultrasound machines is a significant barrier, especially in point-of-care settings.

- Western Europe: 38% are challenged by retrofitting existing clinics with newer ultrasound machines, affecting adoption rates.

- Japan: 55% mention inadequate technical support for advanced models of ultrasound machines, preventing full use of features.

Emerging Investment Priorities

Alignment:

- 71% of world manufacturers intend to expand investment in AI and machine learning integration for advanced diagnostic functionality.

Divergence:

- USA: 63% will concentrate on designing rugged, portable devices for emergency medical services (EMS) and field hospitals.

- Western Europe: 59% are setting priorities for designing green and power-efficient ultrasound models to fit sustainability objectives.

- Japan/South Korea: 48% consider miniaturized devices with high-quality imaging that are simple to carry for rural healthcare facilities.

Regulatory Impact

- USA: 65% of respondents believe FDA regulations are getting tighter, especially for transportable devices with AI capabilities, which may hinder innovation and region entry.

- Western Europe: 78% see the EU Medical Device Regulation (MDR) as a growth driver since it promotes medical technology innovation while maintaining patient safety and device quality.

- Japan/South Korea: 30% indicate that regulatory influence is lower because relatively less stringent enforcement of medical device regulation, particularly of handheld devices, exists.

Conclusion: Variance vs. Consensus

- High Consensus: Stakeholders' top concerns across the world are regulatory compliance, portability, and cost pressures.

Key Variances:

- USA: An emphasis on automation and AI is countered by Japan/South Korea's desire for easier, cheaper options.

- Western Europe: Sustainability dominates the agenda here, with Asia preferring hybrid options that strike a balance between cost and functionality.

Strategic Insight:

- Region-specific strategies, keeping in mind local preferences-wireless and AI-based devices for the USA, small and affordable models for Japan/South Korea, and eco-friendly designs for Western Europe-are the key to effectively penetrating these heterogeneous sectors.

Government Regulations

| Country | Impact of Policies & Regulations |

|---|---|

| USA | FDA Certification: Portable ultrasound devices have to be FDA-approved, particularly for those that incorporate AI and wireless technology. Strict FDA regulations guarantee safety but can delay sector access. |

| India | Bureau of Indian Standards (BIS): Required for some medical devices. Clarity of regulations is increasing, although enforcement is uneven. |

| China | NMPA Certification: National Medical Products Administration (NMPA) approval is necessary for medical devices. China has been increasing regulations for safety. |

| UK | MHRA Approval: Portable ultrasound equipment needs to comply with regulatory requirements set by the Medicines and Healthcare Products Regulatory Agency (MHRA). Post-Brexit, the UK regulatory environment is separating from that of the EU. |

| Germany | CE Marking: Equipment sold in Germany should bear CE marking, confirming that it adheres to EU health, safety, and environmental protection requirements. Intensive enforcement under the MDR. |

| South Korea | KFDA Approval: Devices need to be approved by the Korea Food and Drug Administration (KFDA). A strong regulatory framework that assures medical device safety. |

| Japan | PMDA Approval: Japan's Pharmaceuticals and Medical Devices Agency (PMDA) demands strict approval for ultrasound devices. Increased focus on integrating AI has resulted in delayed approvals. |

| France | CE Marking: Being a part of the EU, France also demands CE marking on medical devices. Sustainability and ecological design regulation is also influencing manufacturers to enhance product lifecycle management. |

| Italy | CE Marking: Like France, Italy demands CE marking, and regulatory adherence is synchronized with EU directives. Italy also has dedicated mandates for medical equipment utilized in healthcare institutions. |

| Australia-New Zealand | TGA Certification (Australia): Portable ultrasound devices must be registered with the Therapeutic Goods Administration (TGA). New Zealand has a parallel regulatory system under Medsafe. |

Segment-Wise Analysis

By Application

The cardiovascular application is likely to be the most profitable segment between 2025 and 2035, fueled by the increasing global incidence of heart diseases and the demand for early, non-invasive diagnostic methods. With heart-related ailments being a top cause of morbidity and mortality globally, the demand for real-time imaging for diagnosis, monitoring of treatment, and pre-surgical evaluation will continue to grow.

In addition, technical improvements in handheld ultrasound devices, including AI-driven image interpretation, will further enhance diagnostic quality, driving still further adoption in cardiology. The cardiovascular segment will grow at a CAGR of 7.2% during the forecast period, mirroring the central and increasing position of portable ultrasound in cardiology.

By Product Type

Portable ultrasound machines are anticipated to be the most rewarding segment for stakeholders during the forecast period. This is largely fueled by their portability, cost-effectiveness, and the growing need for point-of-care diagnosis, particularly in emergency rooms, rural health, and home care.

These machines are small, simple to operate, and can be utilized in various environments without the necessity of a complete imaging system. The capability to deliver immediate, real-time imaging at the bedside greatly improves clinical workflow, rendering handheld devices ever more essential for rapid decision-making across many medical specialties, such as cardiology, gynecology, and musculoskeletal.

The handheld ultrasound devices are expected to grow at a CAGR of 7.5% over the forecast period, spurred by ongoing technological advancements and increasing uptake in low-resource environments.

By End User

Hospitals will be the most profitable segment for 2025 to 2035. This is because of the increasing demand for point-of-care imaging across hospital departments like emergency departments, intensive care units (ICUs), and operating rooms. With hospitals increasingly using portable ultrasound machines for quick, real-time diagnosis, particularly for critically ill patients, this segment will see high growth.

Their integration into clinical workflows, facilitated by advances in AI and imaging technology, will further boost their use within hospitals, where patient throughput and diagnostic effectiveness are critical.

The hospital segment is anticipated to grow at a CAGR of 7.0% through the forecast period, with the rise in the dependency on portable ultrasound for rapid, non-invasive diagnostics and evaluations in high-stress conditions.

Country-Wise Analysis

United States

The USA portable ultrasound equipment industry will witness strong growth during 2025 to 2035 due to the increasing demand for point-of-care diagnosis and telemedicine expansion. Due to the growing population aging and the spread of chronic diseases such as cardiovascular diseases, cancer, and diabetes, medical practitioners need more efficient and portable diagnostic imaging tools.

The USA healthcare industry's ongoing quest for cost-effective solutions will propel the development of portable ultrasound devices, particularly for emergency treatment, outpatient clinics, and home healthcare.

Additionally, the incorporation of high technologies like AI and machine learning into ultrasound devices is increasing their diagnostic power, rendering them more appealing to healthcare providers desiring real-time, accurate imaging to make better-informed decisions. Fact.MR suggests that the CAGR of the USA sector will be 7.2% from 2025 to 2035.

India

The sector in India is growing at a fast pace because of the country's huge population and its growing demand for affordable healthcare services. The demand for portable ultrasound machines is being fueled by the growth in healthcare infrastructure, especially in rural and underdeveloped areas where access to conventional imaging machines is scarce. Increasing cases of chronic diseases, such as cardiovascular diseases and diabetes, are fueling the demand for non-invasive diagnostic equipment.

As mobile healthcare services are growing, particularly in rural parts, the portable ultrasound industry is likely to witness high growth over the forecast period. Fact.MR forecasts that the CAGR of the industry will be 7.5% from 2025 to 2035 in India.

China

China's landscape is fueled by its large population, aging population, and the nation's increasing emphasis on modernizing its healthcare system. The rising incidence of chronic diseases like heart disease, stroke, and cancer is driving up demand for mobile diagnostic technology. The government's heavy investments in the healthcare infrastructure, especially in rural and remote locations, will drive sector growth as portable ultrasound machines offer a cost-effective way to increase diagnostic imaging access.

The healthcare system's transition toward preventive treatments and the early detection of disease will fuel additional demand for portable ultrasound machines, especially in point-of-care applications like emergency rooms and outpatient clinics. China’s sales will be growing at a CAGR of 7.0% from 2025 to 2035.

United Kingdom

The CAGR of the UK’s sales will be 6.5% during the forecast period. In the UK, the sales for portable ultrasound is gaining from the increasing demand for non-invasive diagnostic technology, particularly in the National Health Service (NHS) and private hospitals. The rising incidence of chronic diseases like cardiovascular diseases, musculoskeletal disorders, and cancer is propelling the demand for more effective diagnostic equipment.

Incorporation of AI and cloud-based technologies in portable ultrasounds is improving their diagnostic efficacy, in turn, fuelling their adoption in the UK healthcare infrastructure. These developments will be instrumental in enhancing the provision of healthcare and helping to achieve swifter, more precise diagnoses nationwide.

Germany

Initiatives by the government to make healthcare more accessible in rural and remote regions will be instrumental in growing the sector. In addition, the inclusion of cutting-edge technologies, including machine learning and artificial intelligence, into portable ultrasound equipment will increase the accuracy of diagnostics and render portable ultrasound equipment more appealing to medical professionals. Fact.MR projects that the CAGR of Germany’s sector will be 6.8% from 2025 to 2035.

The German industry for portable ultrasound devices is projected to expand consistently, driven by the nation's sophisticated healthcare system and rising need for point-of-care diagnostics. The incidence of chronic diseases like cardiovascular diseases, diabetes, and musculoskeletal disorders is pushing the use of portable ultrasound devices in emergency rooms, outpatient facilities, and rehabilitation facilities.

South Korea

According to Fact.MR the industry in South Korea’s industry will be growing at CAGR of 7.3% during the assessment period. South Korea's portable ultrasound sector is going to experience substantial growth because of the country's highly advanced healthcare system and increasing demand for mobile diagnostics.

The increase in chronic diseases, including cardiovascular diseases and diabetes, coupled with an aging population, is boosting demand for portable ultrasound devices, especially in emergency care and point-of-care applications.

Moreover, the focus in the country on incorporating artificial intelligence and other advanced technologies into medical devices is likely to increase the functionality of portable ultrasound machines, making them better at diagnosing a variety of conditions.

Japan

Japan's healthcare system is highly developed, and there's an increasing focus on preventative care, early disease diagnosis, and mobile health options, all of which are fueling demand for portable ultrasound units. Since the population of Japan keeps aging, there will be an increasing demand for the management of chronic diseases, especially in musculoskeletal and cardiovascular diseases, further increasing the expansion of portable ultrasound equipment.

Further, Japan's extensive research and development in healthcare technologies, including AI-based ultrasound devices, is expected to fuel the implementation of high-end portable ultrasound devices. The CAGR of Japan’s industry will be 6.7% from 2025 to 2035.

France

Fact.MR opines that the CAGR of France’s sector will be 6.6% from 2025 to 2035.France's point-of-care ultrasound sector will expand as the nation's healthcare infrastructure welcomes point-of-care diagnostics more and more, particularly in emergency settings and among outpatient populations.

As cardiovascular conditions, cancer, and other long-term illnesses become more prevalent, demand for effective, mobile ultrasound machines will grow. France will also witness more integration of new technologies, like AI, in ultrasound machines to enhance diagnostic accuracy and speed.

Italy

Fact.MR forecasts that the CAGR of Italy’s sector will be 6.9% from 2025 to 2035. Italy's portable ultrasound equipment domain is predicted to grow dramatically with the increased need for mobile diagnostics, especially in emergency rooms, outpatient centers, and home care. The country's elderly population and increased rates of chronic disease, like cardiovascular disease, diabetes, and musculoskeletal conditions, will propel the use of portable ultrasound devices.

Furthermore, the efforts of the Italian government to increase healthcare accessibility in rural and underserved areas will also boost the demand for portable ultrasound devices. The integration of AI and telemedicine solutions in ultrasound equipment will also propel the growth of the industry, providing enhanced diagnostic functionality and improving the overall delivery of healthcare.

Australia-New Zealand

The Australia and New Zealand portable ultrasound segment is anticipated to grow steadily with the region's developed healthcare infrastructure and increasing point-of-care diagnostics demand. An increase in chronic conditions, including cardiovascular and musculoskeletal diseases, and the aging population are anticipated to fuel demand for portable ultrasound devices.

Moreover, the high penetration of telemedicine in these nations is fueling the need for mobile diagnostic solutions that offer real-time imaging and minimize patient waiting times. Furthermore, advancements in AI-powered ultrasound technology will increasingly stimulate the uptake of portable ultrasound equipment, facilitating greater accuracy and productivity in diagnostics. Fact.MR suggests that the CAGR of Australia-New Zealand’s industry will be 7.0% from 2025 to 2035.

Competitive Landscape

The portable ultrasound device industry is moderately consolidated with major players such as GE Healthcare, Philips Healthcare, Siemens Healthineers, and Butterfly Network dominating the sector. The presence of innovative startups, however, and regional players infuses competitiveness and dynamism in the industry environment.

Industry leaders are fighting by blending strategies such as price points, technology development, partnership-building, and business growth. Price strategies have been adjusted across various segments, with multiple product offerings from basic models at lower prices to top-end products with superior features. Technology is also a strong point of focus, with firms putting investment into the incorporation of artificial intelligence, wireless functionality, and enhanced imaging capability for differentiation purposes.

Recently during 2024, GE Healthcare introduced the Venue Sprint™, a portable ultrasound device designed to augment point-of-care ultrasound (POCUS) capabilities. The device combines cutting-edge AI-powered tools and facilitates easy connectivity via the Vscan Air™ handheld ultrasound system, looking to optimize workflow efficiency in clinical practice.

Furthermore, Butterfly Network gained FDA clearance in 2024, for its latest-generation handheld point-of-care ultrasound system, the Butterfly iQ3. The device has a new ergonomic design, twice the data-processing speed, and enhanced imaging capabilities, such as improved 3D imaging and automated image capture modes.

Moreover, in 2024, Vave Health collaborated with the Inteleos Foundation to increase access to ultrasound technology in low-income and limited-resourced communities across the world. The collaboration is designed to reduce health disparities by equipping underprivileged people with necessary diagnostic technology.

Market Share Analysis

GE Healthcare ~25-30%

GE Healthcare is a global medical imaging leader, which includes portable ultrasound systems. Established through its Voluson, LOGIQ, and Vivid brands, GE is providing high-performance handheld and cart ultrasound machines for numerous applications (OB/GYN, cardiology, emergency care).

Philips Healthcare~20-25%

Philips is a top competitor in portable ultrasound, offering Lumify (handheld) and EPIQ/Affiniti (cart-based) systems. Philips has a portfolio centered around point-of-care ultrasound (POCUS) and tele-ultrasound solutions, incorporating AI for rapid diagnostics.

Siemens Healthineers~15-20%

Siemens Healthineers provides advanced portable ultrasound equipment such as the ACUSON Freestyle (handheld) and ACUSON Juniper (cart-based). Siemens has a strong track record in AI imaging and specializes in cardiovascular and general imaging sectors.

Canon Medical Systems (previously Toshiba Medical)~10-12%

Canon Medical offers mobile ultrasound solutions under its Aplio and Viamo series, which is known for high-resolution imaging and advanced Doppler technologies. The firm is targeting radiology, cardiology, and women's health, emphasizing the use of lightweight and compact systems in clinics and hospitals.

Fujifilm Sonosite (Fujifilm Holdings) ~8-10%

Fujifilm Sonosite is the point-of-care ultrasound (POCUS), focused on rugged, portable solutions such as the Sonosite LX and Edge II. It leads in emergency medicine, musculoskeletal (MSK), and anesthesia use cases.

Butterfly Network (Butterfly iQ+) ~5-8%

Butterfly Network disrupted the industry with its Butterfly iQ+, the first single-probe, pocket-sized ultrasound based on semiconductor technology. The firm utilizes AI and cloud-based analytics, bringing ultrasound within reach of primary care and telemedicine.

Other Key Players

- EchoNous, Inc.

- Terason(a subsidiary of Teratech Corporation)

- Verathon, Inc.

- Esaote SpA

- Clarius Mobile Health

- Mindray Medical International Limited

- Samsung Healthcare(part of Samsung Medison)

- Healcerion Co., Ltd.

- Sonoscanner

- CHISON Medical Technologies

- Medgyn Products, Inc.

- Promed Technology Co., Ltd.

Segmentation

Segmentation by Application:

- Radiology

- Gynecology

- Musculoskeletal

- Cardiovascular

- Gastrointestinal

- Others

Segmentation by Product:

- Cart/Trolley-based Ultrasound Devices

- Handheld Ultrasound Devices

Segmentation by End User:

- Hospitals

- Diagnostic Centers

- Ambulatory Care Centers

- Others

Segmentation by Region:

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- Middle East and Africa (MEA)

- Frequently Asked Questions -

What are the new developments in portable ultrasound technology?

The industry is evolving with AI-based imaging, wireless functionality, and smaller forms, which increase diagnostic accuracy and convenience across diverse clinical settings.

How are businesses responding to the increased demand for portable ultrasound devices?

Businesses are innovating with enhanced device capability, strategic partnerships, and aligning to users' requirements for mobile, point-of-care diagnosis, particularly in rural and underserved communities.

How do government regulations affect portable ultrasound devices?

Regulatory mechanisms provide safety and effectiveness of the devices by virtue of compulsory certificates and quality management, which inspire innovation and help ensure compliance with major sectors.

How is collaboration between industries impacting the creation of portable ultrasound devices?

Collaborations between providers of healthcare services and technology players are speeding up the adoption of portable ultrasound equipment, driving breakthroughs in integrating AI and friendly user interfaces.

What are the major challenges confronting stakeholders in the handheld ultrasound industry?

Increased material prices, complicated regulatory environments, and requirements for affordable solutions within growing economies are major obstacles confronting manufacturers and distributors alike.

Author:

Md Sanaullah

Editor:

Anushree Karale