Undercarriage Components Market Outlook (2025 to 2035)

The global undercarriage components market is forecast to reach USD 16.7 billion by 2035, up from USD 11.2 billion in 2025. During the forecast period, the industry is projected to register a CAGR of 4.1%, driven by the rising demand for construction and agricultural machinery, as well as advances in undercarriage system technologies. This upward trend is driven by the robust growth of infrastructure development projects worldwide, which require undercarriage systems for heavy machinery.

-2025-to-2035.webp)

What are the Drivers of Undercarriage Components Market?

The global shift toward sustainability and fuel efficiency drives market growth. Manufacturers are developing lightweight, energy-efficient components to minimize overall machine weight and fuel consumption. This complies with environmental requirements and allows companies to reduce emissions and running expenses.

Tracked equipment is becoming increasingly popular in mechanized agriculture for soil preparation, planting, and harvesting. Countries moving from traditional to modern agricultural practices are introducing compact track loaders and other machines that rely heavily on efficient undercarriage systems.

The increased demand for customized equipment also drives market expansion. Contractors and fleet operators are seeking machinery that is well-suited to specific terrains or project requirements, thereby increasing the demand for specialized undercarriage designs and components.

Another major driver is the mining industry, which necessitates machinery capable of operating in harsh and abrasive conditions. Undercarriage systems designed for long wear life and low maintenance are crucial for efficiency in these operations, making performance-optimized components an excellent investment.

The integration of telematics and IoT-based monitoring systems enables real-time tracking of undercarriage wear and tear, assisting operators in planning maintenance and reducing equipment downtime. As a result, end-users are seeking smart, data-driven solutions that extend product life and reduce operating costs.

What are the Regional Trends of Undercarriage Components Market?

The North American undercarriage equipment market is expected to grow due to the increasing number of construction and mining infrastructure projects. Emissions and safety regulations are increasing the demand for advanced undercarriage technologies.

Market leaders Caterpillar Inc., John Deere, and Komatsu Ltd. drive the growth of the undercarriage component market. Changes in raw material prices and labour shortages may cause challenges.

European undercarriage equipment manufacturers prioritize the use of sustainable materials and energy-efficient technologies. Strong infrastructure and environmental regulations drive demand for high-quality undercarriage components. Market leaders Volvo Construction Equipment and Liebherr Group boost growth. Brexit and economic uncertainty may affect market dynamics.

Asia Pacific is expected to grow the fastest due to urbanization in Asian countries. Additionally, they drive demand for residential infrastructure, which in turn boosts the construction equipment market.

The Middle East and Africa region has promising prospects in the undercarriage systems market. Rising infrastructural projects and mining activities in countries such as Saudi Arabia and South Africa fuel demand. The region's strategic focus on diversification and modernization promotes market growth.

What are the Challenges and Restraining Factors of Undercarriage Components Market?

The high maintenance and replacement costs of tracked equipment pose a challenge to the market for undercarriage components. Undercarriage components, such as track chains, idlers, and rollers, are constantly worn in harsh environments, accounting for up to 50% of a heavy machine's total maintenance cost over its lifetime. This financial burden discourages frequent replacements, particularly among small and medium-sized contractors with tight budgets.

The lack of standardization across different equipment models complicates the supply and inventory of aftermarket parts. Each brand frequently requires specific dimensions and configurations, resulting in a fragmented aftermarket landscape. This increases logistical complexity and raises costs for both suppliers and end users.

Environmental regulations are prompting manufacturers to utilize more sustainable materials and operate in an energy-efficient manner, which, although beneficial in the long run, requires significant research and development (R&D) investment. Smaller businesses frequently struggle to meet these expectations due to limited financial resources and technological capabilities.

Furthermore, the growing use of wheeled machines in urban construction, which have lower maintenance requirements and greater manoeuvrability, is reducing reliance on tracked vehicles in some areas. The scarcity of skilled technicians for proper undercarriage system installation and maintenance in developing countries further limits market growth and adoption.

Country-Wise Outlook

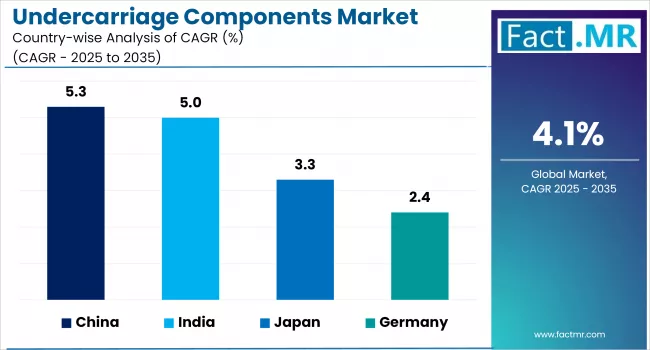

Germany's Leadership in Construction Equipment Drives Undercarriage Component Requirements

Germany's undercarriage component market is shaped by its highly industrialized economy and extensive use of advanced machinery in construction, mining, and agriculture. Germany is Europe's largest construction equipment market, with significant investment in transportation networks and energy-efficient public projects. These initiatives boost demand for tracked machinery, which raises the need for track chains, rollers, idlers, and sprockets.

Since Germany utilizes heavy-duty machines in urban and high-frequency applications, manufacturers and users prefer components with long lifecycles and high wear resistance. Undercarriage systems now feature diagnostic sensors that monitor stress, vibration, and wear, thereby reducing downtime and enhancing productivity through Industry 4.0.

Germany's construction industry often rents equipment, which emphasizes the importance of durability and maintenance. Since then, modular or quick-fit undercarriage suppliers have grown. Flexible servicing and parts replacement are prioritized over long-term capital investment in shorter equipment lifecycles.

-2025-to-2035.webp)

China's Infrastructure Boom Drives Surging Demand for Undercarriage Components

China is one of the world's most dynamic markets for undercarriage components, due to its large construction, mining, and infrastructure sectors. With ongoing investment in transportation and industrial development, there is a high demand for excavators, dozers, and track-mounted machinery. China approved infrastructure projects worth more than USD 1.8 trillion in 2023 alone, significantly increasing the operational fleet of heavy machinery and thus the demand for robust undercarriage systems.

The "Made in China 2025" initiative, which focuses on the local production of advanced machinery and components, is a key market driver in China. This policy encourages domestic manufacturers to enhance the quality of undercarriage parts, including track shoes, rollers, idlers, and sprockets, to meet global standards. Leading Chinese OEMs, including SANY and XCMG, are expanding in-house component production or forming joint ventures to secure supply chains.

The shift toward electric and hybrid construction equipment is a major market trend, particularly in urban areas with strict emission controls. This transition is driving the development of lightweight, energy-efficient undercarriage designs that utilize composite materials and intelligent tension systems to minimize energy loss and enhance battery efficiency.

India’s Shift to Domestic Manufacturing Boosts Undercarriage Component Capabilities

India's undercarriage components market is expanding rapidly, fueled by an aggressive infrastructure development agenda. Government-led initiatives, such as the PM Gati Shakti Plan and the National Infrastructure Pipeline (NIP), which aim to invest more than USD 1.4 trillion by 2025, are driving demand for construction equipment, particularly tracked machinery like excavators, bulldozers, and crawler cranes. This surge directly correlates with increased consumption of undercarriage components, including track chains, rollers, sprockets, and idlers.

One of India's key trends is a shift toward localized manufacturing. To reduce reliance on imports and promote Make in India, domestic manufacturers are expanding their capacity to produce high-durability undercarriage components that meet international performance standards. This not only improves cost competitiveness, but it also opens up new export opportunities to neighboring South Asian and African countries.

India's diverse and often rugged terrain, ranging from the Himalayan foothills to deserts and mining belts, requires undercarriage systems that are not only strong but also adaptable to extreme operational conditions. As a result, OEMs and suppliers are increasingly focusing on reinforced rubber tracks and sealed track link assemblies to ensure longer service life and lower maintenance requirements.

Category-wise Analysis

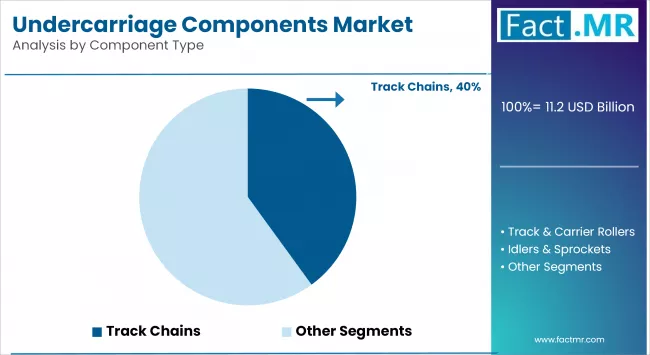

Track and Carrier to Exhibit Leading by Component Type

Track and Carrier Rollers are essential components of tracked machinery undercarriages. Track rollers support the equipment weight on the lower frame, which aligns the track chain. To prevent slippage and wear, top carrier rollers guide the track back to the sprocket. Both rollers are designed for use in heavy-load and harsh-environment applications in the construction and mining industries. Their quality affects machine efficiency, ride smoothness, and the longevity of the undercarriage system.

Track Chains support the undercarriage and keep tracked vehicles moving. Interconnected chains loop around rollers, sprockets, and idlers to transfer load and provide traction. Track chains made of high-strength, wear-resistant steel can withstand constant stress and abrasion. High-performance applications, such as excavators, bulldozers, and forestry machinery, require precision to ensure smooth motion and minimize mechanical failure.

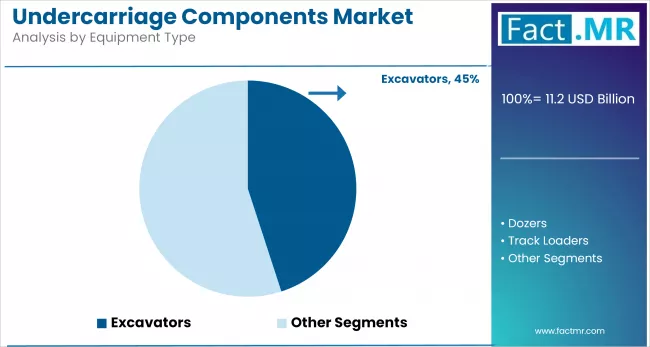

Excavators to Exhibit Leading by Equipment Type

Excavators are a major undercarriage component of Equipment. Strong undercarriage systems enable these machines to dig, lift, and grade effectively in construction, mining, and infrastructure projects. The undercarriage must be able to withstand frequent directional changes, prolonged periods of operation, and challenging terrain. Track chains, rollers, and sprockets help maintain stability and manoeuvrability. As infrastructure projects grow in emerging markets, excavators need heavy-duty and durable undercarriage parts.

Dozers, known for their powerful pushing abilities, put enormous strain on undercarriage systems due to their constant contact with abrasive and rocky surfaces. Reinforced track shoes, heavy-duty rollers, and durable idlers are critical for withstanding the extreme loads and impacts that dozers face. These machines are widely used in mining, land clearing, and road construction, where dependability and minimal downtime are critical.

Construction to Exhibit Leading by End-Use

The construction industry is the largest consumer of undercarriage systems, driven by the global demand for infrastructure development. The need for efficient and long-lasting machinery in construction activities is critical, so undercarriage systems are essential for excavators, bulldozers, and other heavy equipment. The increase in residential, commercial, and industrial construction projects is driving up demand for advanced undercarriage systems that provide improved performance and lower operating costs.

The mining industry is a significant application for undercarriage systems, as it relies on these components to operate heavy machinery in harsh environments. The demand for minerals and metals is driving global mining activity, necessitating robust and long-lasting undercarriage systems that can withstand extreme temperatures. Advances in undercarriage technology, including the development of wear-resistant materials and the integration of IoT for predictive maintenance, are enhancing the operational efficiency and longevity of mining equipment. These advancements are crucial for reducing downtime and improving productivity in mining operations.

OEM to Exhibit Leading by Sales Channel

The OEM (Original Equipment Manufacturer) segment holds the largest market share due to steady demand from manufacturers and first-time buyers. OEM sales are driven by product reliability, warranty coverage, and factory-fitted compatibility. These sales channels typically serve professional users and fleet buyers requiring high-quality, new equipment. OEMs also benefit from strong dealer networks and brand trust. As demand for advanced, integrated stump grinders grows, OEM channels continue to dominate.

The aftermarket segment is witnessing the fastest growth, fueled by aging equipment and the need for replacement parts. It supports users looking to upgrade or maintain existing stump grinders cost-effectively. Customization, blade replacements, and performance enhancements are key drivers. With growing awareness of maintenance and operational cost savings, more users turn to aftermarket suppliers. This segment is also expanding due to the presence of online platforms offering easier access to parts and services.

OEM Undercarriage Components Stand Out as a Key Segment

OEM undercarriage components are supplied directly by equipment manufacturers or authorized vendors. These components are designed specifically for Caterpillar, Komatsu, and Volvo machinery. For heavy-duty equipment used in harsh environments, OEM parts provide a precise fit, durability, and compliance with design specifications. Mining and construction customers choose OEM components to preserve equipment warranties, enhance performance, and ensure reliability.

Independent manufacturers produce aftermarket undercarriage components that fit and function similarly to OEM parts but are usually less expensive. This segment is highly competitive and rapidly growing due to cost-effectiveness, availability, and broader distribution. Aftermarket options are especially popular among equipment owners managing older fleets or operating in cost-sensitive markets. Many aftermarket suppliers now offer high-quality, durable alternatives for a wide range of machines across various industries.

Competitive Analysis

The global undercarriage components market is becoming increasingly competitive, with a mix of OEMs and aftermarket suppliers offering both standard and custom solutions. Durability, cost, and downtime all influence customer purchases. Material advances, such as wear-resistant alloys and reinforced rubber compounds, have extended the life of undercarriage systems and reduced the total cost of ownership. Companies also invest in automation and precision manufacturing to improve tolerances and product consistency.

In the construction, mining, forestry, and agriculture industries, the undercarriage components market is crucial to the performance of heavy-duty equipment. Market components include track chains, rollers, idlers, sprockets, track shoes, and rubber tracks. These parts ensure machine stability, traction, and load distribution, making them essential for operational efficiency in rough terrain and high-wear environments.

Manufacturers are localizing production to reduce lead times and costs due to rising construction demand in Asia-Pacific and the Middle East & Africa. The need for durable undercarriage parts is increased by the development of nations' equipment modernization and government-led infrastructure projects.

While fleet upgrades, emissions compliance, and lifecycle management drive demand in North America and Europe, customers are increasingly opting for remanufactured or modular undercarriage kits to minimze downtime.

Key players in the undercarriage components industry include Caterpillar Inc., Continental AG, Berco S.p.A. (Thyssenkrupp), Deere & Company, DIGBITS Ltd, Dozco Pvt. Ltd, Gemmo Group Srl, Hitachi Construction Machinery Co., Ltd., Hoe Leong Corporation Ltd., Komatsu Limited, MST, Renomag, ThyssenKrupp AG, Titan International, Inc., Topy Industries Ltd., TRIDENT INTERNATIONAL P LTD., TVH Parts Holding NV, USCO SpA, Verhoeven Group, and other players.

Recent Development

- In January 2025, KAGE Innovation introduced its Under-Hitch Tractor Undercarriage System, which features front 3-point hitch technology. This adjustable system improves compatibility with various tractor models, increasing their versatility for applications like snow removal, landscaping, and agriculture.

- In March 2024, Caterpillar, Inc., a leading manufacturer of construction and mining equipment, announced a USD 500 million investment to significantly increase its production capacity for undercarriage components. This strategic expansion aims to address the rising global demand for heavy machinery, particularly in the construction and mining industries, as well as emerging markets.

Segmentation of Undercarriage Components Market

-

By Component Type :

- Track and Carrier Rollers

- Track Chains

- Idlers & Sprocket

- Equalizer Bars

- Track Shoe/Rubber Tracks

- Track Adjuster & Recoil

- Link Assemblies

- Other Components (Bogies, Track guide, pins & busing, etc)

-

By Equipment Type :

- Excavator

- Track Loader

- Dozers

- Multi Terrain Loaders

- Crawler Cranes

- Asphalt Pavers

- Others

-

By End-Use :

- Construction

- Mining

- Agriculture & Forestry

- Landscape & Maintenance

- Other

-

By Sales Channel :

- OEM

- Aftermarket

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the Global Undercarriage Components Market Size in 2025?

The Undercarriage Components market is valued at USD 7.5 billion in 2025.

Who are the Major Players Operating in the Undercarriage Components Market?

Prominent players in the market include Dozco Pvt. Ltd, Gemmo Group Srl, Hitachi Construction Machinery Co., Ltd., Hoe Leong Corporation Ltd., and Komatsu Limited.

What is the Estimated Valuation of the Undercarriage Components Market by 2035?

The market is expected to reach a valuation of USD 11.2 billion by 2035.

What Value CAGR Did the Undercarriage Components Market Exhibit During the Last Five Years?

The historic growth rate of the undercarriage components market was 3.3% from 2020-2024.

Author:

Shubham Patidar

Editor:

Naved Ahmed