Paper Trays Market Outlook (2025 to 2035)

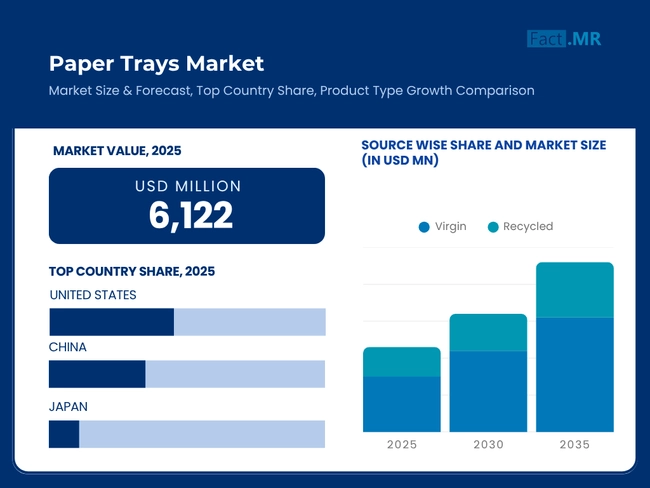

The global paper trays market is expected to reach USD 10,758 million by 2035, up from USD 5,840 million in 2024. During the forecast period 2025 to 2035, the industry is projected to register at a CAGR of 5.8%.

The increasing interest in sustainable and biodegradable packaging solutions is driving the adoption of paper trays in the foodservice and retail markets. Tough environmental measures and a consumer preference for environment-friendly options over plastic are strengthening the product’s adoption.

What are the drivers of paper trays market?

The demand for environmentally friendly materials is the most prominent commercial force in the paper tray market. As more people around the world become aware of the effects of plastic pollution and regulations against single-use plastics, industries are developing alternatives to their current methods of packaging materials, such as paper trays. The EU, North America, and some parts of Asia are actively promoting sustainable packaging, which is boosting demand in the foodservice, healthcare, and consumer goods sectors.

The other major trend is the rise of food delivery and takeaways, particularly following the pandemic. The safe, hygienic, and eco-friendly food packaging using paper trays is a desirable option for restaurants and cloud kitchens. In addition, the growing number of retail and supermarket openings has augmented and intensified the demand for effective and appealing food-grade trays.

Advances in technologies using molded fiber and pulp are also contributing to market expansion, enabling more powerful, customizable, and recyclable designs. Manufacturers are aligning their objectives with green branding, which has further catalyzed investment in paper tray manufacturing and development.

What are the regional trends of paper trays market?

The paper trays market is still dominated by North America and Europe, which are known for having strict environmental regulations and a well-developed consumer base that prefers sustainable products. In Europe, laws such as the EU Single-Use Plastics Directive have driven the adoption of durable, reusable trays across hospitals, retail, and hospitality sectors. Countries like France, Germany, and those in Scandinavia have been at the forefront of this shift, particularly in organic food retail and catering services, where sustainability mandates are more actively enforced.

In North America, the growing environmental awareness and increasing demand for compostable packaging in the USA are driving market growth in the region. The shift towards eliminating paper is evident within major QSR chains that need to pursue corporate sustainability objectives.

The Asia-Pacific region is poised to be the fastest developing market, especially in China, India, and the ASEAN countries. Urbanization and the increasing demand of the middle class for conveniently packaged food, as well as government initiatives promoting plastic awareness, are motivating local manufacturers to boost production of paper trays.

In the meantime, Latin America and the Middle East are slowly implementing paper trays due to retail modernization and campaigns that inform people about the need to develop sustainable consumption habits.

What are the challenges and restraining factors of paper trays market?

The cost competitiveness is one of the main challenges of the market. Although disposable paper carrying trays are eco-friendly, they are more expensive to produce and to obtain raw materials. Virgin or recycled fibre paper pulp is used, and raw production is water-intensive, thus requiring extra coating to make them water resistant.

Durability issues also hamper wider adoption. In applications that contain high moisture or high levels of fat content, paper trays would perform poorly unless barriers are applied, which may make the recycling process harder or more expensive. The end-of-life disposal is also complicated by the fact that in most parts, infrastructure to conduct advanced composting is not very common and thus acts as a deterrent to consumers.

Variation in the supply chain of raw materials like bamboo, sugarcane bagasse and recycled fibers may have impact on the consistency and lead time of manufacturing. The technological or economic constraints of changing to paper trays may be imposed on the small and mid-sized companies, particularly in those markets where prices play an essential role in the purchasing decisions of the consumers thus the dominance of conventional plastic packaging remains the norm.

Country-Wise Outlook

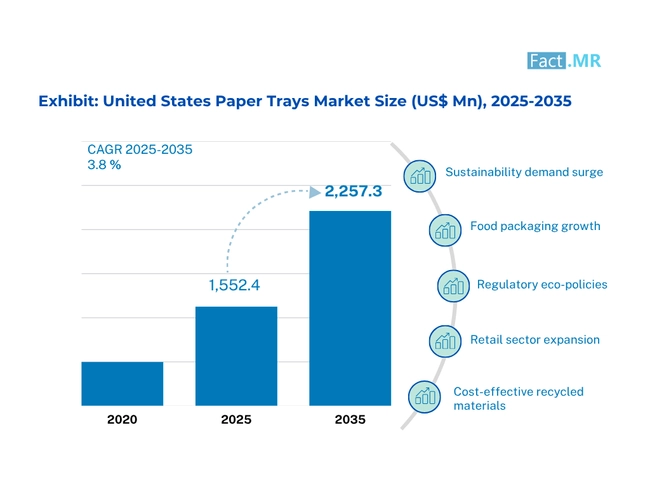

The United States drives growth through retail shifts and eco-mandates

The United States accounts for the largest share of the global paper trays market. With the statewide implementation of ban on plastic, consumer demand growth to use sustainably packaged products, and retail and foodservice chains have increased the adoption. Demand for compostable and recyclable trays is rushing ahead within QSRs, school meal schemes and institutional catering.

New molded fiber technology, water-based coatings, and digitally printable surface technologies are increasing utility and attractiveness. State laws, such as the Plastic Waste Reduction Act and bans on using polystyrene packages in specific states, have helped companies shift towards using paper-based trays. National automation and supply chains connections also reinforce domestic production.

Germany anchors the European market with circular economy leadership

Germany is a key market in the development of paper trays in Europe, supported by the Packaging Act, strict recycling standards, and rapid compliance with the EU Single-Use Plastics Directive. The demand is strong in the fresh produce, meat, and bakery categories.

The producers locally are investing in fiber trays of high-barrier and compostable coatings that satisfy the functional and environmental requirements. The wide usages of lifecycle assessment instruments, traceable supply chains, and recyclability labeling have been introduced. Germany, as a regulatory and technological role model of the industry, is characterized by a mature system infrastructure and environmental policy synergy.

India scales rapidly on the back of plastic bans and urban demand

The paper trays industry is booming with high growth rates in India due to the ban of plastics in the country, an increased food delivery needs in urban centres and the cheap manufacturing. Sugarcane bagasse, wheat bran, and bamboo are agro-waste materials that are used to manufacture trays used in catering, street food and institutional use.

Local manufacturing ecosystems are being encouraged through government initiatives, such as the Swachh Bharat Abhiyan and EPR frameworks. There are also increasing semi-automated pulp molding mills in the major cities, while the rural areas still use the manual method. Policy push, mass-scale demand, and affordability in India are making it a hub of volume-oriented manufacture of paper trays.

Category-Wise Analysis

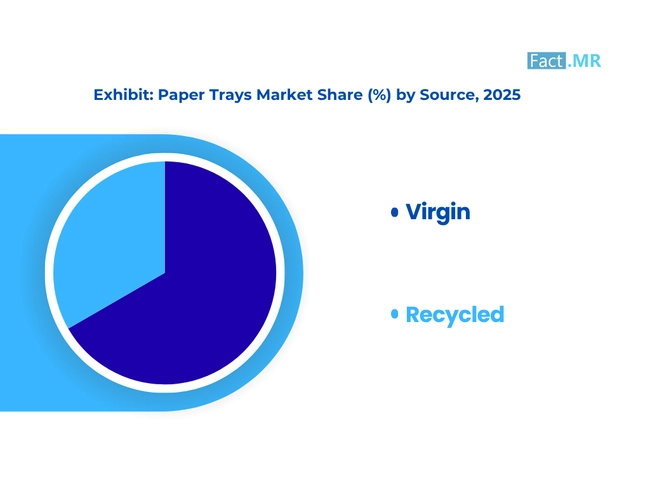

Virgin fiber sourcing ensures strength and hygiene for premium paper tray applications

The use of virgin fiber-based paper trays is very important in areas where product integrity and hygiene are highly regarded. Virgin pulp, compared to recycled fibers, has excellent mechanical strength and purity, which are desired in food-grade and retail packaging.

Virgin-sourced trays, in particular, guarantee a low prospect of contamination in retail sectors, adherence to food safety policies (such as those of the FDA or EFSA), and are able to support increased loads or withstand exposure to moisture. As sustainable forestry procurement standards, such as FSC and PEFC, become increasingly popular, even brands involved in the use of virgin pulps will need to consider more traceable and eco-friendly sourcing solutions to comply with their environmental objectives.

Corrugated boards deliver durable, lightweight solutions for retail packaging needs

Sandwiched fluted paper, incorporated between two linerboards, produces the corrugated boards that are ideal for use in retail-oriented paper trays due to their lightweight nature, strength, and recyclability. This material makes up provides a good cushioning and supporting strength, which in turn makes it flexible to carry and display different consumer products.

Corrugated trays can also be printed at high quality, better communicating the brand and the quality of the stores where they are offered. Improvements in water-resistant coatings and more biodegradable adhesives are also extending their application to semi-moist or refrigerated retail products.

Retail industry drives customization and branding in paper tray demand

The retail sector remains a dominant force as the primary end-use sector for paper trays, with e-commerce packaging, in-store product displays, and the need for alternatives to plastic being the main driving factors. Paper trays provide retailers with the opportunity to create brand-specific, recyclable, and biodegradable packaging formats in various shapes and sizes.

Various product categories, such as bakery goods, electronics, apparel, and cosmetics, are visual, and sustainability is a key factor in customer purchase decisions. The adoption of paper trays has been further boosted by regional legislation that prohibits or restricts the use of single-use plastics. The North American and European paper tray markets have been booming, while the APAC retail markets are experiencing growth driven by rising middle-class consumption and retail expansion.

Competitive Analysis

The paper trays market is characterized by strong competition, which has been influenced by sustainability trends, materials technology, and changes in regulations, and investment. Market players are focusing on creating cost-efficient, biodegradable, and recyclable paper tray products to reduce dependence on single-use plastics.

Besides, companies compete in the technology of materials, more specifically in sectors such as molded fiber and pulp-based innovations, where good performance, moisture resistance, and heat tolerance become the equipment's critical differentiators.

Decisions of business owners, such as mergers, acquisitions, and regional expansions, are frequently seen, with companies allocating funds to automation and manufacturing processes, which lead to improvement of production efficiency and a decrease in the carbon footprint.

A brand is set apart from the rest by certain characteristics, for instance, a certified mark (such as FSC or compostability labels), or by the ability to adapt the trays for different uses, like food packaging, catering, or fresh produce. While large players benefit from scale and distribution networks, smaller firms often leverage niche positioning in premium or local eco-packaging segments. The changing regulatory landscape across geographies further exacerbates competition, thus pushing companies to adhere to strict packaging regulations while remaining profitable.

Key players in the paper trays industry include Mondi Group plc, Huhtamaki Oyj, International Paper, BillerudKorsnäs, UFP Technologies, Inc., CS Packaging, Inc., Stora Enso, Novolex, Orcon Industries, Athena Superpack Private Limited, Henry Molded Products, Inc., and other notable companies.

Recent Development

- In May 2025, Marks & Spencer introduced a recyclable paper fibre tray for its Fiery Chicken Tikka Masala ready meal. This FSC-certified tray is both oven- and microwave-safe, providing consumers with convenience while reducing plastic waste. The innovation aligns with M&S's sustainability goals.

- In October 2024, Yangi unveiled a dry-formed fibre-based food tray designed to replace conventional plastic trays. Made from 100% renewable FSC fibres, the tray is recyclable in existing paper streams and suitable for ready meals, meat, and takeaway options.

Fact.MR has provided detailed information about the price points of key manufacturers in the paper trays market, positioned across regions, including sales growth, production capacity, and speculative technological expansion, in the recently published report.

Methodology and Industry Tracking Approach

The global paper trays market research by Fact.MR in 2025 involved 7,600 participants across 26 countries. The study made sure that there were at least 200 qualified respondents in each national market. The majority of respondents (~60%) represented end-use industries and vendors like food packaging companies, fresh produce exporters, and retail logistics providers.

The data were collected over a one-year timeframe, i.e., from June 2024 to May 2025. The research was primarily intended to identify the key shifts in procurement trends, material cost pressures, and compliance risks related to biodegradable and compostable packaging alternatives.

The exploration has been corroborated and supported by over 190 diverse information sources, including scientific publications on the topic of molded fiber packaging, technology patents archives, regional environmental packaging mandates, and financial records from packaging enterprises.

For several years up to 2018, Fact.MR has been persistently following the development of the molded fiber and paper-based trays industry, as well as changes in regulatory norms, the sustainability pledges of retailers, and the cost-to-performance benchmarks of fiber packaging.

Segmentation of Paper Trays Market

-

By Source :

- Virgin

- Recycled

-

By Material Type :

- Corrugated Boards

- Boxboards/Cartons

- Molded Pulp

-

By End-Use :

- Retail Industry

- Food & Beverage Industry

- Personal Care & Cosmetics Industry

- Healthcare Industry

- Consumer Durables and Electronics Industry

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What was the global paper trays market size reported by Fact.MR for 2025?

The Global Paper Trays Market was valued at USD 6,122 Million in 2025.

Who are the major players operating in the paper trays market?

Prominent players in the market Mondi Group plc, Huhtamaki Oyj, International Paper, BillerudKorsnäs, UFP Technologies, Inc., CS Packaging, Inc., Stora Enso, Novolex, Orcon Industries, Athena Superpack Private Limited, and Henry Molded Products, Inc.

What is the Estimated Valuation of the paper trays market in 2035?

The market is expected to reach a valuation of USD 10,758 Million in 2035.

What Value CAGR did the paper trays market exhibit over the last five years?

The historic growth rate of the Paper Trays Market was 4.6% from 2020 to 2024.

Author:

Ayush Raj

Editor:

Anushree Karale