Pressure Sensitive Adhesives Market Outlook (2025 to 2035)

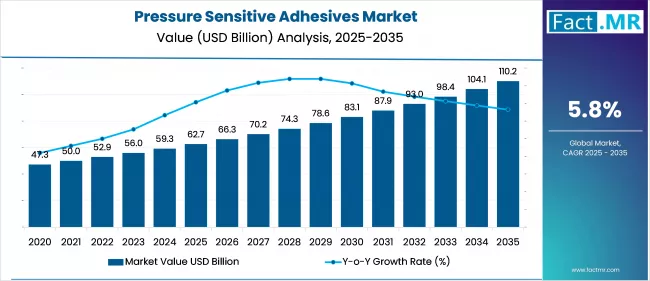

The global pressure-sensitive adhesives market is projected to increase from USD 62.7 billion in 2025 to USD 110.2 billion by 2035, with a CAGR of 5.8%, driven by rising demand from automotive and electronics industries for lightweight, high-performance bonding solutions. The surge in e-commerce and the growing need for sustainable packaging is driving the use of eco-friendly pressure-sensitive adhesives.

What are the Drivers of Pressure Sensitive Adhesives Market?

The growth of the pressure-sensitive adhesives (PSA) market is driven by increasing demand across key end-use industries, including automotive, packaging, electronics, and healthcare. One of the major growth drivers is the increasing use of pressure-sensitive adhesives in the automotive sector, where they provide lightweight bonding solutions that improve fuel efficiency and reduce vehicle weight.

With the rapid adoption of electric vehicles (EVs) and hybrid cars, the demand for adhesives in battery components, wire harnesses, and interior assemblies is growing rapidly. Moreover, pressure-sensitive adhesives play a vital role in reducing noise and vibrations in vehicles, enhancing overall ride quality.

Another key factor contributing to market expansion is the surge in e-commerce and retail packaging. With the global shift toward online shopping, pressure-sensitive adhesives are increasingly used in labels, tapes, and packaging seals that offer tamper resistance and improved logistics tracking.

As packaging companies seek eco-friendly and cost-effective solutions, pressure-sensitive adhesives offer significant advantages due to their ease of use, strong adhesion, and compatibility with a variety of substrates. The shift toward sustainable packaging, particularly in the food, personal care, and consumer goods sectors, is also boosting demand for recyclable and bio-based pressure-sensitive adhesive formulations.

The electronics industry is also driving significant growth for the pressure sensitive adhesives market. As electronic devices become smaller, thinner, and more complex, the need for high-performance adhesives that can bond delicate components without adding bulk has increased. PSA are now integral to the assembly of smartphones, tablets, laptops, and wearable devices, where they provide shock absorption, insulation, and component protection.

Moreover, technological innovations such as UV-cured and hot-melt acrylic adhesives have enhanced performance in high-temperature and moisture-sensitive environments, making them ideal for next-gen consumer and industrial electronics.

The healthcare and medical sectors are creating new avenues for pressure-sensitive adhesives applications. The growing use of medical tapes, wound dressings, and transdermal patches has increased demand for skin-friendly, breathable, and hypoallergenic adhesives.

The push for environmentally sustainable adhesives, due to stringent government regulations and rising consumer awareness, is leading to more innovation in low-VOC, solvent-free, and renewable material-based pressure sensitive adhesives. These multifaceted drivers collectively support a positive outlook for the pressure-sensitive adhesives market in the coming years.

What are the Regional Trends of Pressure Sensitive Adhesives Market?

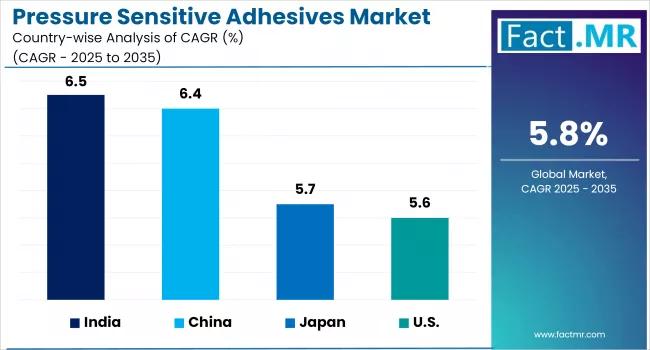

The Asia Pacific region dominates the global market in terms of both production and consumption, driven by rapid industrialization, urbanization, and growth across various end-use industries, including packaging, automotive, and electronics.

Countries like China, India, Japan, and South Korea are major hubs for consumer electronics and automobile manufacturing, both of which are high-demand sectors for pressure-sensitive adhesives. The region also benefits from a cost-effective labor force and the availability of raw materials, which further enhances its market competitiveness.

Advanced technologies, a well-established automotive industry, and growing demand for eco-friendly and high-performance adhesive solutions support the growth of North America's pressure-sensitive adhesives market.

The U.S. leads the region’s market due to its strong industrial base, high packaging standards, and increased adoption of sustainable and recyclable materials. Moreover, regulatory pressures from organizations like the Environmental Protection Agency (EPA) are pushing manufacturers toward developing low-VOC and bio-based pressure-sensitive adhesives, especially in packaging and healthcare applications.

The European region emphasizes sustainability and environmental compliance, leading to the widespread adoption of water-based and hot-melt pressure-sensitive adhesive technologies.

European manufacturers are also heavily investing in R&D to develop recyclable, solvent-free adhesives, aligning with the EU’s Green Deal and circular economy goals. The packaging industry, particularly for food and beverages, and the expanding electric vehicle market are central to pressure sensitive adhesives demand in the region.

The Middle East region is witnessing emerging demand in construction, transportation, and flexible packaging, particularly in countries with rapidly growing urban populations. However, growth in these regions is somewhat limited by higher import dependence and a less developed manufacturing base, although rising investments and trade partnerships are expected to change that in the near future.

What are the Challenges and Restraining Factors of Pressure Sensitive Adhesives Market?

One of the primary restraints on the growth of the pressure-sensitive adhesives market is the volatility of raw material prices, particularly those derived from petroleum-based inputs such as acrylics, rubber, and resins. Fluctuating crude oil prices directly impact the cost structure of pressure-sensitive adhesives manufacturing, leading to uncertainties in pricing and profitability for producers. This poses a significant challenge, especially for small and mid-sized manufacturers operating with narrow margins.

Another major restraint is the environmental and regulatory pressure associated with solvent-based pressure-sensitive adhesives, which emit volatile organic compounds (VOCs) and contribute to air pollution.

Governments across North America and Europe are enforcing stringent environmental norms to limit VOC emissions, which increases the cost of compliance and restricts the use of certain adhesive formulations. While water-based and hot-melt adhesives offer sustainable alternatives, transitioning to these technologies involves high capital investments in R&D and production equipment, which may deter some manufacturers.

The market faces technical challenges related to adhesion performance and substrate compatibility. While pressure-sensitive adhesives are versatile, not all types are suitable for bonding to low-energy surfaces, high-temperature environments, or applications requiring repositionability.

This limits their use in certain industrial applications where structural adhesives or mechanical fasteners may be more reliable. In high-stress or outdoor environments, pressure-sensitive adhesives may degrade more quickly than expected due to UV exposure, moisture, or thermal cycling, which can impact product durability.

Country-Wise Outlook

U.S. Pressure Sensitive Adhesives Market sees Growth Driven by Increasing Adoption of Pressure Sensitive Adhesives

The U.S. pressure-sensitive adhesives (PSA) market is experiencing growth driven by the increasing adoption of pressure-sensitive adhesives in key industries, including packaging, healthcare, construction, and the automotive sector. The market benefits from the United States' highly developed manufacturing infrastructure, rapid innovation in adhesive technologies, and rising consumer demand for more efficient, sustainable, and versatile adhesive products.

Pressure-sensitive adhesives are widely used in the U.S. packaging sector for labeling, tamper-evident sealing, and flexible packaging, particularly in the food, beverage, and personal care segments, where shelf appeal and product integrity are crucial.

The healthcare and medical sector is a significant contributor to the pressure-sensitive adhesives market in the U.S., driven by the growing elderly population, rising rates of chronic illnesses, and an increasing preference for home healthcare. Pressure-sensitive adhesives are essential in the production of medical tapes, wound care dressings, diagnostic electrodes, and transdermal drug delivery systems.

U.S. manufacturers are focusing heavily on hypoallergenic, breathable, and skin-friendly adhesive solutions, with an emphasis on patient comfort and regulatory compliance.

-2025-to-2035.webp)

The automotive and aerospace industries in the U.S. are integrating pressure-sensitive adhesives into various applications to support the growing trend of vehicle lightweighting and assembly efficiency. Adhesives are replacing mechanical fasteners to reduce weight and improve fuel efficiency in both traditional and electric vehicles.

With the expansion of the electric vehicle (EV) market, pressure-sensitive adhesives are being increasingly used in battery assembly, thermal insulation, wire harnessing, and vibration dampening. Aerospace manufacturers also rely on pressure-sensitive adhesives for bonding lightweight components that require high-performance, temperature-resistant, and low-outgassing materials.

The push toward sustainable and low-VOC adhesives is reshaping the U.S. pressure-sensitive adhesives landscape. Regulatory frameworks such as those enforced by the Environmental Protection Agency (EPA) are encouraging the use of water-based, hot-melt, and bio-based adhesives. This has led to a wave of innovations by domestic producers focused on environmentally friendly formulations.

Moreover, U.S. infrastructure development, driven by substantial federal investments, is boosting the use of pressure-sensitive adhesives in building materials, HVAC systems, flooring, and insulation, reinforcing the market’s long-term growth trajectory.

China witnesses Rapid Market Growth Backed by Growing Adoption of Sustainable, Bio-based Adhesives

The growth of pressure sensitive adhesives market in China is driven by surging packaging demand and increased use of bio-based adhesives. Sustainable trends in China’s adhesive industry are gaining momentum. Environmental concerns are encouraging the development and adoption of bio-based, low-VOC pressure sensitive adhesives, produced using materials like soy and vegetable oils. This shift supports regulatory compliance and aligns with global sustainability goals.

The dominance of international adhesive manufacturers in China has prompted local players to intensify their R&D efforts and expand their product offerings. This competitive climate is enhancing product innovation and quality, further solidifying China’s leadership in the pressure-sensitive adhesives market.

China’s industrial and manufacturing powerhouse, particularly in electronics and automotive assembly, also underpins demand for pressure-sensitive adhesives. PSA solutions are vital in everything from flexible electronics and PCB bonding to EV battery systems and NVH (noise, vibration, harshness) reduction.

Japan sees the Manufacturing Sector Fuels Demand for Pressure Sensitive Adhesives

Japan's pressure-sensitive adhesives market is closely tied to its high-tech and manufacturing sectors, particularly electronics and medical devices. Key players, such as Nitto Denko, Toyochem (a division of Toyo Ink), and Lintec, are driving innovation, particularly in acrylic adhesive technologies designed for healthcare, including Toyochem’s Oribain line for medical applications. These advancements align with Japan’s reputation for precision engineering and stringent quality standards.

Japan’s mature industrial economy and strong emphasis on sophisticated applications (medical, electronics, automotive) suggest market growth in the country. Japan differentiates itself by investing heavily in R&D and sustainable adhesive technology.

Manufacturers are adopting greener, low-VOC, water- and hot-melt systems to comply with global environmental standards. Japan’s competitive pressure sensitive adhesives landscape, dominated by both global giants and domestically strong firms, fosters rapid innovation cycles, ensuring that the market continues to grow not only in scale but also in technical sophistication and sustainability.

Category-wise Analysis

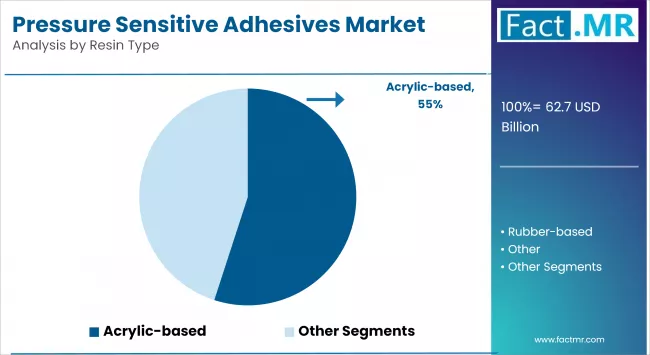

Acrylic-Based to Exhibit Leading by Resin Type

The acrylic-based segment holds the largest share of the global pressure-sensitive adhesives market. Acrylic-based pressure-sensitive adhesives are widely favored for their excellent UV resistance, aging stability, clarity, and adhesion to a wide range of substrates, including plastics, metals, and glass. These adhesives are ideal for outdoor applications, electrical & electronics, automotive trim attachment, and labels where durability and long-term bonding performance are critical. Moreover, their compatibility with water-based and solvent-free systems supports sustainability goals, aligning with regulatory trends in North America and Europe, further strengthening their market dominance.

The fastest growing segment is the rubber-based pressure-sensitive adhesives segment, primarily driven by increasing demand in packaging, hygiene products, and general-purpose tapes. Rubber-based pressure-sensitive adhesives offer superior tackiness, quick bonding capabilities, and cost-effectiveness, making them highly suitable for high-speed production lines in packaging and consumer goods industries. The growing use of these materials in medical tapes, diapers, and disposable hygiene products is also boosting their adoption, especially in developing regions such as the Asia Pacific and Latin America. The flexibility of rubber adhesives to adapt across a wide range of temperatures and substrates further enhances their popularity in dynamic industrial applications.

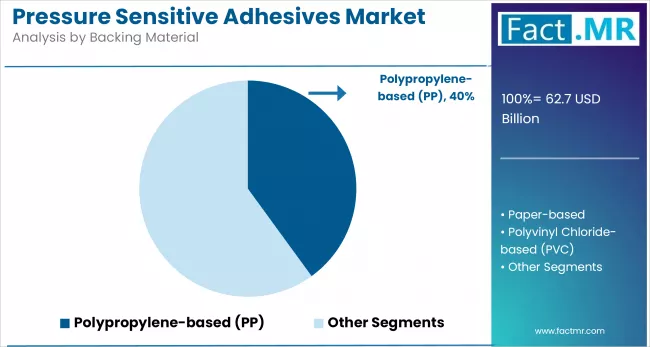

Paper-Based to Exhibit Leading by Backing Material

The polypropylene-based segment is the dominant backing material in the pressure-sensitive adhesives market, owing to its excellent mechanical strength, flexibility, moisture resistance, and low cost. Polypropylene (PP) films are widely used in various applications, including packaging tapes, labels, and surface protection films, due to their lightweight and durable properties.

The material’s compatibility with both water-based and hot-melt adhesives makes it ideal for automated packaging lines and high-speed labeling. Its growing usage in logistics, e-commerce, and FMCG packaging further reinforces its leadership, particularly as demand for tamper-evident and flexible packaging solutions increases globally.

The fastest-growing segment is paper-based backing material, driven by rising demand for sustainable, biodegradable, and recyclable adhesive products. Paper-based pressure-sensitive adhesives are being increasingly adopted in food labeling, masking tapes, and envelope sealing, particularly in regions with strong environmental regulations, such as Europe and North America. As consumers and industries shift toward eco-friendly packaging and labeling solutions, manufacturers are expanding their paper-based pressure sensitive adhesives offerings to align with circular economy goals. Advancements in coating technologies have enhanced the strength and water resistance of paper backings, making them more suitable for a broader range of end-use applications.

Tapes to Exhibit Leading by Application

The tapes segment is the dominant application segment in the global pressure-sensitive adhesives market. PSA tapes are widely used in packaging, automotive assembly, construction, electronics, and various industrial applications due to their ease of use, strong bonding capabilities, and compatibility with a wide range of surfaces.

The surge in e-commerce and logistics, especially in the Asia Pacific and North America, has significantly increased the demand for carton sealing tapes and protective packaging.

The fastest growing segment is medical adhesives, driven by the rising need for non-invasive, skin-friendly, and breathable adhesives in the healthcare sector. The increasing global demand for wound care dressings, surgical tapes, diagnostic electrodes, and transdermal drug delivery systems is accelerating the adoption of pressure-sensitive adhesives in medical applications.

The expansion of home healthcare, growth in the geriatric population, and rising prevalence of chronic illnesses are key factors contributing to this trend.

Competitive Analysis

The global pressure sensitive adhesives (PSA) market is becoming increasingly competitive, witha mix of both multinational giants and regional players. Key companies are focused on product innovation, sustainability, and strategic acquisitions to expand their global footprint and cater to evolving end-user demands.

3M and Henkel lead the market with a strong presence across multiple pressure-sensitive adhesives product lines, especially in tapes, medical adhesives, and industrial bonding applications. Both companies invest heavily in sustainable and bio-based adhesives, offering low-VOC and high-performance solutions aligned with global environmental regulations. Avery Dennison is particularly dominant in the labeling and packaging segment, offering advanced pressure-sensitive adhesives technologies for logistics, retail, and pharmaceuticals.

Arkema, through its Bostik brand, is making strategic moves into high-growth segments, such as hygiene adhesives and flexible packaging, supported by acquisitions and sustainability-focused product lines.

Competition is also intensifying through strategic mergers, acquisitions, and collaborations aimed at expanding product lines and geographical reach. For instance, Arkema’s acquisition of Ashland’s performance adhesives business and Henkel’s continued expansion of its adhesive technologies division signal a push toward market consolidation and technological advancement. Furthermore, as demand grows for pressure-sensitive adhesives in medical, EV, and smart packaging applications, companies are increasingly investing in functional and specialty adhesives to gain a competitive edge.

This ongoing innovation, paired with a rising focus on sustainability and customization, continues to reshape the global pressure sensitive adhesives competitive landscape.

Key players in the pressure-sensitive adhesives industry are 3M Company, Tesa SE, Nitto Denko Corporation, LINTEC Corporation, BASF SE, Lohmann GmbH & Co. KG, Exxon Mobil Corporation, and other players.

Recent Development

- In February 2024, Researchers at Virginia Tech developed a novel approach applying kirigami (paper cutting) designs to pressure-sensitive adhesive tapes. This method increases bond strength by up to 60% while retaining clean removability, offering a promising design innovation for construction, packaging, and industrial tapes.

(Source: https://www.adhesivesmag.com/publications/3/editions/1353.)

Segmentation of Pressure Sensitive Adhesives Market

-

By Resin Type :

- Acrylic-based

- Rubber-based

- Other

-

By Backing Material :

- Polypropylene-based

- Paper-based

- Polyvinyl Chloride-based

- Other

-

By Application :

- Tapes

- Labels

- Hygiene Adhesives

- Graphic Films

- Medical Adhesives

- Other Applications

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the Global Pressure Sensitive Adhesives Market size in 2025?

The pressure sensitive adhesives market is valued at USD 62.7 billion in 2025.

Who are the Major Players Operating in the Pressure Sensitive Adhesives Market?

Prominent players in the market include 3M Company, Tesa SE, Nitto Denko Corporation, LINTEC Corporation, and BASF SE.

What is the Estimated Valuation of the Pressure Sensitive Adhesives Market by 2035?

The market is expected to reach a valuation of USD 110.2 billion by 2035.

What Value CAGR Did the Pressure Sensitive Adhesives Market Exhibit Over the Last Five Years?

The growth rate of the pressure sensitive adhesives market is 5.8% from 2020-2024.

Author:

S.N. Jha

Editor:

Naved Ahmed