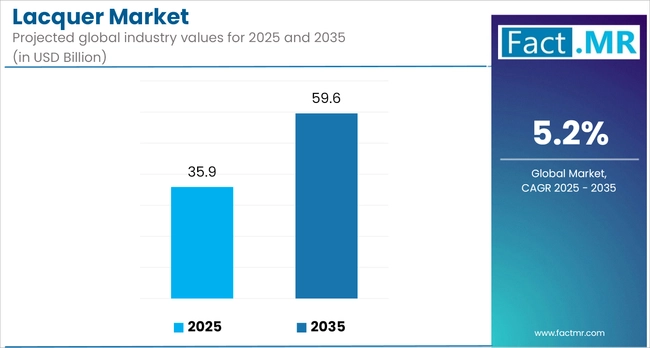

- Base Value(2025): 35.9 Bn

- Forecast Value (2035): 59.6 Bn

- CAGR (2035): %

Lacquer Market Outlook (2025 to 2035)

The global lacquer market is projected to increase from USD 35.9 billion in 2025 to USD 59.6 billion by 2035, with an annual growth rate of 5.20%. Growth is supported by rising demand in the construction, automotive, and furniture industries, where lacquer is valued for its durability and finish quality.

The Asia Pacific, led by China and India, dominates consumption due to its strong manufacturing output and robust infrastructure activity. Regulatory shifts in Europe and North America are accelerating the transition to low-VOC, water-based lacquers. Advances in resin technologies and application methods are further driving efficiency and product innovation.

What are the Drivers of the Lacquer Market?

The lacquer market is driven by strong demand from the construction, furniture, and automotive sectors. In construction and real estate, especially across Asia Pacific, lacquers are widely used for wood finishing and interior applications.

The global shift toward high-end furniture and interior design has also led to an increase in lacquer usage, due to its aesthetic and protective qualities. In the automotive industry, lacquers play a crucial role in providing durable and visually appealing finishes, with increasing vehicle production driving market growth.

Regulatory pressure in Europe and North America is accelerating the adoption of water-based, low-VOC formulations. Additionally, innovations in application technologies and growing consumer preference for premium, glossy finishes continue to fuel market expansion.

What are the Regional Trends of the Lacquer Market?

The lacquer market exhibits varied growth patterns across regions, shaped by industrial activity, regulatory frameworks, and consumer preferences.

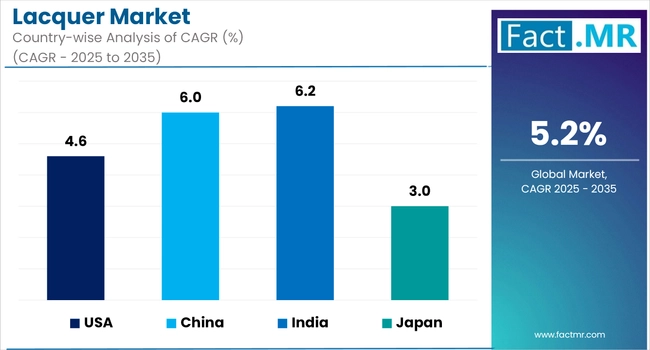

Asia Pacific remains the dominant region, accounting for the largest share of global lacquer consumption. Urbanization, infrastructure investments, and strong furniture and automotive manufacturing in China, India, and Southeast Asia continue to drive demand. China alone contributes over 40% of the global lacquer output, supported by an extensive manufacturing base and cost-effective production methods. India’s growing middle class and real estate boom are also fueling consumption for decorative and wood lacquers.

Europe is experiencing stable demand, with a clear shift toward sustainable, low-VOC, and water-based lacquer products. The region’s stringent environmental regulations, including REACH compliance, are influencing formulation changes and driving innovation among manufacturers. Germany, Italy, and Poland are key markets due to their strong furniture and automotive industries.

North America shows consistent demand, driven by residential remodeling, premium furniture sales, and regulatory-driven shifts toward eco-friendly coatings. The USA market is focusing on advanced application technologies and high-performance formulations, while Canada benefits from steady construction activity and domestic furniture production.

Latin America is seeing moderate growth, led by Brazil and Mexico. Infrastructure development, expansion of the housing sector, and growth in automotive assembly are supporting lacquer consumption, although economic fluctuations occasionally pose constraints.

The Middle East & Africa are emerging markets, with rising construction activity in the UAE, Saudi Arabia, and South Africa creating new opportunities. Demand is growing for durable, weather-resistant coatings that are suited to the region’s climate, particularly in architectural and wood applications.

What are the Challenges and Restraining Factors of the Lacquer Market?

The lacquer market faces structural and regulatory challenges that may limit its growth trajectory across regions.

One of the primary concerns is the tightening of environmental regulations. In regions such as the European Union and North America, policies targeting volatile organic compound (VOC) emissions have limited the use of traditional solvent-based lacquers. Compliance with frameworks such as REACH and the USA EPA Clean Air Act increases production costs and requires reformulation for smaller manufacturers lacking R&D capacity.

Raw material price volatility is another constraint. Lacquer production relies heavily on petrochemical derivatives, resins, and solvents, which are subject to global oil price fluctuations and supply chain disruptions. For example, during the COVID-19 pandemic and the Russia-Ukraine conflict, price spikes in raw inputs squeezed profit margins for manufacturers globally.

Technical limitations also persist. Despite the market shift toward water-based and low-VOC lacquers, these alternatives often lag in performance compared to traditional formulations, particularly in terms of drying time, surface hardness, and chemical resistance factors crucial for industrial and automotive applications.

In developing economies, limited awareness and inconsistent quality standards pose additional challenges. Informal manufacturing practices and a lack of regulatory oversight often lead to substandard products, which can erode end-user confidence.

Moreover, the capital-intensive nature of advanced application systems, such as automated spray booths and UV-curing technologies, can deter adoption among small- and mid-sized enterprises, especially in cost-sensitive markets.

Lastly, consumer demand for fast, customizable finishes puts pressure on producers to balance aesthetics, durability, and sustainability, often at higher operational costs.

Country-Wise Outlook

Evolving Dynamics in the USA Lacquer Market: Regulatory Shifts, Innovation, and Demand Trends

The USA lacquer market is experiencing steady growth, driven by robust demand from the construction, furniture, and automotive industries. Increased residential remodeling and commercial real estate development are fueling the need for high-performance wood and metal finishes. Furniture manufacturers are prioritizing premium coatings to enhance both durability and visual appeal, as consumer interest in interior aesthetics continues to rise.

Environmental regulations, especially under the USA EPA’s Clean Air Act, are reshaping the product landscape. Restrictions on solvent-based coatings are accelerating the adoption of water-based and low-VOC lacquer formulations. States like California have implemented stricter VOC limits, prompting a shift in both manufacturing and procurement practices.

Advancements in application technologies such as automated spray systems, UV-curable finishes, and fast-drying resins are improving operational efficiency and finish quality in automotive refinishing and industrial woodwork. At the same time, consumer preference is shifting toward safer, eco-conscious finishes, reinforcing the demand for sustainable alternatives.

China Witnesses Accelerated Growth in Lacquer Demand

China’s lacquer market is gaining momentum, driven by strong performance in the furniture, automotive, and consumer electronics sectors. Urbanization, increasing disposable income, and a surge in residential construction are fueling demand for high-quality wood coatings and interior finishes. The domestic furniture industry, a key application segment, continues to grow, driven by rising export volumes and a focus on premium, customizable designs.

In the automotive sector, lacquer coatings are widely used for both protective and aesthetic finishes. China's position as the world’s largest vehicle producer has supported consistent demand for fast-drying and high-gloss lacquers. Additionally, the rise of electric vehicles is prompting innovation in coating materials to enhance durability and surface performance.

Industrial lacquer production in China benefits from an integrated supply chain and cost-effective labor, enabling large-scale output and competitive pricing. At the same time, manufacturers are investing in environmentally compliant, low-VOC formulations in response to tightening domestic environmental standards. Government policies aimed at reducing air pollution have accelerated the shift toward water-based alternatives and restricted the use of solvent-heavy coatings.

As the market evolves, local producers face increasing pressure to balance environmental compliance with performance and cost efficiency. This has led to increased investment in R&D and the adoption of advanced application technologies, positioning China as both a leading producer and a key innovator in the global lacquer industry.

Japan Experiences Evolving Dynamics in Its Lacquer Market

Japan’s lacquer market reflects a balance between industrial innovation and cultural heritage. Rising demand from the automotive and infrastructure sectors continues to shape the market, supported by vehicle production and ongoing public investment in modernization and restoration projects. In parallel, the construction and home renovation segments are driving consistent need for high-performance wood and metal finishes.

Environmental regulations are playing a pivotal role in product development. Manufacturers are shifting toward low-VOC and water-based formulations to comply with Japan’s strict sustainability standards. This shift is accelerating R&D investment in coatings that combine durability, safety, and environmental compliance in architectural and industrial applications.

At the same time, Japan’s traditional lacquerware industry is experiencing a revival. Although the historical consumption of natural urushi lacquer has declined over recent decades, contemporary artisans are reimagining its use in modern design, from furniture to lifestyle products. Government initiatives and cultural preservation programs are supporting this trend, helping traditional techniques reach new audiences while sustaining the craftsmanship behind them.

The industrial segment is also advancing, with an increased focus on technologies such as nanocoatings and self-healing resins, for automotive refinishing and high-spec industrial applications. These developments reflect Japan’s broader push for coatings that deliver superior performance while aligning with regulatory and consumer expectations.

Category-wise Analysis

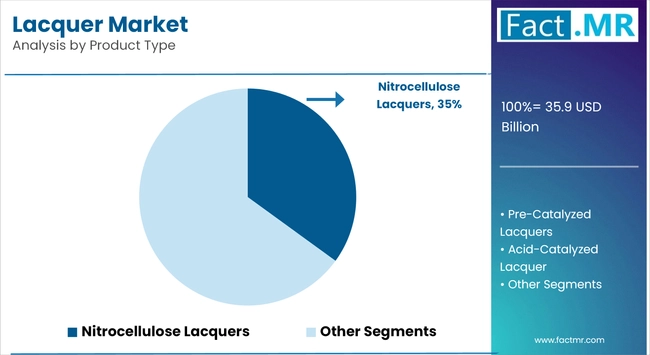

Nitrocellulose Lacquers to Exhibit Leading Share Among Product Types

Nitrocellulose lacquers are positioned to maintain a leading share in the lacquer market, owing to their fast-drying properties, ease of application, and affordability. Widely used across the furniture, automotive refinishing, and musical instrument industries, these lacquers offer a smooth, high-gloss finish that appeals to both manufacturers and end-users.

Their dominance is strong in furniture manufacturing, where production efficiency and aesthetic quality are critical. Small- and medium-scale woodworkers prefer nitrocellulose formulations for their quick turnaround times and compatibility with conventional spray systems. In automotive aftermarket services, these lacquers are favored for spot repairs and refinishing due to their drying and blending characteristics.

Emerging economies, including India, Vietnam, and Brazil, continue to rely on nitrocellulose-based products due to their low cost and widespread availability. Meanwhile, in mature markets like North America and Europe, demand persists in niche applications despite growing regulatory pressure to adopt lower-VOC alternatives.

Although water-based and polyurethane lacquers are gaining traction, especially in regulated markets, the performance, workability, and economic benefits of nitrocellulose lacquers ensure their continued relevance across multiple sectors. Manufacturers are also exploring hybrid formulations to enhance compliance without compromising key properties, helping this product category retain its strong market position.

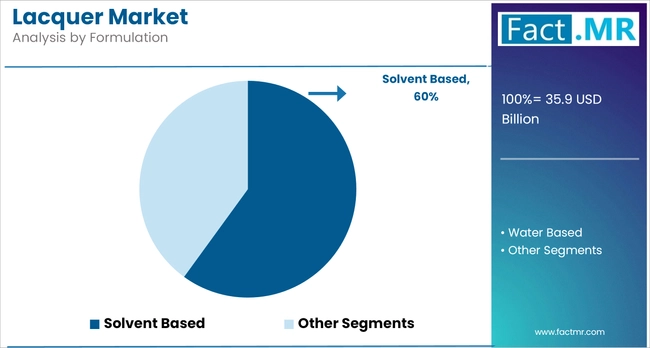

Solvent-Based to Exhibit Leading Share Among Formulation Types

Solvent-based lacquers continue to hold a dominant position in the market, driven by their superior performance characteristics, including rapid drying, high gloss, strong adhesion, and resistance to wear. These properties make them a preferred choice across a wide range of industries, including furniture manufacturing, automotive refinishing, metal fabrication, and electronics.

Their ease of application and compatibility with various substrates provide an advantage in high-volume production settings. In particular, solvent-based lacquers are widely used in woodworking operations where speed and finish quality are critical. In the automotive sector, they remain popular for refinishing and OEM applications due to their durability and efficient curing process.

Despite increasing regulatory scrutiny regarding VOC emissions, solvent-based formulations continue to dominate in regions where environmental policies are less restrictive, particularly in parts of the Asia Pacific, Latin America, and the Middle East. Manufacturers in these regions prioritize cost-efficiency and throughput, which solvent-based systems are well-suited to deliver.

Wood to Exhibit Leading Share Among Applications

Wood remains the dominant application segment in the lacquer market, supported by sustained demand across furniture, flooring, cabinetry, and architectural millwork. Lacquers are widely preferred for wood surfaces due to their ability to enhance grain visibility, provide a uniform finish, and offer moderate protection against moisture and abrasion.

The furniture industry is a key growth driver in Asia Pacific and Eastern Europe, where large-scale production and export-oriented manufacturing fuel high-volume lacquer use. In markets such as India, Vietnam, and Poland, lacquered wood furniture remains a popular choice, both domestically and internationally, driven by competitive pricing and a growing consumer preference for aesthetically pleasing and functional finishes.

Beyond residential use, lacquer coatings are also applied in commercial interiors, retail fixtures, and hospitality settings, where appearance, durability, and maintenance efficiency are key considerations.

Given wood’s widespread use across industries and geographies, along with the material’s compatibility with a broad range of lacquer formulations, it is expected to retain a leading share of the overall application landscape in the lacquer market.

Modern Trade to Exhibit Leading Share Among Distribution Channel

Modern trade is set to dominate lacquer distribution, driven by the growing presence of organized retail chains and home improvement stores. Retailers like Home Depot, Lowe’s, and B&Q offer a wide range of products, technical support, and greater accessibility, making them preferred channels for both professionals and DIY users.

In emerging markets, shifting consumer preferences toward structured retail and branded offerings are accelerating this trend. Additionally, the focus on eco-labeled and low-VOC products aligns with modern trade’s ability to meet evolving regulatory and consumer demands.

East Asia holds the Leading Share in the Lacquer Market

East Asia remains the largest contributor to the global lacquer market, driven by robust manufacturing activity, high construction output, and export-oriented industries in the furniture and automotive sectors. China leads regional demand due to its integrated supply chain, large-scale lacquer production, and consistent demand across various sectors. Japan and South Korea also contribute through advanced coatings technologies and high-quality applications in electronics, automotive, and industrial equipment.

The region benefits from cost-efficient raw material sourcing, skilled labor, and increasing investments in environmentally compliant formulations. With growing urbanization and infrastructure development, East Asia is expected to maintain its dominant position in the lacquer market.

Competitive Analysis

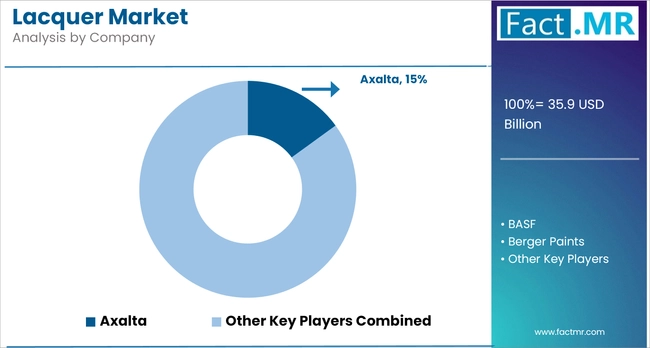

The global lacquer market is marked by intense competition, with both multinational corporations and regional players vying for market share. Leading companies, such as Akzo Nobel, PPG Industries, Sherwin-Williams, and Nippon Paint Holdings, maintain strong positions through extensive product portfolios, global distribution networks, and ongoing investments in sustainable technologies.

Firms like BASF Coatings and Axalta Coating Systems are focused on developing high-performance and low-VOC formulations to meet evolving regulatory standards and environmental expectations in North America and Europe. RPM International and Hempel A/S continue to expand their industrial coatings capabilities, targeting sectors such as automotive refinishing, marine, and infrastructure.

In Asia, companies such as Asian Paints, Berger Paints India, Carpoly Chemical, and Chugoku Marine Paints are leveraging local market expertise and cost-effective manufacturing to strengthen their presence, particularly in high-growth economies like China and India. These players are expanding their production capacity and retail reach to capitalize on the rising demand for furniture, construction, and decorative coatings.

Mid-sized firms such as Cloverdale Paint and Diamond Vogel are focusing on niche markets and customized solutions, catering to regional and application-specific needs.

Across the board, innovation, sustainability, and regional expansion remain core strategies, with companies investing in digital tools, automated application technologies, and R&D partnerships to enhance competitiveness and product differentiation.

Recent Development

- In 2024, Akzo Nobel launched RUBBOL WF 3350, a bio-based wood coating, and initiated collaborations with Arkema and Omya to incorporate circular raw materials into its product lines.

- In 2024, PPG Industries introduced Enviroluxe Plus, a powder coating line incorporating recycled plastics, aligning with the company’s circular economy goals.

Segmentation of the Lacquer Market

-

By Product Type :

- Nitrocellulose Lacquers

- Pre-Catalyzed Lacquers

- Acid-Catalyzed Lacquer

- Polyurethane Lacquers

- Radiation Curing-Lacquers

- Unsaturated Polyester Lacquers

- Other Product Types

-

By Formulation Type :

- Solvent Based

- Water Based

-

By Application :

- Wood

- Metal

- Plastics

- Leather and Textiles

- Others (paper, nail polish, etc.)

-

By Distribution Channel :

- Modern Trade

- Departmental Store

- Online Retailers

- Specialty Stores

- Direct Sales

- Other Sales Channel

-

By End Use Industry :

- Automotive

- Architectural

- Furniture

- Cosmetics

- Other End Users

-

By Region :

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- Middle East & Africa

- Frequently Asked Questions -

What is the Global Lacquer Market Size in 2025?

The lacquer market is valued at USD 35.9 billion in 2025.

Who are the Major Players Operating in the Lacquer Market?

Prominent players in the lacquer market include Axalta Coating, BASF Coatings, Berger Paints India, Carpoly Chemical, Chugoku Marine Paints, and others.

What is the Estimated Valuation of the Lacquer Market by 2035?

The lacquer market is expected to reach a valuation of USD 59.6 billion by 2035.

What Value CAGR Did the Lacquer Market Exhibit over the Last Five Years?

The historic growth rate of the lacquer market was 4.50% from 2020 to 2024.