Bonded Magnet Market Outlook (2025 to 2035)

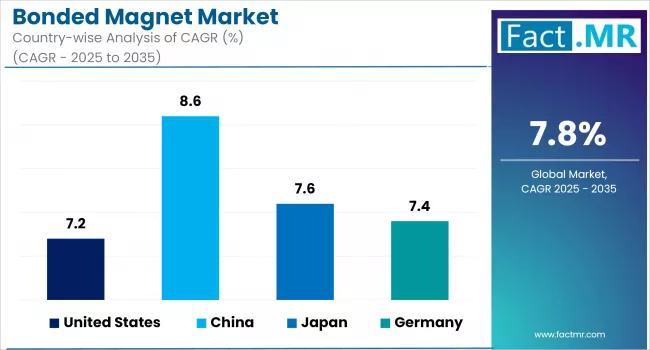

The global bonded magnet market is projected to grow from USD 6,524.9 million in 2025 to USD 13,828.1 million by 2035, with an annual growth rate of 7.8%, driven by increasing demand in the electric vehicle, industrial automation, and electronics sectors.

Lightweight, customizable, and compatible with high-precision applications, bonded magnets are steadily replacing conventional alternatives in compact motor and sensor designs. Further momentum is provided by innovations in injection molding and additive manufacturing, which allow scalable and cost-efficient production.

| Metric | Value |

|---|---|

| Industry Size (2025E) | USD 6,524.9 million |

| Industry Size (2035F) | USD 13,828.1 million |

| CAGR (2025 to 2035) | 7.8% |

What are the Drivers of the Bonded Magnet Market?

The bonded magnet market is gaining traction as manufacturers in the electric vehicle, industrial automation, and electronics sectors shift toward lighter, more efficient component solutions. OEMs are adopting bonded magnets for their design versatility, compact form factor, and ease of assembly in applications such as brushless DC motors, embedded sensors, and actuators used in EV systems, smart devices, and industrial robots.

Advancements in injection molding and additive manufacturing are streamlining production, enabling tighter tolerances and scalable output. The demand for tailored magnetic components that meet cost, performance, and supply chain requirements is driving the wider integration of bonded magnets in modern manufacturing environments.

What are the Regional Trends of the Bonded Magnet Market?

The bonded magnet market is experiencing varied regional growth patterns influenced by industrial strategies, technological capabilities, and access to resources. Asia Pacific dominates global output, led by China's control over rare-earth processing and its high-volume production of EVs and electronics. Japan and South Korea are driving demand through sustained investment in advanced motor systems across the automotive, robotics, and precision device sectors.

In North America, growth is supported by the increasing adoption of electric mobility and efforts to localize the processing of rare earths. The USA is promoting domestic magnet production to strengthen aerospace, automation, and clean energy supply chains, which rely on compact, high-efficiency magnetic components.

Europe remains a major region where regulatory momentum and automotive innovation are driving the wider adoption of lightweight materials despite the limited recyclability of bonded magnets. Applications such as electric drivetrains, HVAC systems, and industrial controls continue to absorb significant volume.

Emerging economies in Latin America, the Middle East, and Africa are witnessing a gradual increase in demand across automotive sub-assemblies, consumer electronics, and light industrial upgrades. Countries like Brazil and Mexico are advancing through localized production and infrastructure investment.

What are the Challenges and Restraining Factors of the Bonded Magnet Market?

A key concern is the dependence on rare earth elements, such as neodymium and dysprosium. These materials are not only costly but are also subject to supply chain risk, as China controls a dominant share of global output. Geopolitical uncertainty, export controls, and price volatility complicate cost control and supply assurance for manufacturers.

Performance limitations also present obstacles. Bonded magnets typically offer lower magnetic strength and reduced thermal resistance compared to sintered alternatives, making them less suitable for high-load or high-temperature use in EV traction motors and industrial heavy-duty systems.

Sustainability presents an additional pressure point. Bonded magnets use synthetic binders that complicate recycling, and few large-scale solutions exist for recovering composite materials. With regulatory expectations tightening, particularly in Europe and North America, manufacturers are being compelled to enhance environmental performance throughout their product lifecycles.

On the technical front, maintaining consistency during bonding and molding remains challenging, particularly in large-scale production. Precision-driven sectors such as robotics and sensors require tighter tolerances than current bonded magnet processes consistently deliver.

Bonded magnets also face stiff competition from ferrite and sintered magnets, which offer superior magnetic strength, better thermal durability, and economies of scale in established use cases. While bonded magnets provide design flexibility and easier integration, continuous material and process improvements are essential to maintain relevance in a maturing market.

Country-Wise Outlook

USA Bonded Magnet Market Grows on Back of EV Demand and Domestic Manufacturing Push

The USA bonded magnet market is gaining momentum, driven by the expansion of electric vehicle programs, a shift toward domestic material sourcing, and broader adoption across high-precision industries. As automakers accelerate EV development, demand is rising for lightweight, adaptable magnet solutions in auxiliary motors, power electronics, and vehicle sensors.

Growth is also supported by increased use in sectors such as aerospace, medical devices, and automation technologies, where the design flexibility and integration benefits of bonded magnets are highly valued. Federal policies, such as the Inflation Reduction Act, are reinforcing this momentum by supporting clean energy production and reducing dependence on imported rare earths.

In parallel, USA-based producers are investing in local processing and advanced molding to meet the evolving requirements of their applications. This emphasis on domestic capability, technical refinement, and supply resilience is positioning the USA as a key supplier of high-performance bonded magnets for next-generation mobility, defense, and industrial systems.

China Witnesses Strong Momentum in Bonded Magnet Production Amid Manufacturing Expansion

China remains a key driver of growth in the global bonded magnet market, anchored by its dominant position in rare earth processing, extensive manufacturing capacity, and expanding downstream sectors. With direct access to critical materials such as neodymium and dysprosium, Chinese producers enjoy cost and supply advantages that enable high-volume output of advanced bonded magnets.

The country’s electric vehicle sector, led by automakers like BYD, NIO, and XPeng, continues to demand bonded magnets for auxiliary systems, power electronics, and compact motor assemblies. Strategic programs, such as "Made in China 2025," are accelerating domestic electrification and industrial automation, thereby further deepening demand across the mobility and equipment markets.

China's role as a global electronics manufacturing hub sustains the use of magnets in miniaturized, precision-driven devices, including smartphones, wearables, and drones. Government-backed investments in smart factories, AI-integrated robotics, and renewable energy infrastructure are expanding application diversity and attracting ongoing research and development (R&D) activity.

Supported by industrial scale, coordinated policy, and end-to-end supply integration, China leads not only in bonded magnet output but also in setting global benchmarks for pricing, quality standards, and material innovation.

Japan Advances Bonded Magnet Applications Through Precision Manufacturing and Automotive Innovation

Japan remains a strategic market for bonded magnets, supported by its strengths in precision manufacturing, advanced electronics, and hybrid automotive technologies. Japanese manufacturers continue to utilize bonded magnets in compact motor assemblies, which are used in electric power steering, cooling systems, and sensor modules - applications where space constraints and exacting performance are critical.

Leading companies such as Toyota, Honda, and Panasonic incorporate bonded magnets into their hybrid vehicles, reflecting Japan's emphasis on fuel efficiency and a phased approach to electrification rather than a full transition to battery-electric cars. This strategic approach aligns with the advantages of bonded magnets in auxiliary systems that require lightweight, adaptable components.

Beyond automotive applications, Japan’s established electronics and automation industries contribute to sustained demand. Bonded magnets are integral to actuators, hard drives, and imaging systems where quiet operation and high positional accuracy are required. Growth in industrial robotics and smart factories continues to drive their use in servo motors and motion control technologies.

Japan is also advancing rare-earth recycling and material innovation to reduce its reliance on imports and strengthen long-term supply chain resilience. Ongoing collaborative R&D efforts are focused on enhancing magnet performance and promoting the efficient utilization of materials.

Category-wise Analysis

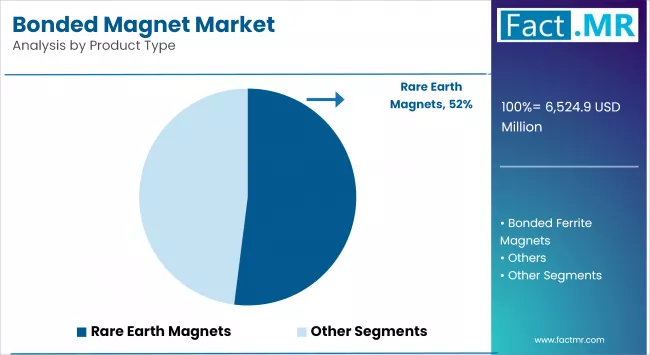

Bonded Ferrite Magnets to Exhibit Leading Share Among Product Types

Bonded ferrite magnets continue to dominate the market due to their cost efficiency, corrosion resistance, and broad material availability. These magnets are suitable for mass-market applications where high magnetic strength is not critical, but durability and stability in harsh environments are essential.

They are widely used in home appliances, HVAC systems, automotive components, and small electric motors, especially in blower motors, wiper systems, power seats, and household fan assemblies, where moderate performance requirements align with high production volumes.

Advancements in injection molding have enhanced the dimensional stability and mechanical strength of ferrite magnets, supporting their integration into more complex assemblies. With neodymium price volatility persisting, ferrite-based bonded magnets offer OEMs a dependable, lower-cost option that balances performance with affordability.

Their ongoing use across both developed and emerging regions underscores their established role in the bonded magnet sector.

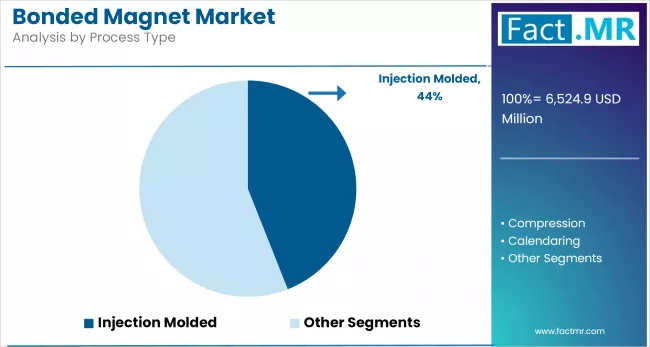

Calendaring to Exhibit Leading Share Among Process Types

Calendaring has become a widely used process in bonded magnet production, particularly for ferrite-based magnets, due to its ability to achieve uniform magnetic properties, precise thickness control, and consistent mechanical strength. The method is especially suited for flexible formats used in magnetic sheets, strips, sensors, and motor components.

Industries such as automotive, white goods, and office equipment prefer calendared magnets for their adaptability, cost efficiency, and suitability for high-volume output. The process enables continuous production, minimizing material waste and ensuring dimensional stability, key requirements for scaled manufacturing.

Calendaring also provides better control over particle alignment, which directly affects magnetic performance. As OEMs prioritize consistent, cost-effective magnet solutions that meet both mechanical and magnetic specifications, calendaring offers a repeatable, production-ready approach.

With rising demand from sectors focused on mass production and operational consistency, calendaring remains a foundational process in bonded magnet manufacturing.

Sensors to Exhibit Leading Share by Application

Bonded magnets are increasingly applied in sensor systems due to their design flexibility, dimensional precision, and suitability for compact electronic assemblies. Their moldability into complex geometries and direct integration into housings make them ideal for Hall effect sensors, position detectors, speed encoders, and proximity sensors.

In the automotive sector, bonded magnets support functions in wheel speed sensors, throttle position sensors, and gear detection modules, all of which are essential to ABS, transmission, and engine control units. As vehicles shift toward electronics-heavy architectures, particularly in electric and hybrid models, the need for lightweight, high-precision magnetic components in sensing platforms continues to rise.

Consumer electronics also drive adoption, with use in smartphones, wearables, and smart home systems that depend on consistent magnetic fields in confined spaces. Bonded magnets also contribute significantly to automation, robotics, and medical devices, enabling precise control and real-time monitoring.

Ongoing advancements in magnet composition and fabrication methods, such as injection molding and calendaring, have improved both performance and integration within sensor assemblies. As industries evolve toward connected and adaptive systems, bonded magnets are expected to remain central to the demand for sensing technology across global sectors.

Automotive Segment to Hold Leading Share in the Bonded Magnet Market by End Use

The automotive segment remains the largest consumer of bonded magnets, driven by the industry’s growing dependence on compact, efficient, and high-performance components. These magnets are widely used in power steering, seat motors, windshield wipers, fuel pumps, and braking systems due to their lightweight structure, design flexibility, and stable magnetic properties.

As electric and hybrid vehicles gain market share, demand has intensified for auxiliary motors and advanced electronic controls. Bonded magnets are well suited to these systems, enabling precise magnetic alignment, miniaturized designs, and quieter, energy-efficient operation. They are also integral to sensors that provide position, speed, and torque feedback, critical to modern vehicle safety and control systems.

In parallel, OEMs are seeking to reduce vehicle weight and production costs while maintaining functionality. Bonded magnets achieve these goals through seamless integration with automated techniques, such as injection molding, thereby reinforcing their value in automotive manufacturing environments.

East Asia holds the Leading Share in the Bonded Magnet Market

East Asia continues to lead the bonded magnet market, driven by the region's dominance in rare earth processing, advanced manufacturing, and high-demand sectors, including automotive, consumer electronics, and industrial automation. China, Japan, and South Korea collectively account for a significant share of global bonded magnet output, supported by mature supply chains and strong domestic demand.

China plays a central role, not only as the largest producer of rare earths but also as a key exporter of bonded magnets. Its expansive electric vehicle manufacturing sector, alongside household electronics and renewable energy infrastructure, sustains consistent demand for cost-effective magnet solutions. Chinese firms benefit from vertical integration, which enables them to control raw materials, enhance production efficiency, and determine pricing.

Japan contributes through precision applications in hybrid vehicles, robotics, and medical equipment. Manufacturers emphasize reliability by incorporating bonded magnets into compact motors and advanced sensor systems. South Korea supports regional growth through its consumer electronics and semiconductor industries, where miniaturized magnetic components play a critical role.

Ongoing investment in automation, electrification, and digital technologies continues to reinforce East Asia’s role as the global hub for bonded magnet innovation and manufacturing scale.

Competitive Analysis

The bonded magnet industry is shaped by a competitive landscape of established global manufacturers and specialized regional players, each contributing through innovation, vertical integration, and targeted end-use solutions. Leading companies, such as TDK Corporation, Hitachi Metals, Ltd., and Magnequench International, LLC, continue to influence the sector through their strong R&D capabilities and advanced material technologies in rare-earth-based magnet production.

Firms such as Ningbo Yunsheng Co., Ltd., Advanced Technology Materials Co., Ltd., and SDM Magnetics Co., Ltd. benefit from proximity to China's rare earth supply chain, which supports efficient manufacturing and cost competitiveness. Meanwhile, players such as Arnold Magnetic Technologies, Adams Magnetic Products, and Dura Magnetics, Inc. focus on high-performance applications in the automotive, aerospace, and industrial automation sectors, often emphasizing customization and compliance with stringent quality standards.

Other notable contributors include Mate Co., Ltd., Evitron Sp. z o.o., MMC Magnetics Corp., National Imports, LLC, and Super Magnet Co., Ltd., which serve niche markets through product differentiation and specialized formats. European firms such as RHEINMAGNET Horst Baermann GmbH and Daido Electronics Co., Ltd. emphasize precision and regulatory alignment, tailoring solutions to meet region-specific expectations.

Emerging players, including Galaxy Magnets, Shanghai San Huan Magnetics Co., Ltd., and MP Materials, are gaining traction by investing in downstream processing, supply chain control, and recycling initiatives aimed at reducing dependence on rare earths.

Recent Development

- In 2025, Nichia showcased advancements in bonded SmFeN magnets at MDSM 2025 in Florida, focusing on improved magnetic performance and injection-bonding processes. In June, the company presented further materials updates at Coiltech North America, promoting higher flux density and process improvements.

- In 2025, MP Materials commenced commercial production of NdPr metals and conducted trials of NdFeB magnets at its Independence, Texas, facility. The site aims to produce up to 1,000 tonnes annually by late 2025, helping to reestablish a full domestic rare-earth magnet supply chain.

Segmentation of Bonded Magnet Market

-

By Product Type :

- Rare Earth Magnets

- NdFeB

- SmCo

- Bonded Ferrite Magnets

- Others

- Rare Earth Magnets

-

By Process Type :

- Injection Molded

- Compression

- Calendaring

- Extrusion

-

By Application :

- Sensors

- Motors

- Hard Disk Drives

- Level Gauges

- Instrument Panels

- Copier Rotors

- Fuel Filters

- Magnetic Couplings

-

By End Use :

- Automotive

- HVAC Equipment

- Medical Devices

- Cameras

- Consumer Electronic Appliances

- Computers and Magnetic Storage Devices

- Electrical Equipment

- Measurement Instruments

- Printers and Copiers

-

By Region :

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- MEA

- Frequently Asked Questions -

What is the Global Bonded Magnet Market Size in 2025?

The bonded magnet market is valued at USD 6,524.9 million in 2025.

Who are the Major Players Operating in the Bonded Magnet Market?

Prominent players include TDK Corporation, Hitachi Metals, Ltd., Ningbo Yunsheng Co., Ltd., Advanced Technology Materials Co., Ltd., Magnequench International, LLC, and others.

What is the Estimated Valuation of the Bonded Magnet Market by 2035?

The market is expected to reach USD 13,828.1 million by 2035.

What Value CAGR Did the Bonded Magnet Market Exhibit over the Last Five Years?

The historic growth rate was 4.2% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed