Europe Construction Equipment Market Outlook from 2025 to 2035

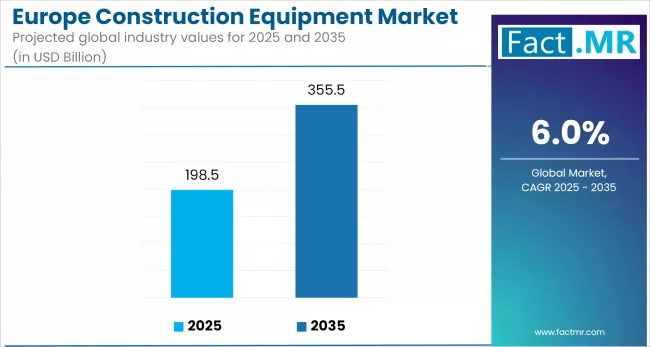

The Europe Construction Equipment Market is projected to increase from USD 198.5 billion in 2025 to USD 355.5 billion by 2035, with a CAGR of 6.0%, driven by EU-funded infrastructure projects, growing demand for electric and low-emission machinery, and a rise in the use of smart technologies.

Key markets, such as Germany, France, and the Nordics, are leading investments in urban redevelopment and transportation upgrades. Meanwhile, the expansion of rental services and digital tools is enhancing access and efficiency across the sector.

What are the Drivers of the Europe Construction Equipment Market?

Stricter environmental regulations, particularly from the European Union, are pushing industries to adopt effective waste management practices in order to meet recycling targets and minimize their environmental impact. Furthermore, the region's growing emphasis on sustainability is fueling demand for technologies that support the circular economy, which reduces the need for raw material extraction by recycling and reusing materials.

Technological advancements in automated shredders and energy-efficient systems are driving the construction equipment market in Europe by enhancing processing capabilities and improving operational efficiency. The growing emphasis on recycling in industries like plastics, metals, and municipal waste has also aided shredder adoption. These devices aid in waste reduction and facilitate the sorting and processing of materials for reuse in subsequent production cycles.

The amount of waste produced is increasing due to Europe's ongoing urbanization and industrialization, making efficient waste management solutions even more important. Shredder adoption is accelerating across various industries due to the shift towards a circular economy model, where products are designed to be both recyclable and reusable. Shredders are also utilized by businesses and municipalities to reduce disposal costs, increase recycling rates, and achieve sustainability objectives. All of these elements work together to set up the European construction equipment market for future growth and innovation.

What are the Country Trends of the Europe Construction Equipment Market?

The growth patterns of the European construction equipment market vary by nation and are influenced by industrial capacity, local infrastructure agendas, and regulatory frameworks.

Germany remains the largest market in the region, supported by substantial investments in energy transition infrastructure, digital construction technologies, and the development of transportation networks. The need for cutting-edge, low-emission equipment remains driven by the government's commitment to decarbonization and infrastructure renewal through initiatives such as the "Klimaschutzprogramm 2030." For efficiency and compliance, German contractors are also at the forefront of adopting telematics and digital technology.

France’s construction boom is being propelled by major public infrastructure initiatives, such as the opening of the Grand Paris Express project and the expansion of urban transportation systems. The nation has also accelerated the transition to electric and hybrid equipment by enacting stronger emissions and noise regulations on urban construction sites. French OEMs and rental companies are quickly upgrading fleets to comply with new environmental regulations.

Road, rail, and residential construction is expanding in the UK as a result of post-Brexit policy realignment and ongoing infrastructure investment under the National Infrastructure Strategy. There is a steady demand for earthmoving and tunneling equipment due to projects such as HS2 and the Thames Tideway Tunnel. The use of small and specialized machinery is also encouraged by the increased focus on energy-efficient housing and building retrofits.

Italy is modernizing its aging infrastructure and promoting economic growth in the southern regions by utilizing EU recovery funds. Over €190 billion in public investments are outlined in the government's "Piano Nazionale di Ripresa e Resilienza" (PNRR), with a large portion of those investments focusing on digital construction, mobility, and sustainability, all of which are closely related to equipment demand. Wider access to contemporary equipment is made possible by the resurgence of the rental industry in the Italian market.

Nordic nations, such as Sweden, Norway, and Finland, are becoming pioneers in environmentally friendly building techniques. These markets are early adopters of autonomous equipment, electric machinery, and zero-emission job site concepts, and they have aggressive net-zero emissions targets. The region's standing as a testing ground for cutting-edge construction technologies is being strengthened by government support for innovation and the robust presence of manufacturers like Volvo CE.

EU cohesion funds are helping Eastern European nations, such as Poland and Romania, invest in infrastructure. Urban development initiatives, energy infrastructure, and road expansion are creating the need for long-lasting, reasonably priced equipment. Although the area still relies heavily on traditional machinery, as regulations tighten, interest in mid-tier automation and hybrid models is increasing.

What are the Challenges and Restraining Factors of the Europe Construction Equipment Market?

Despite its potential for expansion, the European construction equipment market is facing some obstacles. Adoption is hampered by the high upfront costs of electric and hybrid machinery for small and mid-sized contractors. Demand cycles are slowed by infrastructure project delays resulting from complex permitting and regulatory procedures, particularly in France and Italy.

The region is experiencing a growing labor shortage, and the efficient use of sophisticated machinery is hampered by a shortage of qualified operators. Internationally operating manufacturers and rental companies face greater compliance burdens due to fragmented environmental regulations across EU nations.

Furthermore, the deployment of electric machines is limited by a lack of adequate charging infrastructure, and equipment deliveries are being delayed by persistent supply chain problems concerning batteries and semiconductors. Long-term equipment investment decisions are made even riskier by economic uncertainties and changes in public spending.

Country-Wise Outlook

Germany’s Construction Equipment Market Sees Steady Expansion Amid Infrastructure Modernization

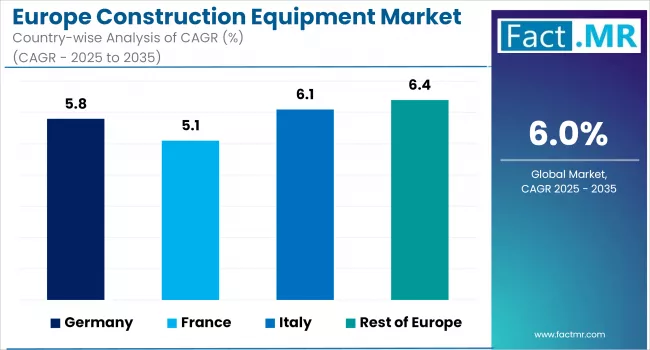

| Countries | CAGR (2025 to 2035) |

|---|---|

| Germany | 5.8% |

| France | 5.1% |

| Italy | 6.1% |

Construction technologies are all contributing to the country's steady growth in the construction equipment market. The Federal Transport Infrastructure Plan (BVWP 2030) and the government's multibillion-euro "Klimaschutzprogramm 2030" are driving a steady demand for energy-efficient buildings, rail development, and road construction.

Large-scale transportation improvements, such as autobahn extensions and high-speed rail corridors, are Germany's top priority. These projects call for a steady supply of pavers, heavy-duty earthmoving equipment, and tunneling machinery. With activity in public infrastructure, industrial parks, and affordable housing, the residential and commercial construction sectors are likewise demonstrating resilience.

Procurement decisions in the public and private sectors are being influenced by sustainability regulations. Contractors are being pushed to use hybrid and electric machinery due to the implementation of EU Stage V emission standards and increasing limitations on diesel-powered equipment in urban areas. The aggressive promotion of zero-emission construction zones by major cities like Berlin, Hamburg, and Munich is driving demand for battery-powered loaders, compact equipment, and excavators.

France Construction Equipment Market: Growth Anchored in Public Investment and Urban Development

Large-scale public infrastructure projects, urban redevelopment initiatives, and the drive for environmentally friendly building techniques are all contributing to the steady transformation of the French construction equipment market. Among the main motivators are ongoing construction of the Grand Paris Express, one of the biggest transportation infrastructure projects in Europe, and investments linked to France's France Relance recovery plan, which allocates more than €100 billion for economic revitalization, including sizeable sums for building and energy-efficient renovations.

Upgrades to the urban infrastructure in Paris, Lyon, Marseille, and other large cities are consistently driving up demand for small, low-emission devices that work well in crowded, noisy settings. In line with growing regulatory restrictions on diesel-powered machinery, inner-city sites are increasingly favoring electric excavators, battery-powered loaders, and low-noise demolition tools.

The thermal renovation of more than 700,000 homes by 2030 is one of France's energy transition and sustainable housing priorities. The market for equipment used in residential construction, site preparation, and demolition is expanding as a result of this policy direction. Concurrently, the government's encouragement of low-carbon building methods is promoting the wider use of intelligent, networked equipment that has telematics and emissions monitoring capabilities.

In France, the rental market is growing steadily, especially among small and medium-sized contractors who want to have access to cutting-edge machinery without having to shoulder the cost of ownership. Prominent rental companies are quickly adding electric and hybrid equipment to their fleets to meet local environmental regulations and rising customer demands.

Italy Construction Equipment Market: Strengthening Through Public Funding and Infrastructure Revitalization

The Italy construction equipment market is gaining momentum, driven by robust public funding and national efforts to modernize infrastructure. Strategic investments through government-backed initiatives and EU recovery funds are revitalizing the sector. Projects aimed at improving transportation, energy efficiency, and urban development are fueling demand for a wide range of machinery. As Italy accelerates its infrastructure overhaul, equipment manufacturers and rental companies are benefiting from increased procurement activity and rising demand for modern, efficient, and sustainable construction solutions.

Public infrastructure projects, particularly in roads, bridges, and railways, are boosting equipment sales across the country. The focus on green construction and energy-efficient practices is encouraging the adoption of advanced, low-emission machinery. Companies are also integrating digital tools and telematics into their fleets, improving operational efficiency and site management, further reinforcing the market’s steady growth and appeal to both domestic and foreign investors.

The Italy government’s push toward smart and resilient infrastructure is creating long-term opportunities for construction equipment suppliers. With increased attention to safety, automation, and productivity, demand for earthmoving, lifting, and material handling equipment continues to grow. Additionally, incentives for sustainable construction and emissions reduction are driving the transition toward electric and hybrid models, aligning Italy’s equipment market with broader European environmental and climate goals.

Italy’s construction equipment market is also benefiting from the resurgence of residential and commercial development. As urbanization increases and housing needs expand, construction activity is expected to remain high. Combined with favorable policy support and improved financing options, these factors are expected to sustain the market’s upward trajectory in the coming years.

Category-wise Analysis

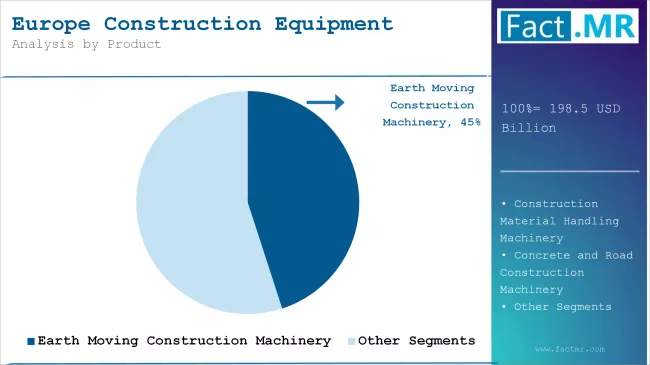

Earth Moving Construction Machinery to Exhibit Leading Share By Product

Earthmoving machinery continues to account for the largest share of the construction equipment market in Europe, underpinned by its critical role in a broad range of infrastructure, commercial, and residential projects. Excavators, bulldozers, backhoe loaders, and wheel loaders remain essential across all stages of construction, from site preparation and grading to trenching and foundation work.

The steady pipeline of large-scale civil projects across Europe, including transportation corridors, energy facilities, and urban redevelopment zones reinforces the segment's dominance. For example, projects such as Germany’s rail network modernization and France’s Grand Paris Express rely heavily on high-capacity earthmoving fleets to meet strict timelines and performance requirements.

Demand is strong in road and railway construction, where large excavators and bulldozers are vital for clearing, leveling, and shaping terrain. Similarly, compact earthmoving equipment is increasingly favored in urban environments where space constraints require maneuverable, low-emission machines for excavation and demolition tasks.

Ongoing shifts toward electrification and automation are also influencing the segment. Manufacturers are introducing battery-powered and hybrid models of mini-excavators and loaders to comply with stricter environmental regulations, particularly in cities with low-emission construction zones. Additionally, the integration of GPS guidance systems, machine control technologies, and remote diagnostics is enhancing the efficiency and precision of earthmoving operations.

In rental markets, earthmoving equipment accounts for a significant portion of demand, given its high utilization rate and versatility across various project types. With infrastructure spending on the rise across Europe, driven by both public investment and private-sector initiatives, earthmoving machinery is expected to continue its dominant role in the construction equipment sector.

Competitive Analysis

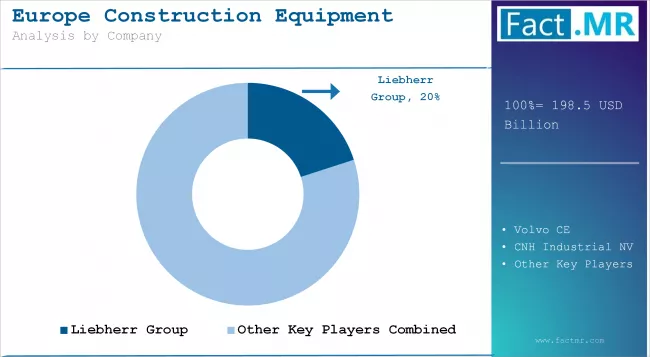

The European construction equipment market is led by a group of well-established manufacturers driving innovation, sustainability, and market expansion.

The Liebherr Group maintains a strong presence with its diverse range of machinery and continues to invest in hybrid and automation technologies. JCB is a key player in compact and hydrogen-powered equipment, especially suited to the UK’s evolving environmental goals. Volvo Construction Equipment leads in electric machinery, offering a growing fleet of battery-powered excavators and loaders tailored for urban sites.

CNH Industrial, through its Case and New Holland brands, supports a broad equipment portfolio and is enhancing its smart machine capabilities following the acquisition of Raven Industries. Wirtgen Group, part of John Deere, dominates the road construction segment with advanced pavers, compactors, and digital site solutions.

Other notable contributors include Hitachi, Bobcat, Kubota, and Manitou, all of which are expanding their electric and rental-ready equipment lines to meet the regulatory and operational demands of Europe.

Recent Development

- In 2025, Komatsu unveiled its latest range of electric mini-excavators (PC20E, PC26E, PC33E) at Bauma, offering extended runtime, reduced noise, and lower maintenance.

- In 2025, Hitachi Construction Machinery unveiled ten new models at Bauma, including the HX19e electric mini-excavator, loaders, and the hydrogen-powered HW155H wheeled excavator, highlighting its push into low-emission machinery.

Segmentation of the Europe Construction Equipment Market

-

By Product :

- Earth Moving Construction Machinery

- Excavator

- Loader

- Others

- Construction Material Handling Machinery

- Crawler Cranes

- Trailer-Mounted Cranes

- Truck-Mounted Cranes

- Concrete and Road Construction Machinery

- Concrete Mixer & Pavers

- Construction Pumps

- Others

- Earth Moving Construction Machinery

-

By Countries :

- Germany

- France

- UK

- Italy

- BENELUX

- Nordics

- Rest of Europe

- Frequently Asked Questions -

What is the Global Europe Construction Equipment Market Size in 2025?

The Europe Construction Equipment market is valued at USD 198.5 billion in 2025.

Who are the Major Players Operating in the Europe Construction Equipment Market?

Prominent players in the Europe Construction Equipment market include Liebherr Group, Joseph Cyril Bamford Excavators Ltd., Volvo CE, CNH Industrial NV, and others.

What is the Estimated Valuation of the Europe Construction Equipment Market by 2035?

The Europe Construction Equipment market is expected to reach a valuation of USD 355.5 billion by 2035.

What Value CAGR Did the Europe Construction Equipment Market Exhibit over the Last Five Years?

The historic growth rate of the Europe Construction Equipment market was 5.5% from 2020 to 2024.

Author:

Shubham Patidar

Editor:

Naved Ahmed