Europe Trash Compactor Market Outlook (2025 to 2035)

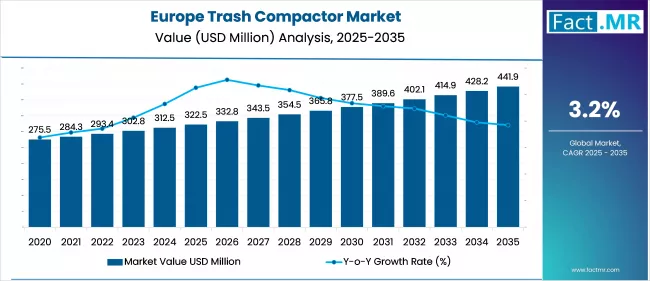

The Europe trash compactor market is projected to increase from USD 322.5 million in 2025 to USD 441.9 million by 2035, with a CAGR of 3.2% during the forecast period. Growing waste volumes, high landfill costs, and strict EU sustainability rules drive growth. There is a growing interest in smart, eco-friendly models, particularly for homes, businesses, and recycling, making the market ripe with new opportunities.

What are the Drivers of Europe Trash Compactor Market?

The European trash compactor market is supported by a solid manufacturing base, stringent environmental rules, and advanced recycling systems. Businesses and municipalities throughout the region are rapidly adopting smart, automated compactors as a means to lower disposal costs, reduce waste levels, and contribute to national sustainability objectives. People regard compacting solutions as crucial tools for enabling companies to achieve ESG goals and enhance operational efficiency.

Rapid urbanization and increasing waste generation in the U.K. are straining local waste management infrastructure even further. Consequently, both public and private businesses are investing in compactors to maximize space, simplify waste collection, and reduce reliance on landfills. Rising landfill levies and stricter environmental compliance standards are driving increased adoption in the commercial and residential sectors.

Furthermore, the Europe trash compactor market is driven by EU-aligned circular economy regulations, while France and Italy are also seeing consistent expansion. Rules like landfill bans and extended producer responsibility (EPR) are forcing companies to develop waste-reducing technologies, including compactors.

Public-private partnerships and government incentives that foster sustainable infrastructure help drive these initiatives. Meanwhile, in Southern and Eastern Europe, poor waste management and a lack of funds have slowed market uptake relatively. However, rising environmental awareness and increasing EU regulatory pressure are opening up new possibilities for compactor use in these developing areas, gradually.

What are the Country Trends of Europe Trash Compactor Market?

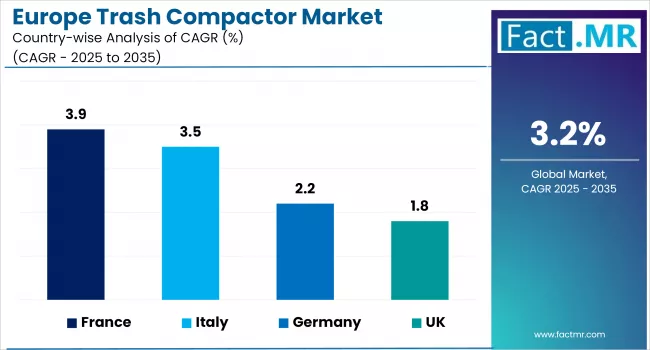

In Germany, factors such as strong dedication to environmental sustainability, modern waste infrastructure, and industrial maturity are expected to drive the country's growth during the forecast period. High-waste industries, such as manufacturing, logistics, and retail, have adopted intelligent and automated compactors. These systems help meet national goals of reducing reliance on landfills and align with circular economy principles. German companies are aggressively adopting technology-driven waste solutions to enhance efficiency and compliance with regulations.

In the UK, rising residential and commercial waste volumes, along with rapid urbanization, are driving demand for compactors. Tight municipal waste systems in large cities have prompted both the public and commercial sectors to invest in compactors as a cost-effective means of reducing disposal frequency, addressing space constraints, and improving urban cleanliness. Companies are utilizing compactors to meet sustainability requirements and enhance operational efficiency in space-constrained environments, particularly in retail and hospitality.

France remains committed to its EU circular economy goals, with the consistent rise in compactor usage reflecting this dedication. Encouraging broad implementation in both municipal and business environments, government rules stress recycling, source segregation, and landfill reduction. Together with growing sustainability objectives among companies, the legislative drive is aiding compactor systems to become a major component of national waste management plans.

What are the Challenges and Restraining Factors of Europe Trash Compactor Market?

A major problem for the European trash compactor industry is the high initial investment cost. Buying and installing advanced compactors, especially those with intelligent features, can be expensive. This poses a significant obstacle for local governments and small companies operating on limited budgets. The initial cost frequently postpones or hinders adoption even when obvious long-term savings and efficiency improvements are evident.

A lack of knowledge and understanding of contemporary waste management techniques is another obstacle. Many companies and institutions remain uncertain about the operation of garbage compactors and the benefits they may offer over time. Decision-makers may dismiss compactors as a practical solution without adequate training and exposure, thereby overlooking opportunities to reduce operating expenses and improve sustainability performance. Poor trash management systems in Southern and Eastern Europe exacerbate the difficulty.

The advantages of compactors are more difficult to see in areas where recycling systems and regular garbage collection are scarce. Although EU legislation and increasing environmental consciousness are gradually driving interest, this disconnect hinders market expansion in these areas.

Country-Wise Outlook

Germany Leads Europe’s Trash Compactor Market with Sustainability-Driven Innovation and Smart Waste Solutions

Driven by a deep-seated dedication to environmental sustainability and effective waste management, Germany's trash compactor sector is getting tremendous attention. The demand for dependable, space-saving, and reasonably priced waste management solutions has grown more pressing than ever as both industrial and civic sectors produce huge amounts of trash.

Companies across a variety of sectors, manufacturing, logistics, retail, and hospitality among them, are progressively using trash compactors to cut down the frequency of trash collection, save transportation costs, and improve operational space management. Particularly in urban areas with high population density, small and smart compactor solutions are seeing great demand as they address garbage fees and space restrictions.

The policy environment of Germany also serves as a strong development engine for this sector. Regulations like the Circular Economy Act call for strict waste prevention, separation, and recycling procedures, therefore pressure companies to use more environmentally friendly waste management techniques.

Adding to this, Germany's adherence to the EU Green Deal and severe enforcement of the Packaging Act further motivate the usage of compactors to more effectively handle packaging waste and recyclables. Also providing an environmentally responsible substitute for compactors are high landfill taxes and use limitations lowering trash bound for landfills.

Emerging technologies are accelerating this momentum. The market is increasingly demanding smart, solar-powered compactors equipped with IoT sensors, offering features such as automatic compaction cycles and real-time fill-level monitoring. Large-scale business and industrial consumers seeking high-tech solutions that align with their environmental objectives find particular appeal in these systems. Germany is emerging as a hub for cutting-edge, AI-driven waste management solutions, thanks to its robust innovation infrastructure and growing emphasis on ESG reporting.

Urban Waste Challenges and Green Regulations Drive Smart Compactor Adoption in the U.K.

Urbanization, limited space, and escalating landfill taxes are propelling quick growth in the U.K. trash compactor market. London, Birmingham, and Manchester, among other cities, are fighting rising amounts of household and business trash. By lowering collection frequency and shrinking the physical footprint of garbage, compactors provide a solution that directly helps companies and towns become cost-effective.

Prominent adopters include sectors like building, hospitality, healthcare, and retail. Specifically, the Environment Act 2021, a U.K. legislation, promotes sustainable waste management and underpins the Extended Producer Responsibility (EPR) programme. Companies are now expected to handle the waste they create more effectively, thereby motivating spending on waste reduction technology, including compactors. Furthermore, the U.K. government has implemented landfill restrictions on compostable municipal waste, making trash compaction a vital tool for compliance.

U.K. startups and waste-tech companies are exploring sensor-based compactors that initiate collection only when bins are full, enhancing operational efficiency and reducing fuel consumption.

France Accelerates Trash Compactor Adoption Through Circular Economy Laws and Urban Waste Innovation

Strict national regulations geared toward waste reduction and recycling are driving growth in the French trash compactor industry. French cities generate a significant amount of domestic and business waste; therefore, local authorities are under increasing pressure to handle it in an ecologically responsible manner. Particularly in retail, education, healthcare, and food services, companies are seeking to simplify waste collection and meet corporate sustainability objectives through the use of compactors.

France has implemented a progressive legal system, including the Anti-Waste and Circular Economy Law (AGEC Law), which aims to eliminate single-use plastics and promote eco-design in waste management systems. The government also forbids the landfilling of recyclables and requires sorting at the source. These rules are driving businesses toward small solutions that improve recyclability and reinforce separation. Emphasizing decentralized and effective waste management techniques, the results of the Grenelle Environment Forum also promote the use of compactors throughout towns.

Multi-stream compactors, which allow for the separation of multiple waste types (organic, plastic, and cardboard) within one system, offer significant potential in France. Equipment makers and service providers can access funded projects because of government assistance for public-private partnerships in waste infrastructure. In metropolitan areas, there is also an increasing need for compactors, combined with recycling booths, to promote citizen participation and reduce illegal dumping.

Category-wise Analysis

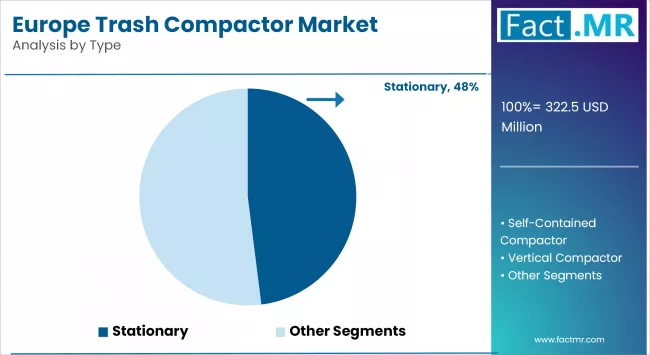

Stationary Compactors to Exhibit Leading by Type

Stationary compactors have a high-capacity design, making them ideal for industries with consistent, large-scale waste streams such as manufacturing, logistics, and large commercial hubs. These fixed systems are well-suited for dry waste and offer long-term cost efficiency for facilities with predictable waste output. Their dominance in countries like Germany and France is attributed to widespread industrial adoption and well-developed waste infrastructure.

Stationary compactors have low maintenance requirements, durability, and automatic compatibility. In high-output situations, these units may be easily combined with chute-fed systems and dock loading techniques to simplify operations. Their robust construction helps reduce failures and facilitates continuous use, a must for manufacturing and distribution facilities with 24/7 operations.

Additionally, encouraging long-term stationary system investments is a regulatory focus on effective waste management and landfill diversion across Europe. Their affordable lifecycle and configurable alternatives for specific industry needs render them a dependable and scalable solution for companies seeking to maximize waste management.

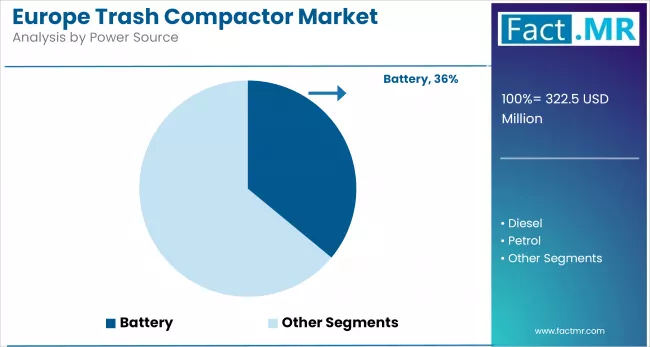

Battery-Powdered to Exhibit Leading by Power Source

Battery-powered waste management equipment dominates the market due to its increasing use in urban areas and indoor environments, where noise and emissions are restricted. Their energy efficiency, low maintenance requirements, and suitability for compact, automated systems make battery-powered solutions highly preferred for households and institutional facilities.

While diesel-powered units are not as dominant, they continue to hold strong relevance, especially in large-scale or remote applications such as construction sites and outdoor public areas. Their high power output and ability to operate for extended periods without frequent recharging or refueling make them suitable for heavy-duty applications.

Automatic to Exhibit Leading by Mechanism

Automatic compactors integrated with sensors and smart controls are becoming the preferred choice in commercial and municipal settings. These systems offer features such as remote monitoring, auto-compaction based on fill levels, and scheduling, resulting in greater efficiency and reduced labor costs. This trend is closely tied to the region’s digital transformation of urban infrastructure and the push toward “smart city” waste management solutions.

When it comes to waste type, compactors are used for dry, wet, and recyclable waste. Dry waste, such as paper, plastic, and cardboard, is the most commonly processed in both commercial and industrial environments. However, demand for multi-stream compactors that handle various waste types is increasing due to the EU’s push for circular economy practices. These systems enable on-site waste segregation, enhancing recycling rates and facilitating compliance with environmental regulations, such as the EU Waste Framework Directive and local recycling mandates.

Dry to Exhibit Leading by Waste Type

Dry waste holds the leading position in the market due to its greater volume in both residential and commercial sectors. Materials such as paper, plastic, and packaging waste contribute significantly to daily waste generation, prompting the use of specialized dry waste collection and disposal systems, particularly in urban areas and commercial establishments.

Wet waste, while generated in comparatively smaller volumes, is gaining increased attention, particularly in hotels, restaurants, and households. The need for proper segregation and treatment of biodegradable waste, including food and organic material, is driving the adoption of advanced composting and bio-processing technologies.

Commercial to Exhibit Leading by Application

Commercial applications are driven by the waste volumes generated in the retail, hospitality, healthcare, and food service industries. Compactors help these businesses reduce waste collection frequency and operational costs while meeting sustainability targets. Meanwhile, municipal applications are gaining traction, particularly with the introduction of smart, solar-powered compactors in public spaces, parks, and transit hubs. Local councils are increasingly adopting such systems to reduce overflowing bins and improve urban cleanliness.

The need for commercial applications for space optimization, regulatory compliance, and brand image management makes them the most preferred applications. Often working in space-constrained surroundings, companies in industries such as hospitality and retail need to reduce the amount of waste.

Compactors assist in managing odors, reducing bin mess, and maintaining tidier surroundings, which are major elements for health code compliance and customer satisfaction. Furthermore, environmental certifications and waste reporting mandates encourage commercial companies to use more effective, traceable waste solutions. This operational and reputational advantage helps the business sector lead compactor adoption.

Households to Exhibit Leading by End-Use

Households represent the largest end-use segment, driven by the sheer scale of residential waste generation and the growing adoption of waste segregation practices. Government-led awareness programs and the availability of user-friendly waste disposal products have significantly contributed to this segment’s dominance.

Healthcare facilities are another critical end-use area, requiring stringent waste handling due to the hazardous nature of biomedical waste. The need for safe, compliant, and efficient disposal methods is fueling the adoption of specialized waste treatment systems in hospitals, clinics, and labs.

Competitive Analysis

The Europe trash compactor market is highly competitive, with a mix of global giants, regional manufacturers, and tech-driven innovators. Major players like Gladiator Garageworks and Maren Engineering Corporation dominate the large-scale industrial segment with durable, high-capacity compactors and strong service networks. Regional leaders cater to local regulations and demand with customizable, modular systems suited for commercial, industrial, and municipal applications.

Innovation is a key trend, introducing smart, solar-powered, and IoT-enabled compactors to meet the growing demand for sustainable and efficient waste management solutions. Companies like Ecube Labs, Europress, and others focus on niche areas like vertical balers and underground compactors that serve urban environments with space constraints. These firms are leveraging AI, remote monitoring, and automation to enhance efficiency and appeal to municipalities and businesses that prioritize ESG goals.

Strategic partnerships and service bundling are becoming common, especially as customers seek integrated waste management solutions. Players are aligning with tech companies and waste service providers to offer predictive maintenance, data analytics, and smart monitoring systems.

Recent Development

- In January 2025, Ecube Labs (Seoul) expanded its CleanCUBE line throughout major European cities. Through this expansion, the company will deploy solar-powered smart bins equipped with remote fill-level monitoring and compaction algorithms to enhance smart-city waste infrastructure.

- In October 2024, Lisbon (Portugal) launched a new initiative to improve urban cleanliness and optimize waste collection with the deployment of solar-powered public waste compactors. These smart bins, modeled after units like Bigbelly, offer up to eight times the capacity of traditional bins due to their compaction technology.

Segmentation of Europe Trash Compactor Market

-

By Type :

- Stationary

- Self-Contained compactor

- Vertical Compactor

-

By Power Source :

- Battery

- Diesel

- Petrol

-

By Mechanism :

- Automatic

- Semi-Automatic

- Hydraulic

-

By Waste Type :

- Dry Waste

- Wet Waste

-

By Application :

- Commercial

- Industrial

- Residential

- Agricultural

- Municipal

-

By End-use :

- Healthcare

- Hotels & Restaurants

- Amusement Parks

- Institutional Facilities

- Construction Sites

- Households

- Others

-

By Country :

- Germany

- France

- U.K.

- Benelux

- NORDIC

- Italy

- Spain

- Rest of Europe

- Frequently Asked Questions -

What is the Europe Trash Compactor Market size in 2025?

The Europe trash compactor market is valued at USD 322.5 million in 2025.

Who are the Major Players Operating in Europe Trash Compactor Market?

Prominent players in the market include Bharati Industries, Orwak, CK International, Jenn-Air, Marathon Equipment Company.

What is the Estimated Valuation of the Europe Trash Compactor Market by 2035?

The market is expected to reach a valuation of USD 441.9 million by 2035.

What Value CAGR did the Europe Trash Compactor Market Exhibit over the Last Five Years?

The historic growth rate of the Europe Trash Compactor market was 2.1% from 2020 to 2024.

Author:

Shubham Patidar

Editor:

Naved Ahmed