Europe Ductile Iron Pipes Market Outlook (2025 to 2035)

The Europe Ductile Iron Pipes Market is forecast to reach USD 2,147 million by 2035, up from USD 1,370 million in 2025. During the forecast period, the industry is projected to register a CAGR of 4.6%, driven by increasing demand for clean and safe drinking water, as well as the growing production of ductile iron pipes tailored to the unique needs of various end-users.

| Metric | Value |

|---|---|

| Industry Size (2025E) | USD 1,370 million |

| Industry Size (2035F) | USD 2,147 million |

| CAGR (2025 to 2035) | 4.6% |

What are the Drivers of Europe Ductile Iron Pipes Market?

Numerous end-use industries are currently experiencing an increase in the utilization of ductile iron pipelines in conjunction with infrastructure development. Manufacturers are providing customized ductile iron pipes that are tailored to the specific needs of their consumers. The sales of ductile iron pipes are expected to increase in the near future due to this customization in the manufacturing process, which is expected to attract more customers.

Additionally, manufacturers are introducing ductile spools and coatings, fitting modifications, customized stainless spools, value chamber accessories, and other components for water work applications, as well as tapping fittings for custom machinery.

Market growth in Europe is expected to be driven by increased production of customized ductile iron pipes by key industry players in the coming years. The demand for ductile iron pipes is likely to increase due to the growing number of smart cities in Europe and the resulting rise in infrastructure development projects.

Additionally, governments are being compelled to implement water and wastewater management initiatives on a larger scale as a result of the increasing pressure to improve sanitation in urban areas and economic growth.

In addition to the aforementioned factors, the increasing awareness of the availability of clean and safe drinking water is a trend that will provide market participants with growth opportunities. Rising technological advancements, stricter regulations for agricultural irrigation and wastewater management, and the emergence of more efficient wastewater solutions are expected to create lucrative opportunities in the ductile iron pipeline production market.

Governments across Europe are investing in water purification initiatives to strengthen the procurement of ductile iron pipe fittings. This initiative is expected to generate substantial revenue streams for suppliers of ductile iron pipes.

What are the Country Trends of Europe Ductile Iron Pipes Market?

The highest sales of ductile iron pipes are recorded in Italy and Germany.

Germany's and Italy's markets, respectively, account for the largest share of the European markets. The market in Germany and Italy is expected to experience a steady CAGR increase during the assessment period, driven by substantial demand for infrastructural services, including water and electricity supply, roads and transportation, and sanitation.

Additionally, the increased demand for a durable, dependable, and robust water distribution system will create numerous opportunities for ductile iron pipes to provide water without contamination. In addition to the aforementioned factors, market demand will be driven by the increasing need for wastewater disposal to maintain a healthy environment and ensure excellent sanitary conditions in residential areas. This is due to the fact that the pipelines that transport sewage water must be of high quality and not react with the components of wastewater.

What are the Challenges and Restraining Factors of Europe Ductile Iron Pipes Market?

The market faces several significant challenges and restraining factors. High initial costs and the heavy weight of pipes make transportation and installation more expensive and logistically complex compared to lighter alternatives.

The market also competes with other materials, such as PVC and HDPE, which can offer lower costs or easier handling for certain applications. Additionally, susceptibility to environmental corrosion despite improvements in coatings remains a technical concern that can impact the longevity and reliability of pipes if not properly addressed.

Regulatory hurdles and economic factors further restrain market growth, as compliance with stringent European standards can increase costs and slow project timelines. Economic fluctuations and uncertainties in government infrastructure spending may also delay or reduce investments in large-scale water and wastewater projects, which can directly impact demand for ductile iron pipes.

These factors collectively create a challenging environment for market expansion, despite the strong underlying demand for durable and sustainable pipe solutions.

Country-Wise Outlook

Germany Ductile Iron Pipes Market Sees Growth Driven by Infrastructure Modernization and Expansion

The Germany market is witnessing strong growth, primarily driven by rising investments in infrastructure development, particularly in water supply, wastewater management, and sanitation systems. Germany holds a significant share of the European market and is expected to see its market grow at the fastest CAGR through 2032 to 2034, outpacing the regional average.

This growth is driven by the increasing need to upgrade outdated water and sewage infrastructure, address the rising demand for clean and safe drinking water, and comply with strict environmental regulations. Ductile iron pipes are favored for their durability, resistance to corrosion, and sustainability, as they are made with up to 90% recycled content and are fully recyclable. Growing urbanization and population pressures are also driving upgrades and expansions of municipal infrastructure. At the same time, innovations in pipe coatings and manufacturing processes further boost the adoption of pipes in Germany and across Europe.

Italy witnesses Rapid Market Growth Backed by Rising Investments in Water Infrastructure

Italy, along with Germany, holds one of the highest shares of ductile iron pipe consumption in Europe. This is largely due to increased investments in upgrading and expanding water supply and wastewater management systems to meet the growing demand for both urban and rural areas.

Compliance with EU water quality directives and environmental standards is prompting utilities to replace outdated, leakage-prone pipes with ductile iron alternatives, which offer superior corrosion resistance, durability, and sustainability (up to 90% recycled content and 100% recyclability). Furthermore, Italy is witnessing significant new launches and investments in its water infrastructure sector, with a strong focus on enhancing efficiency, resilience, and climate adaptation.

The France market is experiencing growth driven primarily by Sustainability and Climate Resilience.

France, in alignment with broader European trends, is investing in sustainable and climate-resilient infrastructure. Ductile iron pipes, being largely recyclable and capable of withstanding high pressure and harsh conditions, fit well with these sustainability goals. Their use is expanding, especially in flood-prone and seismically active areas where resilience is critical.

Substantial government funding is being allocated to water infrastructure upgrades, including water treatment and desalination projects, to address water scarcity and enhance water quality. This is generating attractive revenue streams for manufacturers and driving further market growth. Innovations in pipe coatings, linings, and jointing technologies are enhancing the performance and longevity of ductile iron pipes, making them even more attractive for new installations and replacements.

Key industry players, including Saint-Gobain PAM Canalisation (a major French manufacturer), are actively launching new ductile iron pipe products with improved hydraulic performance, enhanced corrosion resistance, and simplified joint installation. These launches are often aligned with the adoption of advanced coatings and linings that extend pipe lifespan and reduce maintenance costs.

Category-wise Analysis

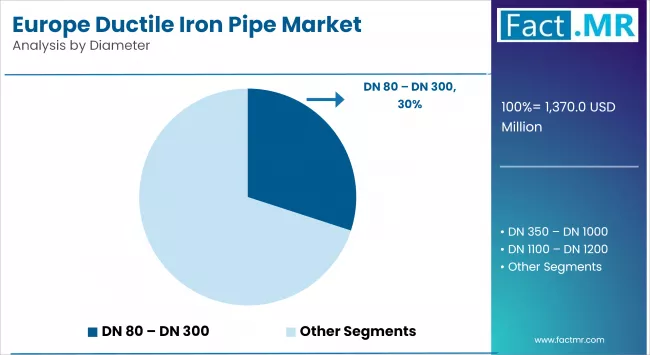

DN 350 - DN 1000 Diameter Ductile Iron Pipe Consumption to Remain the Highest

The diameter segment of the European market is divided into the following categories: DN80-DN300, DN350-DN1000, DN1000-DN1200, DN1400-DN2000, and DN2000 and above.

Among them, pipes with diameters ranging from DN 350 to DN 1000 are frequently used for sewerage purposes and hold the largest market share in the industry. They are capable of withstanding severe operating conditions due to their high-alumina cement mortar lining, which can withstand highly alkaline to highly acidic conditions.

Additionally, these pipelines are used to provide drinking water and are also in high demand in mining applications. The segment is projected to register significant compound annual growth throughout the forecast period. The demand for pipes with a diameter of DN 80 to DN 300 is expected to increase, driving an increase in market share during the forecast period.

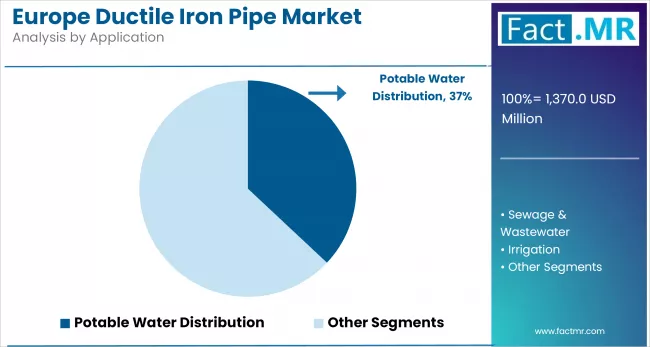

Potable Water Distribution Emerges as Key Application Due to Extensive Use of Ductile Iron Pipes

The market is segmented into the following application segments: potable water distribution, sewage & wastewater, irrigation, mining, and others. Potable water distribution is the market leader, with the largest share of the overall market. The segment is expected to experience a significant CAGR from 2025 to 2032, driven by the increased utilization of ductile iron pipes for water distribution, wastewater treatment facilities, and sewage outfall lines.

Ductile iron pipelines are also utilized extensively in the mining sector. In mining operations, these pipes are employed to convey water, slurry, and other materials. Ductile iron pipelines are well-suited to the rigorous conditions found in mining environments due to their durability and robustness.

The demand for pipes in this application segment is primarily driven by the need for efficient water and material transportation systems, as well as the growing number of mining activities. Furthermore, the mining sector's expansion of the market is further strengthened by the emphasis on sustainable mining practices and the reduction of environmental impact.

Industrial water supply systems, fire protection systems, and various infrastructure initiatives are among the other applications of ductile iron pipes. Ductile iron pipelines are suitable for a diverse array of applications due to their reliability and adaptability.

Significant factors contributing to the market expansion in these application areas include the growing demand for efficient water supply and fire protection systems in industrial zones, as well as the increasing number of industrial activities. Additionally, the demand for ductile iron pipelines in various other applications is expected to be driven by increasing investments in infrastructure projects, including transportation and energy infrastructure.

Zn/Zn-Al + Bitumen/Epoxy leads by External Protection in the Market

The dominating segment for external protection of pipes in the Europe market is Zn/Zn-Al + Bitumen/Epoxy. This is supported by industry trends and common practices in the European market, where zinc or zinc-aluminum coatings with a bitumen or epoxy overcoat are the standard and most widely adopted method for external protection of ductile iron pipes. This is due to their proven effectiveness in corrosion resistance and durability in various soil conditions.

Other external protection options, such as PE (polyethylene), PU (polyurethane), and ceramic epoxy, are used in more specialized or demanding environments; however, they do not match the market share or widespread adoption of the Zn/Zn-Al + Bitumen/Epoxy system in Europe. This aligns with the focus on reliable and cost-effective corrosion protection for large-scale water and wastewater infrastructure projects across the region.

Direct Sales Leads by Sales Channel in the Market

Direct sales are the dominant sales channel segment in the market. While the provided search results do not explicitly break down the market share between direct and indirect sales channels, industry norms and the nature of the pipes business, characterized by large-scale infrastructure projects, government contracts, and customized product requirements, strongly favor direct sales.

Direct sales channels enable manufacturers to work closely with municipal authorities, utilities, and construction firms, ensuring compliance with technical standards and project specifications. This inference is supported by the fact that ductile iron pipes are typically sold in bulk for major infrastructure projects, where direct negotiation, technical consultation, and after-sales support are critical. Indirect sales (via distributors or third parties) tend to play a smaller role, mainly serving smaller-scale or replacement orders.

Competitive Analysis

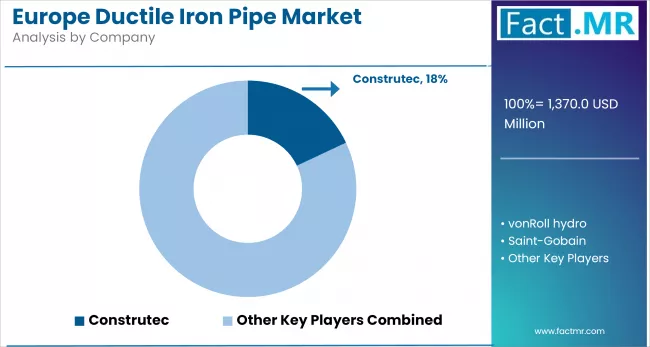

The market is defined by steady growth and intense competition, driven by the region's focus on modernizing water infrastructure, complying with strict environmental regulations, and advancing sustainable utility networks.

Strategic moves, such as mergers, acquisitions, and joint ventures, are common, enabling firms to consolidate expertise, optimize production, and expand geographically. Product innovation is a key competitive factor, with manufacturers investing in advanced materials, corrosion-resistant linings, and intelligent pipeline monitoring technologies.

Key players in the European ductile iron pipes industry include Construtec, vonRoll hydro GmbH & Co. KG, Saint-Gobain, LTK Svobodny Sokol LLC, Pulsar Measurement, Xylem, FT Pipeline Systems Ltd., VIP-Polymers Ltd., YTM Pipe, and other notable companies.

Recent Development

- In February 2025, Welspun Corp incorporated a wholly-owned subsidiary, Welspun Europe S.A., in Spain. The new entity will engage in trading pig iron/crude iron and various conduits, including ductile iron pipes, to boost exports and strengthen its presence in the European market.

- In April 2024, the Italian government allocated Euro 2 billion to primary water infrastructure, with a strong focus on securing water supply for major urban and irrigated areas and prioritizing the completion of large, unfinished plants in Southern Italy. The goals include enhancing network resilience, augmenting water transport capacity, and narrowing the North-South infrastructure gap. This investment also aims to create jobs within the sector and adapt infrastructure to ongoing climate change.

Segmentation of Europe Ductile Iron Pipes Market

-

By Diameter :

- DN 80 - DN 300

- DN 350 - DN 1000

- DN 1100 - DN 1200

- DN 1400 & DN 2000

- DN 2000 and Above

-

By External Protection :

- Zn/Zn-Al + Bitumen/Epoxy

- PE

- PU

- Ceramic Epoxy

-

By Application :

- Potable Water Distribution

- Sewage & Wastewater

- Irrigation

- Mining

- Others

-

By Sales Channel :

- Direct Sales of

- Indirect Sales of

-

By Country :

- Germany

- Italy

- France

- Spain

- U.K.

- Rest of Europe

- Frequently Asked Questions -

What is the Europe Ductile Iron Pipes Market size in 2025?

The Europe ductile iron pipes market is valued at USD 1,370 million in 2025.

Who are the Major Players Operating in the Europe Ductile Iron Pipes Market?

Prominent players in the market include Construtec, vonRoll hydro GmbH & Co. KG, Saint-Gobain PAM, LTK Svobodny Sokol LLC, and Pulsar Measurement.

What is the Estimated Valuation of the Europe Ductile Iron Pipes Market by 2035?

The market is expected to reach a valuation of USD 2,147 million by 2035.

What Value CAGR did the Europe Ductile Iron Pipes Market Exhibit over the Last Five Years?

The historic growth rate of the Europe ductile iron pipes market was 3.7% from 2020 to 2024

Author:

Shubham Patidar

Editor:

Naved Ahmed