Silicone Release Coatings Market Outlook (2025 to 2035)

The global silicone release coatings market is projected to increase from USD 851.4 million in 2025 to USD 1787.6 million by 2035, with a compound annual growth rate of 7.7%, driven by expanding demand from industries such as packaging, labels, medical devices, and industrial tapes.

The superior release properties, thermal stability, and chemical resistance of silicone-based coatings continue to make them the preferred choice for high-performance applications. In addition, the rising emphasis on efficient labeling solutions in logistics and e-commerce, along with technological advancements in solventless and UV-cured silicone systems, is further accelerating adoption across both developed and emerging markets.

What are the Drivers of Silicone Release Coatings Market?

The silicone release coating market is witnessing steady growth, primarily driven by increasing demand across the packaging, medical, and industrial sectors. In the packaging industry, the widespread use of pressure-sensitive labels, tapes, and liners, particularly in e-commerce logistics and retail, has significantly driven the adoption of silicone-based coatings due to their ability to ensure smooth release and high-speed processing.

Additionally, the healthcare sector is expanding its use of silicone release coatings in wound care, surgical drapes, and personal hygiene products, driven by rising healthcare expenditures and an aging population. In industrial applications, particularly in electronics and automotive, silicone release coatings play a crucial role in manufacturing specialty tapes and die-cut adhesives that require heat and chemical resistance.

Meanwhile, regulatory pressure and environmental concerns are accelerating the shift toward solventless and UV-curable silicone systems, which reduce emissions and improve energy efficiency. The growing integration of smart packaging and RFID technology is also enhancing the relevance of silicone-coated liners in modern manufacturing. These combined developments are shaping a strong demand trajectory for silicone release coatings across global markets.

What are the Regional Trends of Silicone Release Coatings Market?

The regional landscape of the silicone release coatings market is shaped by distinct industrial demands, regulatory environments, and technological advancements.

North America continues to lead in technological innovation and product adoption, especially in high-performance packaging and medical-grade applications. The United States, in particular, is experiencing a growing demand from the healthcare and food packaging sectors, where silicone-coated liners are preferred due to their consistency, cleanliness, and ease of processing. Increased investments in medical device manufacturing and stringent FDA packaging standards are further fueling market penetration.

Europe is also a key player, driven by a strong focus on sustainability and regulatory compliance. Countries such as Germany, France, and the Netherlands are promoting solventless and UV-cured silicone technologies to align with EU environmental directives. The region’s mature label printing and personal care industries continue to adopt advanced-release coatings to meet performance and recyclability targets.

The Asia-Pacific region is emerging as the fastest-growing market, driven by rapid industrialization, urbanization, and expansion in sectors such as electronics, consumer goods, and healthcare. China, Japan, South Korea, and India are witnessing an increase in the use of silicone-release coatings in flexible packaging, electronics adhesives, and hygiene products. Rising manufacturing capabilities and supportive government policies for exports are also contributing to growth.

Latin America presents opportunities in consumer packaging and personal care segments, particularly in Brazil and Mexico. However, growth here is somewhat restrained by economic instability and limited local manufacturing infrastructure for high-performance coating formulations.

In the Middle East and Africa, the market remains at a nascent stage but is gradually expanding with developments in food packaging and pharmaceuticals. Strategic partnerships with global suppliers and an increasing focus on improving local production standards are likely to drive future adoption.

What are the Challenges and Restraining Factors of Silicone Release Coatings Market?

The silicone release coatings market, while expanding steadily, faces several operational and strategic challenges that may hinder its broader adoption.

One of the key restraints is the high cost of silicone-based raw materials, such as polydimethylsiloxane (PDMS) and platinum catalysts. These materials are significantly more expensive than conventional coatings, making silicone-release liners less economically viable for price-sensitive markets, particularly in emerging economies. Additionally, fluctuations in the global supply of silicone intermediates can cause price volatility, disrupting production and supply chain planning.

Environmental and regulatory concerns also present barriers to growth. Solvent-based silicone coatings, while widely used for their performance attributes, emit volatile organic compounds (VOCs), which are tightly regulated in regions such as North America and the European Union. As sustainability becomes a more pressing requirement for manufacturers and end-users, compliance with evolving regulations, such as the EU REACH directive and US EPA standards, adds complexity and cost to manufacturing processes.

The limited recyclability of silicone-coated substrates poses another challenge. The non-stick properties that make silicone coatings effective also make it difficult to separate the release liner from its base material during recycling. This has led to increased scrutiny from environmentally conscious consumers and brand owners seeking more circular packaging solutions.

Technical complexity in formulation and application is a further limitation. Achieving consistent cure rates, anchorage, and coating weight across substrates requires advanced coating lines and skilled labor. This deters small- to mid-sized manufacturers from entering the market due to the high initial capital investments required for equipment and technology.

Lastly, competition from alternative release technologies, such as non-silicone polymer coatings and fluorinated compounds, adds pressure on silicone-based solutions. Although these alternatives may not offer the same level of performance, they are often marketed as more cost-effective or environmentally friendly, drawing interest from converters looking to reduce overall production costs.

Addressing these challenges will require industry-wide efforts in material innovation, recycling-friendly product design, cost optimization, and adherence to sustainability regulations, especially as end-user industries increasingly prioritize both performance and environmental accountability.

Country-Wise Outlook

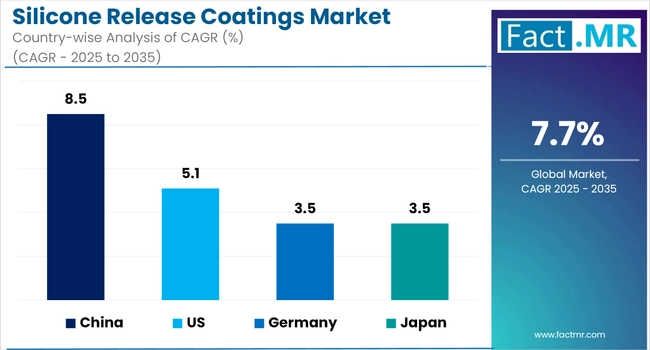

United States Silicone Release Coatings Market is Experiencing Robust Momentum, Driven By Increasing Demand From Key Sectors, Including Labels, Tapes, Hygiene Products, And Medical Packaging

The silicone release coating market in the United States is gaining steady traction, supported by expanding demand across diverse end-use industries, including packaging, healthcare, electronics, and hygiene.

The growth in pressure-sensitive labels, driven by increased consumption in the food and beverage, logistics, and pharmaceutical sectors, has significantly boosted the need for high-performance release liners. Silicone coatings are preferred in these applications for their consistent release force, heat resistance, and compatibility with various substrates, including glassine paper and PET film.

In the healthcare sector, the growing adoption of advanced wound care products and medical tapes is further elevating the demand for medical-grade silicone coatings that meet stringent biocompatibility and regulatory standards. Additionally, the shift toward UV-curable and solventless technologies aligns with environmental mandates and industry goals to lower VOC emissions, prompting USA-based manufacturers to modernize production lines. Strategic investments in R&D and capacity expansions are also underway, particularly among companies seeking to achieve faster curing times and enhanced coating uniformity to support high-speed converting processes.

China Witnesses Rapid Market Experiencing Strong Momentum, Driven by The Rapid Expansion of the Packaging, Electronics, and Hygiene Product Industries

China’s silicone release coatings market is experiencing strong momentum, driven by the rapid expansion of the packaging, electronics, and hygiene product industries.

As one of the world’s largest producers and consumers of pressure-sensitive labels, China has seen a significant increase in the use of silicone-based coatings to enhance release liner efficiency, particularly in e-commerce logistics, where demand for durable, low-friction label materials continues to rise.

Additionally, the domestic hygiene sector, including diapers, sanitary napkins, and medical disposables, has expanded significantly, resulting in a growing demand for reliable and skin-friendly silicone coatings. Chinese manufacturers are also investing in solventless and UV-curable technologies to comply with national environmental standards and reduce VOC emissions.

Moreover, the country's electronics sector is increasingly using silicone-coated films in protective masking and precision component assembly, further diversifying demand. These trends, coupled with government-backed initiatives supporting green materials and advanced manufacturing, are positioning China as a key growth engine in the global silicone release coatings market.

Japan Witnessing Steady Growth in its Silicone Release Coatings Market, Largely Supported by the Country’s Well-Established Electronics, Automotive, and Medical Sectors

Japan is witnessing steady growth in its silicone release coatings market, largely supported by the country’s well-established electronics, automotive, and medical sectors. Precision manufacturing remains a hallmark of Japanese industry, and silicone release coatings are increasingly integrated into high-performance applications such as semiconductor wafer handling, electronic component masking, and automotive adhesive systems.

The country's strong focus on quality control and low-defect manufacturing has accelerated the use of solventless and UV-curable silicone technologies to ensure clean release and reduced contamination.

Additionally, Japan’s aging population is fueling demand for advanced hygiene and medical products, where silicone-coated liners are essential in the production of wound care materials, transdermal patches, and disposable healthcare items.

Regulatory pressure to reduce volatile organic compounds (VOCs) has further encouraged innovation in eco-friendly formulations, with leading Japanese chemical firms investing in R&D to improve coating performance while adhering to strict environmental standards. As a result, Japan continues to play a strategic role in the Asia-Pacific market for high-precision silicone release coatings.

Category-wise Analysis

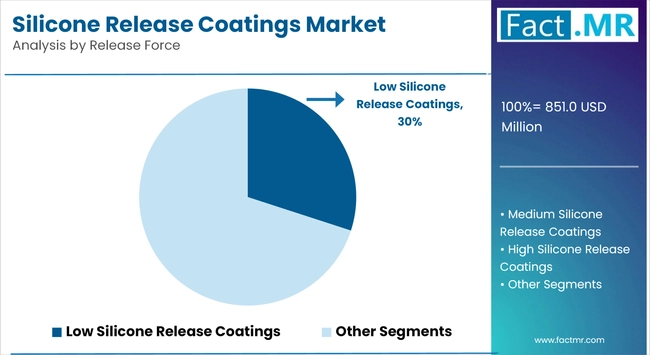

Medium Silicone Release Coatings to Exhibit Leading Share Among Release Force

Medium-release silicone coatings are expected to command the dominant share in the global silicone release coatings market, owing to their optimal balance between adhesion and release performance. These coatings are particularly well-suited for a broad range of industrial applications, including pressure-sensitive labels, graphic films, and medical tapes, where consistent release characteristics are essential for performance and process efficiency.

Medium-release coatings are favored for their compatibility with various adhesives, including acrylics, hot melts, and silicones, making them the preferred choice for converters and end users seeking versatility across product lines. Their widespread use in consumer goods packaging, hygiene products, and logistics labeling further underscores their market relevance.

Additionally, manufacturers are increasingly turning to solventless and UV-curable medium-release coatings to meet regulatory demands for lower emissions and sustainability. The scalability and ease of processing associated with medium-release formulations position them as a cost-effective solution for high-throughput applications, particularly in mature markets such as North America, Europe, and East Asia.

Solventless Silicone Release Coatings Category to Hold Leading Share in Silicone Release Coatings Market

Solventless silicone release coatings are expected to maintain a leading position in the global silicone release coatings market, driven by their superior performance characteristics and alignment with evolving environmental regulations. These coatings eliminate the need for organic solvents, thereby reducing volatile organic compound (VOC) emissions and enhancing workplace safety, a factor of increasing importance in industries under regulatory scrutiny, particularly in North America and the European Union.

The demand for solventless systems is particularly strong in applications such as pressure-sensitive adhesives, hygiene products, medical disposables, and industrial labels, where clean, consistent release performance is essential. Their fast curing speed and compatibility with high-speed coating lines contribute to increased production efficiency, making them a cost-effective solution for converters handling large-scale manufacturing.

Additionally, advances in platinum-catalyzed and UV-curable solventless technologies are enabling better control over coating weights and curing times, allowing for customization to meet specific end-use requirements. With growing interest in sustainable and energy-efficient production processes, manufacturers across the packaging, electronics, and healthcare sectors are increasingly shifting toward solventless silicone systems, further solidifying their market dominance.

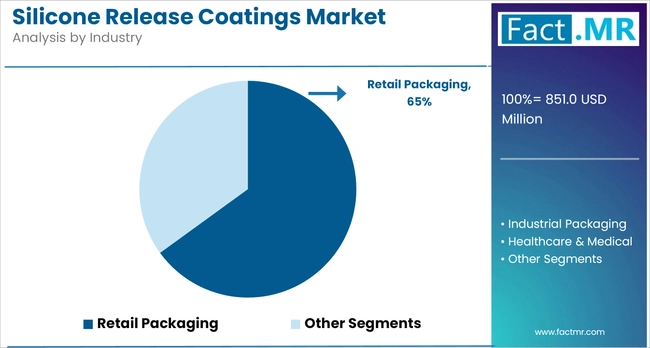

Labels/Laminates Category to Hold Leading Share in Silicone Release Coatings Market by End User

The labels and laminates segment is expected to hold the dominant share in the silicone release coatings market by end-user, driven by the surge in demand across industries such as consumer goods, logistics, pharmaceuticals, and food and beverage. As pressure-sensitive labels continue to play a vital role in branding, regulatory compliance, and inventory management, manufacturers are increasingly adopting silicone-based release coatings for their excellent peel performance and surface uniformity.

Silicone release coatings enable clean and efficient dispensing of labels, reduce downtime in high-speed labeling operations, and ensure consistent quality key requirements in automated packaging lines. The laminates sector is also benefiting from silicone coatings that enhance the bond strength and flexibility of multi-layered materials, making them ideal for flexible packaging and barrier films.

Furthermore, with the rise of e-commerce and increasing global logistics activity, there is a greater need for durable, weather-resistant labels that perform reliably in varied conditions. This trend is fueling investments in high-performance release liners, particularly those coated with solventless or UV-curable silicone systems, which offer both environmental compliance and operational efficiency. As brands seek to differentiate their products through premium labeling and smart packaging technologies, the demand for advanced silicone release solutions in the labels and laminates segment continues to grow steadily.

East Asia Hold Leading Share in Silicone Release Coatings Market

East Asia maintains a dominant position in the global silicone release coatings market, driven by the region’s extensive manufacturing base and high-volume demand across the packaging, electronics, and consumer goods sectors. Countries like China, Japan, and South Korea are driving adoption through robust industrial activity, growing export-oriented packaging needs, and investments in high-speed labeling technologies.

In China, the packaging industry continues to expand in tandem with rising domestic consumption and the booming e-commerce logistics sector. Silicone release coatings are widely used in label stock, tapes, and liners that meet the performance demands of fast-paced automated systems.

Japan’s focus on precision manufacturing and high-quality output fuels the demand for technically advanced silicone-coated substrates, particularly in electronics and healthcare packaging. Meanwhile, South Korea’s strong presence in semiconductor and display manufacturing contributes to specialized applications of release coatings in cleanrooms and protective films.

Moreover, the regional push toward sustainability through solventless and UV-curable silicone technologies aligns with both regulatory trends and corporate commitments to reduce environmental impact. Backed by technological innovation, competitive production costs, and growing end-user demand, East Asia remains at the forefront of the silicone release coatings market, both in terms of volume and innovation.

Competitive Analysis

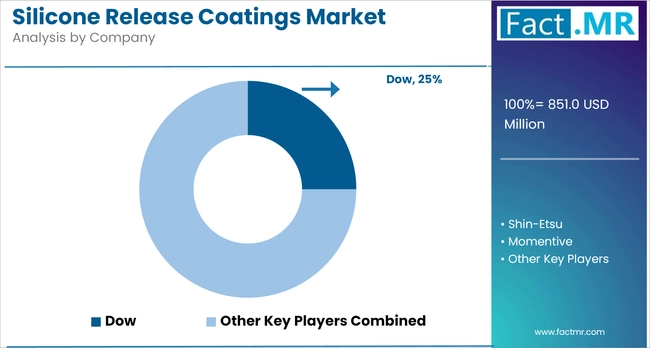

The silicone release coatings market is defined by intense competition, with several established global players driving innovation and setting industry benchmarks. Leading companies, such as Dow Corning Corporation, Shin-Etsu Chemical Co., Ltd. (Japan), Wacker Chemie AG, and Momentive Performance Materials Inc., play a pivotal role in shaping market dynamics through their extensive product portfolios and focus on R&D to enhance coating performance, durability, and environmental compliance.

Other notable contributors include Evonik Industries AG, KCC Silicone, Elkem Silicones, and Silibase, all of which actively invest in developing tailored solutions for high-growth sectors such as packaging, medical devices, electronics, and industrial labels. These firms often leverage advancements in solventless and UV-curable technologies to meet tightening sustainability regulations and growing customer demand for low-emission, high-efficiency materials.

Additionally, PPG’s entry into specialty coatings further underscores the growing interest in high-performance silicone release technologies, particularly in pressure-sensitive applications. The competitive landscape is further intensified by regional manufacturers expanding their global footprint through strategic collaborations, capacity expansions, and customized product offerings, ensuring the market remains dynamic and innovation-driven.

Recent Development

- In 2023, Dow Inc. introduced SYL-OFF SL 184, a carbon-neutral silicone release coating, at Labelexpo Europe. The product is designed for high-speed labeling operations and supports sustainability goals by reducing carbon footprint.

- In 2023, Wacker Chemie AG introduced the DEHESIVE eco series, an environmentally friendly silicone release agent designed for label and tape manufacturers seeking low-VOC and sustainable options.

Segmentation of Silicone Release Coatings Market

-

By Release Force :

- Low Silicone Release Coatings

- Medium Silicone Release Coatings

- High Silicone Release Coatings

-

By Type :

- Solvent-based Silicone Release Coatings

- Solventless Silicone Release Coatings

- Thermal

- UV Radiation

-

By End User :

- Packaging Industry

- Tapes

- Labels / Laminates

- Medical Industry

- Adhesive Bandages

- Wound Dressings

- ECG

- Others

- Hygienic Release Liners

- Baby Diapers

- Sanitary napkins

- Cooking & Baking

- Bakery Items

- Other Food Products

- Advertising Industry

- Graphic Arts

- Outdoor Advertising

- Others

- Packaging Industry

-

By Region :

- North America

- Latin America

- Europe

- East Asia

- South-East Asia & Oceania

- Middle East & Africa

- Frequently Asked Questions -

What is the Global Silicone Release Coatings Market Size in 2025?

The silicone release coatings market is valued at USD 851.4 million in 2025.

Who are the Major Players Operating in the Silicone Release Coatings Market?

Prominent players in the silicone release coatings market include Dow Corning Corporation, Shin-Etsu Chemical Co. Ltd. (Japan), PPG and among others.

What is the Estimated Valuation of the Silicone Release Coatings Market by 2035?

The silicone release coatings market is expected to reach a valuation of USD 1787.6 million by 2035.

What Value CAGR Did the Silicone Release Coatings Market Exhibit over the Last Five Years?

The historic growth rate of the silicone release coatings market was 8.1% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed