Europe Silicone Rubber Market Outlook (2025 to 2035)

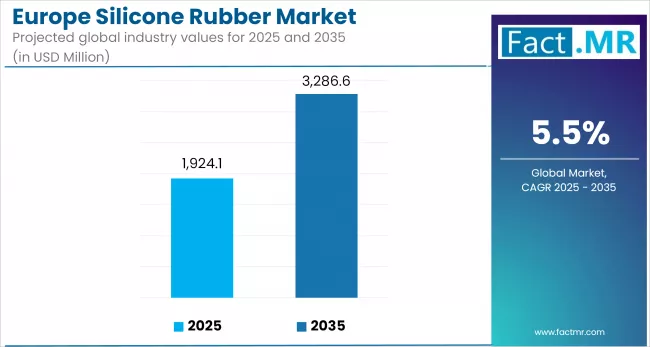

The European Silicone Rubber Market is expected to increase from USD 1,924.1 million in 2025 to USD 3,286.6 million by 2035, with a CAGR of 5.5% from 2025 to 2035, driven by rising demand in automotive, healthcare, construction, and renewable energy sectors.

The increased adoption of electric vehicles, medical devices, and solar applications is driving the demand for durable, heat-resistant elastomers.

What are the Drivers of the European silicone Rubber Market?

The European silicone rubber market is primarily driven by growing demand for high-performance applications across the automotive, healthcare, electronics, and construction sectors. In the automotive industry, the shift toward electric and hybrid vehicles is accelerating the use of silicone rubber for components such as thermal insulation, connectors, gaskets, and cable protection materials that must withstand heat, vibration, and chemical exposure.

The healthcare sector is another major growth area. The rise in aging populations and advancements in wearable medical technology are increasing the use of biocompatible silicone in devices such as catheters, tubing, and implants. Regulatory approvals across the EU for medical-grade materials continue to reinforce this trend.

In renewable energy and infrastructure, silicone rubber is used in photovoltaic panels, wind turbines, and weatherproof sealing systems. Europe’s push for clean energy and stricter building standards is prompting the wider adoption of silicone materials, which offer a long service life and resistance to UV and moisture.

Electronics and consumer goods also contribute, as silicone rubber is favored for flexible keypads, seals, and heat-dissipation components in compact, high-performance devices.

Finally, increasing regulatory emphasis on sustainability, fire safety, and low-emission materials in Europe is encouraging the shift from traditional polymers to durable, chemically stable silicone-based alternatives. These factors are reinforcing silicone rubber’s role as a critical material in Europe’s advanced manufacturing and infrastructure landscape.

What are the Country Trends of the Europe Silicone Rubber Market?

Germany leads the European silicone rubber market, backed by its strong automotive and engineering sectors. The country’s focus on electric vehicle production and advanced manufacturing fuels demand for high-performance silicone components used in thermal management, sealing, and vibration control. Additionally, Germany’s well-established medical device industry continues to adopt medical-grade silicones for tubing, implants, and surgical instruments.

France is seeing growing demand for silicone rubber in both infrastructure and renewable energy projects. The country's push toward decarbonization, including the expansion of offshore wind and solar, is increasing the need for weather-resistant silicone sealants and insulators. Government investments in healthcare and public transportation are also supporting the adoption of silicone in critical systems requiring long-term durability and safety.

Italy contributes through its footwear, textiles, and consumer goods industries. Manufacturers are using silicone rubber for flexible molds, fashion accessories, and industrial rollers due to their resilience and aesthetic versatility. Additionally, Italy’s strong presence in food processing equipment drives demand for FDA-compliant silicone materials used in hygienic applications.

In the United Kingdom, growth is concentrated in the healthcare and aerospace sectors. Demand for lightweight, high-purity silicone rubber components is rising in applications where regulatory compliance and material performance are critical. UK-based R&D in medical technologies is also fostering new silicone formulations for diagnostic and therapeutic tools.

Spain and the Nordics are investing in sustainable construction and green energy, increasing the use of silicone-based adhesives, sealants, and insulators in extreme weather environments. Meanwhile, Eastern European countries such as Poland and the Czech Republic are expanding production capabilities for automotive and industrial parts, creating new demand for both liquid and high-consistency silicone rubber.

What are the Challenges and Restraining Factors of the Europe Silicone Rubber Market?

Despite its strong outlook, the European silicone rubber market faces several structural and operational challenges that could affect long-term growth and competitiveness.

Raw material price volatility remains a persistent concern. Silicone rubber production relies on high-purity silicon and specialty chemicals, which are often imported or vulnerable to global supply disruptions. Periodic shortages and price surges, exacerbated by geopolitical tensions and energy costs, can strain profit margins for both producers and downstream manufacturers.

Energy-intensive manufacturing processes are another limiting factor for the growth of the silicone rubber market in Europe. Producing silicone rubber involves high-temperature synthesis and curing stages, which conflict with Europe’s tightening carbon emission regulations and rising electricity costs. This puts pressure on producers to modernize facilities or shift toward cleaner technologies, often requiring capital investment.

Regulatory compliance and chemical safety laws under the EU’s REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) framework also pose barriers. These regulations demand rigorous testing and documentation for chemical substances, including additives and curing agents used in silicone formulations. For small and mid-sized companies, maintaining compliance can be a resource-intensive task.

Limited scalability in some high-performance applications, such as aerospace, defense, or specialized medical devices, further constrains growth. These industries often require custom silicone grades, where qualification cycles are long and market entry is challenging due to strict performance standards.

Competition from thermoplastic elastomers (TPEs) is also growing because they offer cost-effective alternatives with simpler processing requirements in applications where the superior heat and chemical resistance of silicone rubber is not essential. Their versatility, recyclability, and compatibility with standard plastic manufacturing methods make TPEs increasingly attractive in industries such as consumer goods, electronics, and automotive interiors.

Lastly, recycling and end-of-life management for silicone rubber remain underdeveloped. Unlike thermoplastics, cured silicones are not easily recyclable, which raises concerns about their end-use sustainability. As circular economy policies gain traction across Europe, the lack of scalable recycling infrastructure for elastomers could become a competitive disadvantage.

Country-Wise Outlook

Germany Strengthens Its Position in Silicone Rubber Applications Across Advanced Industries

Germany’s silicone rubber market continues to grow, supported by its leadership in automotive manufacturing, engineering, and medical technology. With the country's strong push toward electric mobility, demand for high-performance silicone components, such as thermal insulation, cable protection, and battery gaskets, has increased significantly. Leading automakers, such as Volkswagen, BMW, and Mercedes-Benz, are integrating silicone materials into their EV powertrain systems and electronic modules to meet thermal management and durability requirements.

The healthcare sector is another key contributor. Germany’s robust medical device industry utilizes medical-grade silicone rubber in applications including tubing, surgical components, prosthetics, and diagnostic devices. The material’s biocompatibility and resistance to sterilization make it ideal for hospitals and clinical environments with strict hygiene standards.

In industrial machinery and automation, silicone rubber is widely used in seals, diaphragms, and high-precision molded parts that must withstand extreme temperatures and repetitive motion. This aligns with Germany’s ongoing investment in Industry 4.0 technologies and precision engineering.

Moreover, the construction sector is adopting silicone-based sealants and insulating materials in response to evolving energy efficiency and fire resistance regulations. These applications are particularly relevant for retrofitting older buildings to meet new sustainability benchmarks outlined in Germany’s national climate strategy.

With an emphasis on R&D, material innovation, and regulatory compliance, Germany remains a central hub for the development and application of silicone rubber in Europe’s high-performance sectors.

France Advances Silicone Rubber Use in Energy, Healthcare, and Industrial Innovation

France's silicone rubber market is evolving steadily, supported by the country’s strategic investments in renewable energy, medical technology, and aerospace manufacturing. The national focus on decarbonization, driven by the French Energy and Climate Law, has accelerated the deployment of solar panels, wind turbines, and building retrofits, all of which require durable silicone materials for sealing, insulation, and weather protection.

In the construction sector, silicone-based adhesives and sealants are increasingly used in high-performance glazing systems, fire-resistant facades, and energy-efficient infrastructure. These materials meet France’s stringent thermal regulation codes (RT 2020), contributing to the government's broader environmental targets.

France also maintains a robust presence in the pharmaceutical and medical device industry in regions such as Île-de-France and Auvergne-Rhône-Alpes. Here, demand for medical-grade silicone rubber continues to grow in applications like tubing, respiratory components, diagnostic systems, and implantable devices. The material’s biocompatibility, chemical resistance, and flexibility make it essential in sterile and high-precision environments.

Meanwhile, France’s aerospace and defense sectors, anchored by companies such as Airbus and Safran, utilize silicone rubber in gaskets, vibration dampeners, and lightweight thermal insulation systems for both civilian and military aircraft. The material’s reliability under high stress and variable temperatures makes it standard in mission-critical applications.

With increasing demand for locally manufactured, compliant, and high-performance elastomers, France is emerging as a key player in the European silicone rubber value chain, backed by regulatory alignment, public-private innovation, and its advanced industrial base.

Italy Expands Use of Silicone Rubber Across Industrial and Consumer Manufacturing Sectors

Italy’s silicone rubber market is growing steadily, underpinned by strong demand in automotive components, food processing equipment, consumer goods, and industrial machinery. The country’s established manufacturing base in northern regions, such as Lombardy and Emilia-Romagna, supports consistent consumption of high-performance elastomers in both B2B and B2C applications.

The automotive sector, with the presence of global OEMs and a vast network of Tier 1 and Tier 2 suppliers, utilizes silicone rubber in gaskets, hoses, and sensor housings that must perform reliably under thermal and mechanical stress. The transition to hybrid and electric vehicles is further expanding the use of silicone-based materials for battery insulation and cable protection.

In the food and beverage processing industry, silicone rubber is widely used due to its thermal resistance, hygienic properties, and compliance with EU food-contact safety standards. Manufacturers in Italy increasingly use FDA-grade silicone in seals, conveyor belts, and mold components in dairy, pasta, and bottling plants, where durability and cleanliness are essential.

The consumer goods sector also plays a significant role. Silicone rubber is commonly used in kitchenware, molds, baby care products, and flexible electronics due to its tactile quality and design flexibility. Producers of high-end home and fashion accessories in Italy are incorporating silicone into their modern product lines, where aesthetics meet functionality.

Additionally, Italy’s industrial automation and tooling sectors use silicone rubber in applications such as rollers, vibration dampers, and protective covers. As machine builders and toolmakers prioritize material longevity and operational efficiency, silicone offers an effective solution under high-load and high-temperature conditions.

Category-wise Analysis

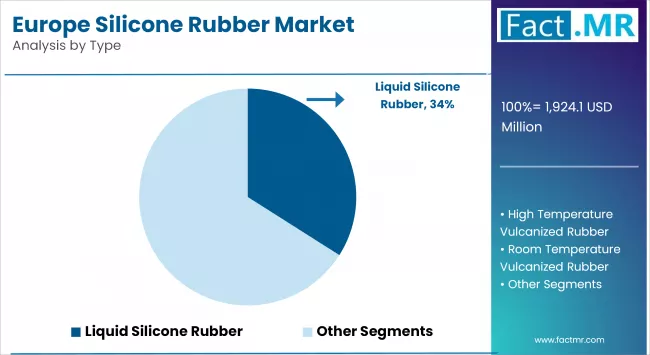

High Temperature Vulcanized (HTV) Rubber to Exhibit Leading Share By Type

High-Temperature Vulcanized (HTV) silicone rubber holds the largest market share in Europe, driven by strong demand in automotive, construction, aerospace, and industrial machinery. Its superior heat resistance, mechanical strength, and electrical insulation make it ideal for under-the-hood components, weatherproof seals, and molded parts exposed to harsh environments.

HTV is widely adopted in EVs, building systems, and flame-retardant transport applications, meeting strict EU safety and durability standards. As industries prioritize long-life, compliant materials, HTV remains the preferred silicone type for high-stress, high-temperature operations.

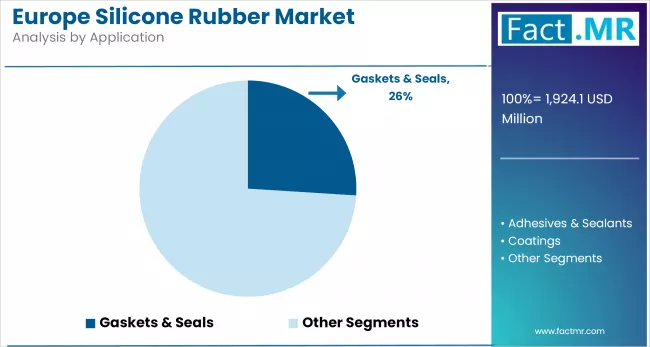

Gaskets & Seals to Hold Leading Share in Europe Silicone Rubber Market by Application

Gaskets and seals account for the leading share of silicone rubber demand in Europe, driven by their widespread use across automotive, aerospace, industrial equipment, and construction sectors. These components are essential for preventing fluid leakage, maintaining pressure, and ensuring thermal insulation in high-performance systems.

In the automotive industry, silicone-based gaskets are widely used in engines, battery enclosures, and exhaust systems due to their resistance to heat, oil, and vibration, which is especially critical as electric vehicle adoption increases. The aerospace and rail transport segments also rely on silicone seals that meet stringent fire, smoke, and toxicity (FST) regulations for passenger safety.

In construction, weather-resistant silicone seals are applied in facades, curtain walls, and glazing systems to support energy efficiency and compliance with EU building codes. Meanwhile, industrial machinery uses custom silicone gaskets in pumps, compressors, and fluid-handling systems to ensure performance under mechanical and thermal stress.

Given their role in improving reliability, extending equipment life, and meeting regulatory standards, gaskets and seals will continue to anchor demand in Europe’s silicone rubber market.

Automotive to Hold Leading Share in Europe Silicone Rubber Market by End User

The automotive industry holds the largest share of silicone rubber consumption in Europe, supported by the region’s robust vehicle production and ongoing transition to electric mobility. Silicone rubber is integral to a wide range of automotive components due to its superior thermal stability, weather resistance, and flexibility under mechanical stress.

Major European automakers, such as Volkswagen, Stellantis, BMW, and Mercedes-Benz, rely on silicone for applications, including gaskets, seals, ignition cables, thermal insulation, and sensor housings. In electric vehicles, silicone is increasingly used in battery packs, charging connectors, and powertrain components, where materials must endure high temperatures and maintain long-term reliability.

The material also plays a growing role in ADAS (Advanced Driver Assistance Systems), helping to protect sensors and electronic modules from moisture, vibration, and electromagnetic interference. Additionally, silicone’s compliance with strict EU automotive safety and environmental regulations makes it the preferred elastomer for both traditional and next-generation vehicle platforms.

With continued investment in EV infrastructure, stricter emission standards, and growing demand for lightweight, durable materials, the automotive sector is expected to remain the dominant end-user of silicone rubber across the European market.

Competitive Analysis

The European silicone rubber market is characterized by the presence of several established global and regional players that continue to drive innovation, expand application portfolios, and strengthen supply chains.

Key participants in the Europe silicone rubber industry include Momentive Performance Materials, Dow Inc., and Wacker Chemie AG, all of which have a manufacturing footprint and R&D presence across Europe. These companies lead in the development of high-consistency rubber (HCR), liquid silicone rubber (LSR), and specialty compounds tailored to automotive, healthcare, electronics, and construction applications.

Elkem Silicones and Simtec Silicone Parts are also prominent, offering vertically integrated solutions from raw material production to precision-molded parts, with a focus on sustainability and regulatory compliance. Reiss Manufacturing and Stockwell Elastomerics cater to niche demands in the aerospace, medical device, and industrial sealing systems sectors, emphasizing custom formulation and short-run flexibility.

Meanwhile, Innovative Silicones and other mid-sized firms are gaining traction through agile production strategies and specialize in high-performance, application-specific silicone products.

Together, these players are shaping market dynamics through product development, automation investments, and a growing emphasis on energy-efficient and recyclable silicone technologies. Strategic partnerships, capacity expansions, and compliance with evolving EU standards further reinforce their positions in the highly competitive European landscape.

Recent Development

- In 2025, Wacker Chemie AG introduced two innovative silicone rubber products, ELASTOSIL N 9189 and N 2076, specifically designed for power plant generators, featuring a tin-free formulation and thermal stability of up to 230 °C.

- In 2024, Momentive Performance Materials expanded its distribution of beauty and personal care products in Europe through a partnership with TER Chemicals, covering Germany and Austria. The agreement includes the launch of HARMONIE™, a line of bio‑based, high-performance silicone formulations.

Segmentation of the Europe Silicone Rubber Market

-

By Type :

- Liquid Silicone Rubber

- High Temperature Vulcanized Rubber

- Room Temperature Vulcanized Rubber

- Fluorosilicone Rubber

-

By Application :

- Gaskets & Seals

- Adhesives & Sealants

- Coatings

- Encapsulants

- Catheters & Tubing

- Others

-

By End-user Industry :

- Electronics

- Aerospace

- Construction

- Medical

- Automotive

- Consumer Products

- Frequently Asked Questions -

What is the Global Europe Silicone Rubber Market Size in 2025?

The Europe Silicone Rubber market is valued at USD 1,924.1 million in 2025.

Who are the Major Players Operating in the Europe Silicone Rubber Market?

Prominent players in the Europe Silicone Rubber market include Materials, Dow Inc., Wacker Chemie AG, Simtec Silicone Parts, and others.

What is the Estimated Valuation of the Europe Silicone Rubber Market by 2035?

The Europe Silicone Rubber market is expected to reach a valuation of USD 3,286.6 million by 2035.

What Value CAGR Did the Europe Silicone Rubber Market Exhibit over the Last Five Years?

The historic growth rate of the Europe Silicone Rubber market was 4.8% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed