U.S. Scrap Metal Recycling Market Outlook (2025 to 2035)

The U.S. Scrap Metal Recycling market is expected to reach USD 18,472 million by 2035, up from USD 10,284 million in 2024. During the forecast period 2025 to 2035, the industry is projected to expand at a CAGR of 5.5%.

The U.S. scrap metal recycling market is propelled by growing industrial demand for sustainable, cost-effective raw materials, reinforced government incentives, steelmaking electrification, and green initiatives in the automotive and construction sectors.

| Metric | Value |

|---|---|

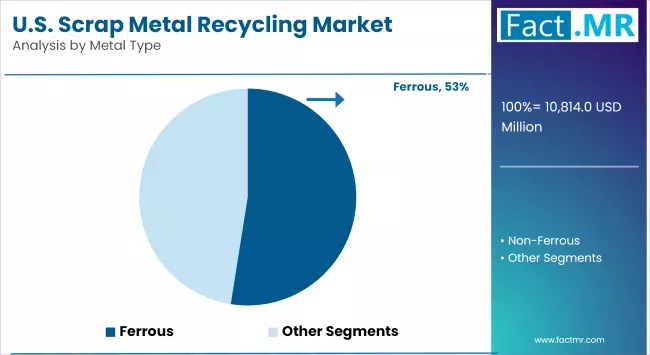

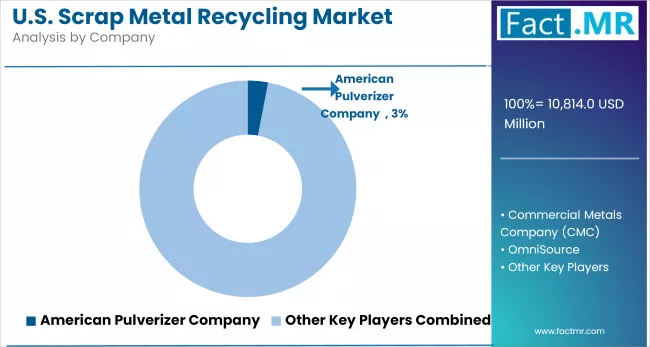

| Estimated Size in 2025 | USD 10,814 Million |

| Projected Size in 2035 | USD 18,472 million |

| CAGR (2025 to 2035) | 5.5% |

What are the drivers of the U.S. Scrap Metal Recycling Market?

The U.S. scrap metal recycling market is advancing steadily due to a combination of regulatory, economic, and environmental factors. The manufacturing industry is shifting towards sustainable production, and recycled metal is an effective and versatile alternative to virgin materials. This transition is particularly evident in steelmaking, where electric arc furnace (EAF) operations are accelerating demand for high-quality ferrous scrap.

The automotive and construction industries continue to be major end-use markets, and the momentum is shifting towards lightweighting, emissions reduction, and green building certification. The incorporation of more recycled aluminum and steel into the supply chains of these industries is being improved to meet environmental objectives and reduce dependence on raw materials.

Additionally, there are policy incentives encouraging recycling infrastructure and extended product liability models at the federal and state levels. These actions are stimulating the investment into high-level sorting equipment and logistics streamlining to increase the level of recovery.

Moreover, the increased demand of consumers and companies for sustainable products is strengthening the emphasis on recycled materials in production. Collectively, these factors are establishing a solid foundation for future prosperity in the U.S. scrap metal recycling sector.

What are the regional trends of the U.S. Scrap Metal Recycling Market?

The market for recycling scrap metal in the United States is experiencing regional growth dynamics driven by the sustainability trend, industrial demand, and infrastructure development. In the West U.S., momentum is building steadily due to progressive environmental agendas and a heightened focus on material recovery. Industrial and municipal operators are adopting advanced recycling technologies to align with circular economy goals and reduce landfill usage and carbon emissions.

The South-west U.S. is also gaining momentum to become substantial, with commercial construction and infrastructure development serving as the driving force. As the price volatility of raw materials increases, industries in this region are investing in an efficient system of metal recovery to enhance cost optimization and sustainability levels.

The Midwest U.S. remains the market’s stronghold, underpinned by a robust manufacturing ecosystem and integration with domestic steel and automotive industries. Its established network of processors and end-users ensures operational efficiency and consistent demand for both ferrous and non-ferrous scrap.

In the Northeast U.S., scrap generation is high due to urban redevelopment and industrial refurbishment. While zero-waste initiatives are reinforcing recycling, facility expansion constraints could moderate growth.

The Southeast U.S. is rapidly scaling its recycling operations, supported by industrial investment, port infrastructure, and low-carbon steel production. A favorable business climate and modern facilities are driving large-scale scrap consumption across the region.

What are the challenges and restraining factors of the U.S. Scrap Metal Recycling Market?

The U.S. scrap metal recycling market is facing several structural challenges that hinder efficiency and long-term scalability. A major concern is the persistent volatility in metal prices, especially steel, copper, and aluminum. Fluctuating commodity prices disrupt planning cycles and discourage capital investment, particularly for mid-sized recyclers that lack the financial capacity to hedge against market swings.

The interest in technological disparity across various facilities also hinders development. Although a few operators have adopted the use of more advanced sorting and shredding facilities, not many have done so. Due to this technology gap, productivity declines, contamination risks rise, and the value of the materials decreases.

Labor shortages also present ongoing difficulties. Skilled workers for dismantling, separation, and machine operation are in short supply. Attracting talent is becoming increasingly difficult due to concerns about workplace safety, limited advancement opportunities, and rising wage demands.

Regulatory compliance adds another layer of complexity. Recyclers must meet stringent environmental standards for emissions, noise, runoff, and material handling. Yet, the absence of cohesive national recycling policies creates regulatory uncertainty and inconsistency across states.

Moreover, the increasing complexity of consumer products, such as electronics and hybrid composites, complicates sorting processes. These new material blends require sophisticated recovery systems, demanding significant capital outlays and long-term technological adaptation to remain economically viable.

Region-Wise Insights

| Region | CAGR (2025 to 2035) |

|---|---|

| Southwest U.S. | 6.6% |

| West U.S. | 6.2% |

| Midwest U.S. | 5.0% |

Clean Energy and Urban Growth Drive Recycling in Southwest U.S.

Scrap metal recycling is gaining significant traction in the Southwest US, fueled by rapid urban development and growing investment in renewable energy. A surge in construction and redevelopment projects is generating a steady flow of recyclable ferrous and non-ferrous metals. At the same time, the region’s expanding solar and wind energy sectors are boosting demand for secondary metals like copper and aluminum, which are critical for clean energy infrastructure.

Supportive policy measures and grant-backed recycling programs are incentivizing processors to upgrade facilities with AI-based sorting and automation, enhancing recovery efficiency. Industrial zones and logistic corridors are optimizing intra-regional scrap flow and export readiness. With both environmental and economic factors aligning, the region is positioning itself as a key player in the national circular economy, balancing infrastructure growth with resource sustainability. The integration of smart technology and supportive regulation continues to accelerate Southwest’s transition toward modernized metal recovery systems.

Policy and Innovation Strengthen Metal Recycling in West U.S.

The West US stands out in the scrap metal recycling landscape due to its strict environmental regulations and rapid adoption of advanced processing technologies. Legislation targeting waste reduction and producer accountability has intensified efforts to recover and repurpose scrap metals across industrial sectors. Facilities in the region are deploying AI-enhanced sorting systems, robotic separation units, and low-emission processing lines to meet stringent recovery benchmarks. High demand for recycled materials in construction, tech manufacturing, and green infrastructure is driving consistent throughput.

Export-oriented ports bolster regional scrap flow to international buyers, adding resilience to market dynamics. Public awareness and business alignment around low-carbon, circular materials further reinforce the recycling ecosystem. With innovation embedded into its policy and operational framework, the West is redefining efficiency and compliance in metal recovery. The region’s leadership continues to influence national standards and shape the evolution of a tech-forward, sustainable recycling industry.

Industry and Infrastructure Fuel Recycling Momentum in Midwest U.S.

The Midwest US is strengthening its role in the national scrap metal recycling market, bolstered by a legacy of manufacturing and a surge in infrastructure investment. Heavy industries in the region continue to generate sizable scrap volumes, particularly from machinery, transportation, and industrial equipment. Current federal infrastructure funding is adding to this flow through projects involving road, bridge, and utility upgrades.

Recycling facilities are undergoing modernization, integrating automated sorting, energy-efficient furnaces, and material tracking systems to boost operational performance. The region’s central location and robust transportation networks facilitate streamlined distribution and processing logistics.

Municipal and industry-led collection programs are enhancing scrap intake, particularly in urban areas. The growing interest in using recycled content for new manufacturing aligns with climate goals and enhances the region’s strategic relevance. As modernization efforts scale, the Midwest is emerging as a key pillar in the US circular economy, merging economic revitalization with sustainable materials management.

Category-Wise Analysis

High-Quality Feedstock and Efficiency Gains Accelerate Ferrous Metal Use

Ferrous metals are gaining renewed momentum in the U.S. scrap recycling industry due to their abundance, cost-effectiveness, and critical role in infrastructure and manufacturing. As steel-intensive sectors such as automotive, construction, and transportation rebound, the demand for ferrous scrap is rising steadily. These metals serve as a reliable feedstock for electric arc furnaces (EAFs), which are gaining popularity due to their lower carbon emissions compared to traditional blast furnaces.

Increased adoption of circular production models by manufacturers is also enhancing the value proposition of ferrous recycling. Innovations in magnetic separation and sensor-based sorting have improved material purity and yield.

Additionally, domestic mills prefer ferrous scrap due to its lower logistics costs and compliance with emission regulations, further fueling its uptake. As the U.S. emphasizes decarbonization in the heavy industry sector, ferrous metals are emerging as a strategic input that supports both industrial growth and sustainability mandates.

Automation and Material Recovery Efficiency Boost Shredding Adoption

Shredding has become a core process in scrap metal recycling, offering scalable and efficient handling of complex, mixed-material inputs. It is especially effective for processing end-of-life vehicles, white goods, and construction waste, breaking down bulky materials into uniform fragments that can be easily sorted and refined. The adoption of high-efficiency, low-speed shredders is helping reduce energy consumption while maintaining high output rates. Facilities are increasingly integrating shredders with advanced downstream separation systems such as magnetic sorters, eddy current separators, and air classifiers to improve metal recovery and purity.

Digital controls and real-time performance monitoring are also enhancing throughput and minimizing downtime. With demand rising for clean, recyclable inputs across automotive, construction, and infrastructure sectors, shredding is a vital enabler of modern recycling operations. Its ability to support high-volume processing while improving material quality makes it a key driver in the scaling of circular manufacturing in the U.S.

EV Shift and Light Weighting Trends Drive Scrap Demand in Automotive

The automotive sector remains a dominant end-user of recycled metals, with scrap playing a central role in enabling cost and sustainability goals across the supply chain. With automakers under pressure to reduce emissions and embrace circular practices, recycled ferrous and non-ferrous metals are being increasingly integrated into vehicle manufacturing. Aluminum and high-strength steel are especially in demand due to their use in electric vehicles (EVs), which prioritize lightweight construction.

Automakers are also collaborating with recyclers to recover production scrap and end-of-life vehicle components, boosting the role of closed-loop systems. Furthermore, upcoming federal vehicle efficiency and recycling regulations are incentivizing the use of secondary materials. Advances in metal separation technologies are ensuring automotive-grade purity from scrap inputs, supporting their direct use in the body, chassis, and structural components. As vehicle platforms transition toward electrification and sustainability, the automotive sector will remain a cornerstone of U.S. scrap metal consumption.

Competitive Analysis

Key players in the U.S. scrap metal recycling industry include American Pulverizer Company, Commercial Metals Company (CMC), OmniSource, Metal Management Inc., Tube City Inc., Philip Metals, Hugo Neu, Sims Metal (formerly Simsmetal), Samuel Recycling, and DBW Metals Recycling.

The scrap metal recycling market is growing due to the rising demand for sustainable raw materials in the automotive, construction, and industrial sectors. Increasing environmental regulations and focus on circular economy models are driving operational shifts.

Technological innovations, such as automated shredding, sensor-based sorting, and AI-driven processing, are enhancing efficiency and purity. Companies are adopting energy-efficient, low-emission systems to boost sustainability. This evolving landscape is encouraging recyclers to enhance their logistics, invest in technology, and establish robust supply partnerships to meet the increasing demands of end-users.

Recent Development

- In March 2025, TOMRA introduced a deep learning-based solution to enhance sorting accuracy in wrought aluminum scrap recycling. Utilizing AI-driven object recognition, the technology enhances purity, boosts recovery, and facilitates low-carbon secondary aluminum production, enabling recyclers to meet the growing demand for sustainable, high-quality metal.

Fact.MR has provided detailed information about the price points of key manufacturers in the U.S. Scrap Metal Recycling Market, positioned across regions, including sales growth, production capacity, and speculative technological expansion, as recently published in the report.

Methodology and Industry Tracking Approach

Fact.MR’s 2025 U.S. scrap metal recycling market report draws from insights provided by 10,200 stakeholders across 30 countries, with at least 280 participants per market. Approximately 58% of responses were gathered from producers and end-users, including scrap yard operators, smelters, and secondary metal manufacturers. The remaining 42% comprised industry professionals, including sustainability advisors, regulatory officers, and supply chain managers. The research was conducted from June 2024 to May 2025, focusing on demand trends, recycling efficiency, capital investments, regulatory shifts, and value chain risks. Data was weighted according to regional recycling volumes and trade activity.

The report is based on an analysis of over 270 sources, including regulatory documents, technical journals, financial statements, and environmental filings. Techniques such as correlation analysis and time-series modeling were applied. Since 2018, Fact.MR has tracked recycling trends, making this a trusted resource for industry participants and policymakers.

Segmentation of U.S. Scrap Metal Recycling Market

-

By Metal Type :

- Ferrous

- Stainless Steel

- Carbon Steel

- Mild Steel

- Cast Iron

- Non-Ferrous

- Aluminum

- Copper

- Lead

- Nickel

- Zinc

- Brass

- Tin

- Gold

- Others

- Ferrous

-

By Scrap :

- New Scrap

- Old Scrap

-

By Recycling Type :

- Shearing

- Shredding

- Bailing

-

By End-User :

- Automotive

- Shipbuilding

- Construction

- Mining

- Railway & Transportation

- Aerospace & Defense

- Oil & Gas

- Heavy Equipment

- Others

-

By Region :

- West U.S.

- Southwest U.S.

- Midwest U.S.

- Northeast U.S.

- Southeast U.S.

- Frequently Asked Questions -

What was the U.S. Scrap Metal Recycling Market Size Reported by Fact.MR for 2025?

The U.S. Scrap Metal Recycling Market was valued at USD 10,814 Million in 2025.

Who are the Major Players Operating in the U.S. Scrap Metal Recycling Market?

Prominent players in the market are American Pulverizer Company, Commercial Metals Company (CMC), OmniSource, Metal Management Inc., among others.

What is the Estimated Valuation of the U.S. Scrap Metal Recycling Market in 2035?

The market is expected to reach a valuation of USD 18,472 million in 2035.

What Value CAGR did the U.S. Scrap Metal Recycling Market Exhibit Over the Last Five Years?

The historic growth rate of the U.S. Scrap Metal Recycling Market was 4.9% from 2020 to 2024.

Author:

Shubham Patidar

Editor:

Naved Ahmed