Straddle Carriers Market Outlook (2025 to 2035)

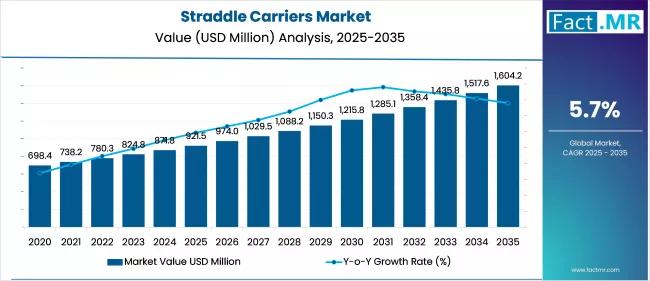

The global straddle carriers market is projected to increase from USD 921.5 million in 2025 to USD 1,604.2 million by 2035, with a CAGR of 5.7%, driven by port automation, container traffic expansion, and the demand for more flexible and efficient container handling systems. The emphasis on faster turnaround times and minimal human intervention in maritime logistics is driving the global business.

What are the Key Drivers of the Straddle Carriers Market?

Port authorities and terminal operators are increasingly adopting straddle carriers to meet the rising demand for efficient container handling operations. As global maritime trade continues to expand, the number of container movements in major seaports has increased significantly, resulting in logistical bottlenecks. Straddle carriers offer flexibility by allowing containers to be stacked and unstacked independently, eliminating the need for additional lifting equipment and thereby reducing dwell time and improving port throughput.

Technological advancements, particularly in electric and hybrid straddle carriers, have improved energy efficiency, reduced emissions, and lowered operational costs. Automation and integration with terminal operating systems (TOS) are enhancing safety, accuracy, and labor optimization. These innovations enable better fleet management and predictive maintenance, particularly in large-scale terminals across Europe and Asia.

Moreover, rising investments in smart ports, such as those in Rotterdam, Singapore, and Shanghai, are further encouraging the adoption of automated and semi-automated straddle carriers. Government-led initiatives to reduce carbon footprints and promote electrification in heavy-duty vehicles provide additional tailwinds to the market.

What are the Regional Trends in the Straddle Carriers Market?

Asia Pacific remains the dominant region, driven by container traffic in China, India, South Korea, and Southeast Asia. China’s major ports, such as Shanghai, Ningbo-Zhoushan, and Shenzhen, are aggressively adopting automation and smart port technologies, supporting the uptake of straddle carriers. India’s Sagarmala project, along with the increasing use of public-private partnerships in port development, further contributes to regional growth. Japan and Singapore continue to invest in electric and autonomous straddle carrier fleets as part of decarbonization roadmaps.

Europe holds the second-largest share, particularly in countries with highly automated container terminals. Ports in Germany, the Netherlands, and Belgium have heavily invested in semi-automated terminals that rely on straddle carriers for yard operations. For example, the Port of Rotterdam's Maasvlakte terminal employs a fleet of automated electric straddle carriers. EU policies supporting the clean energy transition in logistics also incentivize the integration of electric vehicles in port operations.

North America shows steady growth, led by port modernization programs in the U.S. and Canada. Ports such as Long Beach, Los Angeles, and Vancouver are retrofitting and expanding their container yards, creating opportunities for straddle carriers. The growing demand for e-commerce and inland transportation further pressures port authorities to enhance efficiency, favoring the use of straddle carriers.

In the Middle East & Africa, rising transshipment activities in the UAE, South Africa, and Morocco support infrastructure development. Although adoption remains lower compared to other regions, ongoing port expansion projects suggest future growth straddle carriers market.

What are the Challenges and Restraining Factors in the Straddle Carriers Market?

A key challenge lies in the high capital investment required for acquiring and maintaining straddle carrier fleets. Advanced units, especially those integrated with autonomous features and electric drivetrains, require significant upfront investment, which may deter smaller ports from adoption.

Additionally, maintenance and technical complexity remain ongoing challenges. Straddle carriers undergo heavy-duty, continuous operations, requiring specialized upkeep to ensure reliability. Any mechanical downtime can significantly disrupt container flow and reduce profitability, particularly in busy terminals. The situation is further strained by a lack of skilled operators and technicians, making it difficult to maintain consistent performance and uptime.

Another restraint is the limited standardization across ports, which creates integration issues when deploying new or upgraded systems. Furthermore, the slow pace of electrification in emerging markets, largely due to a lack of charging infrastructure, also limits the adoption of electric straddle carriers. Environmental regulations may also complicate the deployment of diesel-powered carriers, forcing ports to shift to cleaner alternatives sooner than expected.

Country-Wise Outlook

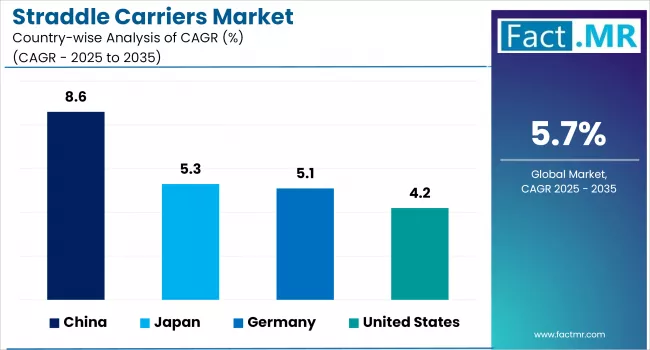

China Focuses on Port Automation and Electric Straddle Carriers

China leads the global straddle carriers market in terms of deployment volume and technological innovation. Major container ports such as Shanghai and Ningbo-Zhoushan handle high volumes and require efficient container stacking and retrieval systems. Straddle carriers are increasingly integrated with China's smart port infrastructure, supported by the country's 14th Five-Year Plan, which focuses on logistics automation and emissions reduction.

China's homegrown companies, including SANY and ZPMC, are producing electric and hybrid straddle carriers, which align with national objectives to phase out diesel engines in heavy-duty port equipment. In 2024, the Port of Tianjin announced full electrification of its container yard vehicles, many of which are straddle carriers. Moreover, government-backed R&D funding supports the development of autonomous mobility solutions in port settings.

Germany Champions Semi-Automated Terminals and Low-Emission Equipment

Germany has established itself as a key European hub for advanced container handling systems. The Port of Hamburg and Wilhelmshaven are known for their semi-automated terminals, where straddle carriers serve as core yard transportation systems. Most of the fleet in these ports is semi-autonomous and powered by low-emission diesel-electric or fully electric drives.

With Germany's strong focus on green logistics and digital transformation, the use of straddle carriers is reinforced by subsidies for clean port equipment. German firms such as Terex Port Solutions and Könecranes provide tailored carrier systems with high precision and energy efficiency. The country's strict emissions laws ensure rapid electrification and smart monitoring integration across container terminals.

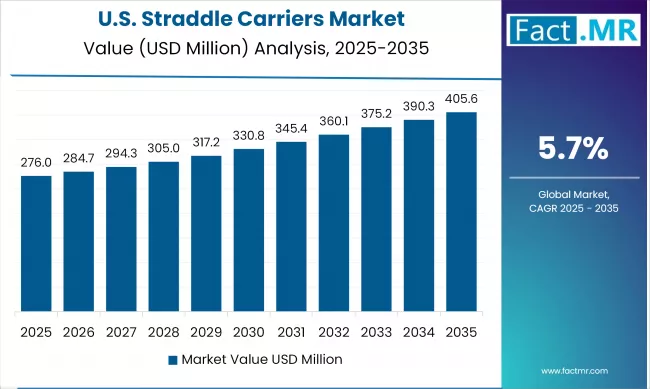

The U.S. Ramps Up Modernization to Tackle Port Congestion

The U.S. straddle carriers market is seeing renewed interest due to infrastructure revitalization efforts and persistent port congestion, particularly on the West Coast. Ports of Los Angeles and Long Beach are enhancing their yard automation capabilities with modern container-handling fleets, including hybrid and electric straddle carriers.

Straddle carriers that can be deployed without reconfiguring terminals are favored due to space constraints in older U.S. ports. Companies such as Taylor Machine Works and Konecranes have increased their presence in U.S. projects with scalable, low-emission solutions.

Category-wise Analysis

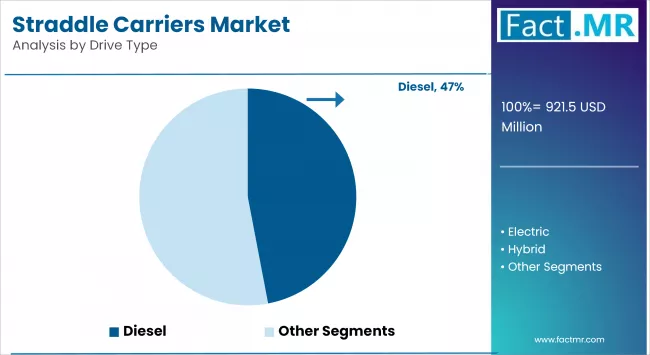

Diesel-Powered to Exhibit Leading by Drive Type

Diesel-powered straddle carriers continue to dominate the global market, particularly in developing ports and terminals with limited access to electric infrastructure. These machines offer high horsepower and operational efficiency, making them suitable for medium- to heavy-duty lifting in container handling and transport applications. Their robust performance, coupled with a long lifespan and ease of maintenance, makes them ideal for port operators seeking proven, conventional systems with minimal technological dependency.

Several terminals in Southeast Asia, Africa, and Latin America rely on diesel-powered equipment due to the lack of reliable electric grid connectivity or high initial cost of transitioning to hybrid or electric models. In these regions, diesel variants offer cost advantages over time due to widespread service availability and established operator familiarity. Moreover, diesel models provide extended operational range, especially critical for terminals handling large cargo volumes without interruptions for recharging or refueling.

However, with increasing pressure on ports to reduce emissions, manufacturers are improving diesel technologies by integrating cleaner-burning engines, improved fuel injection systems, and particulate filter technologies to make these machines more compliant with environmental standards. While demand may gradually shift to greener alternatives, diesel straddle carriers will maintain relevance, particularly in transitional economies and retrofitted hybrid configurations.

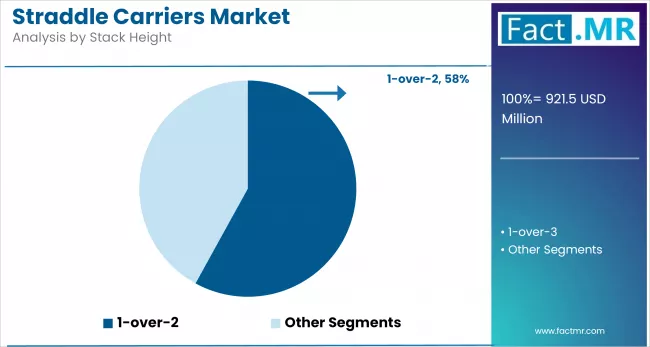

1-Over-2 Straddle Carriers to Exhibit leading by Stack Height

1-over-2 straddle carriers dominate the market, primarily due to their widespread use at small to mid-sized terminals and facilities where moderate stacking height meets operational needs without incurring excessive infrastructure costs. These carriers offer a good balance between cost, operational efficiency, and maneuverability, making them highly preferred in ports with space constraints.

1-over-3 straddle carriers are gaining traction in high-density terminals where maximizing vertical space is critical. These carriers allow for greater stacking, improving yard storage capacity. Although they require more robust infrastructure and are costlier, their growing adoption in major global ports reflects a trend towards higher productivity in container handling.

Container Stacking to Exhibit Leading by Application

Container stacking holds the largest market share, as it is the primary function of straddle carriers in port operations. Their ability to stack containers efficiently without relying on cranes makes them essential for quick turnaround times and optimized yard usage.

Intermodal terminal operations, on the other hand, represent a significant growth segment. As global trade increasingly relies on multimodal logistics, straddle carriers are becoming integral in efficiently transferring containers between different transport modes. Their mobility and versatility make them ideal for these dynamic, space-sensitive environments.

Port Terminals to Exhibit Leading by End-Use

Port terminals are the dominant segment, driven by the ever-increasing volume of international maritime trade. Straddle carriers at ports enable quick and efficient container movement from vessels to yards, supporting high throughput and minimizing dwell times.

Inland Container Depots (ICDs) are witnessing steady adoption of straddle carriers due to the need for efficient inland logistics infrastructure. As trade corridors expand and the focus on decongesting coastal ports intensifies, ICDs are playing a bigger role, prompting investment in advanced material handling equipment like straddle carriers.

Competitive Analysis

The straddle carriers market is becoming moderately competitive, with major players emphasizing innovation, geographic expansion, and after-sales support. Leading manufacturers, such as Kalmar (Cargotec Corporation), Konecranes, Terex Port Solutions, Liebherr, and SANY Group, dominate due to their comprehensive product portfolios and global service networks.

Technological advancements form a critical competitive lever. Players invest in electrification, autonomous navigation systems, and fleet management platforms to differentiate their offerings. Kalmar, for instance, offers its AutoStrad™ platform, combining automated carriers with cloud-based control systems. Konecranes provides ECO straddle carriers with advanced fuel-saving features and connectivity.

Regional customization and compliance with emission norms influence OEM market penetration. Local players in China and India, such as ZPMC and TIL Limited, focus on cost-effective diesel variants for domestic ports. Aftermarket services, leasing programs, and lifecycle management are crucial for maintaining customer loyalty.

Recent strategic collaborations have centered on automation and data-driven operations. In 2024, Konecranes and Microsoft Azure partnered to enhance smart fleet diagnostics. Kalmar launched a retrofit automation package for existing carriers, targeting terminal upgrades in budget-conscious ports.

Recent Developments

- In May 2024, Kalmar unveiled a new all-electric straddle carrier model featuring enhanced regenerative braking technology, which reduces energy consumption by 23% compared to the previous generation.

- In March 2024, Konecranes secured a significant order from the Port of Antwerp, Belgium, for 20 hybrid straddle carriers. These advanced machines are designed to combine diesel and electric power, offering substantial reductions in fuel consumption and emissions compared to conventional diesel-only models.

Segmentation of the Straddle Carriers Market

-

By Drive Type :

- Diesel

- Electric

- Hybrid

-

By Stack Height :

- 1-over-2

- 1-over-3

-

By Application :

- Container Stacking

- Container Transport

- Intermodal Terminals

-

By End-Use :

- Port Terminals

- Intermodal Yards

- Inland Container Depots (ICDs)

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the global market size of the straddle carriers market in 2025?

The global straddle carriers market is valued at USD 921.5 million in 2025.

Who are the major players operating in the global straddle carriers market?

Prominent players in the market include Kalmar, Konecranes, Terex Port Solutions, Liebherr, SANY, and ZPMC.

What is the estimated valuation of the straddle carriers market by 2035?

The market is expected to reach a valuation of USD 1,604.2 million.

What value CAGR is the straddle carriers market exhibit over the last five years?

The historic growth rate of the straddle carriers market was 5.7% from 2020 to 2024.

Author:

Shubham Patidar

Editor:

Naved Ahmed