Functional Coil Coatings Market Outlook (2025 to 2035)

The functional coil coatings market will be valued at USD 7.38 billion by 2025. As per Fact.MR's analysis, functional coil coatings will grow at a CAGR of 4.71% and reach USD 11.58 billion by 2035.

In 2024, the building and construction industry continued to be a major customer, with impressive growth in commercial and residential buildings. Urbanization and infrastructure development, especially in developing economies, caused increased demand for long-lasting and attractive building materials.

Coil coatings found wide applications in roofing, cladding, and insulation, improving the durability and energy efficiency of buildings. Likewise, the automotive industry also experienced strong growth in the adoption of automotive coatings, promoted by the desire for lightweight materials with corrosion-resistant properties.

As the electric vehicle industry share rose, producers concentrated on coatings providing superior performance together with sustainability-friendly alignment.

Ahead to 2025 and beyond, a number of trends will dominate the industry. Sustainability continues to be a top priority, with a growing demand for environmentally friendly coatings with low VOC emissions.

Regulatory forces and consumer demands are forcing the development of water-based and bio-based coatings, lowering environmental impact without sacrificing performance.

In addition, the Asia-Pacific landscape is also set to achieve significant expansion as a result of fast-paced industrialization and urbanization, where nations such as China and India are heavily investing in infrastructure development, creating increased demand for use in construction and automotive sectors.

Key Metrics

| Metrics | Values |

|---|---|

| Industry Size (2025E) | USD 7.38 billion |

| Industry Value (2035F) | USD 11.58 billion |

| Value-based CAGR (2025 to 2035) | 4.71% |

Fact.MR Survey on Functional Coil Coatings Industry

Fact.MR Survey Findings: Trends According to Stakeholder Insights

(Surveyed Q4 2024, n=500 stakeholder respondents evenly split between manufacturers, distributors, construction companies, and automotive suppliers in the US, Western Europe, China, and Japan.)

Stakeholder Top Priorities

Environmental Compliance:

84% of stakeholders worldwide named compliance with VOC and hazardous air pollutant (HAP) regulations as a "critical" priority.

Durability & Corrosion Resistance:

78% pointed to the demand for highly durable and anti-corrosion coatings, especially in humid or heavy-traffic applications.

Regional Variance:

- US: 67% cited energy-efficient, reflective coatings for commercial and residential roofs, versus 45% in China.

- Western Europe: 86% cited low-carbon and bio-based coatings because of stringent sustainability policies, compared to 52% in the US.

- China/Japan: 64% highlighted high-performance coatings to withstand extreme weather, particularly in typhoon-sensitive and industrially intensive regions, as compared to 29% in the US.

Adoption of Advanced Technologies

High Variance:

- US: 61% of building companies utilized self-healing and anti-bacterial coatings, mainly in the healthcare and food processing industries.

- Western Europe: 54% incorporated smart coatings with self-cleaning and air-purifying capabilities, Germany being at 65%.

- China: 39% of companies implemented nano-ceramic functional coatings for added weather resistance.

- Japan: Just 25% utilized next-generation smart coatings, blaming high expense and traditional formula preference.

Convergent and Divergent ROI Views:

74% of US stakeholders found automation in coil coating application "worth the investment."

Japan trailed, with 41% continuing to use traditional solvent-based coatings because of budget limitations.

Material & Coating Type Preferences

Consensus

PVDF-based coatings: Chosen by 66% globally for their excellent weather ability and chemical resistance, particularly in construction and automotive applications.

Regional Variance:

- Western Europe: 55% used water-based coil coatings, versus 34% globally, due to EU emissions regulations.

- China/Japan: 43% opted for hybrid silicone-polyester coatings as the balance of performance and price, particularly in industrial use.

- US: 72% remained with PVDF coatings, though Midwest producers experienced a 22% move toward water-based options for regulatory conformity.

Price Sensitivity & Cost Challenges

Shared Challenges:

90% mentioned increasing costs of materials (aluminum rose by 28%, specialty polymers by 21%) as a severe challenge.

Regional Differences:

- US/Western Europe: 64% were ready to pay a 10–20% premium for high-end coatings with self-healing or high UV resistance benefits.

- China/Japan: 79% had a preference for low-cost, high-volume production models (

- China: 47% of respondents favored leasing or bulk purchase models to manage costs, compared to 19% in the US.

Pain Points in the Value Chain

Manufacturers:

- US: 58% experienced supply chain disruptions in specialty resins due to geopolitical trade restrictions.

- Western Europe: 49% mentioned regulatory complexity (e.g., REACH compliance).

- China: 63% encountered overcapacity, resulting in price competition and thinner margins.

Distributors:

- US: 71% experienced delays in raw material imports, especially for fluoropolymers.

- Western Europe: 56% experienced competitive pressure from low-cost Asian imports.

- Japan: 60% were challenged by insufficient domestic production capacity for high-end functional coatings.

End-Users (Construction & Automotive Companies):

- US: 46% mentioned "high reapplication costs" due to rising durability expectations.

- Western Europe: 41% experienced challenges in retrofitting older infrastructure to meet new coil coating requirements.

- China: 53% experienced insufficient technical support for high-end, imported coil coatings.

Future Investment Priorities Alignment

76% of world manufacturers intend to invest in water-based and bio-based R&D for future-generation coatings.

Divergence:

- US: 63% emphasized high-durability coatings for harsh weather conditions.

- Western Europe: 59% targeted carbon-neutral production processes, e.g., low-VOC coatings.

- China/Japan: 51% targeted cost-efficient hybrid coatings with a balance of performance and price.

Regulatory Impact on Growth

- US: 69% of respondents mentioned state-level emissions regulations (e.g., California's more stringent VOC limits) as "highly disruptive."

- Western Europe: 83% viewed the EU's Green Deal and Circular Economy Plan as a driver of growth for sustainable products.

- China/Japan: 35% alone saw regulations having a significant influence on purchase decisions, citing lower enforcement and weaker compliance costs.

Conclusion: Variance vs. Consensus

High Consensus:

Green compliance, durability, and cost pressures are worldwide concerns.

Increased material costs are a universal challenge worldwide.

Key Variances:

- US: Spending on high-performance, automation-linked coil coatings.

- Western Europe: Ahead on sustainability, prioritizing bio- and water-based coatings.

- China/Japan: Cost-focused, with hybrid coatings preferred to expensive formulations.

Strategic Insight:

Regionalization (e.g., water-based in Europe, PVDF in the US, cheaper hybrids in Asia) is important for penetration in the industry.

Government Regulations on the Functional Coil Coatings Industry

| Country/Region | Regulatory Impact & Mandatory Certifications |

|---|---|

| U.S. | VOC Emission Regulations: The U.S. Environmental Protection Agency (EPA) enforces strict limits on volatile organic compound (VOC) emissions under the Clean Air Act. California’s CARB Regulations: California Air Resources Board (CARB) has stricter VOC limits than federal regulations, impacting solvent-based coil coatings. LEED Certification: The Leadership in Energy and Environmental Design (LEED) rating system encourages the use of low-VOC and sustainable coatings in construction projects. ASTM Standards: ASTM D4145 (coating flexibility), ASTM D2244 (color retention), and ASTM D4214 (chalk resistance) are widely followed in the industry. |

| Western Europe | EU REACH Compliance: The Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH) regulation mandates safety assessments of chemicals used in coil coatings. EU Green Deal: Aims to make Europe carbon-neutral by 2050, pushing for bio-based and water-based coatings. Ecolabel Certification: The EU Ecolabel certifies coatings with low environmental impact, limiting hazardous substances. CE Marking: Mandatory for coil coatings used in construction and infrastructure projects to ensure quality and environmental compliance. BREEAM Certification: A sustainability certification for buildings that promotes eco-friendly coatings. |

| China | New VOC Regulations (GB 33372-2020): Introduced in 2020, limits solvent-based coatings to reduce air pollution. "Made in China 2025" Policy: Encourages local companies to develop high-performance, sustainable coil coatings. CCC Certification (China Compulsory Certification): Required for coatings used in automotive and industrial applications. Environmental Protection Tax: High-VOC coatings are subject to higher taxation, promoting the shift to water-based coatings. |

| Japan | Japan Industrial Standards (JIS K 5675): Sets performance and safety criteria for functional coatings. Low-VOC Regulations: While not as strict as the EU or US, Japan has introduced policies promoting low-VOC and solvent-free coatings. Eco-Mark Certification: A voluntary but widely recognized eco-label for sustainable and non-toxic coatings. Building Standard Law: Encourages the use of fire-retardant and anti-corrosion coatings in construction projects. |

| South Korea | Air Quality Control Act: Imposes VOC emission limits on coatings used in construction and automotive industries. KS Certification (Korean Standards): Required for coil coatings used in infrastructure and public projects. Green Certification Program: This program offers government incentives for companies producing low-VOC, eco-friendly coatings. Industry-Specific Regulations: Automotive and electronics manufacturers are shifting towards high-performance, corrosion-resistant coatings due to export compliance with EU/US standards. |

Market Analysis

The industry is transitioning towards high-performance, sustainable solutions due to increasingly stringent environmental legislation and increased demand for energy-efficient, durable coatings in the automotive and construction industries.

Bio-based and water-based coatings are emerging as governments globally enforce stricter VOC and hazardous emissions regulations, encouraging manufacturers to become more innovative.

Firms venturing into environment-friendly formulations and next-generation coating technologies have the potential to gain, while those dependent on conventional solvent-based coatings will lose industry shares because of the increasing cost of compliance and government pressures.

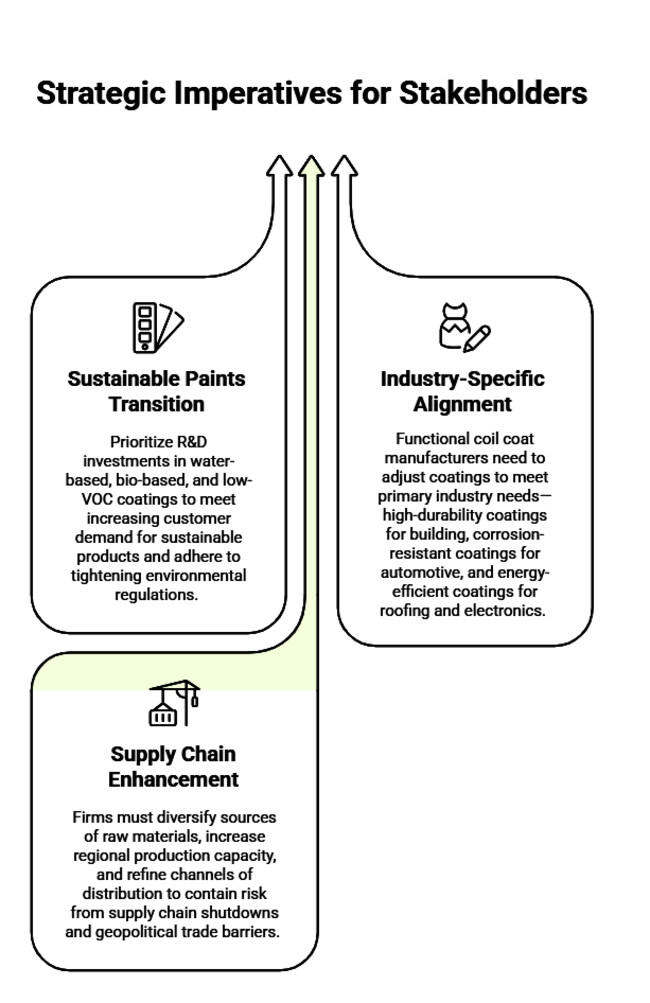

Top 3 Strategic Imperatives for Stakeholders

Speed Up Transition to Sustainable Paints

Executives should prioritize R&D investments in water-based, bio-based, and low-VOC coatings to meet increasing customer demand for sustainable products and adhere to tightening environmental regulations. Strategic alliances with chemical innovators and regulation agencies can accelerate product approval and access.

Align Product Offerings with Industry-Specific Needs

Functional coil coat manufacturers need to adjust coatings to meet primary industry needs-high-durability coatings for building, corrosion-resistant coatings for automotive, and energy-efficient coatings for roofing and electronics. OEM and infrastructure developer partnering ensures meeting changing performance and sustainability requirements.

Enhance Global Supply Chain & Distribution Networks

Firms must diversify sources of raw materials, increase regional production capacity, and refine channels of distribution to contain risk from supply chain shutdowns and geopolitical trade barriers. Entry into strategic partnerships with regional distributors and investment in localized manufacturing can improve saturation and cost savings.

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability/Impact |

|---|---|

| Regulatory Uncertainty & Compliance Costs - Stricter environmental laws (VOC limits, hazardous chemical bans) could increase production costs and force rapid reformulation of coatings. | High |

| Raw Material Price Volatility & Supply Chain Disruptions - Fluctuations in prices of key raw materials (resins, pigments, solvents) and geopolitical instability could strain profitability and delay production. | Medium-High |

| Slow Adoption of Sustainable Coatings in Emerging - While developed industries push for eco-friendly coatings, emerging economies may lag due to cost concerns and regulatory laxity. | Medium |

Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Sustainability Compliance & Innovation | Accelerate R&D on low-VOC, water-based, and bio-based coatings to meet upcoming regulatory deadlines in the U.S., EU, and China. |

| Supply Chain Resilience | Secure alternative raw material suppliers and establish regional production hubs to mitigate risks from geopolitical instability and price fluctuations. |

| Penetration in Emerging Economies | Develop a localized pricing and product strategy to drive the adoption of eco-friendly coatings in cost-sensitive areas such as India and Southeast Asia. |

For the Boardroom

To stay ahead, companies need to remain ahead of the changing market conditions. The company will need to double down on sustainable innovation, lock down its supply chain, and customize industry strategies for local growth.

As VOC and emissions regulations tighten, short-term investments in water-based and bio-based formulations will be essential to long-term compliance and competitive positioning. Diversifying suppliers and local production bases will reduce cost volatility and geopolitical risk.

Also, tapping the emerging demand necessitates a localized pricing policy and strategic collaborations with regional OEMs. The roadmap is now to transition from reactive compliance to proactive leadership such that the company leads the transformation to next-generation coatings and does not end up being adapted to.

Segment-wise Analysis

By Technology

Solvent-based coatings are the most universally utilized in the functional coil coatings industry because of their better durability, adhesion, and resistance to severe environmental conditions. These coatings work very effectively in construction, automotive, and industrial manufacturing industries, where long-term protection against corrosion, UV exposure, and chemicals is crucial.

Even with their dominance, strict VOC emission mandates are driving manufacturers toward water-borne and powder coatings that have a lower environmental footprint. These newer technologies offer enhanced sustainability by reducing solvent content, making them more compliant with increasingly stringent environmental regulations and promoting greener manufacturing processes.

By Product Type

Primers are used most extensively in the functional coil coatings industry because of their critical function of providing strong adhesion between the substrate (e.g., metal) and the topcoat. Primers are formulated to improve the corrosion resistance of the underlying material, offering a protective base coat that enhances the durability and lifespan of the coating system.

They are particularly crucial in sectors such as automotive, construction, and industrial manufacturing, where corrosion resistance is a paramount concern. In addition to corrosion protection, primers also improve the overall performance of the coating by enhancing resistance to chemicals, UV degradation, and environmental wear.

By Material

Among all the types of coatings, Polyester and PVDF (Polyvinylidene Fluoride) are used most extensively in the functional coil coatings industry. Polyester is widely used because of its affordability, great durability, and resistance to UV degradation, making it the best for use in construction, roofing, and cladding applications. They provide good flexibility and attractive finishes with a broad spectrum of colors, hence, they control the market in these industries.

Alternatively, PVDF coatings are in great demand in high-performance applications like architectural facades and automotive coatings because of their outstanding corrosion resistance, weatherability, and chemical resistance. PVDF coatings, though more costly, are especially preferred for exterior use where high long-term durability and resistance to extreme conditions are essential.

By Application

Steel coatings outnumber aluminum coatings in the functional coil coatings industry because they are stronger, more durable, and more cost-efficient. Steel is a stronger material and thus is the best for heavy-duty use in industries such as construction, automotive, and industrial manufacturing, where there is the need for high resistance to corrosion, wear, and impact.

Steel coating offers greater protection, particularly in high-traffic, severe environments, and for this reason is widely applied to roofing, cladding, and load-bearing components. Aluminum coatings, by contrast, are prized for being light and corrosion-resistant but are generally reserved for more specialized uses like architectural facades and light-duty automotive components.

By End-Use

Coatings for transportation use, especially auto and aerospace coating, are utilized most extensively over consumer appliance coatings such as air conditioners, refrigerators, and HVACs. Automotive coating demand is pushed by the demand for durability, corrosion resistance, and cosmetic appearance in vehicles where coatings not only safeguard metal parts from extreme weather conditions but also give a satisfactory appearance.

Moreover, braking, suspension, and transmission parts in the transport industry need coatings that deliver high-performance endurance against harsh conditions, including high friction or temperature cycling.

Country-wise Analysis

U.S.

The size of the U.S. industry is expected to grow at a CAGR of 5.5% during the period 2025-2035 due to the large industrial base of the country and stringent environment regulations. In the construction sector and automotive segment, the application of high-quality, long-lasting coatings for corrosion protection, along with their pleasing finishes, are especially in high demand. The shift toward green coatings, such as water-based and bio-based solutions, is also becoming increasingly popular due to increasing environmental pressure and regulatory drivers.

UK

The U.K. industry will increase at a CAGR of 4.8% during the period 2025-2035, driven by the increasing demand for green, eco-friendly coating products owing to tougher environmental regulations.

The U.K. is committed to reducing carbon emissions and promoting circular economy principles, which has stimulated the transition to bio-based and water-borne coatings in various industries, including construction and automotive. The construction sector is a significant consumer, especially in commercial and residential buildings, where coil coatings are utilized on roofing, cladding, and insulation applications.

France

The industry in France is expected to expand at a CAGR of 4.5% in the next decade, aided by growing demand for sustainable coatings based on regulatory frameworks such as the French Environment and Energy Management Agency (ADEME) and the EU's Green Deal.

The country's heavy investment in renewable energy equipment, such as solar panels and green buildings, will stimulate the demand for sustainable and durable coatings for building applications.

The automotive industry, which is undergoing a shift towards electric vehicles (EVs), is another huge opportunity for coatings with high performance, especially corrosion protection and lightness.

Germany

Germany's industry will expand the most in Europe, at a CAGR of 5.7% from 2025 to 2035. The expansion is led by the country's industrial base, including automotive, construction, and manufacturing sectors. Germany is famous for its automobile sector, and it is gradually shifting toward electric vehicles and eco-friendly manufacturing processes.

This is generating demand for high-performance coil coatings with excellent corrosion resistance, durability, and appearance. Sustainability leadership is another important factor, with the government continuously imposing strict environmental regulations on VOC emissions and toxic chemicals.

Italy

Italy's functional coil coating industry will register a CAGR of 4.2% between 2025 and 2035, with the construction and automotive industries maintaining constant demand.

Italy's automotive industry keeps on increasing, particularly with an increased focus on the production of electric vehicles, wherein advanced, durable coatings for light parts and protection from corrosion are needed.

Italy's construction industry, also with tremendous importance given to aesthetics in design and energy efficiency, also fuels demand for high-performance coatings used in roof coverings, exterior cladding, and insulation.

South Korea

South Korea's industry is likely to achieve a CAGR of 4.0% between 2025 and 2035 because of the strong industrial production in the nation in the manufacturing of electronics and automobiles.

South Korea's automotive sector, particularly electric vehicle production, is evolving fast, and hence, corrosion-resistant, high-performance coatings are required.

The construction sector also fuels growth, especially in urban infrastructure projects, where functional coil coatings are used in roofing, cladding, and insulation.

Japan

The Japanese economy will develop at a CAGR of 3.8% from 2025 to 2035 on the back of demand from the automotive and construction sectors. The auto sector of Japan, particularly in electric vehicle (EV) production, is one of the largest consumers of high-performance coatings due to its need for materials that are corrosion-resistant as well as light in weight. The building sector in Japan is also increasingly looking at sustainability and energy efficiency, hence the need for green coil coatings.

China

The industry of China will expand at a CAGR of 6.2% during 2025-2035, driven by its enormous industrial base and urbanization. Construction and automotive industries in China are strong demand drivers, with the nation placing a strong focus on energy-efficient, green construction methods and electric vehicle production.

The application of high-tech, corrosion-resistant coatings in the construction sector is gaining popularity as China continues to expand its infrastructure and real estate activities. Similarly, the automotive sector, particularly with the growing electric vehicle sector, requires lightweight yet resilient coatings for metal parts.

Industry Share Analysis

AkzoNobel N.V.

Share: ~23-25%

AkzoNobel is a world leader in the industry, with a wide range of coatings solutions addressing critical industries like automotive, construction, and industrial use. Renowned for manufacturing high-performance, long-lasting coatings, AkzoNobel's offerings are widely utilized in steel and aluminum applications, especially in buildings, appliances, and transportation. The firm is strategically placed to leverage the increasing momentum toward sustainability and product innovation.

PPG Industries, Inc.

Share: ~20-22%

PPG Industries is a leader in the global business, known for its array of high-performance coatings aimed primarily at the construction, automotive, and consumer appliance industries. PPG stands out for its unparalleled durability, corrosion resistance, and beauty in coatings, rendering its products highly appealing to high-end, finish-oriented industries.

BASF SE

Share: ~15-17%

As the largest chemical company in the world, BASF enjoys a leadership position in the products segment. BASF provides a diverse portfolio of products for the automotive, construction, and consumer industries, with a strong emphasis on developing sustainable solutions. The company’s leadership in green functional coatings has positioned it well in an environment where customers increasingly seek to reduce environmental footprints. BASF’s wide-ranging research and development has led to the creation of bio-based and waterborne coatings that meet strict VOC requirements.

Sherwin-Williams

Share: ~10-12%

Sherwin-Williams is a significant player in the global industry, known for its automotive, construction, and industrial coatings. The firm specializes in delivering high-performance solutions that meet demanding durability and environmental requirements. One of Sherwin-Williams' strengths is its dedication to sustainability, with a strong emphasis on creating low-emission coatings for commercial and residential industries.

Henkel AG & Co. KGaA

Share: ~8-10%

Henkel, with its strong 8-10% share, is a prominent player in the industry, offering a portfolio of products mainly for the automotive, appliance, and construction industries. The company’s focus on sustainable development, along with continued innovation on low-VOC and waterborne products that meet demanding regulatory requirements, solidifies its position in the market.

Key Players

- ALCEA

- ARCEO Engineering

- Axalta Coating Systems

- Becker Group

- Chemetall Group

- Dura Coat Products, Inc.

- Eastman Chemical Company

- Henkel AG & Co. KGaA

- Huhoco GmbH

- Italcoat S.r.l.

- Jotun Group

- Kansai Paint Co. Ltd.

- kömmerling chemische fabrik gmbh

- Lampre srl

- Lord Corporation

- Nipsea Group (Nippon Paint)

- NOROOS CO., LTD

- PPG Industries

- Recubrimientos Plasticos SA

- Salchi Metal Coats S.r.l

- The Chemours Company

- The Valspar Corporation

- Titan Coatings, Inc

- Unichem

Segmentation

By Technology

With respect to the technology, it is classified into liquid coating, waterborne, solvent-based, and powder coating.

By Product Type

In terms of product type, it is divided into top coats, primers, backing coats, and others.

By Material

In terms of material, it is divided into polyester, epoxy, vinyl, plastisols, acrylic, PVDF, and polyurethane.

By Application

In terms of application, it is divided into steel coating and aluminum coating.

By End-Use

In terms of end-use, it is divided into transportation, braking & suspension, transmission, consumer appliances, refrigerators, air conditioners, and HVAC.

By Region

In terms of region, it is segmented into North America, Latin America, Europe, East Asia, South Asia, Oceania, and MEA.

- Frequently Asked Questions -

How big is the functional coil coatings industry?

The industry is anticipated to reach USD 7.38 billion in 2025.

What is the outlook on functional coil coating sales?

The industry is predicted to reach a size of USD 11.58 billion by 2035.

Who are the key functional coil coating companies?

Prominent players include ALCEA, ARCEO Engineering, Axalta Coating Systems, Becker Group, Chemetall Group, Dura Coat Products, Inc., Eastman Chemical Company, Henkel AG & Co. KGaA, Huhoco GmbH, Italcoat S.r.l., Jotun Group, Kansai Paint Co. Ltd., kömmerling chemische fabrik gmbh, Lampre srl, Lord Corporation, Nipsea Group (Nippon Paint), NOROOS CO., LTD, PPG Industries, Recubrimientos Plasticos SA, Salchi Metal Coats S.r.l, The Chemours Company, The Valspar Corporation, Titan Coatings, Inc, Unichem.

Which technology type of functional coil coating is being widely used?

The solvent-based technology type is widely used.

Which country is likely to witness the fastest growth in the functional coil coatings market?

China, expected to grow at 6.2% CAGR during the study period, is poised for the fastest growth.

Author:

S.N. Jha

Editor:

Naved Ahmed