Infrared Detector Market Outlook (2025 to 2035)

The global infrared detector market is valued at USD 620.27 million in 2025. As per Fact.MR analysis, the infrared detector will grow at a CAGR of 7.7% and reach USD 1302.38 million by 2035.

In 2024, the infrared detector industry experienced tangible growth, largely driven by heightened demand across automotive safety systems, consumer electronics, and industrial automation. Fact.MR analysis found that this growth was underpinned by a surge in thermal imaging applications, especially within surveillance and defense sectors. Manufacturers responded to the uptick in night vision and temperature sensing needs with improved sensor sensitivity and miniaturized components.

In particular, the integration of infrared technology in smartphones and smart home devices expanded noticeably. Additionally, several governments increased infrastructure spending on border security and public safety, which boosted procurement of infrared-based detection systems. These trends set the stage for continued growth.

As 2025 unfolds, the industry is estimated to reach a valuation of USD 620.27 million. This trend will continue with innovations pouring into uncooled thermal detectors and their application in wearable health devices and energy-efficient building systems, according to Fact.MR, the expanding AI role in image processing, will help streamline diagnostics, predictive maintenance, and environmental monitoring further.

Key Metrics

| Metric | Value |

|---|---|

| Estimated Size in 2025 | USD 620.27 Million |

| Projected Size in 2035 | USD 1302.38 Million |

| CAGR (2025 to 2035) | 7.7% |

Fact.MR Survey Results: Industry Dynamics Based on Stakeholder Perspectives

(Surveyed Q4 2024, n=500 stakeholder participants evenly distributed across manufacturers, distributors, automotive, healthcare, and electronics sectors in the USA, Western Europe, Japan, South Korea, and Asia-Pacific)

Key Priorities of Stakeholders

- Adoption of Energy-Efficient Solutions: 80% of stakeholders globally identified the need for energy-efficient thermal sensors as a "critical" priority, driven by rising energy costs and regulatory pressure for sustainable solutions.

- Advanced Performance Capabilities: 72% emphasized the demand for high-performance thermal sensors with improved resolution and sensitivity, particularly in the automotive and healthcare sectors.

- Compliance with Industry Regulations: 68% highlighted the importance of meeting regional regulatory standards, particularly for automotive safety systems and medical diagnostic applications.

Regional Variance:

- USA: 74% of stakeholders prioritized the integration of thermal sensors in ADAS (Advanced Driver Assistance Systems) to meet stringent safety standards.

- Western Europe: 82% focused on compliance with the EU's stringent environmental regulations, particularly in terms of reducing the carbon footprint of thermal sensor technology.

- Asia-Pacific: 65% of manufacturers emphasized the demand for cost-effective models due to price sensitivity in the region's rapidly expanding consumer electronics industry.

Embracing Sophisticated Technologies

High Variance in Technology Adoption

- USA: 60% of automotive stakeholders integrated thermal sensors with AI-driven solutions for better predictive maintenance and safety features.

- Western Europe: 53% of medical equipment manufacturers adopted thermal detection systems with advanced temperature sensing for non-invasive diagnostics.

- Japan: Only 28% of stakeholders used cutting-edge technology, with many still relying on traditional thermal sensors due to cost constraints in smaller-scale operations.

- South Korea: 42% of manufacturers in the electronics sector integrated thermal technology for smart home devices and energy-efficient appliances.

Convergent and Divergent Perspectives on ROI:

- 75% of USA stakeholders viewed advanced AI-enabled thermal systems as a "worthwhile investment" for automotive safety. However, only 38% of stakeholders in Japan and South Korea considered automated solutions as cost-effective, preferring more traditional setups.

Material Preferences

Consensus:

- Metal Alloys: 68% of stakeholders globally preferred using advanced metal alloys, such as titanium and stainless steel, for the housing of thermal sensors, owing to their durability and heat resistance.

Regional Variance:

- Western Europe: 58% of stakeholders selected aluminum for its lightweight properties and recyclability, aligning with the region's sustainability goals.

- Asia-Pacific: 45% favored hybrid designs combining metal and composite materials to strike a balance between cost and durability, particularly in consumer electronics.

- USA: 71% of stakeholders in the automotive industry continued using high-grade metal alloys due to their performance under extreme temperatures. However, some manufacturers have experimented with plastics to reduce weight and cost.

Price Sensitivity & Supply Chain Challenges

Shared Challenges:

- 85% of stakeholders cited rising material costs as a significant issue, with steel prices up 25% and aluminum costs rising by 12% over the past year, impacting profit margins.

Regional Differences:

- USA/Western Europe: 63% of respondents indicated a willingness to pay a 15-25% premium for thermal sensors offering advanced features like AI integration and enhanced durability.

- Asia-Pacific: 72% of respondents preferred cost-effective models under USD 4,000, with 10% willing to invest in premium options.

- South Korea: 50% of manufacturers showed interest in leasing thermal sensor systems as a way to reduce capital expenditure and avoid upfront costs.

Pain Points in the Value Chain

Manufacturers:

- USA: 58% of manufacturers struggled with supply chain delays, particularly in procuring critical components such as thermal sensors and AI chips.

- Western Europe: 45% highlighted challenges related to complying with increasingly complex environmental and safety regulations.

- Asia-Pacific: 62% of manufacturers faced difficulties with maintaining consistent quality control in mass production environments.

Distributors:

- USA: 68% reported difficulties in inventory management due to the unpredictability of demand for thermal sensors, especially in the automotive and healthcare sectors.

- Western Europe: 55% of distributors cited the growing competition from low-cost Asian manufacturers as a threat to their share.

- Asia-Pacific: 48% of distributors noted logistical inefficiencies in transporting thermal sensors across rural and urban regions due to infrastructure limitations.

End-Users (Automotive, Healthcare, Electronics):

- USA: 52% of automotive sector users expressed concerns over the high maintenance costs associated with thermal sensors integrated into ADAS.

- Western Europe: 47% of healthcare users struggled with retrofitting old diagnostic systems with newer thermal detection technology.

- Japan: 60% of electronics sector stakeholders reported a lack of comprehensive support for integrating thermal sensors into emerging smart devices.

Future Investment Priorities

Alignment:

- 78% of global stakeholders plan to increase investment in R&D for AI-enhanced thermal sensors, with a particular focus on improving precision, sensitivity, and integration with IoT systems.

Divergence:

- USA: 64% of stakeholders focused on investing in thermal sensors for autonomous vehicles and advanced driver assistance systems (ADAS).

- Western Europe: 58% prioritized investing in thermal technology for healthcare diagnostics, especially for remote patient monitoring and non-invasive diagnostic tools.

- Asia-Pacific: 53% allocated funds to developing cost-effective thermal sensors for consumer electronics and smart appliances, aiming to tap into the growing demand for smart homes and connected devices.

Regulatory Impact

- USA: 70% of stakeholders viewed compliance with NHTSA (National Highway Traffic Safety Administration) standards for automotive safety as a crucial factor in thermal sensor adoption for ADAS.

- Western Europe: 82% of stakeholders viewed the EU’s “Green Deal” and the “Circular Economy Action Plan” as significant drivers for adopting thermal sensors made from recyclable and sustainable materials in automotive and medical applications.

- Asia-Pacific: Only 38% of stakeholders in Japan and South Korea felt that regional regulations significantly influenced their purchase decisions, despite strong government support for energy-efficient technologies.

Conclusion: Variance vs. Consensus

- High Consensus: The global push for energy-efficient and high-performance thermal sensors is a shared priority, driven by both regulatory pressures and technological advancements.

- Key Variances: USA: Strong emphasis on automotive applications and autonomous driving, with AI and ADAS as major investment areas.

- Western Europe: A focus on healthcare applications, particularly for non-invasive diagnostics, driven by strict environmental regulations.

- Asia-Pacific: A growing demand for cost-effective thermal sensors in consumer electronics, with a significant focus on hybrid technologies to balance cost and performance.

Strategic Insight:

- A "one-size-fits-all" approach will not suffice in the industry. Companies must adapt their product offerings based on regional demands, focusing on automotive safety in North America, healthcare diagnostics in Europe, and cost-effective solutions for consumer electronics in Asia-Pacific.

- For customized insights and to navigate the evolving thermal sensor industry, connect with Fact.MR for industry intelligence and strategic support.

Impact of Government Regulation

| Country | Impact of Policies, Government Regulations & Mandatory Certifications |

|---|---|

| United States |

|

| European Union |

|

| Japan |

|

| South Korea |

|

| China |

|

| India |

|

| Brazil |

|

| Australia |

|

Market Analysis

The infrared detector industry is on a steady growth trajectory, fueled by rising adoption in consumer electronics, automotive safety, and industrial automation. The key driver is the increasing demand for thermal imaging and motion sensing technologies across both commercial and defense sectors. Companies investing in miniaturization and AI-enhanced infrared solutions stand to gain, while those slow to adapt to smart technology integration risk losing relevance.

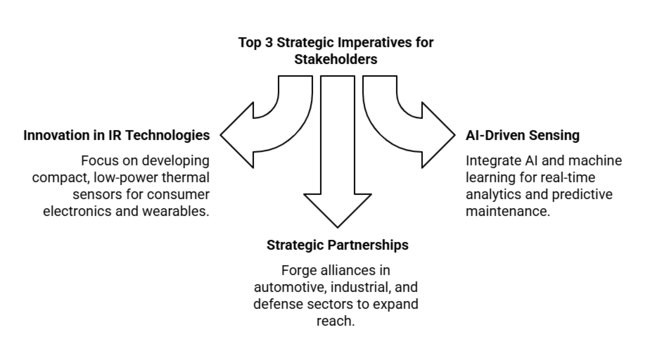

Top 3 Strategic Imperatives for Stakeholders

Accelerate Innovation in Miniaturized IR Technologies

Invest in the development of compact, low-power thermal sensors tailored for consumer electronics and wearables to capitalize on surging demand in smart home and personal health monitoring applications.

Align with AI-Driven Sensing and Predictive Capabilities

Integrate AI and machine learning into infrared systems to enable real-time analytics, predictive maintenance, and adaptive sensing-aligning offerings with the shift toward intelligent automation across industries.

Forge Strategic Partnerships and Expand Vertical Reach

Pursue distribution alliances and OEM partnerships in automotive, industrial, and defense sectors, while simultaneously increasing R&D spending or exploring M&A opportunities to scale capabilities and shorten go-to-market timelines.

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability & Impact |

|---|---|

| Technological Obsolescence- Rapid advancements in infrared technology may lead to older models becoming obsolete, forcing manufacturers to invest in constant innovation. | High Probability, High Impact |

| Regulatory Challenges- Changes in environmental or safety regulations could increase compliance costs for manufacturers and hinder the speed of product launches, especially in regions with strict regulations. | Medium Probability, High Impact |

| Supply Chain Disruptions- Geopolitical tensions, natural disasters, or component shortages could disrupt the supply chain, delaying production and leading to higher material costs. | Medium Probability, Medium Impact |

Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Expansion of AI-Enabled Infrared Detection | Conduct R&D trials on AI-driven infrared detection systems for automotive and healthcare applications. |

| Regulatory Compliance & Certification | Secure certifications for compliance with regional infrared detection standards in key industries. |

| Industry Penetration in Emerging Regions | Establish localized partnerships and offer tailored pricing models to drive adoption in price-sensitive regions. |

For the Boardroom

To stay ahead, companies must prioritize R&D investments in AI-enabled detection systems, focusing on the automotive and healthcare sectors to leverage emerging trends. Additionally, securing regulatory certifications across key regions will ensure smoother entry and compliance.

By forming strategic partnerships in emerging regions with tailored pricing strategies, the client can accelerate adoption in price-sensitive industries. This intelligence emphasizes the need for proactive innovation and regional customization, altering the roadmap by shifting focus toward AI integration, regulatory preparedness, and regional penetration to maintain a competitive edge through 2035.

Segment-wise Analysis

By Spectral Range

The Short-Wave Infrared (SWIR) detectors segment is projected to register a CAGR of 8.0% between 2025 and 2035. Their application in industrial inspection, agriculture, and security systems is driving the growth mainly. They are able to perform high-resolution imaging in low-light environments and are being incorporated into IoT-based monitoring systems for real-time leak detection and remote use.

With the expanding demand for night vision and thermal imaging technologies across the defense industry, the segment of SWIR will continue to experience high growth. Fact.MR research demonstrated that firms are increasingly implementing SWIR detectors across key industrial purposes like plant condition monitoring and defect detection in materials.

By Technology

The Mercury Cadmium Telluride (MCT) detectors segment is anticipated to expand at a CAGR of 8.4% during the period 2025 to 2035, based on their high sensitivity and broad wavelength detection range. MCT detectors are used mainly in military, defense, and scientific research applications such as surveillance, missile guidance, and thermal imaging.

The growing need for state-of-the-art infrared-based systems, including infrared cameras for medical diagnostic applications in cancer detection and environmental monitoring, is also driving the expansion. Fact.MR study revealed that the growing application of MCT detectors across multiple industries is a prominent driver for their growth.

By Application

The automotive segment is anticipated to grow at a CAGR of 7.5% from 2025 to 2035. Thermal cameras are used increasingly in driver assistance, night vision, and pedestrian detection systems. As manufacturers of automobiles concentrate on improving safety features and making autonomous driving technology a part of the vehicles, demand for thermal sensors will grow considerably in the automobile sector.

As per Fact.MR, the increasing popularity of intelligent, connected cars will continue to drive the growth of the segment, with more cars featuring advanced thermal-based sensors for increased safety as well as functionality.

Country-wise Insights

USA

The USA is expected to register a CAGR of 7.5% during the period 2025 to 2035, buoyed by growing demand in end-use applications across segments like aerospace, defense, and consumer electronics. Although still a growth driver, this has been mainly on the spur of sensor technology through the application of thermal sensors in autonomous and industrial applications.

Increased USA government expenditure for defense technologies and smart cities, thermal sensors becoming increasingly important in advanced surveillance, monitoring and safety systems. Furthermore, the application of such thermal sensors in smart devices is likely to be boosted by Energy Star energy efficiency regulations.

The in-store availability of thermal sensors for consumer products, such as security cameras, and the growing demand for and adoption of IoT-based solutions for continuous growth. Stringent regulatory standards, such as FCC and UL Certification, also assure product safety and growth. With companies moving toward automation and sustainability, thermal sensors will be critical to applications ranging from temperature sensing to advanced imaging systems, resulting in consistent growth.

UK

The UK is anticipated to grow with a CAGR of 6.0% during the period between 2025 and 2035. The demand is fueled by technological advancements in the automotive and healthcare industries, increasing investments in autonomous vehicle technology, and the increasing requirement for advanced diagnostics in medical imaging. The emphasis by the UK government on minimizing carbon emissions and favoring energy-efficient technologies has created a higher demand for thermal sensors used for environmental monitoring and smart grids.

Further, the dominant role of top-notch semiconductor producers and research organizations within the nation is driving innovation and product development across thermal sensing technology. CE Marking and compliance with RoHS are obligatory marking and certification of conformity to standards that affect UK thermal sensor production, promoting safety and environmental guidelines.

With the growing emphasis on smart buildings, industrial automation, and security applications, the UK is a profitable industry for thermal sensing technologies with huge prospects in both industrial and consumer spaces.

France

France is anticipated to grow at a CAGR of 6.5% from 2025 to 2035. Environmental sustainability in France and continuous efforts to develop smart infrastructure are major drivers for demand for thermal sensors in energy-saving applications like building automation and smart grids.

In the defense industry, the demand for increased security and surveillance features has driven the uptake of sophisticated thermal detection technologies. France is also seeing a growth in demand for thermal sensors used in automotive safety systems, specifically for driver assist technologies in autonomous vehicles. As a member of the European Union, France follows the EU RoHS Directive, encouraging the use of green materials and recycling.

In addition, the increasing trend of IoT integration in multiple industries like healthcare and industrial monitoring is likely to boost growth. The government's efforts to foster research and development, as well as the ongoing development of industrial applications, make for a strong outlook for thermal sensors in the nation.

Germany

Germany is also expected to develop at a CAGR of 7.2% from 2025 to 2035 due to the technological leadership of the country in the automotive, industrial, and healthcare sectors. The robust automotive industry of Germany, especially the emphasis on autonomous driving and safety features, has greatly pushed the demand for thermal sensors in car sensor systems.

The nation's strict environmental laws, such as those under the CE Marking and RoHS compliance, promote the use and creation of energy-efficient thermal sensors. The growth is likely to be supported by Germany's eminence in industrial automation and intelligent manufacturing. Thermal sensors, on the other hand, are used for most temperature sensing, environmental monitoring, and machine vision systems.

Among other things, the development of Industry 4.0 and the orientation toward sustainable growth will require more thermal sensors to help improve energy efficiency, safety, and performance in industry. As innovation in thermal sensing technology is spearheaded by top manufacturers and research facilities, Germany is still the most profitable destination in Europe.

Italy

Italy is anticipated to grow at a CAGR of 6.0% from 2025 to 2035, driven by Italy's increasing focus on energy-efficient technologies and industrial automation. As industries shift towards smart manufacturing and IoT-based solutions, thermal sensors are becoming imperative to boost productivity and energy efficiency.

Italy's automotive industry, which is centered on electric cars and autonomous driving technology, is also driving demand for thermal sensors. The nation's initiatives in curbing greenhouse gas emissions and enhancing air quality will increase thermal sensor use in environmental monitoring and smart grid systems.

In addition, Italy's dominance in the design and production of quality consumer electronics is fueling thermal sensor growth applications in security systems, home automation, and health care devices. CE Marking and RoHS compliance regulations guarantee that thermal sensors are safe, high-quality, and environmentally friendly. As Italy develops smart infrastructure and renewable technologies, the demand for thermal sensors will increase steadily.

South Korea

South Korea is expected to expand at a CAGR of 6.7% from 2025 to 2035 due to the advanced technology infrastructure of South Korea and high demand for sophisticated electronics for consumer applications, defense purposes, and medical treatments. Growing emphasis from the country on autonomous car technology and smart cities will drive the use of thermal sensors in advanced driver-assistance systems (ADAS) as well as city infrastructure monitoring.

South Korea's electronics and semiconductor manufacturing industries are among the largest contributors to the demand, with thermal sensors being used across a broad range of products like mobile phones, cameras, and medical devices. The demand for thermal sensors for use in security and surveillance systems is also on the rise, especially in metropolitan areas and sensitive infrastructure.

The nation's rigorous K-EMC regulation of electromagnetic compatibility and RoHS compliance for environmental safety ensures thermal sensors have passed tests to be up to par. The high-tech fields will grow heavily as South Korea keeps funding such investments.

Japan

Japan is anticipated to grow at a CAGR of 5.8% from 2025 to 2035, driven by robust demand from the automotive, consumer electronics, and healthcare industries. Japan is at the forefront of robotics and automation, and demand for thermal sensors in industrial robots and autonomous vehicles is likely to rise.

In addition, Japan's aging population is driving the expansion of medical thermal sensors applied in diagnostic imaging and health monitoring equipment. Despite its relatively slow adoption of advanced thermal technologies in comparison to other regions, Japan is focusing on innovation in the field of energy-efficient sensors for smart homes and industrial applications.

Stringent regulations under the Japan Industrial Standards (JIS) and environmental guidelines push the adoption of safer, more efficient thermal sensors. The focus on energy efficiency and sustainability in the country is also bound to propel the demand for thermal sensors, especially in energy management systems. The industry will also experience steady growth through continuous technology advancements and Japan's robust industrial sector.

China

China is also expected to grow at a significant 8.3% CAGR from 2025 to 2035, driven by swift industrialization, urbanization, and rising consumption of consumer electronics. China's initiative towards the ambitious Made in China 2025 initiative and growing focus on technology innovation have created huge demand for thermal sensors across various industries like automotive, defense, and medical.

Increasing use of thermal sensors in thermal imaging cameras, security systems, and industrial monitoring is driving growth. The expansion of electric and autonomous vehicles in China is also augmenting the demand for thermal sensors to be used in safety and navigation systems. China's regulatory system, such as RoHS compliance and CCC certification, ensures that products are safe, environmentally friendly, and meet quality requirements.

The increasing awareness of the environment in the country, coupled with policies encouraging the use of energy-efficient technologies, is likely to drive the uptake of thermal sensors in green technology and energy management. With its strong manufacturing industry and government backing of high-technology industries, China is expected to continue as a leading player in the sector.

Australia-New Zealand

Australia-New Zealand is expected to grow at a CAGR of 6.2% from 2025 to 2035. Various technologies added to industries like mining, defense, and agriculture are driving the consistent demand for thermal sensors. Presently, high usage of environmental monitoring systems happens in places with changes in temperature levels, air quality, and other ecological factors in more remote and industrial parts of Australia.

The defense industry of the country is another major driving force for thermal sensor uptake, especially in surveillance, night vision, and thermal imaging systems. New Zealand, with its emphasis on sustainability and renewable energy, is experiencing growing demand for thermal sensors in energy management and smart grids. Both nations have strict environmental and safety standards, with SAA certification in Australia guaranteeing the safety of thermal sensors.

Additionally, CE Marking and RoHS compliance in both countries ensure adherence to European standards for product quality and environmental impact. The demand is also driven by the increasing use of thermal sensors in healthcare applications, particularly for medical diagnostics and monitoring devices.

Market Share Analysis

Teledyne FLIR (USA): ~25-30%

Teledyne FLIR is expected to continue its dominance in the industry, led by its military, automotive as well as industrial thermal imaging technologies. Its focus on next-generation infrared cameras, as well as broadening its footprint in industrial and defense segments, will drive growth.

Raytheon Technologies(USA): ~15-20

Raytheon Technologies is expected to strengthen its position in defense and aerospace infrared systems. Its continued focus on advanced military surveillance technologies, alongside its defense partnerships, is set to propel its share in the industry over the next decade.

L3Harris Technologies (USA): ~10-15%

L3Harris Technologies is poised to grow with its focus on military surveillance and space applications. Its technological advancements in infrared systems for defense applications, coupled with ongoing contracts in space-related projects, will drive steady expansion through 2035.

Leonardo S.p.A. (Italy): ~8-12%

Leonardo S.p.A. will benefit from its strong presence in European defense contracts and expertise in cooled thermal imaging technology. The company’s strategic initiatives, including new defense projects in Europe and partnerships with major defense agencies, will contribute to its growth.

BAE Systems (UK): ~7-10%

BAE Systems is positioned for sustained growth, with a focus on next-generation military thermal sensing systems and warfare technology. Its innovations in advanced imaging systems for military and defense applications are expected to support its growth trajectory.

Lynred (France): ~5-8%

Lynred will continue to grow with its high-performance cooled thermal sensing systems, particularly in defense and industrial applications. The company’s strong focus on innovation and expanding its presence in European and international markets is expected to bolster its share.

Key Companies

- FLIR Systems, Inc.

- Leonardo S.p.A.

- Northrop Grumman Corporation

- L3Harris Technologies, Inc.

- Thales Group

- Raytheon Technologies Corporation

- Hamamatsu Photonics K.K.

- Lockheed Martin Corporation

- BAE Systems plc

- Murata Manufacturing Co., Ltd.

- AeroVironment, Inc.

- Bosch Security Systems

- Teledyne Technologies Incorporated

- Sensors Unlimited, Inc.

- Smiths Detection

- Excelitas Technologies Corp

- Texas Instruments Incorporated

- Teledyne FLIR LLC

- OMRON Corporation

- Lynred

- Nippon Avionics Co., Ltd.

- OSI Optoelectronics

- Apogee Instruments, Inc.

- Kromek Group plc

- InfraTec GmbH

- Honeywell International Inc.

- Raptor Photonics

- Princeton Instruments

- Allied Vision Technologies GmbH

- Other Prominent Players

Infrared Detector Market Segmentation

By Spectral Range:

By spectral range, the industry is segmented into short wave infrared detector, mid-wave infrared detector, and long wave infrared detector.

By Technology:

Based on technology, the industry is segmented into mercury cadmium telluride, indium gallium arsenide, pyroelectric, thermopile, micro bolometer, and others.

By Application:

In terms of application, the industry is segmented into automotive, consumer electronics, medical, military, and security.

By Region:

The industry is segmented by region into North America, Latin America, Western Europe, South Asia & Pacific, East Asia, Middle East, and Africa.

- Frequently Asked Questions -

What are the key factors driving the demand for infrared detectors?

Technological advancements and growing applications in defense, automotive, and healthcare drive the demand.

How do infrared detectors work in military applications?

They detect heat signatures for thermal imaging, surveillance, and target tracking in low-light environments.

What industries benefit the most from infrared detector technology?

Defense, automotive, healthcare, security, and industrial manufacturing benefit the most.

What is the expected growth of infrared detector usage over the next decade?

Usage is expected to grow significantly, fueled by technological advancements and increasing adoption in various sectors.

What are the main types of infrared detectors?

Short-wave, mid-wave, and long-wave detectors are used for different thermal imaging and surveillance applications.

Author:

Shubham Patidar

Editor:

Naved Ahmed