- Base Value(2025): 1208.0 Mn

- Forecast Value (2035): 5708.1 Mn

- CAGR (2035): 15.4%

Silicon Carbide Composites Market Outlook 2025 to 2035

The global silicon carbide composites market is expected to reach USD 5,708.1 million by 2035, up from USD 1,034.2 million in 2024. During the forecast period, the industry is projected to expand at a CAGR of 16.8%.

Rising demand in aerospace, defense, and EV sectors, as well as superior thermal and mechanical properties, technological advancements in processing, regulatory push for lightweight, fuel-efficient materials, and growth in nuclear and renewable energy applications.

-2025-to-2035.webp)

What are the drivers of Silicon Carbide Composites market?

A combination of industrial utilization trends, material technological improvements, and expanding sector performance standards underpins the growth of the silicon Carbide (SiC) composites market.

Lightweight materials with high-temperature resistance have become essential to aerospace and defense applications. Commercial and military aircraft benefit from Silicon Carbide composites because they offer superior strength-to-weight ratios and thermal stability, which enable designers to use these materials for turbine parts, heat shields, and structural components, including planes and spacecraft.

The automotive industry's focus on power electronics alongside braking systems and structural weight reduction has driven the EV sector to utilize SiC composites more frequently. High temperatures, combined with corrosive conditions, enable SiC composites to expand their applications in nuclear and renewable energy systems through their use in heat exchangers and reactor components.

The reduction of production expenses through improved composite fabrication techniques, incorporating chemical vapor infiltration, polymer infiltration, and pyrolysis systems, leads to simpler commercialization of complex component designs.

As manufacturers pursue industrial automation alongside a growing need for durable components in harsh environments, such as those found in chemical processing and metallurgy, their applications continue to expand.

Surface engineering discovery, along with microstructural control, has reformed material trends, thereby solidifying SiC composites' role as foundational materials for future engineering applications.

What are the regional trends of Silicon Carbide Composites market?

The silicon carbide composites market advances most rapidly in North America because it’s aerospace and defense industries remain at high levels of development. Programs for military modernization, alongside the rapid pace of space exploration, demand high-performance SiC composites due to the substantial financial investments made in these initiatives.

The market grows steadily because of both robust research and development infrastructure, as well as state-sponsored innovation programs.

European nations, including Germany, France, and the UK, focus on lightweight materials to advance their automotive and aerospace manufacturing sectors. The combination of strict environmental regulations and fuel efficiency mandates in this region has caused SiC composites to quickly enter hybrid and electric vehicles.

The Asia-Pacific proves to be the market's fastest-growing area thanks to its rapid industrial development, infrastructure construction, and homegrown defense projects, combined with energy initiatives.

The three Asian nations, Japan, China, and South Korea, lead the scene with budget-friendly production capabilities as they expand their investment efforts in novel materials for both their local markets and international export needs.

What are the challenges and restraining factors of Silicon Carbide Composites market?

Despite strong growth prospects, the Silicon Carbide (SiC) composites market performs its widespread adoption encounters various obstacles. The main obstacle to widespread adoption results from manufacturing costs run high because of complex energy-intensive techniques including chemical vapor infiltration (CVI) and polymer infiltration and pyrolysis (PIP).

The manufacturing methods demand both exact control measures and extended processing durations, which drive up production expenses and limit scalability for large-scale manufacturing operations.

The fabrication of SiC composites faces obstacles from both the lack of experienced professionals and skilled experts, who limit its ability to achieve high standards of quality and develop new solutions. Standardization processes across various industry sectors remain incomplete, which hinders the ability of technical systems to interact with one another.

The worldwide availability of high-purity silicon carbide and reinforcement fibers is hindered by supply chain uncertainties and risks stemming from geopolitical dynamics. The production methods of SiC composites, which can lead to environmental energy issues and waste production, may result in heightened regulatory oversight, potentially leading to additional compliance expenses. These elements combine to restrict business development, especially among applications that focus on costs.

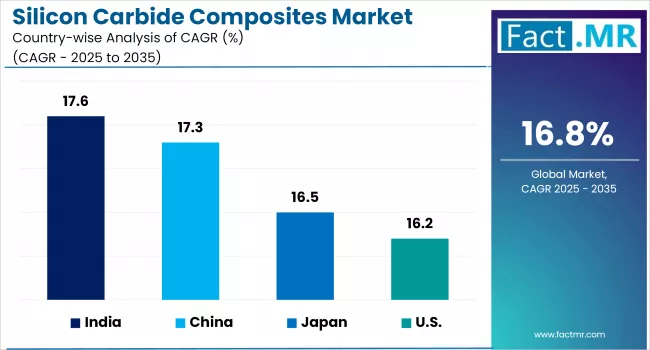

Country-Wise Outlook

U.S. Leadership in High-Performance Silicon Carbide Composites Driven by Defense, Aerospace, and Energy Sectors

The United States maintains its position as the world's leading producer of high-performance Silicon Carbide composites through fundamental research initiatives, combined with defense requirements and the needs of the aerospace sector. General Electric and 3M lead American businesses in SiC technology development for various applications, including gas turbine engines, as well as thermal protection systems and lightweight armored components.

Government-supported defense projects in collaboration with NASA enable the United States to lead worldwide advances in ceramic matrix composite technology (CMC). The aerospace, automotive, and energy sectors drive domestic SiC component demand because these materials demonstrate excellent performance when exposed to extreme temperatures and mechanical stress.

-2025-to-2035.webp)

EV power electronics and renewable energy infrastructure drive the growing adoption of SiC semiconductors because of their energy efficiency requirements. The United States maintains its position as a leader in premium-grade SiC composites because of stringent purity requirements and technological advances supported by government military investments and private sector sponsorship.

China’s Dominance in Silicon Carbide Composites Fueled by Manufacturing Scale, EV Demand, and Strategic Policy Support

China leads global Silicon Carbide (SiC) composite production due to its extensive manufacturing sector, along with its abundant raw materials and government support for performance-driven materials. Integrated supply chains, cost-efficient manufacturing, combined with the rapid adoption of SiC in electric vehicles (EVs), rail transport sectors, and aerospace applications, benefit China significantly.

SiC materials from Weifang Huawei and Ningxia Tianjing specialize in power electronics components, as well as load-bearing applications. China achieves market growth in exports through pricing competitiveness coupled with massive manufacturing capabilities. The SiC composites manufacturing leadership position in China extends from its ability to produce high-volume materials at competitive low costs, which is particularly beneficial for global industries seeking thermally stable, lightweight materials.

Japan’s Role in Advancing Silicon Carbide Composites Through Precision Engineering, Automotive Innovation, and Clean Manufacturing

The global silicon carbide composites market relies heavily on Japan due to its expertise in precision engineering, combined with superior materials production and advancements in automotive and electronics development. Japanese manufacturers lead the world in microstructure control techniques, resulting in advanced SiC products with enhanced thermal conductivity characteristics and improved mechanical strength performance.

Japanese manufacturers meet domestic automotive requirements for SiC-based components, including heat exchangers, brake systems, and power modules, due to their established presence in the hybrid and electric vehicle sector. Through its investments in next-generation power systems, Japan increases its consumption of SiC material for advanced smart energy applications.

Japan excels in producing premium, reliable SiC composite materials due to its robust intellectual property rights infrastructure, stringent manufacturing standards, and collaborative relationships with global automobile manufacturers.

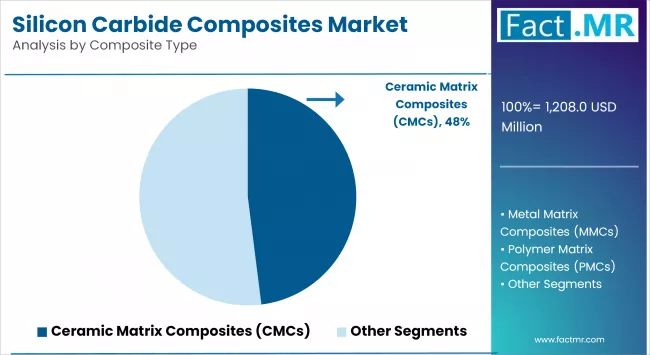

Category-Wise Analysis

By Composite Type – Ceramic Matrix Composites (CMCs) Dominate the Market Due to High Temperature Resistance

Within the silicon carbide composites market Ceramic Matrix Composites (CMCs) represent the highest performing material segment. The aerospace defense sector chooses CMCs because they demonstrate superior resistance to corrosive elements heat and shock due to their exceptional thermal properties. The extreme conditions present in jet engines and turbine blades and hypersonic vehicles render CMCs an ideal material due to their native mechanical stability under adverse conditions. The market's drive toward increased fuel efficiency combined with reduced carbon emissions makes CMCs attractive because they reduce overall weight substantially when compared with conventional metallic construction elements.

Manufacturing of CMCs through Chemical Vapor Infiltration (CVI) produces dense defect-free structures which exhibit exceptional bonding performance. The penetration of this material into low-cost markets remains constrained by production cost expenses and manufacturing duration.

The accelerated adoption of CMCs depends on regulatory support from aerospace authorities and military agencies who create material standards and certifications. CMCs continue to grow their applicability into energy systems and nuclear environments thanks to research developments that optimize production costs through hybrid processing methods and enhance market performance across high-end applications.

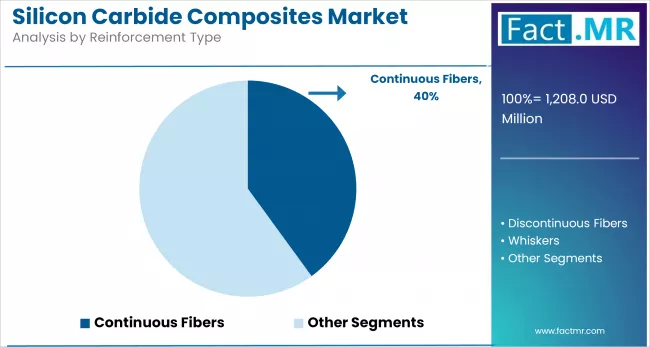

By Reinforcement Type – Continuous Fibers Reinforcement Leads Due to Enhanced Mechanical Strength

Silicon carbide composites market technology leads with continuous fiber reinforcement specifically when combined with ceramic matrix systems. The use of these fibers enables composites to maintain exceptional mechanical integrity and enhanced fracture toughness which allows them to operate under extreme operational stresses without breaking catastrophically. Their extended fiber layout efficiently moves load distances throughout design elements such as aerospace engines and defense applications and turbine housing systems.

Forward laser etching of continuous fiber-reinforced composites at high temperatures enables both dimensional retention and protection against creep elements. Modern ceramic coating techniques like CVI link tightly to this reinforcement method by applying ceramic material precisely across fiber networks to produce tough reliable matrices. These materials provide sufficient strength-to-weight performance and endurance capabilities to warrant their high cost application in critical systems.

Technological innovation is focused on enhancing fiber-matrix bonding and integrating next-gen materials such as SiC-SiC composites. With aerospace propulsion and hypersonic research driving material demands, continuous fibers are becoming a cornerstone in the evolution of high-performance composite engineering.

Competitive Analysis

The silicon carbide composites market contains companies of multinational scale alongside specialized material innovation experts. Main industry players compete based on their capabilities to create high-performance ceramics while delivering thermal resistance and lightweight structural applications. The market demand originates from aerospace, energy and electronics industries which requires improved fuel economy together with high-temperature functionality.

The market demands innovation in chemical vapor infiltration and sintering processes to function as a critical differentiating factor for companies in this industry. The rising importance of sustainability along with environmental requirements modifies both raw material selection and manufacturing methods.

A continuous wave of consolidation takes place within the market through planned partnerships alongside vertical integration and purposeful acquisitions. Companies from Asia-Pacific and other emerging regions drive market competition because they execute cost-efficient manufacturing combined with quick production scaling abilities. High-tech material innovation receives support from the current state of the market.

Key players in the market are COI Ceramics, General Electric, Rolls-Royce, SGL Carbon, Kyocera, Ube Industries, NGS Advanced Fibers, Suzhou Saifei Group, Saint-Gobain, Morgan Advanced Materials, CoorsTek, CeramTec, Schunk Group, and Tokai Carbon.

Recent Development

- In March 2025, the Schunk Group completed the acquisition of ESK-SIC GmbH, a raw materials manufacturer specializing in silicon carbide. This strategic move allows Schunk to broaden its product portfolio and strengthen its position in the SiC market, particularly benefiting its IntrinSiC business, which focuses on 3D-printed silicon carbide components.

- In February 2024, Kyocera Fineceramics Europe GmbH and ESK-SIC GmbH announced a partnership to improve the efficiency and sustainability of the silicon carbide value chain. The collaboration focuses on developing new manufacturing technologies, optimizing production processes, and establishing circular economy principles for recycling SiC materials.

Fact.MR has provided detailed information about the price points of key manufacturers of Silicon Carbide Composites Market positioned across regions, sales growth, production capacity, and speculative technological expansion, in the recently published report.

Segmentation of Silicon Carbide Composites market

-

By Composite Type :

- Ceramic Matrix Composites (CMCs)

- Metal Matrix Composites (MMCs)

- Polymer Matrix Composites (PMCs)

- Others

-

By Reinforcement Type :

- Continuous Fibers

- Discontinuous Fibers

- Whiskers

- Particles

- Others

-

By Manufacturing Process :

- Chemical Vapor Infiltration (CVI)

- Polymer Infiltration and Pyrolysis (PIP)

- Hot Pressing

- Sintering

- Others

-

By End-Use Industry :

- Aerospace and Defense

- Automotive

- Energy

- Electronics and Semiconductors

- Nuclear

- Others

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What was the Global Silicon Carbide Composites Market Size Reported by Fact.MR for 2025?

The global silicon carbide composites market was valued at USD 1,208.0 Million in 2025.

Who are the Major Players Operating in the Silicon Carbide Composites market?

Prominent players in the market are COI Ceramics, General Electric, Rolls-Royce, SGL Carbon, Kyocera, Ube Industries.

What is the Estimated Valuation of the Silicon Carbide Composites Market in 2035?

The market is expected to reach a valuation of USD 5,708.1 Million in 2035.

What Value CAGR did the Silicon Carbide Composites Market Exhibit over the Last Five Years?

The historic growth rate of the silicon carbide composites market was 16.2% from 2020-2024.