U.S. Electrical Steel Market Outlook (2025 to 2035)

The U.S. electrical steel market is forecast to reach USD 8.7 billion by 2035, up from USD 4.4 billion in 2025. During the forecast period, the industry is expected to register a CAGR of 7.1%, driven by increasing demand from critical sectors, including electric vehicles, renewable energy, and power infrastructure.

The shift toward electrification, the surge in EV production, grid modernization projects, and utility-scale solar and wind installations is reinforcing the need for advanced electrical steel grades. Additionally, domestic manufacturers are increasing their investments to meet performance standards and reduce their reliance on imports in response to supply chain vulnerabilities and federal clean energy incentives.

What are the Drivers of the U.S. Electrical Steel Market?

Several key factors are driving the growth of the U.S. electrical steel market. One of the primary drivers is the expansion of the electric vehicle (EV) industry. Electrical steel is a core material in EV motors. As automakers ramp up domestic production to meet clean energy goals, demand for high-efficiency steel grades like non-grain-oriented (NGO) electrical steel is rising sharply.

According to the U.S. Department of Energy, EV sales are expected to account for over 50% of new vehicle sales by 2030, which is expected to increase material consumption.

Another growth factor is the modernization of the country’s aging power grid. Electrical steel is vital for transformers, generators, and other grid equipment. With increased investment in grid resilience and renewable integration backed by the Inflation Reduction Act and infrastructure spending, utilities are upgrading components to improve energy efficiency and reduce transmission losses.

Additionally, the rise of distributed energy systems, including wind and solar power, is increasing the deployment of inverters and power transformers that rely heavily on grain-oriented electrical steel (GOES). The push for domestic sourcing and reshoring of manufacturing has also prompted U.S.-based steelmakers to expand capacity and introduce advanced, low-loss steel variants to compete globally and meet internal demand.

What are the Country Trends of the U.S. Electrical Steel Market?

The U.S. electrical steel market exhibits strong regional momentum, driven by increasing investment in power grid upgrades, domestic electric vehicle (EV) production, and the expansion of clean energy. In the Midwest and industrial heartland, states like Ohio, Michigan, and Pennsylvania are modernizing legacy steel mills to produce advanced grades of grain-oriented and non-grain-oriented electrical steel. These facilities are increasingly supplying material for transformers, motors, and EV components as domestic automakers ramp up electrification strategies.

Southern states like Georgia, Kentucky, and Tennessee have become emerging hubs for EV and battery manufacturing. This regional growth is spurring demand for high-efficiency electrical steels used in drive motors and charging infrastructure. In Texas, the expansion of renewable energy capacity, particularly wind and solar, has led to increased use of grain-oriented electrical steel for utility transformers, substations, and storage systems.

On the West Coast, states such as California are implementing stricter energy efficiency regulations and electrification mandates. These policies are pushing the adoption of advanced electrical steels with reduced core losses in applications spanning from public transit to residential energy storage. Meanwhile, in the Northeast, aging grid infrastructure is being retrofitted to meet modern reliability standards, further increasing demand for specialty steels.

What are the Challenges and Restraining Factors of the U.S. Electrical Steel Market?

The U.S. electrical steel market faces a range of structural and operational challenges that may hinder its long-term growth trajectory. One of the key obstacles is the limited number of domestic manufacturers capable of producing high-grade grain-oriented electrical steel (GOES), which is essential for transformers and high-efficiency motors.

As of 2024, Cleveland-Cliffs remains the only major domestic supplier of GOES, creating a supply bottleneck and increasing reliance on imports to meet the growing demand for grid modernization and electric vehicle applications.

Furthermore, the increasing global demand for electrical steel, driven by renewable energy projects, electric vehicles, and industrial automation, has intensified competition for limited raw materials and manufacturing capacity. Delays in infrastructure funding disbursement and lengthy permitting timelines further complicate expansion efforts in the U.S.

Labor shortages in specialized metallurgical and engineering roles also constrain production capacity and operational efficiency. Combined, these challenges underscore the need for coordinated investment, workforce development, and policy support to secure the U.S. electrical steel supply chain.

Category-wise Analysis

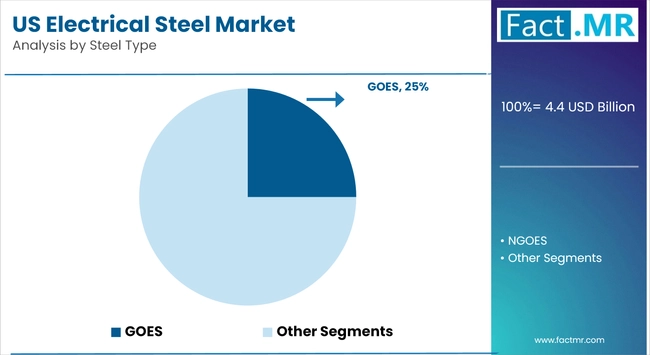

Grain-oriented electrical steel continues to account for the largest Contributor to U.S. Electrical Steel.

Grain-oriented electrical steel (GOES) continues to dominate the U.S. electrical steel market, maintaining its position as the leading product segment due to its essential role in power distribution and high-efficiency transformers. Widely used in the cores of transformers and other energy infrastructure components, GOES offers superior magnetic properties, including low core loss and high permeability in a specific direction, attributes critical to minimizing energy loss in transmission and distribution systems.

Additionally, the rise in electric vehicle (EV) production and the associated need for charging infrastructure are driving up demand for high-performance electrical steel in both distribution transformers and auxiliary energy systems. Given its performance efficiency and regulatory compliance with energy conservation standards, GOES remains a strategic material for meeting DOE transformer efficiency rules.

The segment is further supported by domestic producers such as Cleveland-Cliffs, which are focusing on expanding capacity and upgrading production technologies to meet rising quality specifications. Despite competitive pressure from overseas producers in Asia, the strategic importance of GOES in national energy security and grid stability ensures its continued dominance in the U.S. electrical steel market.

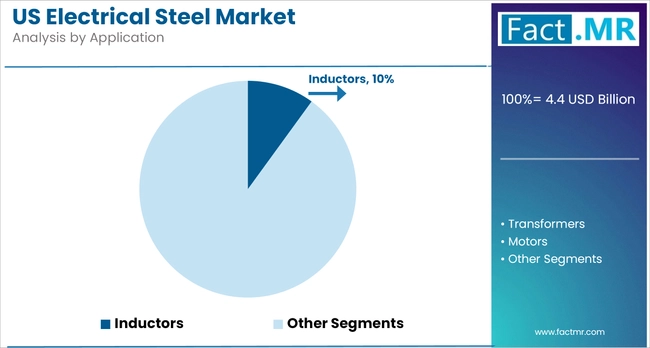

Transformers by Application Continue Accounting for the largest Contributor for U.S. Electrical Steel

Transformers remain the primary application segment driving demand for electrical steel in the U.S. electrical steel market, accounting for the largest share due to their critical role in power generation, transmission, and distribution networks. The increasing focus on modernizing aging grid infrastructure and integrating renewable energy sources has heightened the need for efficient and reliable transformers, which rely heavily on high-grade electrical steel, specifically grain-oriented types.

According to the U.S. Energy Information Administration (EIA), ongoing grid expansion and refurbishment projects across various states are intensifying demand for power and distribution transformers. These projects aim to enhance grid reliability, reduce transmission losses, and accommodate the increasing share of decentralized energy sources, such as wind and solar. Transformers built with advanced electrical steel contribute directly to energy efficiency goals by minimizing core losses.

Domestic steel manufacturers, including Cleveland-Cliffs and AK Steel, are actively responding to this surge by scaling up production and aligning their product specifications with those of transformer OEMs. As energy systems evolve and grid complexity grows, transformers will continue to serve as the core application area, reinforcing their dominant position in the U.S. electrical steel landscape.

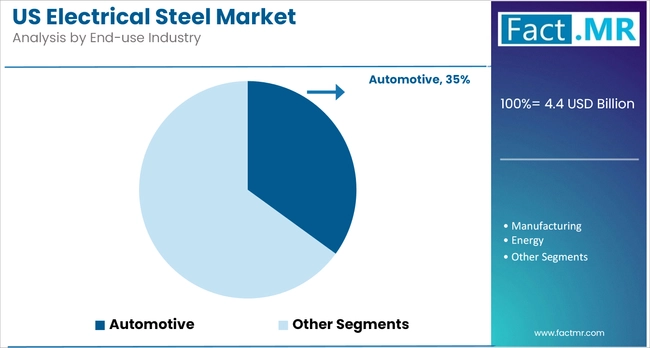

Energy electrical steel continues accounting for the largest Contributor to U.S. Electrical Steel by end-use industry

Energy infrastructure remains the leading end-use segment in the U.S. electrical steel market, driven by sustained investments in power generation, transmission, and grid modernization. The sector's reliance on grain-oriented and non-grain-oriented electrical steel for transformers, generators, and motors reinforces its position as the top consumer of high-efficiency magnetic materials.

The push toward decarbonization and electrification is intensifying the demand for advanced electrical steel grades that improve energy efficiency and reduce core losses. According to the U.S. Department of Energy, more than 70% of the nation’s grid infrastructure is over 25 years old, prompting federal and state-level investment in utility-scale transformer replacement and substation upgrades. These efforts align with the broader goals of enhancing grid reliability and integrating renewable energy sources, including wind, solar, and hydro.

Domestic producers are scaling up capacity to meet this demand. Companies such as Cleveland-Cliffs and U.S. Steel are focusing on high-performance, energy-grade electrical steel tailored for the evolving requirements of the power sector. As these structural energy upgrades progress, the U.S. electrical steel market will remain closely tied to the energy industry, which will continue to anchor its growth trajectory.

South-West by Region Continue Accounting for the largest Contributor for U.S. Electrical Steel

The South-West region remains the leading contributor to the U.S. electrical steel market, supported by large-scale industrial activity, a robust energy sector, and expanding investments in electrical infrastructure. States like Texas, Arizona, and New Mexico are experiencing high demand for transformers, electric motors, and grid components, which depend heavily on grain-oriented and non-grain-oriented electrical steel.

Texas, in particular, stands out due to its role as the nation's top energy producer and consumer. The Electric Reliability Council of Texas (ERCOT) continues to expand its transmission capacity to accommodate population growth and increase the integration of renewable energy. As of 2023, Texas accounted for over 26% of the country’s wind power capacity and leads in utility-scale solar development, both of which require transformers and inverters built with high-grade electrical steel.

Arizona and New Mexico are also increasing investment in solar infrastructure, further boosting the need for efficient electrical steel components. Additionally, the region’s strong presence of manufacturing facilities, electric vehicle (EV) supply chain development, and semiconductor production is driving demand for precision-grade steel used in motor laminations and switchgear.

With a favorable regulatory climate, substantial energy consumption, and ongoing infrastructure upgrades, the Southwest is expected to maintain its dominant position in the U.S. electrical steel market over the coming decade.

Competitive Analysis

Key players in the U.S. electrical steel industry include prominent manufacturers such as AK Steel Holding Corporation, Cleveland-Cliffs, Inc., Allegheny Technologies Inc., and United States Steel Corporation. These companies anchor the domestic supply chain by producing specialized grain-oriented and non-grain-oriented electrical steel, which is critical for transformers, electric motors, and power generation equipment.

Cleveland-Cliffs, following its acquisition of AK Steel, has strengthened its position by integrating vertically from mining to finished electrical steel products, offering enhanced supply stability and cost efficiency. Allegheny Technologies Inc. continues to serve niche applications with advanced metallurgical capabilities in high-performance alloys for energy and industrial sectors.

Meanwhile, Big River Steel (a part of U.S. Steel) is expanding its presence in advanced flat-rolled steel production through modern electric arc furnace (EAF) technology, supporting demand from the renewable energy and EV industries. Mid-sized and specialty firms such as Arnold Magnetic Technologies and Gibbs Wire & Steel Company, LLC, focus on custom-engineered laminations, slitting services, and precision strip solutions tailored for small motors and high-efficiency devices.

Distributors like Continental Steel & Tube Co. and AAA Metals Company, Inc. enhance U.S. electrical steel market accessibility by offering a wide range of electrical steel products with value-added processing capabilities. Together, these players shape a competitive landscape driven by innovation, regional supply optimization, and the accelerating push for domestic sourcing in the U.S. electrical steel industry.

Recent Development

- In October 2023, U.S. Steel inaugurated a new non‑grain‑oriented (NGO) electrical steel production line at its Big River Steel mill in Osceola, Arkansas. This USD 450 million, 2,333-foot line, with a 200,000-ton capacity, positions U.S. Steel as the largest domestic steel producer. Branded "InduX," the steel is manufactured with up to 90% scrap and claims a 70-80% reduction in Scope 1 and 2 CO₂ emissions compared to traditional integrated steelmaking.

- In July 2024, Cleveland-Cliffs announced a $150 million investment to convert its idle Weirton, WV, facility into a transformer manufacturing plant. This plant will utilize domestically produced grain-oriented electrical steel (GOES) from its Butler Works mill, thereby supporting U.S. energy grid needs.

Segmentation of the U.S. Electrical Steel Market

-

By Product Type :

- Grain-Oriented

- Non-Grain-Oriented

- Fully-Processed

- Semi-Processed

-

By Application :

- Inductors

- Transformers

- Transmission

- Portable

- Distribution

- Motors

- 1hp - 100hp

- 101hp - 200hp

- 201hp - 500hp

- 501hp - 1000hp

- Above 1000hp

-

By End-use Industry :

- Automotive

- Manufacturing

- Energy

- Household Appliances

- Others (Construction, Fabrication)

-

By Region :

- West U.S.

- Southwest U.S.

- Midwest U.S.

- North-East U.S.

- South-East U.S.

- Frequently Asked Questions -

What is the U.S. Electrical Steel Market Size in 2025?

The U.S. electrical steel market is valued at USD 4.4 billion in 2025.

Who are the Major Players Operating in the U.S. Electrical Steel Market?

Prominent players in the U.S. electrical steel market include AK Steel Holding Corporation, Allegheny Technologies, Inc., United States Steel Corporation, and others.

What is the Estimated Valuation of the U.S. Electrical Steel Market by 2035?

The U.S. electrical steel market is expected to reach a valuation of USD 8.7 billion by 2035.

What Value CAGR Did the U.S. Electrical Steel Market Exhibit over the Last Five Years?

The historic growth rate of the U.S. electrical steel market was 5.0% from 2020-2024.

Author:

S.N. Jha

Editor:

Naved Ahmed