Automotive Windshield Market Size, Market Forecast and Outlook By Fact.MR

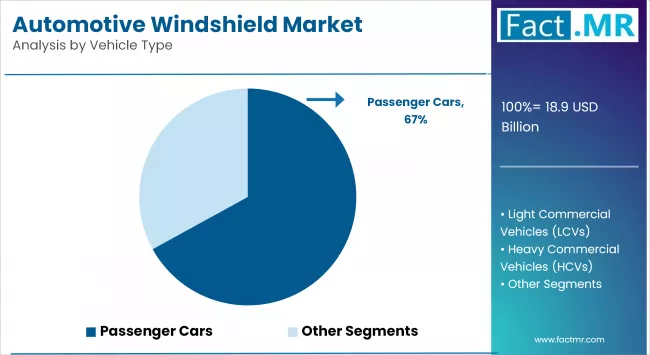

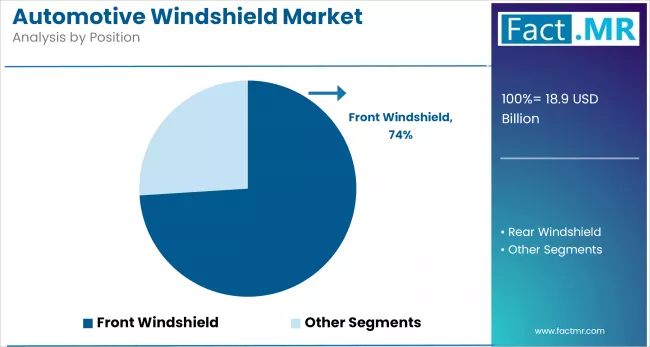

The global automotive windshield market was valued at USD 18.90 billion in 2025, projected to reach USD 20.13 billion in 2026, and is forecast to expand to USD 37.78 billion by 2036 at a 6.5% CAGR. Front windshields account for 71.3% of the position segment in 2026, reflecting the concentration of value in the primary forward visibility safety glass whose laminated construction, heating element integration, HUD projection surface preparation, and ADAS camera mounting provisions create substantially higher per-unit value than side and rear glass equivalents. Laminated glass holds 67.8% of the glass type segment, mandated by safety regulations for front windshields globally as the inner PVB interlayer prevents glass fragmentation on impact and maintains structural contribution to vehicle roof crush resistance.

The absolute dollar expansion of USD 17.65 billion over the forecast period reflects both volume growth from expanding vehicle production in emerging markets and significant per-windshield value increases from the integration of progressively advanced functional content, including HUD projection laminate layers, acoustic dampening interlayers, solar control coating stacks, and ADAS camera field-of-view demisting zones that transform the windshield from a passive transparency into a functional system component. OEM channels account for 73.5% of sales, reflecting windshields as safety-critical glass with vehicle-specific curvature and embedded component specifications establishing OEM supply relationships across full model production lifecycles.

Automotive Windshield Market Key Takeaways

| Metric | Details |

|---|---|

| Industry Size (2026) | USD 20.13 Billion |

| Industry Value (2036) | USD 37.78 Billion |

| CAGR (2026-2036) | 6.5% |

Germany leads country growth at 5.3% CAGR through 2036, driven by premium vehicle manufacturer investment in HUD projection windshields, acoustic interlayer specifications, and advanced ADAS camera integration glass solutions across high-value passenger car platforms. Japan follows at 4.8% CAGR, where domestic glass manufacturers supply the global Japanese OEM base with advanced laminated and functional windshield systems. The United States advances at 4.2% CAGR, supported by large vehicle parc aftermarket replacement demand and growing OEM HUD windshield specification across mid-premium and premium passenger car and SUV platforms.

Summary of Automotive Windshield Market

- Automotive Windshield Market Definition

- The automotive windshield market covers front and rear windshields and side window glazing for passenger and commercial vehicles across laminated, tempered, acoustic, solar control, and HUD projection glass configurations, supplied through OEM production and aftermarket replacement channels globally.

- Demand Drivers in the Market

- Head-up Display Adoption Requiring Specialised HUD Projection Windshield Specifications: The expansion of head-up display systems from premium exclusivity toward mid-segment standard specification across European, Japanese, and Chinese passenger car platforms requires OEM engineers to specify HUD projection windshields with controlled optical wedge geometry, anti-double-image coatings, and heating element layouts maintaining demisted HUD projection zones, creating a per-windshield value uplift opportunity for glass manufacturers who can supply HUD-optimised specifications at mid-segment cost targets.

- ADAS Camera Integration Requiring Optically Clear Camera Aperture Zones: Mandatory forward-facing camera integration for lane departure warning and automatic emergency braking under EU GSR and equivalent regulations requires front windshield glass with defined optically clear zones free of distortion, tinting, or heating element obstruction in the camera field of view, increasing the per-unit engineering content of ADAS-compatible windshield assemblies compared to pre-ADAS specifications.

- Acoustic Interlayer Adoption for EV Cabin Noise Management: Battery electric vehicles without engine noise masking expose occupants to road and wind noise transmitted through windshield and glass surfaces with greater perceptual clarity, creating OEM interior acoustic engineering demand for laminated windshields with enhanced acoustic interlayer PVB or EVA formulations that attenuate mid-frequency road noise components most perceptible in the absence of engine noise.

- Key Segments Analyzed in the Fact.MR Report

- Front Windshield Position: Commands 71.3% share in 2026 as the primary value-generating glass position, concentrating functional content including lamination safety, heating elements, rain sensors, HUD projection surfaces, and ADAS camera aperture zones that create per-unit value substantially exceeding rear and side glass.

- Laminated Glass Type: Holds 67.8% share in 2026, mandated for front windshield positions by safety regulations globally as PVB interlayer prevents fragmentation on impact and maintains structural roof crush resistance, while simultaneously enabling functional interlayer additions for acoustic, solar control, and HUD projection that drive premium glass specification adoption.

- OEM Distribution Channel: Accounts for 73.5% of 2026 market value, reflecting windshields as safety-critical components with vehicle-specific geometry, embedded component specifications, and regulatory compliance requirements establishing supply relationships across full model lifecycles, with aftermarket representing the complementary damage and wear replacement demand stream.

- Analyst Opinion at Fact.MR

- Fact.MR analysis indicates the automotive windshield is undergoing the most significant functional transformation since the original laminated safety glass mandate, as the simultaneous convergence of HUD display expansion, ADAS camera integration, acoustic EV optimisation, and solar control energy efficiency requirements is converting the windshield from a passive transparency into the most functionally complex glass component in the vehicle. This functional complexity escalation is creating per-windshield value growth substantially outpacing unit volume growth over the forecast period, with the 6.5% CAGR significantly exceeding the underlying vehicle production growth rate as value content per unit increases. The most structurally significant development is the emerging requirement for augmented reality HUD windshields projecting a wide-field navigation overlay across the full windshield surface, as AR HUD technology requires specialised optical laminate systems whose manufacturing complexity creates significant barriers concentrating supply among the small number of manufacturers with advanced coating and lamination capability.

- Strategic Implications / Executive Takeaways

- AR HUD Windshield Technology Development Investment: Automotive glass manufacturers should invest in the optical laminate coating and precision wedge geometry manufacturing capability required for augmented reality HUD windshield systems, as AR HUD adoption across premium and subsequently mid-premium OEM platforms will create a high-value glass category whose manufacturing barriers protect suppliers with established qualification from competitive pricing pressure.

- Acoustic Glass Product Line for EV Platform OEM Qualifications: Glass manufacturers should develop EV-specific acoustic interlayer product lines validated for the noise transmission attenuation requirements of electric vehicle interior acoustic targets, engaging EV platform OEM glass specification teams during vehicle development phases when acoustic glass specifications are being defined and supplier qualification decisions are made.

- ADAS Camera Aperture Certification Programme: Suppliers should develop standardised ADAS camera aperture optical quality certification programmes validated against the field-of-view distortion and optical clarity specifications required by major front-facing camera sensor suppliers, as OEM camera integration engineering teams are requiring glass suppliers to provide aperture optical certification data as a prerequisite for windshield programme nomination on ADAS-equipped platforms.

What are the Drivers of the Automotive Windshield Market?

Many companies in the automotive industry design, develop, manufacture, market, and sell cars. Automobile windshields shield the occupants and interior from dust, rain, wind, and other elements, also helping to strengthen the car's structure. According to the Belgian European Automobile Manufacturers' Association, new car registrations increased by 3.9% in August 2024, exceeding 6.5 million units. Spain (+5.6%), Italy (+5.2%), Germany (+4.3%), and France (+2.2%) were the bloc's largest markets, all experiencing slight growth.

The European Automobile Manufacturers Association (ACEA) reported that vehicle production in the European Union increased by nearly 14% in the first three quarters of 2023 compared to the same period in 2022. The consistent increase in automotive production following the pandemic is influencing market growth. Furthermore, rising demand for personal transportation and improving living standards in emerging economies are anticipated to fuel the market in the coming years.

Increased demand for electric and premium vehicles is also having an impact on the market. These vehicles often feature advanced windshield technologies, including solar-reflective coatings and acoustic insulation, to enhance passenger comfort and improve energy efficiency.

What are the Regional Trends of Automotive Windshield Market?

The North American automotive glass market is expected to grow due to several factors. Rising local adoption of electric vehicles is boosting demand for specialized glass, while stricter safety regulations are accelerating the need for advanced glass technologies, driving overall market growth. This region's focus on lightweight materials to improve fuel efficiency offers opportunities for innovative glass solutions. The North American automotive glass market is poised for growth due to the strong automotive industry and rising concerns for vehicle aesthetics and safety.

Europe is renowned for pioneering and adopting advanced technologies across various industries. Consequently, the region's market is growing due to the increased use of innovative automobile windshield technologies, such as electronically heated and UV-protected ones. Volkswagen, Mercedes-Benz, Renault, and other major automakers in the region, along with a focus on vehicle safety and comfort, are expected to boost market growth in the coming years.

The Asia-Pacific region is witnessing significant advancements in automotive technology, including smart windshields and Advanced Driver Assistance Systems (ADAS). The incorporation of these technologies into vehicles increases demand for high-tech windshields, which strengthens the region's automotive windshield market.

The automotive windshield market in the Middle East and Southeast Asia is expanding due to increased car production, consumer demand, and urbanization. Heat-resistant and UV-protective glass drives demand in the Middle East, while OEM growth helps Southeast Asia. Government road safety initiatives, rising disposable income, and a growing preference for technologically advanced vehicles are propelling market growth.

What are the Challenges and Restraining Factors of Automotive Windshield Market?

Global economic fluctuations lead to inflation, significantly increasing the cost of automotive components, including windshields and other parts. As a result, due to the high cost of automotive and related components, consumers avoid or delay vehicle purchases in favour of alternative, less expensive repair options rather than purchasing a new aftermarket product. As a result, consumer preference for cheaper repairs over purchasing new windshields may hinder market growth in the years to come.

Governments worldwide are implementing scrappage policies to eliminate obsolete and older automobiles. For instance, in April 2022, the Indian government implemented a vehicle scrapping policy. Similarly, other countries have implemented vehicle scrappage policies. As a result of the market uncertainty caused by these scrappage policies, the public is avoiding spending on windshield replacements for outdated or older automobiles. As a result, the aftermarket demand for automotive windshield replacement may decrease.

Supply chain disruptions and raw material price volatility have an impact on the market. Glass manufacturing requires specific raw materials such as silica and soda ash, and their fluctuating prices, combined with energy-intensive production processes, present cost challenges for manufacturers.

Environmental regulations governing the recycling of laminated glass are also emerging as a barrier. Due to their multi-layered structure, laminated windshields are challenging to recycle, prompting manufacturers to seek sustainable alternatives while maintaining safety standards.

Country-Wise Outlook

The U.S. Windshield Market Thrives on High Vehicle Ownership

The U.S. holds a significant share of the global automotive windshield market, largely due to its large vehicle fleet, high vehicle ownership rates, and robust aftermarket ecosystem. With over 280 million registered vehicles in 2023, the U.S. is expected to experience consistent demand for OEM and replacement windshields across a wide range of passenger and commercial vehicles.

The National Highway Traffic Safety Administration (NHTSA) and the Federal Motor Vehicle Safety Standards (FMVSS) enforce regulatory standards requiring the use of laminated safety glass in front windshields, with an emphasis on impact resistance and occupant protection. These regulations ensure a consistent quality standard and support the demand for advanced glass technologies.

The aftermarket segment presents significant opportunities, given the high frequency of windshield replacements resulting from accidents, weather, or road debris. Insurance coverage for glass damage, combined with the widespread availability of mobile repair services, helps sustain this segment. For instance, the average cost of a windshield replacement in the U.S. ranges from $200 to over $1,000, depending on the integration of ADAS and other advanced features.

Germany Drives Windshield Market Growth with Strong Manufacturing and Safety Standards

Germany is a key player in the global automotive windshield market, owing to its advanced manufacturing capabilities and stringent safety regulations. Germany, Europe's largest car producer, is expected to produce over 3.7 million vehicles in 2023, driving demand for innovative and high-quality windshield solutions in both domestic and export markets.

Compliance with EU safety directives requires the use of laminated front windshields and advanced glazing materials that ensure occupant safety and structural integrity in the event of an accident. German automakers are also incorporating camera-based ADAS systems, which require high-precision, optically clear windshields, hastening the transition to multifunctional and sensor-compatible glass.

The German government supports the use of recyclable materials and energy-efficient production processes, in line with its Climate Action Plan 2050. This encourages local manufacturers to adopt greener methods and invest in eco-friendly windshield technologies that reduce the carbon footprint.

India’s Shift Toward Premium Vehicles Boosts Adoption of Smart Windshield Features

India’s growing inclination toward premium vehicles is accelerating the adoption of smart windshield features. As more consumers opt for premium cars, manufacturers are incorporating advanced windshield technologies such as acoustic glass, infrared-reflective coatings, and heads-up display (HUD) compatibility, particularly in mid-range and luxury models. Hyundai and Tata Motors are now offering premium windshield features in models priced under ₹15 lakh.

India's climatic conditions, such as intense heat, UV exposure, and heavy monsoons, are driving demand for solar-controlled and water-repellent glass products. These features are becoming standard in higher trim levels to improve cabin comfort and visibility, particularly in major cities such as Delhi, Bengaluru, and Chennai.

Regulatory frameworks are also influencing the market. The Bharat New Vehicle Safety Assessment Program (BNVSAP) and Automotive Industry Standards (AIS-037) mandate laminated safety glass in front windshields, resulting in increased adoption across all vehicle categories. These regulations ensure minimum safety standards, and there is a gradual increase in demand for quality-certified windshield products.

Category-wise Analysis

Passenger Cars to Exhibit Leading Vehicle Type

The passenger car segment of the automotive glass market encompasses glass products used in personal transportation. The windshields, side windows, and rear windows of sedans, hatchbacks, and SUVs are included. In this segment, heads-up displays and smart glass are used to improve driving. Additionally, lightweight glass solutions are in demand to improve fuel efficiency and meet the automotive industry's sustainability goals.

The light commercial vehicles segment is anticipated to witness rapid growth over the projected period. The automotive glass market includes vans and pickup trucks as light commercial vehicles (LCV). For safety and longevity, this segment is demanding more durable and impact-resistant automotive glass. Manufacturers are developing LCV glass solutions that prioritize safety and cost. Light commercial vehicles are increasingly being utilised in various industries, driving the demand for reliable and high-quality automotive glass products.

Front Windshields to Exhibit Leading by Position

The front windshield is a crucial component of any vehicle, generating the most revenue. The vital role of the front windshield in protecting the driver from debris, wind, and other elements is expected to cement this segment's dominance in the long run. Furthermore, because of their critical role in ensuring cabin safety and integrity, front windshields have an advantage over other segments.

Rear windshields are widely used in passenger cars, and the rising sales of passenger cars are expected to generate new opportunities for this segment in the future. These windshields provide clear visibility of traffic behind the driver and also help to keep vehicles safe. The emphasis on improving vehicle safety and integrity for rear collisions and impacts is expected to increase the importance of rear windshields in the future.

Tempered to Exhibit Leading by Glass Type

Tempered glass is a type of automotive glass that is strengthened through a controlled thermal treatment. Tempered glass is a type of automotive glass that is durable and shatter-resistant. It is primarily used for side and rear windows. Tempered glass is becoming a popular choice in this category due to its safety features. Tempered glass is popular among automakers and consumers because it shatters into small, blunt pieces when struck, lowering the risk of injury during accidents and contributing to overall automotive safety trends.

Laminated glass is a popular segment of the automotive glass market due to its safety features. It is composed of two layers of glass bonded together by a layer of polyvinyl butyral (PVB) or a similar material that remains intact upon impact, thereby reducing the risk of shattering. The growing use of laminated glass for windshields, fueled by stringent safety regulations, is a notable trend in this segment. Manufacturers are constantly innovating to improve laminated glass's protection, UV filtering, and acoustic insulation, which contributes to its increasing popularity in the automotive industry.

OEM Segment to Exhibit Leading by Distribution Channel

The original equipment manufacturer (OEM) segment refers to the direct production and supply of glass to vehicle manufacturers for initial installation. In this segment, manufacturers collaborate with automakers to provide customized glass solutions tailored to specific vehicle models. A noticeable trend in the OEM segment is an increase in demand for advanced technologies, such as heads-up displays and smart glass, as automakers seek to incorporate innovative features that enhance safety, aesthetics, and overall driving experiences in newly manufactured vehicles.

The aftermarket segment of the automotive glass market refers to the replacement and customization of previously sold glass components. It includes services like windshield replacement and aesthetic or feature upgrades. The rising demand for replacement glass, resulting from wear, accidents, or changing safety standards, is a notable trend in this segment. As vehicles age, there is a consistent demand for automotive aftermarket glass services, resulting in a steady market for manufacturers and service providers to provide replacement solutions and cater to consumer preferences.

Competitive Analysis

The global automotive windshield industry is highly competitive, with major OEM suppliers and specialized glass manufacturers competing based on technology integration, safety features, performance, and cost-efficiency. Leading players such as AGC Inc., Saint-Gobain Sekurit, Nippon Sheet Glass Co., Ltd., Fuyao Glass Industry Group, Guardian Industries, Xinyi Glass Holdings, and Magna International are at the forefront of innovation.

These companies are investing in R&D to develop advanced windshield solutions incorporating heads-up displays (HUDs), acoustic insulation, solar control coatings, infrared-reflective layers, and rain-sensing technologies to meet evolving regulatory standards and growing consumer expectations for safety and comfort.

Integration of Advanced Driver Assistance Systems (ADAS) is a significant competitive advantage. With regulations pushing for increased vehicle automation and safety, windshields must now support cameras, sensors, and LiDAR. Manufacturers that can provide windshields with precise optical clarity and ADAS compatibility are more likely to form OEM partnerships. ADAS-compliant glass requires strict design tolerances, which increases production complexity and cost, putting newer or lower-tech competitors at a disadvantage.

Sustainability and recycling are emerging as key competitive differentiators. Governments and consumers alike prefer suppliers who are environmentally responsible. Windshield manufacturers that use recyclable materials or energy-efficient manufacturing processes have an advantage, particularly in Europe and North America, where environmental regulations are stringent.

Key players in the automotive windshield market include Saint-Gobain SA, Sisecam Group, Asahi Glass Co., Ltd., Magna International, Fuyao Glass Industry Group Co., Ltd., Shenzhen Benson Automobile, Xinyi Glass, Vitro, Nippon Sheet Glass Co., Ltd., Guardian Industries, PPG Industries, Safelite Auto Glass, and other notable companies.

Recent Development

- In April 2025, Saint-Gobain introduced a new line of laminated automotive windshields designed to improve both durability and energy efficiency. This innovative technology enhances heat insulation and noise reduction, thereby improving overall driving comfort for consumers.

- In March 2025, Tesla's latest electric vehicle models began to feature advanced smart windshields. These windshields feature augmented reality (AR) displays that offer real-time navigation, driving assistance, and enhanced safety features, transforming the driving experience.

Bibliography

- 1. United Nations Economic Commission for Europe. (2024, January). ECE Regulation No. 43: Uniform Provisions Concerning the Approval of Safety Glazing Materials and Their Installation on Vehicles. UNECE.

- 2. European Commission, Directorate-General for Internal Market. (2024, March). EU General Safety Regulation: ADAS Camera Field-of-View Windshield Optical Quality Requirements for Mandatory Lane Departure and Emergency Braking Systems. European Commission.

- 3. SAE International. (2024, February). SAE J673: Automotive Safety Glazing Materials - Specifications for Laminated and Tempered Safety Glass Including HUD Projection Surface Requirements. SAE International.

- 4. Government of China, Ministry of Industry and Information Technology. (2024, April). GB 9656: Automotive Safety Glass Standards for Passenger Vehicles Including Head-up Display Integration Requirements. MIIT China.

- 5. Government of India, Bureau of Indian Standards. (2024, March). IS 2553: Safety Glass for Automobiles - Laminated Glass Performance Requirements and Test Methods. BIS India.

- 6. International Energy Agency. (2024, May). Global EV Outlook 2024: Electric Vehicle Interior Acoustic Management and Glass Specification Requirements for Noise Attenuation. IEA.

This bibliography is provided for reader reference. The full Fact.MR report contains the complete reference list with primary research documentation.

This Report Addresses

- Market sizing and quantitative forecast metrics: detailing precise revenue projections, absolute dollar growth, and compound annual growth rates across major automotive windshield segments and geographies through 2036.

- Segmentation analysis: mapping adoption velocity of leading product, technology, and end-use categories and evaluating structural factors driving segment share transitions over the forecast period.

- Regional deployment intelligence: comparing growth dynamics in high-momentum Asia Pacific and emerging markets against the mature replacement and upgrade demand patterns prevalent in European and North American hubs.

- Regulatory compliance assessment: analyzing how evolving product safety standards, environmental directives, and sector-specific mandates are reshaping procurement decisions, material specifications, and supplier qualification criteria.

- Competitive posture evaluation: tracking consolidation trends, platform integration strategies, technology differentiation investments, and the resulting competitive dynamics among established players and emerging challengers.

- Capital project strategic guidance: defining the procurement specifications, investment thresholds, and performance benchmarks required to support next-generation product adoption and facility modernization programs.

- Supply chain vulnerability analysis: identifying sourcing concentration risks, logistics bottlenecks, raw material price dependencies, and geographic exposure scenarios that affect market participant cost structures.

- Custom data delivery formats: encompassing interactive dashboards, raw Excel datasets, and comprehensive PDF narrative reports tailored for executive decision-making and analyst reference applications.

Automotive Windshield Market Definition

The automotive windshield market encompasses automotive safety glazing assemblies for front and rear windshields and side window positions in passenger vehicles, light commercial vehicles, and heavy commercial vehicles, including laminated safety glass front windshields, tempered glass rear windows, acoustic interlayer glass, solar control coated glass, and HUD projection surface prepared glass assemblies, supplied to vehicle manufacturers through OEM production and the aftermarket replacement channel.

Automotive Windshield Market Inclusions

Market scope includes PVB and SGP laminated front windshield assemblies, embedded heating element windshields, rain and light sensor integration windshields, HUD projection laminate windshields, acoustic interlayer noise reduction windshields, solar control and infrared reflecting coated glass, tempered rear and side window glass, and electrically heated rear windows. Geographic analysis covers North America, Latin America, Europe, East Asia, South Asia, Oceania, and Middle East and Africa through 2036.

Automotive Windshield Market Exclusions

Architectural and building glass for vehicle manufacturing facilities, railway and aerospace transparency systems, aftermarket window tinting films applied over existing glass, decorative privacy film products, and glass repair services without full glass replacement fall outside this market scope.

Automotive Windshield Market Research Methodology

- Primary Research: Fact.MR analysts conducted interviews with automotive glass engineering managers at vehicle OEMs, windshield product development engineers at tier-one glass suppliers, and aftermarket windshield replacement service network managers to validate HUD glass adoption timelines, ADAS camera integration requirements, and acoustic and solar control glass adoption rates across passenger car platform programmes.

- Desk Research: Secondary research aggregated safety glazing regulation documentation from ECE Regulation 43 and equivalent national standards, HUD display system adoption data from automotive electronics publications, ADAS camera field-of-view specification requirements, and corporate revenue disclosures from listed automotive glass manufacturers.

- Market-Sizing and Forecasting: Baseline market values derive from a bottom-up aggregation of windshield unit volumes by vehicle type and position, multiplied by average unit prices across standard, acoustic, solar control, and HUD-prepared glass tiers. Advanced functional glass adoption penetration rates were applied as per-unit value uplift drivers as HUD specification expands from premium to mid-segment platforms.

- Data Validation and Update Cycle: Segment forecasts are cross-validated against revenue disclosures from publicly listed automotive glass manufacturers and vehicle production data from automotive associations. Annual updates incorporate actual HUD windshield fitment rates by vehicle segment and updated OEM glass specification data from new model launches.

Scope of the Report

| Metric | Value |

|---|---|

| Quantitative Units | USD 20.13 billion to USD 37.78 billion, at a CAGR of 6.5% |

| Market Definition | Front and rear windshields and side window glazing for passenger and commercial vehicles across laminated, tempered, acoustic, solar control, and HUD projection glass configurations, supplied through OEM production and aftermarket replacement channels. |

| Vehicle Type Segmentation | Passenger Cars, LCVs, HCVs |

| Position Segmentation | Front Windshield, Rear Windshield, Side Windows |

| Glass Type Segmentation | Laminated, Tempered, Acoustic, Solar Control, Heads-up Display Glass |

| Distribution Channel Segmentation | OEMs, Aftermarket |

| Regions Covered | North America, Latin America, Europe, East Asia, South Asia, Oceania, Middle East and Africa |

| Countries Covered | Germany, Japan, USA, and 40 plus countries |

| Key Companies Profiled | Saint-Gobain SA, Sisecam Group, Asahi Glass Co. Ltd., Magna International, Fuyao Glass Industry Group Co. Ltd., Shenzhen Benson Automobile, Xinyi Glass, Vitro, Nippon Sheet Glass Co. Ltd., Guardian Industries, PPG Industries, Safelite Auto Glass |

| Forecast Period | 2026 to 2036 |

| Approach | Bottom-up aggregation of windshield units by vehicle type and position with advanced functional glass adoption penetration and per-unit value uplift modeling |

Segmentation of the Automotive Windshield Market

-

By Vehicle Type :

- Passenger Cars

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

-

By Position :

- Front Windshield

- Rear Windshield

-

By Glass Type :

- Laminated

- Tempered

-

By Distribution Channel :

- OEMs

- Aftermarket

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

How large is the automotive windshield market in 2026?

The global automotive windshield market is estimated to be valued at USD 20.13 billion in 2026.

What will the windshield market size be by 2036?

The market is projected to reach USD 37.78 billion by 2036.

What is the expected CAGR between 2026 and 2036?

The automotive windshield market is expected to grow at a CAGR of 6.5% between 2026 and 2036.

Which position segment leads in 2026?

Front windshield commands 71.3% share in 2026, reflecting concentration of value in the primary forward visibility glass whose laminated construction, heating elements, HUD projection surfaces, and ADAS camera aperture zones create per-unit value substantially exceeding rear and side glass.

Which glass type holds the largest share?

Laminated glass holds 67.8% share in 2026, mandated for front windshield positions globally as PVB interlayer prevents fragmentation on impact and simultaneously enables functional interlayer additions for acoustic, solar control, and HUD projection driving premium specification adoption.

What is driving Germany's leading 5.3% CAGR?

Germany's growth is driven by premium vehicle manufacturer investment in HUD projection windshields, acoustic interlayer specifications, and advanced ADAS camera integration glass solutions across high-value passenger car platform portfolios.

What is excluded from this report?

Architectural building glass for manufacturing facilities, railway and aerospace transparencies, aftermarket window tinting films, decorative privacy films, and glass repair services without full replacement fall outside this market scope.

Author:

Shubham Patidar

Editor:

Naved Ahmed