Plastic Containers Market Outlook (2025 to 2035)

The global plastic containers market is projected to increase from USD 112.8 billion in 2025 to USD 187.3 billion by 2035, with a CAGR of 5.2%, driven by rising demand for convenient and lightweight packaging across the food, beverage, and personal care industries. Surge in e-commerce and online retail is driving the need for durable, cost-effective plastic packaging solutions.

-2025-to-2035.webp)

What are the Drivers of Plastic Containers Market?

The growth of the plastic containers market is driven by rising demand across industries for lightweight, durable, and cost-effective packaging solutions. As modern consumers increasingly seek convenience in their daily lives, plastic containers offer the ideal packaging format for ready-to-eat meals, beverages, cosmetics, and household products.

Their portability, reusability, and ability to preserve freshness make them highly preferred over traditional materials, such as glass or metal. The food and beverage industry, particularly the segments for dairy, soft drinks, and packaged foods, remains one of the most significant end users due to the protective and lightweight nature of plastics like PET and HDPE.

Another major factor fueling market growth is the global surge in e-commerce and online retail. With more consumers shopping online, particularly in emerging markets such as India, Brazil, and Southeast Asia, the need for secure and reliable packaging has become increasingly critical.

Plastic containers offer shock resistance and cost-effective mass transportation capabilities, making them ideal for shipping personal care products, pharmaceuticals, and electronics. Moreover, pharmaceutical and healthcare sectors are increasingly turning to plastic containers for packaging syrups, tablets, and ointments due to their sterility, non-reactive nature, and ability to withstand chemical exposure.

Furthermore, sustainability and innovation are reshaping the landscape of the plastic containers market. While environmental concerns and regulations regarding single-use plastics pose challenges, they also open opportunities for manufacturers to develop recyclable, biodegradable, and reusable containers. Innovations such as recycled PET (rPET), plant-based plastics (PLA), and compostable packaging are gaining traction, driven by growing consumer awareness and corporate sustainability goals.

Governments and regulatory bodies are promoting circular economy practices, offering incentives for the use of eco-friendly materials, thereby encouraging the adoption of sustainable plastic containers.

The growth of emerging economies significantly contributes to market expansion. Rapid urbanization, increasing disposable incomes, and shifting consumption patterns in regions such as the Asia Pacific, Latin America, and the Middle East are driving substantial demand for packaged consumer goods.

As populations in these areas continue to adopt more modern lifestyles, the demand for packaged food, beverages, cosmetics, and pharmaceuticals increases, directly driving the growth of the plastic containers market.

What are the Regional Trends of Plastic Containers Market?

The Asia Pacific region dominates the global plastic containers market and is also the fastest-growing region. This growth is largely driven by rapid urbanization, a rising middle-class population, and increased consumption of packaged food, beverages, cosmetics, and pharmaceuticals. Countries such as China, India, Indonesia, and Vietnam are experiencing a significant surge in demand due to the booming retail and e-commerce sectors.

Moreover, the Asia Pacific region benefits from low production costs, the availability of raw materials, and a large base of plastic manufacturers. Growing awareness about sustainable packaging is also prompting investments in recyclable and biodegradable plastic solutions, particularly in developed markets such as Japan and South Korea.

North America remains a significant market due to its high consumption of packaged goods and strong presence of established players in the packaging industry.

The U.S. and Canada are leading in innovation, especially in the development of recyclable and sustainable plastic packaging. Environmental regulations and growing consumer awareness have prompted companies to adopt materials such as recycled polyethylene terephthalate (rPET) and bio-based plastics.

The healthcare and pharmaceutical sectors also contribute significantly to demand, particularly for sterile and tamper-evident plastic containers. As a result, companies in this region are focusing on R&D and advanced technologies, such as smart and lightweight packaging.

In Europe, sustainability and regulation are the primary forces shaping market trends. The region has implemented strict environmental directives, such as the EU’s Single-Use Plastics Directive and circular economy policies, which are pushing manufacturers to reduce plastic waste and increase recycling rates.

Consumers are also highly environmentally conscious, creating a strong demand for eco-friendly and reusable plastic containers. Countries like Germany, France, Italy, and the U.K. are at the forefront of adopting biodegradable plastics and closed-loop recycling systems. This regulatory environment is prompting innovations in material composition, packaging design, and life-cycle assessment tools.

Rising urbanization, expanding retail sectors, and increasing disposable incomes are boosting the demand for packaged consumer goods in countries such as Brazil, Mexico, South Africa, and the UAE. However, these regions still face challenges, including inadequate recycling infrastructure and policy enforcement.

Despite these obstacles, the entry of global packaging companies and growing awareness of sustainable practices are beginning to positively influence the market. As infrastructure and regulatory frameworks improve, these regions are expected to offer significant growth opportunities for manufacturers of plastic containers.

What are the Challenges and Restraining Factors of Plastic Containers Market?

The plastic containers market is increasingly challenged by rising environmental concerns and the growing regulatory pressure to curb plastic waste. Governments around the world are implementing stringent regulations and bans on single-use plastics, particularly in Europe, parts of Asia, and North America.

These regulations require manufacturers to shift toward sustainable, recyclable, or biodegradable alternatives, posing a challenge for companies heavily reliant on conventional plastics, such as PET and HDPE.

Another key restraint for the market is the volatility in raw material prices, particularly as plastic containers are largely derived from petroleum-based compounds. Prices of polyethylene, polypropylene, and PET are subject to fluctuations based on global crude oil trends, geopolitical instability, and supply chain disruptions.

This unpredictability not only increases production costs but also impacts pricing strategies and profit margins across the industry. For companies operating on thin margins or in price-sensitive regions, these cost instabilities can disrupt operations and lead to reduced competitiveness.

Limited recycling infrastructure in many developing and emerging economies hinders the adoption of recycled plastic containers. While sustainable and circular packaging solutions are gaining momentum in developed regions, many parts of Latin America, Africa, and Southeast Asia lack the necessary systems for efficient plastic waste collection, sorting, and reprocessing.

This leads to higher plastic pollution and a negative public perception of plastic usage, ultimately affecting market demand. The lack of consumer awareness and inconsistent regulations around plastic recycling further exacerbate the issue in these regions.

Country-Wise Outlook

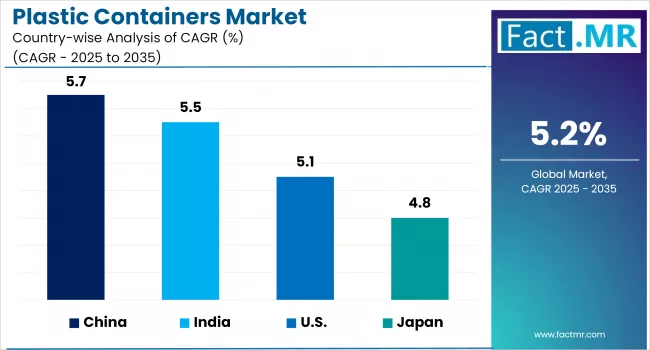

U.S. Plastic Containers Market sees Growth Driven by Growth in Food & Beverage and Pharmaceutical Industries

The U.S. plastic containers market is on a steady growth path, with robust projection figures and diverse drivers shaping its trajectory. This consistent growth reflects strong demand from multiple sectors, including food & beverage, pharmaceuticals, personal care, and household products, all seeking lightweight and high-performance packaging solutions.

Several key trends are fueling this growth. The e-commerce and food delivery boom continues to elevate demand for durable, tamper-evident packaging. In 2021, e-commerce sales accounted for 16% of U.S. retail sales, accelerating the use of plastic containers in last-mile distribution. Moreover, post-pandemic hygiene concerns have intensified the preference for sealed and sterile packaging, particularly within the food and medical industries.

Another significant growth factor is the increasing government emphasis on recycling and sustainable packaging. The Environmental Protection Agency (EPA) aims for a 50% recycling rate by 2030, prompting manufacturers to integrate recycled plastic content (e.g., rPET) and develop biodegradable alternatives.

Regulatory and consumer pressure toward eco-friendly packaging also fosters innovation in lightweighting and closed-loop systems, which in turn broadens market opportunities.

-2025-to-2035.webp)

Technological advancements in polymer science and manufacturing processes are enhancing both efficiency and product diversity. New materials, such as biodegradable polymers, and production methods, like 3D printing and smart packaging design (e.g., tamper-evident features), are enabling brands to meet evolving consumer and regulatory standards.

Through R&D investments, U.S. manufacturers are poised to maintain steady growth, adapt to sustainability trends, and retain global competitiveness in the coming decade.

China witnesses Rapid Market Growth Backed by Rapid Urbanization

The China plastic containers market continues to grow, primarily fueled by a booming e‑commerce sector and rising urban consumer demand. This steady growth trajectory reflects sustained consumption, driven largely by online retail and packaged food sectors.

Urbanization and changing consumer lifestyles also contribute significantly. With an urban population of over 65% and rising disposable incomes, there is an increasing demand for ready-to-eat, portion-controlled food and beverage products, all packaged in plastic containers.

Moreover, the growing awareness of food safety and hygiene, especially post-pandemic, has prompted manufacturers to adopt tamper-evident and high-barrier packaging formats.

However, sustainable packaging trends and environmental regulations are influencing market dynamics. Companies are investing in recycled PET (rPET), biodegradable materials, and closed‑loop recycling systems. These efforts reflect China's broader circular economy strategy aiming to reduce plastic waste and promote resource efficiency.

Japan sees Growth in E-commerce Fuels Demand for Plastic Containers

Japan’s strong focus on reducing plastic waste is accelerating the shift to sustainable packaging. The “Plastic Resource Circulation Strategy” (3Rs + Renewables) targets a 60% reuse/recycling rate by 2030 and 100% sustainable plastic packaging by 2025. As a result, manufacturers are transitioning to biodegradable plastics, recycled-content containers, and innovative recycling methods, such as bottle-to-bottle chemical recycling.

Innovations include lightweight, high-strength bioplastics, smart designs, and chemical recycling tech like HELIX (JEPLAN’s resin). Industrial players are investing heavily in automation, smart sensors, and flexible multipurpose packages to meet both performance and environmental standards. This supports Japan’s reputation for superior packaging quality and consumer trust.

E-commerce growth, particularly in the Kanto and Kansai regions, is driving demand for protective, lightweight containers that are easy to ship and convenient for consumers. Urbanization and the rise of one-person households (~35%) are driving a trend toward portion-controlled containers and resealable flexible packaging for convenience foods and skincare products.

Although plastic remains dominant, Japan is facing stiff competition from glass, paper, and aluminum packaging. For example, paperboard packaging grew due to sustainability demands and the aging population's need for easy-to-use options.

Glass packaging is also experiencing a resurgence in pharmaceuticals and beverages, with a recycling rate of approximately 73%, compared to 27% for plastics. Moreover, achieving Japan’s ambitious plastic recycling and reduction targets is challenging: only ~22 % of plastic is mechanically recycled domestically.

Category-wise Analysis

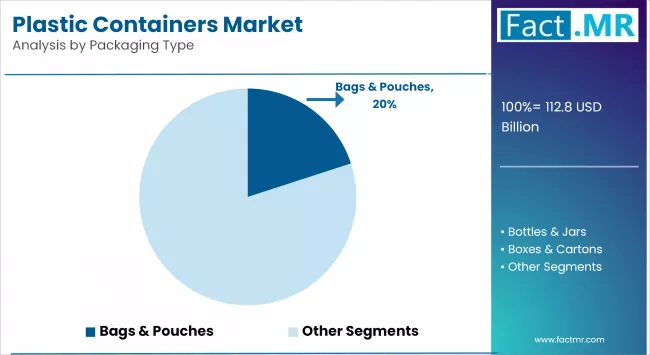

Bottles & Jars to Exhibit Leading by Packaging Type

Bottles & Jars hold the largest market share among packaging types. This dominance is primarily driven by widespread usage across food & beverage, pharmaceutical, personal care, and household sectors.

Plastic bottles, particularly those made from PET and HDPE are favored for packaging water, carbonated drinks, juices, dairy products, shampoos, and cleaning agents due to their durability, transparency, and lightweight nature.

The segment also benefits from growing demand for hygienic and tamper-evident packaging, especially in health-conscious and emerging markets. Moreover, the increasing adoption of recycled PET (rPET) and bottle-to-bottle recycling technologies is strengthening this segment’s role amid global sustainability efforts.

Bags & pouches is the fastest-growing segment driven by shifting consumer preferences toward flexible, lightweight, and resealable packaging solutions. These formats are increasingly used in snack foods, ready-to-eat meals, sauces, baby food, and pet food, as well as in personal care and healthcare products.

The growth is particularly strong in Asia Pacific and North America, where rising e-commerce activity and the demand for convenience-based packaging are expanding the usage of pouches. Technological advancements in barrier films, vacuum-sealing, and spouted pouches are also driving innovation.

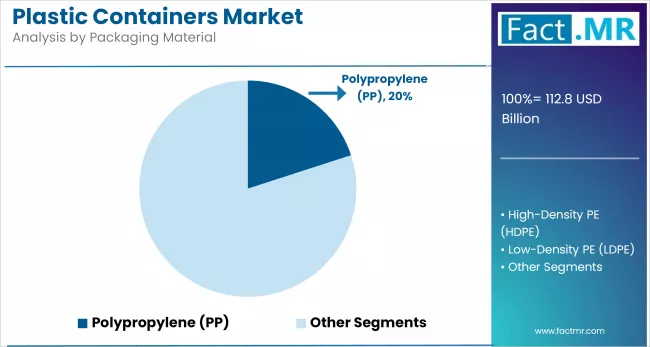

Polypropylene (PP) to Exhibit Leading by Packaging Material

Polyethylene Terephthalate (PET) dominates the global plastic containers market. PET is widely used for packaging applications in food & beverages, pharmaceuticals, and personal care due to its excellent strength-to-weight ratio, clarity, chemical resistance, and recyclability.

The dominance of PET is especially pronounced in bottled water, soft drinks, and edible oil segments, where its lightweight nature and cost-effectiveness make it a preferred choice over glass and metal.

Furthermore, the growing global emphasis on sustainable packaging has led to an increased focus on recycled PET (rPET), further solidifying PET’s position as the leading material in the market. Governments and corporations are increasingly supporting bottle-to-bottle recycling initiatives, which enhances PET’s environmental credibility.

Polypropylene (PP) is the fastest-growing material segment, driven by its expanding use in food containers, medical packaging, and household goods. PP offers excellent moisture barrier properties, heat resistance, and flexibility, making it ideal for microwaveable food containers, yogurt tubs, medicine bottles, and personal care products.

Its durability and compatibility with advanced manufacturing technologies like injection molding and thermoforming support its growing adoption across multiple end-user industries.

Alcoholic to Exhibit Leading by Application

Alcoholic beverages hold the largest market share due to the global popularity of beer, spirits, and wine. Beverage packaging and processing equipment is heavily used for bottling, quality control, and hygiene.

High-volume production lines in breweries and distilleries ensure consistent demand. In addition, branding, premiumization, and new flavor introductions further support market growth. Stringent safety and cleanliness standards also necessitate advanced equipment and materials.

Ready-to-drink (RTD) beverages are the fastest-growing segment, driven by convenience, urban lifestyles, and health trends. This includes RTD teas, coffees, smoothies, and functional drinks targeting on-the-go consumers. Brands are investing in sleek packaging and innovative flavors to appeal to younger demographics.

Growth in e-commerce and vending machine channels fuels RTD demand. This segment also benefits from sustainability efforts, such as recyclable packaging and portion control.

Food & Beverages to Exhibit Leading by End-Use

The food & beverages segment holds the largest share in the global plastic containers market. This dominance is fueled by the extensive use of plastic containers in packaging bottled water, carbonated drinks, dairy products, sauces, snacks, and ready-to-eat meals.

The rising demand for lightweight, resealable, and cost-effective packaging especially in emerging markets with growing urban populations, continues to support this trend. Additionally, plastic containers provide excellent barrier properties, tamper-evident sealing, and extended shelf life, making them ideal for preserving food quality and safety.

Pharmaceuticals is the fastest-growing end-use segment, driven by the global expansion of the healthcare industry and increased demand for secure, sterile, and chemically resistant packaging. Plastic containers are widely used for storing tablets, capsules, syrups, and topical medications due to their durability, lightweight structure, and excellent protection against contamination and moisture.

Moreover, advancements in medical-grade polymers and compliance with regulatory standards (such as FDA and EU guidelines) are pushing pharmaceutical companies toward adopting high-performance plastic containers, particularly in regions like North America, Europe, and parts of Asia-Pacific.

Competitive Analysis

The global plastic containers market is becoming increasingly competitive, with the presence of several international, regional, and local players. Major companies compete based on product innovation, material sustainability, cost efficiency, and geographic reach.

Companies invest significantly in R&D to develop lightweight, recyclable, and biodegradable plastic containers to align with global sustainability trends and comply with tightening environmental regulations.

Mergers, acquisitions, and strategic partnerships are common in this space, as companies seek to expand their geographic presence, diversify product offerings, and integrate advanced technologies. For instance, many large players are acquiring smaller niche firms that specialize in bio-based or compostable plastic packaging, especially in the Asia Pacific and North American markets.

Moreover, global packaging firms are increasingly partnering with recycling companies and technology providers to strengthen their closed-loop recycling systems and improve circularity across their operations.

Sustainability and innovation are critical differentiators among market leaders. Companies are actively investing in rPET production, bioplastics, and lightweighting technologies to reduce material usage and carbon footprint.

The shift toward smart packaging including tamper-evident features, QR code tracking, and intelligent labeling, is also being explored, especially in pharmaceuticals and high-value food segments. Firms that can successfully integrate functionality with environmental compliance are likely to gain a long-term competitive edge.

Regional players in Asia Pacific, Latin America, and the Middle East are gaining traction by offering cost-effective solutions and capitalizing on growing local demand.

While global companies dominate the high-volume and innovation-driven segments, regional firms cater to localized preferences and regulatory landscapes. As the market matures, the competitive landscape is expected to shift increasingly toward players that offer eco-conscious products, efficient supply chains, and digital packaging solutions.

Key players in the plastic containers industry include Alpha Packaging Holdings Inc., Amcor, Bemis Company, Inc., CKS Packaging, Inc., Constar International LLC, Huhtamäki Oyj, Letica Corporation, Linpac Group Ltd., Sonoco Products Company, Plastipak Holdings Inc., and other notable companies.

Recent Development

- In July 2025, Dow launched its INNATE TF 220 BOPE precision packaging resin, a significant step toward improving the recyclability of flexible plastic packaging, which has traditionally been challenging to recycle. This innovative high-density polyethylene (HDPE) resin enables the creation of high-performance, biaxially oriented polyethylene (BOPE) films, addressing the industry's need to balance performance and recyclability.

(Source: https://www.ourmidland.com/news/article/dow-recyclable-packaging-resin-20403049.php)

- In June 2025, Versalis, a subsidiary of Italy's Eni, launched a demonstration plant in Mantua utilizing its proprietary Hoop® technology for chemical recycling of mixed plastic waste. This innovative process aims to transform mixed plastic waste into feedstock that can be used to produce new, high-quality plastic materials, including those suitable for food and pharmaceutical packaging, complementing traditional mechanical recycling methods.

(Source: https://www.reuters.com/sustainability/land-use- biodiversity/eni-unveils-plant-chemical-recycling-plastic-waste-2025-06-19)

Segmentation of Plastic Containers Market

-

By Packaging Type :

- Bags & Pouches

- Bottles & Jars

- Boxes & Cartons

- Containers (Plastic Containers & Metal Cans)

- Others (Cups, Tubs, and Bowls)

-

By Packaging Material :

- High Density Polyethylene (HDPE)

- Low Density Polyethylene (LDPE)

- Polyethylene Terephthalate (PET, PETE, PETG, Polyester)

- Polypropylene (PP)

- Polystyrene (PS)

- Polyvinyl Chloride (PVC)

- Others

-

By Application :

- Alcoholic Beverages

- Bottled Water

- Carbonated Soft Drinks

- Energy Drinks

- Milk Products

- Ready-to-Drink Beverages

- Tea/Coffee

-

By End-Use :

- Cosmetics & Personal Care

- Electronics

- Food & Beverages

- Pharmaceuticals

- Printing & Stationary

- Others

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the Global Plastic Containers Market size in 2025?

The plastic containers market is valued at USD 112.8 billion in 2025.

Who are the Major Players Operating in the Plastic Containers Market?

Prominent players in the market include Alpha Packaging Holdings Inc., Amcor, Bemis Company, Inc., CKS Packaging, Inc., and Constar International LLC.

What is the Estimated Valuation of the Plastic Containers Market by 2035?

The market is expected to reach a valuation of USD 187.3 billion by 2035.

What Value CAGR Did the Plastic Containers Market Exhibit Over the Last Five Years?

The growth rate of the plastic containers market is 4.4% from 2020-2024.

Author:

Shubham Patidar

Editor:

Naved Ahmed