Portable Air Compressor Market Outlook (2025 to 2035)

The portable air compressor market is valued at USD 1,780 million in 2025. As per Fact.MR analysis, the industry will grow at a CAGR of 4.1% and reach USD 2,660 million by 2035.

The year 2024 marked a period of consolidation and strategic repositioning for the global portable air compressor sector. Fact.MR research revealed that producers reacted to increased cost pressures by streamlining design-to-delivery cycles, especially for compact rotary screw and reciprocating models.

Such models gained acceptance in automotive repair shops and mid-sized construction facilities where mobility and dependability continued to be primary procurement concerns. A sharp increase in short-term rental activity was witnessed in Western Europe due to infrastructure rehabilitation projects following severe weather disruptions.

At the same time, North America moved more rapidly toward oil-free portable compressors due to energy efficiency regulations. The development compelled top OEMs to invest more in next-generation models that met strict emissions and noise-level standards.

Rather than focusing purely on production volume, most Tier-1 suppliers concentrated on securing environmental certifications and digital enhancements-especially in fleet applications that demand real-time monitoring and adaptive load management features.

Looking ahead 2025 and beyond, Fact.MR believes the industry will grow consistently at a 4.1% CAGR and reach USD 2,660 million by 2035. Development will be driven by growing infrastructure spending in Asia as well as tightening regulations in mature economies.

IoT-enabled monitoring, lightweight composite housings, and connectivity with predictive maintenance ecosystems will be the distinguishing factors, especially in mining, utilities, and disaster response applications. In addition, industrial energy audits will lead to a preference for compressors with high-efficiency ratings as well as modular expandability.

Key Metrics

| Metric | Value |

|---|---|

| Estimated Size in 2025 | USD 1,780 Million |

| Projected Size in 2035 | USD 2,660 Million |

| CAGR (2025 to 2035) | 4.1% |

Fact.MR Survey Results: Industry Dynamics Based on Stakeholder Perspectives

(Surveyed Q4 2024, n=500 stakeholder participants evenly distributed across manufacturers, distributors, rental operators, and end-users in the USA, Western Europe, Japan, and South Korea)

Key Priorities of Stakeholders

- Energy Efficiency: 85% of stakeholders globally identified compliance with energy efficiency standards as a "critical" priority, especially under tightening environmental regulations.

- Durability: 79% emphasized robust design (cast aluminum, powder-coated steel) as essential to withstand outdoor industrial conditions.

Regional Variance:

- USA: 72% highlighted remote start/stop capabilities and telemetry for fleet optimization, compared to only 38% in Japan.

- Western Europe: 83% cited low-noise models (<65 dB) as essential for urban deployment, versus 44% in South Korea.

- Japan/South Korea: 66% emphasized compactness and vertical stacking to minimize storage footprint, compared to 29% in the USA

Adoption of Advanced Technologies

High Variance:

- USA: 61% of fleet managers adopted IoT-enabled compressors with pressure/temperature analytics, especially in rental applications.

- Western Europe: 53% integrated VSD (Variable Speed Drive) compressors to optimize energy draw in dynamic load conditions.

- Japan: Only 24% used digital controls, citing over-specification for small-scale applications.

- South Korea: 39% used battery-powered portable models, mainly indoor or tunnel maintenance.

Convergent and Divergent Perspectives on ROI:

- 76% of USA stakeholders reported clear ROI from GPS tracking and load monitoring, whereas only 31% in Japan found such systems viable at scale.

Material Preferences & Sustainability Trends

Consensus:

- Powder-coated steel remained the material of choice (62% globally) for durability and corrosion resistance.

Variance:

- Western Europe: 49% preferred aluminum for lighter-weight mobility and easier recycling.

- Japan/South Korea: 43% preferred composite hybrids (steel frame with polymer casing) for compact urban operations.

- USA: 68% retained full steel frames for higher HP machines, but 21% showed a shift to aluminum for construction site mobility.

Price Sensitivity & Supply Chain Challenges

Shared Challenges:

- 91% cited rising raw material costs as a constraint - steel (+26%), aluminum (+19%) in 2024.

Regional Variance:

- USA/Western Europe: 59% expressed willingness to pay a 10-15% premium for electric or hybrid-drive models.

- Japan/South Korea: 74% favored low-cost models under USD 3,000, with interest in second-hand imports.

- South Korea: 48% preferred leasing options or usage-based rental models, compared to only 20% in the USA

Pain Points in the Value Chain

Manufacturers:

- USA: 57% struggled with labor shortages in skilled assembly and electronics integration.

- Western Europe: 51% faced regulatory documentation hurdles tied to CE marking and energy labeling.

- Japan: 62% cited domestic demand stagnation due to declining infrastructure expansion.

Distributors:

- USA: 68% cited port delays affecting component lead times.

- Western Europe: 54% flagged rising competition from lower-cost Eastern European imports.

- Japan/South Korea: 63% cited inconsistent delivery cycles in mountainous or remote regions.

End-Users (Construction Firms, Workshops, Utilities):

- USA: 41% noted recurring maintenance costs as a primary concern.

- Western Europe: 38% found noise restrictions limiting usage hours in urban zones.

- Japan: 56% reported a lack of product support for digital features and interface troubleshooting.

Future Investment Priorities

Alignment:

- 72% of global OEMs and rental providers planned to increase R&D in battery-powered and electric-drive compressors.

Divergence:

- USA: 63% plan to invest in telematics integration to enable preventive maintenance.

- Western Europe: 58% in ultra-low noise variants for city operations.

- Japan/South Korea: 47% in modular, stackable units to meet site-specific space constraints.

Regulatory Impact

- USA: 69% cited state-level noise and engine emissions policies (e.g., California CARB) as highly disruptive to product planning.

- Western Europe: 82% reported the EU’s Zero Pollution Action Plan as a clear driver toward low-emission portable compressors.

- Japan/South Korea: Only 34% found national regulations impactful on buying behavior due to lax enforcement and limited inspection cycles.

Conclusion: Variance vs. Consensus

- High Consensus: Efficiency, durability, and cost escalation are central concerns across geographies.

Key Variances:

- USA: Leads in telematics and large-fleet optimization; Japan/South Korea: Seek compact and affordable alternatives.

- Western Europe: Prioritizes low-noise and recyclable materials under strong regulatory pressure.

- Strategic Insight: Portfolios must align to regional constraints-mobility and emissions in the EU, cost and space in Asia, and connectivity and fleet ROI in the USA

Impact of Government Regulation

| Country | Policy & Regulatory Impact |

|---|---|

| United States | State-level air quality regulations, especially in California (CARB), mandate low-emission engines for portable compressors. OSHA requires compliance with noise exposure limits and safety protocols. EPA Tier 4 Final certification is mandatory for diesel-powered units above 25 HP. |

| Germany | The EU's Zero Pollution Action Plan and Ecodesign Directive drive the adoption of energy-efficient, low-noise compressors. CE Marking and compliance with EN ISO 12100 (safety of machinery) are mandatory for distribution. Noise emissions must also conform to the 2000/14/EC directive. |

| France | Follows the EU environmental compliance framework. REACH, and RoHS directives regulate material content, and compressors must-have CE markings. Local noise emission ordinances in urban zones drive demand for quieter units. |

| United Kingdom | Post-Brexit, UKCA (UK Conformity Assessed) marking has replaced CE marking. Products must also comply with the Supply of Machinery (Safety) Regulations 2008. The focus is increasing on the decarbonization of industrial machinery. |

| Italy | Enforcement of CE and Machinery Directive 2006/42/EC is strict. Urban deployment requires low-noise certification under directive 2000/14/EC. Fiscal incentives exist for adopting energy-efficient models under Italy's Transition Plan 4.0. |

| South Korea | Regulations on engine emissions under the Clean Air Conservation Act promote electric-driven compressors. No mandatory certification exists for portable compressors yet, but compliance with KC (Korea Certification) for electrical safety is required. |

| Japan | No compressor-specific federal emission laws, but voluntary efficiency standards apply under the Energy Conservation Act. PSE (Product Safety Electrical Appliance & Materials) certification is mandatory for electric compressors. Local governments may impose noise and use restrictions in residential zones. |

| Australia | National Environment Protection Measures (NEPM) guide emissions compliance. Compliance with Australian Standard AS 1210 (for pressure equipment) and mandatory RCM (Regulatory Compliance Mark) labeling for electrical compressors. Local environmental protection agencies regulate noise limits. |

Market Analysis

The industry is entering a phase of steady, efficiency-driven growth, supported by rising infrastructure development and stricter environmental regulations worldwide. Demand is being propelled by the need for compact, mobile, and energy-efficient equipment across the construction, automotive, and utility sectors. Manufacturers offering digitally integrated, low-emission models stand to gain the most, while legacy systems lacking compliance features risk being phased out.

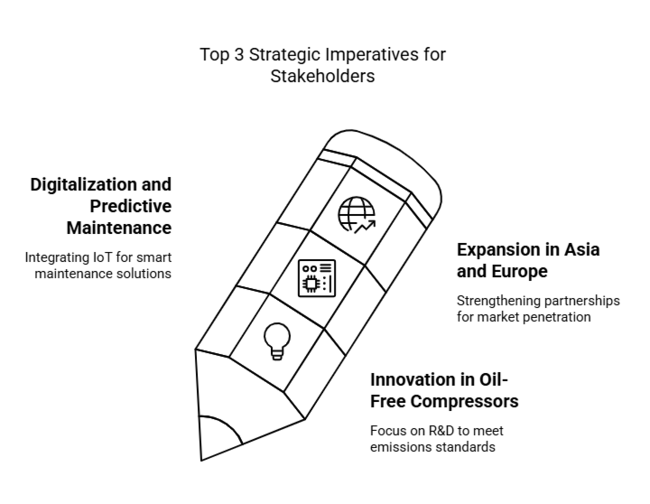

Top 3 Strategic Imperatives for Stakeholders

Accelerate Innovation in Oil-Free and Hybrid Compressor Models

Executives should prioritize R&D investments in oil-free and hybrid portable compressors to meet tightening global emissions standards and capture demand from energy-conscious sectors such as healthcare, food processing, and precision manufacturing.

Align Offerings with Digitalization and Predictive Maintenance Trends

To stay relevant in evolving industrial ecosystems, companies must embed IoT capabilities and remote diagnostics into product lines. This will ensure alignment with client preferences for smart, data-driven maintenance solutions and reduce the total cost of ownership.

Strengthen Channel Partnerships in Asia and Rental Ecosystems in Europe

With infrastructure spending surging across Asia and rental usage rising in Europe, executives should expand distribution networks, build localized service hubs, and explore joint ventures or acquisitions to deepen regional penetration and scale responsiveness.

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability & Impact |

|---|---|

| Regulatory Compliance Costs - Stricter noise and emissions regulations in urban and industrial zones may elevate compliance costs and delay approvals for non-certified models. | High Probability, High Impact |

| Raw Material Price Volatility - Fluctuations in steel, aluminum, and lithium prices could compress margins and disrupt production planning, especially for companies without robust procurement hedging strategies. | Medium Probability, High Impact |

| Supply Chain Disruptions - Port congestion, geopolitical instability, or critical component shortages may affect inventory availability and delay deliveries, especially in export-reliant industries. | Medium Probability, Medium Impact |

Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Evaluate Low-Emission Portfolio Gaps | Run feasibility on sourcing components for oil-free and hybrid models |

| Customer-Centric Product Design | Initiate OEM feedback loop on digital monitoring and predictive maintenance features. |

| Channel Expansion Strategy | Launch aftermarket channel partner incentive pilot in rental-heavy regions |

For the Boardroom

To stay ahead, companies must pivot toward high-efficiency, digitally integrated, and regulation-ready product lines. This intelligence signals a clear need to fast-track the development of oil-free and hybrid models while embedding smart diagnostics to meet growing industrial automation demands.

Over the next 12 months, the strategic focus should shift toward strengthening rental ecosystems in Europe and expanding supply chain localization in Asia. Aligning R&D with sustainability mandates and customer-centric features will not only future-proof portfolios but also unlock access to high-growth verticals like utilities, disaster response, and precision manufacturing.

Segment-wise Analysis

By Design

The rotary screw type is expected to be the fastest growing segment with a CAGR of 4% during the assessment term, driven by increasing demand for reliable and efficient equipment across industries. Rotary screw compressors are known for their continuous operation, making them ideal for commercial and industrial use where reliability is crucial.

The demand is particularly high in sectors like automotive, construction, and manufacturing due to their ability to operate for extended periods without overheating. With advancements in efficiency and energy-saving technologies, this segment is projected to maintain steady growth.

Despite competition from other types, the rotary screw design remains dominant because of its ease of maintenance and consistent performance, which justifies its higher initial investment. This segment will continue to lead the industry, especially in North America and Europe, where industrial applications drive significant demand.

By Lubrication

The oiled segment will be most profitable, growing at a CAGR of 4.2%. These units are ideal for continuous operation and heavy-duty applications, where the lubrication helps reduce friction and extend the lifespan of the components.

Oiled compressors are preferred in industrial settings where large volumes of compressed air are required over long periods. This segment benefits from the demand for high-performance, long-lasting equipment in industries like manufacturing, construction, and mining.

However, environmental regulations and a growing preference for oil-free alternatives may moderate the pace of growth. Still, their reliability and cost-effectiveness in high-demand environments keep the segment robust.

By Drive Type

The electric drive type segment will be most lucrative, at a CAGR of 4.5% during the forecast period. Electric-powered units are increasingly preferred due to their energy efficiency, lower operational costs, and ease of integration into various settings, including manufacturing, construction, and residential applications.

The push towards renewable energy and energy-efficient solutions in industrial processes is driving the demand for electric-powered compressors. Additionally, technological improvements are enhancing the performance of electric air compressors, making them more versatile and capable of handling heavy-duty tasks.

This trend will continue to drive growth, especially in regions like Europe and North America, where energy regulations are becoming more stringent.

By End-use

The automotive sector is projected to grow fastest at a CAGR of 4.8% from 2025 to 2035. Air compressors are essential in the automotive industry for tire inflation, vehicle maintenance, and pneumatic tools.

With the rise of electric vehicles (EVs) and the expansion of vehicle maintenance centers, demand for air compressors in the automotive sector will continue to grow. Furthermore, as vehicle manufacturing processes become more automated, the need for reliable, high-performance compressors in assembly lines is increasing.

This segment is expected to benefit from ongoing developments in automotive technology, including electric vehicles, where compressors are used for various applications like air suspension systems and pneumatic controls.

Country-wise Insights

USA

The industry in USA is projected to grow at a CAGR of 4.5% during the 2025 to 2035 period. The USA is a significant hub for air compressors, driven by key industries like construction, oil & gas, and automotive. The increasing demand for energy-efficient and low-emission models is bolstered by stringent environmental regulations such as the EPA’s Tier 4 Final emissions standards for diesel compressors.

Moreover, state-specific mandates, such as California's strict air quality regulations, are driving the adoption of greener technologies. The industry is also influenced by the increasing trend of automation in industries, particularly in construction and manufacturing. Another driver is the growing adoption of IoT-enabled compressors, providing real-time data for efficient maintenance and monitoring.

UK

The UK’s sales is expected to grow at a CAGR of 4.0% during the period. Post-Brexit, the UK industry is changing certification and compliance processes, particularly with the introduction of the UKCA (UK Conformity Assessed) mark, replacing the CE mark for certain products.

The growing emphasis on green technology and energy efficiency is driving the demand for low-emission, electrically driven models. The government's commitment to achieving net-zero carbon emissions by 2050, along with its strict environmental policies, is expected to influence industry dynamics significantly.

France

Driven by the European Union’s focus on environmental sustainability, France is expected to see increased demand for energy-efficient, low-emission compressors. French regulations align with EU directives like Ecodesign and the Zero Pollution Action Plan, pushing manufacturers toward greener solutions. France’s sales is projected to grow at a CAGR of 3.9% from 2025 to 2035.

The construction industry in France, a major consumer, is shifting toward automation and sustainable machinery, fostering the use of electric and hybrid systems. Additionally, France’s focus on carbon-free production processes, such as utilizing green steel, is expected to boost demand for energy-efficient equipment. French manufacturers are also benefiting from governmental initiatives promoting infrastructure upgrades and environmental compliance.

Germany

Germany’s revenue for the industry is expected to experience a CAGR of 4.3% in the industry from 2025 to 2035. As the largest economy in Europe, Germany is at the forefront of adopting cutting-edge technologies, including energy-efficient and automated equipment. The country’s strict environmental regulations, including the EU’s Ecodesign Directive and noise emission standards, are pushing for the development and deployment of quieter, low-emission compressors.

The construction and automotive sectors are major drivers, with growing demand for automation and Industry 4.0 technologies contributing to higher adoption rates. The trend toward electric-powered and hybrid compressors is becoming more prominent as industries aim to reduce their carbon footprints. Germany benefits from a well-established manufacturing base, focusing on high-quality, durable machinery, making it an attractive region for both domestic and international players.

Italy

The Italian Government’s Transition Plan 4.0 is offering fiscal incentives for businesses adopting green technologies, boosting demand for eco-friendly systems. Italy’s manufacturing sector is also increasingly focusing on modular designs, contributing to higher versatility and lower operating costs. The demand is driven by the country’s strong infrastructure and ongoing construction projects.

The industry in Italy is expected to witness a CAGR of 4.1% during the 2025 to 2035 forecast period. Driven by both domestic demand and the country’s participation in the EU’s green energy transition, Italy is focused on adopting energy-efficient, low-emission technologies. With the EU's Ecodesign Directive, Italy is under pressure to push for quieter, more energy-efficient solutions, especially in sectors like construction, automotive, and manufacturing.

South Korea

The country has an increasing focus on sustainability, with the government encouraging eco-friendly technologies through subsidies and incentives. Additionally, rising demand for automated dairy farms and robotic systems in agriculture is pushing for advanced solutions. However, the industry faces challenges such as the high cost of advanced technologies, which may deter smaller businesses.

South Korea’s portable air compressor industry is anticipated to grow at a CAGR of 4.2%. As one of the leading industrial hubs in Asia, South Korea is witnessing a rise in automation and IoT integration, driving demand for advanced systems. The construction and automotive industries are major drivers of growth, as both sectors demand high-performance, energy-efficient solutions.

Japan

The landscape in Japan has relatively high penetration levels of automated and energy-efficient equipment. Growth may be slower in comparison to other regions, however, due to the high front-end investment necessary and the affinity for smaller manual systems in numerous rural communities. Japan’s sales is projected to expand at a CAGR of 3.8% during the forecast period.

The construction industry and agriculture sectors are still top consumers. With the government placing emphasis on a carbon-free society by the year 2050, energy-efficient and low-emission technology is gaining traction.

Even in the face of challenges like high expenditure on cutting-edge systems and low uptake of IoT and robotics systems in the countryside, Japan is likely to develop moderately as it transitions towards more energy-efficient and automated options.

China

As China advances on the path to a green economy, there is growing focus on energy efficiency and low-emission technologies. Government efforts to enhance sustainable infrastructure and minimize pollution will fuel demand for systems that adhere to new environmental standards. The industry in China is expected to expand at a CAGR of 5.0% during the assessment period, fueled by fast-paced industrialization and urbanization.

Besides, China's increased demand for construction and farm machinery automation as well as robot-based solutions is helping fuel growing technology adoption. Its large-scale infrastructure development as well as substantial industrial base also help fuel demand. But supply chain interruptions as well as increases in raw materials are potentially factors to influence cost. Despite these obstacles, China’s industrial growth and sustainability focus make it a lucrative region.

Competitive Landscape

The portable air compressor industry remains moderately fragmented, with a mix of global players and regional manufacturers competing on technology, pricing, and distribution strength. However, recent M&A activity indicates a gradual shift towards consolidation, especially among North American and European manufacturers.

Top companies are actively competing through pricing differentiation, innovation in energy-efficient models, and strategic partnerships to expand regional footprints. Innovation is centered around cordless, oil-free, and low-noise compressor technologies to meet rising industrial and residential demand. Key players are focusing on expanding service networks, forming joint ventures, and enhancing aftersales offerings to retain customers and capture new segments.

Atlas Copco has been aggressively expanding its footprint. In February 2024, it acquired National Pump & Compressor’s air compressor division in the USA to bolster its rental service presence in North America. This move reflects Atlas Copco’s dual-pronged strategy of expanding both sales and rental channels.

Ingersoll Rand, another major player, announced in April 2024 its acquisition of Howden Roots from Chart Industries for USD 300 million to strengthen its industrial air business, especially in process industries. The acquisition is set to improve product breadth and boost its global competitiveness through synergies in engineering and aftermarket services.

Doosan Portable Power has focused on technological upgrades, launching a new line of Tier 4 Final portable compressors in March 2024 with enhanced fuel efficiency and remote diagnostics. This aligns with tightening emission standards and rising demand for greener alternatives across Europe and North America.

Meanwhile, Sullair (a Hitachi Group company) formed a strategic partnership with Sunbelt Rentals in early 2024 to supply a new fleet of electric-powered portable compressors across the USA, accelerating its move toward electrification.

Market Share Analysis

Atlas Copco (18-22%)

Atlas Copco will dominate with its energy-efficient, IoT-connected compressors. Robust R&D, complemented by a vast global supply chain, will make it a commanding force in major industries such as automotive as well as construction. The firm will grow its industry share by offering advanced, sustainable solutions for multiple sectors.

Ingersoll Rand (15-18%)

Ingersoll Rand will concentrate on taking advantage of its robust industrial footprint as well as expanding portfolio of IoT-compressed machinery. With ongoing innovation, the company will enter new emerging industries, exploiting increasing demand for energy-efficient solutions and intelligent technology integration, setting it up for stable growth during the forecast period.

Kaeser Compressors (12-15%)

Kaeser will concentrate on creating sustainable, hydrogen-capable compressors and focusing on regions in which energy efficiency as well as long-term costs are the most important. Its dedication to innovation, especially in renewable energy, will enable it to enhance its share, especially in the European as well as North American regions.

Sullair (Hitachi) (10-12%)

Sullair will continue to expand its presence in the Asia-Pacific region, especially with its oil-free compressors, which are increasingly in demand. With the backing of Hitachi, the company will most likely diversify its product offerings and further consolidate its grip in global construction and industrial industries, driving expansion in key industries.

Doosan Portable Power (8-10%)

Doosan will be looking to witness growth in the construction and mining industries, especially in emerging industries. The focus of the company on long-lasting and high-performance compressors will increase its share in industries needing robust, heavy-duty equipment for infrastructure development and industrial uses.

Makita (6-8%)

Makita will take advantage of increasing demand for cordless, portable compressors, particularly in the do-it-yourself and small business industries. Through its strong product line and emphasis on user convenience, Makita will establish itself as a leading contender for compact, portable solutions in consumer and industrial industries.

Other Key Players

- Cummins

- Gardner Denver

- Hitachi

- Fusheng

- Boge Compressors

- Hyundai Heavy Industries

- Airman

- Lonking

- Mi-T-M Corporation

- Pneumatech

- Quincy Compressor

- United Rentals

- Chicago Pneumatic

- Wuxi Pioneering Compressors

- ELGi's

- Bac Compressors

- Rolair Systems

- TEWATT

- Sumake Industrial Co., Ltd.

- REMEZA

- Zycon

Portable Air Compressor Market Segmentation

By Design:

- Rotary Screw Type

- Rotary Centrifugal

- Reciprocating Type

By Lubrication:

- Oiled

- Oil-Free

By Drive Type:

- Electric

- Diesel Powered

By End-Use:

- Automotive

- Aerospace

- Oil & Gas

- Building & Construction

- Mining

- Power Generation

- Others (Defense, Research etc.)

By Region:

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- Middle East & Africa

- Frequently Asked Questions -

What is the expected industry size of portable compressors by 2035?

The expected industry size is USD 2,660 million by 2035.

What factors influence demand for portable air compressors?

The demand for portable air compressors is influenced by factors such as industrial growth, construction projects, technological advancements, and energy efficiency needs.

Which segment grows fastest by design?

Rotary screw compressors, due to durability and continuous operation.

Why are electric-driven compressors gaining popularity?

They're energy-efficient and align with stricter environmental standards.

Which end-use industry leads in growth?

The automotive sector, fueled by EV expansion and maintenance demand.

Author:

Shubham Patidar

Editor:

Naved Ahmed