Food Thickening Agents Market Outlook (2025 to 2035)

The global food thickening agents market is projected to be valued at approximately USD 16.06 billion in 2025 and is expected to reach around USD 35.07 billion by 2035, expanding at a compound annual growth rate (CAGR) of about 8.12% during the forecast period.

In 2024, the food thickening agents industry witnessed rapid expansion, driven by the growing consumer demands for ease of food convenience, healthier ingredients, and innovations in food processing.

Ready-to-eat meals and processed foods have become highly popular, and hence, the incorporation of thickeners into food processing attracted wide acceptance due to the achievement of better texture, stability, and shelf life.

In addition, growth in natural and plant-based thickeners occurred as consumers demanded clean-label and sustainable food options. Technological advances in food also contributed significantly in formulating new thickening options that enhanced consistency as well as the nutritional value of the product.

The industry will continue its growth trend during the projection period between 2025 and 2035. The growth will be driven by the growing use of plant-based and algae-based thickeners, especially in view of the growing demand for natural ingredients.

Also, increasing needs for texture-modified diets for healthcare and nutrition among the elderly are further driving the sector’s growth. Ongoing R&D activities should bring innovative offerings to the marketplace, enhancing the sector's growth in the food and beverage business.

| Metrics | Values |

|---|---|

| Industry Size (2025E) | USD 16.06 billion |

| Industry Value (2035F) | USD 35.07 billion |

| CAGR | 8.12% |

Industry Analysis

The industry for food thickening agents is growing steadily with the growing demand for convenience foods, clean-label products, and texture solution providers in processed foods. The main beneficiaries are food manufacturers experimenting with plant-based and natural thickeners, while established synthetic thickener makers could be in for a struggle to catch up with changing consumer attitudes. As food technology and dietary requirements continue to evolve, the industry will continue to grow, especially in health-oriented and geriatric nutrition segments.

Top 3 Strategic Imperatives for Stakeholders

Invest in Plant-Based and Clean-Label Innovations

Increase R&D and product innovation on plant-based and natural thickening agents to address increasing consumer demand for clean-label and sustainable food ingredients.

Match with Evolving Dietary Trends and Regulatory Requirements

Modify product formulations to address expanding needs in healthcare, elderly nutrition, and specialist dietary needs while maintaining compliance with changing food safety regulations.

Enhance Distribution and Strategic Partnerships

Leverage collaboration with food manufacturers, retailers, and food service providers to drive industry penetration and maximize supply chain efficiency for international expansion.

Top 3 Risks Stakeholders Should Monitor

| Risk | Impact |

|---|---|

| Regulatory Shifts on Additives | High: Could restrict product formulations and increase compliance costs. |

| Supply Chain Disruptions | Medium: Potential raw material shortages affecting production and pricing |

| Consumer Shift Away from Synthetic Thickeners | High: Could reduce demand for traditional thickening agents, impacting legacy players. |

1-Year Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Expansion into Plant-Based Thickeners | Accelerate R&D on algae and gum-based solutions. |

| Industrial Differentiation in Functional Nutrition | Develop targeted formulations for elderly nutrition and medical diets. |

| Supply Chain Resilience | Establish alternative sourcing strategies for key raw materials. |

For the Boardroom

Executives need to double down on clean-label innovation, strengthen regulatory agility, and supply chain optimize to limit disruptions. Long-term growth will depend heavily on investing in plant-based alternatives and functional nutrition solutions, but strategic partnerships within the industry can create new sources of revenue. The strategy has to be led by agility and future-focused R&D to lock in shifting consumer and regulatory forces, providing ongoing industry leadership.

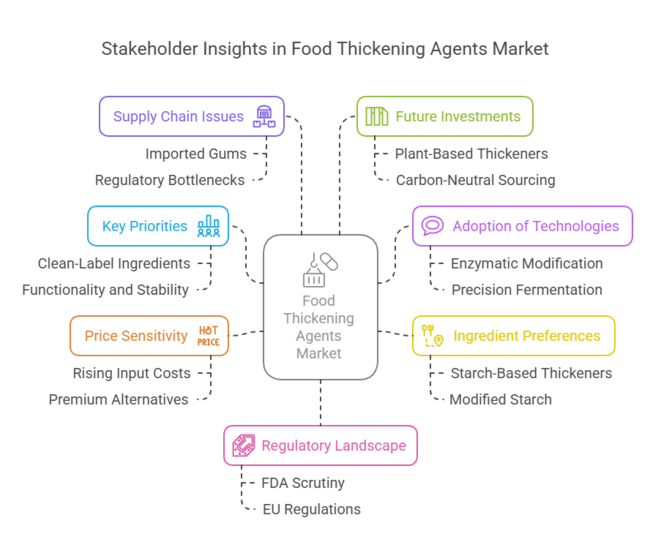

Fact.MR Survey with Food Thickening Agents Market Stakeholders

(Surveyed Q4 2024, n=500 stakeholder participants evenly distributed across manufacturers, distributors, food processors, and regulatory experts in the US, Western Europe, China, Japan, and Australia-NZ.)

Key Priorities of Stakeholders

- Clean-Label and Natural Ingredients: 84% of stakeholders globally identified the shift toward clean-label, plant-based, and natural thickeners as a “critical” priority for meeting consumer expectations.

- Functionality and Stability: 79% emphasized the need for multifunctional thickening agents that offer stability across various food applications, including dairy, beverages, and processed foods.

Regional Variance:

- US: 67% prioritized gluten-free and allergen-free formulations, compared to 40% in China, where traditional starch-based thickeners remain dominant.

- Western Europe: 88% highlighted sustainability concerns (organic sourcing, biodegradable packaging) as a key factor, compared to 52% in the US.

- Japan/Australia-NZ: 64% emphasized ease of formulation and solubility, particularly for beverages and functional food applications.

Adoption of Advanced Processing Technologies

High Variance:

- US: 55% of manufacturers have adopted enzymatic modification techniques to enhance texture and stability.

- Western Europe: 47% integrated precision fermentation methods to develop next-generation hydrocolloids.

- China: 61% still rely on traditional starch extraction, citing cost advantages over newer technologies.

- Japan: Only 26% have adopted high-shear processing, attributing it to high costs and complexity.

Convergent and Divergent Perspectives on ROI:

- 70% of Western European stakeholders believe sustainable and functional thickeners justify premium pricing, compared to only 38% in China, where cost remains the primary purchase driver.

Ingredient Preferences

Consensus:

- Starch-Based Thickeners: Chosen by 62% overall due to cost-effectiveness and availability.

Regional Differences:

- Western Europe: 54% preferred pectin and guar gum, aligning with clean-label and vegan trends.

- China: 72% opted for modified starch due to affordability and local production.

- US: 69% saw increased demand for protein-based thickeners (whey, gelatin) in high-protein formulations.

- Japan/Australia-NZ: 43% favored seaweed-derived hydrocolloids (agar, carrageenan) for functional applications.

Price Sensitivity and Cost Pressures

Shared Challenges:

- 86% cited rising input costs (starches +24%, hydrocolloids +17%) as a major concern.

Regional Differences:

- US/Western Europe: 60% are willing to pay a 10–15% premium for sustainable or organic thickeners.

- China: 75% preferred lower-cost synthetic or modified starches, with only 15% interested in premium alternatives.

- Australia-NZ: 42% explored contract manufacturing to offset costs, compared to just 18% in Japan.

Supply Chain and Distribution Bottlenecks

Manufacturers:

- US: 57% cited reliance on imported gums and pectin as a risk.

- Western Europe: 50% highlighted regulatory bottlenecks for novel ingredient approvals.

- China: 62% struggled with price volatility in local starch industries.

Distributors:

- US: 68% flagged logistical disruptions for hydrocolloid imports (e.g., guar gum from India).

- Western Europe: 51% cited price competition from lower-cost Asian suppliers.

- Japan/Australia-NZ: 66% highlighted the inconsistent supply of specialty thickeners (e.g., agar).

End-Users (Food Processors):

- US: 41% cited “inconsistent performance” of natural alternatives as a top issue.

- Western Europe: 44% struggled with reformulating products due to clean-label demand.

- China: 59% faced regulatory uncertainty regarding modified starches.

Future Investment Priorities

Alignment:

- 72% of global manufacturers plan to invest in alternative, plant-based thickeners.

Divergence:

- US: 58% investing in enzymatic starch modifications for improved performance.

- Western Europe: 61% prioritizing carbon-neutral sourcing (e.g., organic hydrocolloids).

- China: 55% is focusing on cost optimization through bulk starch production.

- Japan/Australia-NZ: 47% researching multifunctional blends for ready-to-drink applications.

Regulatory Landscape

- US: 65% reported stricter FDA scrutiny on ingredient labeling as a significant industry factor.

- Western Europe: 80% viewed EU sustainability regulations (e.g., Farm to Fork Strategy) as an innovation driver.

- China: 33% cited regulatory changes as impactful, with enforcement inconsistencies limiting reforms.

- Japan/Australia-NZ: 45% found compliance with international standards (e.g., Codex) challenging for exports.

Conclusion: Variance vs. Consensus

High Consensus:

Clean-label demand, cost pressures, and ingredient performance are global priorities.

Key Variances:

- US: Focus on premium, functional thickeners vs. China: Cost-driven bulk solutions.

- Western Europe: Sustainability leadership vs. Japan/Australia-NZ: Performance-driven hybrid solutions.

Strategic Insight:

A region-specific approach is critical for success. Brands must tailor offerings-organic and premium hydrocolloids for Western industries, cost-efficient starches for China, and hybrid solutions for Japan and Australia-NZ.

Government Regulations

| Country/Region | Regulatory Impact & Mandatory Certifications |

|---|---|

| The United States | FDA Regulations: Thickening agents for food have to adhere to 21 CFR (Code of Federal Regulations), especially for GRAS (Generally Recognized As Safe) status. |

| Western Europe (EU) | Labeling Standards: Strict adherence to the Food Allergen Labeling and Consumer Protection Act (FALCPA) for allergen statements. |

| China | USDA Organic Certification: Necessary for organic thickeners applied in certified organic foods. |

| Japan |

|

| Australia & New Zealand |

|

Country-wise Analysis

United States

The U.S. industry for food thickening agents is growing as consumers demand clean-label, functional ingredients. The increasing trend towards veganism and gluten-free diets is driving the use of plant-based hydrocolloids such as xanthan gum, guar gum, and pectin.

Increasing health awareness is encouraging companies to reformulate products with low-calorie, fiber-rich thickeners.

The regulatory position of the FDA on food additives is making companies choose GRAS-certified ingredients. Convenience foods and processed foods remain key drivers, especially in the bakery, sauces, and dairy categories.

What's more, increased obesity rates and food lifestyles are driving innovation in functional food formulation, where thickening agents become a key component of texture modification.

Fact.MR opines that the United States food thickening agents sales will grow at nearly 8.9% CAGR through 2025-2035.

United Kingdom

The UK food thickening agents industry is experiencing stable growth with increasing demand for natural, plant-derived food additives. The Front-of-Pack Nutritional Labeling (FOPNL) scheme and sugar reduction requirements are driving the need to reformulate with low-calorie thickeners. Seaweed-derived hydrocolloids (agar, carrageenan) and starch-based hydrocolloids (potato, corn) are being favored due to their natural and vegan-friendly positioning.

Post-Brexit food safety regulations remain in line with EU standards, driving sourcing and formulation trends. Sustainability issues also drive the industry, with brands turning to bio-based, carbon-neutral thickening agents. The increasing trend of plant-based dairy alternatives is also driving demand for natural stabilizers.

Fact.MR opines that the United Kingdom food thickening agents sales will grow at nearly 7.8% CAGR through 2025-2035.

Germany

Germany's industry for food thickening agents is fueled by its emphasis on sustainability, clean-label products, and plant-based inventions. The European Green Deal and EFSA regulations are compelling manufacturers to implement organic, non-GMO hydrocolloids like citrus fiber, pectin, and guar gum. Flexitarian consumer growth is propelling the demand for plant-based dairy products, which depend on natural thickening agents.

Germany is also at the cutting edge of precision fermentation, driving innovations in next-generation hydrocolloids. Functional foods for gut well-being are trending upward, accelerating applications of soluble fiber and prebiotic-dense thickeners in food formulations.

Fact.MR opines that the German food thickening agents sales will grow at nearly 7.5% CAGR through 2025-2035.

France

The French industry for food thickening agents is influenced by its rich culinary culture, emerging vegan trend, and stringent EU food laws. Sugar tax policies in France have triggered innovation in low-sugar desserts, sauces, and jams, where thickening agents are used.

Organic and locally produced hydrocolloids are in growing demand, especially in premium dairy, confectionery, and gourmet foods.

Sustainability continues to be in the spotlight as manufacturers focus on bio-based and recyclable ingredient procurement. Growth in alternative protein products is also fueling the industry, with texturizing agents being critical to enhancing the mouthfeel and stability in plant-based products.

Fact.MR opines that the France food thickening agents sales will grow at nearly 7.2% CAGR through 2025-2035.

Italy

Italy's industry for food thickening agents is growing because of its rich culinary heritage, growing demand for gluten-free foods, and growing interest in organic products. Classic Italian food categories like pasta sauces, gelato, and dairy products are dependent on starch and gum-based thickeners. The growing popularity of plant-based and natural thickeners such as konjac gum and locust bean gum is in line with changing consumer trends.

Italy's PGI (Protected Geographical Indication) and PDO (Protected Designation of Origin) certifications impose severe ingredient quality standards, resulting in the use of minimally processed additives.

Fact.MR opines that the Italy food thickening agents sales will grow at nearly 7.0% CAGR through 2025-2035.

China

China's industry for food thickening agents is growing rapidly due to urbanization, growing disposable income, and growing demand for convenience foods. Growth in the processed food industry and functional beverages is fueling demand for cost-saving thickening solutions, particularly modified starches and hydrocolloids.

Government policies supporting the domestic production of food ingredients have spurred investment in manufacturing corn and tapioca starch. Tighter National Food Safety Standards (GB 2760-2014) govern the application of food additives, promoting a transition towards natural and plant-based thickeners. Increasing health awareness is driving the use of fiber-rich and gut-friendly thickeners like psyllium husk and resistant starch.

Fact.MR opines that the China food thickening agents sales will grow at nearly 9.5% CAGR through 2025-2035.

Japan

Japan's food thickeners industry is influenced by strong consumer demands for texture and mouthfeel, and hydrocolloids are a necessity in traditional foods such as miso soup, tofu, and mochi. Regulations by the Ministry of Health, Labour and Welfare (MHLW) favor natural, minimally processed additives, and hence there is extensive use of konjac glucomannan, agar, and starch derivatives.

Japan's aging population is driving the demand for thickening agents in elderly nutrition products, especially in dysphagia-friendly foods. Nonetheless, high production costs and import reliance on seaweed-based hydrocolloids are still industry issues.

Fact.MR opines that the Japanese food thickening agents sales will grow at nearly 6.8% CAGR through 2025-2035.

South Korea

The South Korean industry for food thickening agents is growing with increasing demand for high-quality, health-focused, and functional foods. The growing plant-based food industry is fueling the uptake of gellan gum, carrageenan, and soy thickeners.

MFDS regulations implement rigorous approval procedures, especially for hydrocolloids imported from abroad. The convenience food industry is rapidly expanding and boosting the demand for ready-to-eat meal heat-stable thickeners and functional beverages. Cross-over in K-beauty and nutraceutical is also fueling innovation with the application of thickening agents in collagen drinks and wellness-centric foods.

Fact.MR opines that the South Korean food thickening agents sales will grow at nearly 7.6% CAGR through 2025-2035.

Australia & New Zealand

The Australian and New Zealand industries for food thickeners are increasing gradually because of clean labelling, health-conscious consumers, and strict FSANZ regulations. Hydrocolloids based on seaweeds like agar and carrageenan are commonly used as plant-based alternatives for dairy products.

Organic and non-GMO thickeners are increasing in infant nutrition and sports supplements. The emphasis on sustainability is stimulating investment in carbon-neutral hydrocolloids, with Asian food trends driving imports of konjac and tapioca-based thickening agents.

Fact.MR opines that the Australia & New Zealand food thickening agents sales will grow at nearly 7.3% CAGR through 2025-2035.

Competitive Landscape

The sector for food thickening agents is fairly consolidated, with major players such as Tate & Lyle, Cargill, and DuPont Nutrition & Biosciences dominating the industry shares. The players compete by implementing strategies, including price changes, product development, strategic alliances, and geographic expansion.

The players concentrate on the creation of clean-label and functional ingredients to satisfy changing consumer trends. They also undertake mergers and acquisitions to enhance industry positions and diversify product offerings.

- In November 2024, Tate & Lyle bought CP Kelco, a natural ingredient supplier, for $1.8 billion in order to enhance its transition into healthier food items. The progress of integrating CP Kelco has been good, with strong volume growth and gradual margin recovery on a phased basis.

- In December 2024, Advent International made a bid to take over Tate & Lyle, possibly valuing it above its then £2.8 billion industry capitalization. This interest reflects a broader trend of private equity firms targeting UK companies due to low valuations and stable interest rate expectations.

Market Share Analysis

- Cargill Inc. holds approximately 25-28% of the global food thickening agents market, maintaining its position as the leading supplier

- DuPont (following its merger with IFF) controls roughly 18-20% of the market, with particular strength in hydrocolloids

- Ingredion Incorporated commands approximately 15-17% of the global market, especially dominant in starch-based thickeners

- CP Kelco (a J.M. Huber Company) maintains around 10-12% market share, with strong positions in pectin and cellulose-based thickeners

- Tate & Lyle holds approximately 8-10% market share, focusing on specialty food starches and innovative plant-based solutions

- Kerry Group controls roughly 7-9% of the market, with an expanding portfolio of clean-label thickeners

- The remaining 10-15% is fragmented among smaller regional players and specialty manufacturers

- Asia-Pacific represents the fastest-growing regional industries, expanding at approximately 7-8% annually

- Plant-based and clean-label thickening agents have seen the highest growth rate (9-10%), capturing market share from traditional options

Key Companies

- Cargill, Incorporated

- Archer Daniels Midland Company (ADM)

- Tate & Lyle PLC

- Ingredion Incorporated

- CP Kelco (A Huber Company)

- DuPont Nutrition & Biosciences

- Darling Ingredients Inc.

- Ashland Global Holdings Inc.

- Kerry Group plc

- FMC Corporation

- Koninklijke DSM N.V.

- Nestlé S.A.

- BASF SE

- Naturex (A Givaudan Company)

- Jungbunzlauer Suisse AG

- Avebe U.A.

- Taiyo International

- Kemin Industries, Inc.

- Deosen Biochemical Ltd.

- TIC Gums (Ingredion Incorporated)

Segmentation-wise Analysis

By Application

The sector for food thickeners is growing in various applications through changing consumer behaviors and innovations within the industry. In the bakery and confectionary industry, food thickeners provide texture, stability, and shelf life, which are key in low-fat and gluten-free recipes.

The meat and poultry industry is increasingly using thickeners as a way to enhance moisture content and consistency in processed meat alternatives. Sauces and dressings remain a dominant use area, where thickening agents stop separation and provide a uniform, creamy texture. In the beverage industry, hydrocolloids and starches contribute to mouthfeel, stability, and suspension in plant-based, functional, and dairy beverages.

Dairy products depend on thickeners to enhance viscosity in yogurts, creams, and ice creams, making them rich and creamy. Other uses, such as soups, infant foods, and therapeutic nutrition, are experiencing constant growth owing to increased demand for functional and texture-modified foods. Fact.MR believes that the application segment in the food thickening agents industry will expand at a rate of almost 7.1% CAGR between 2025 to 2035.

By Source

The origin of food thickening agents is crucial in determining their functionality, usage, and consumer acceptance. Vegetable-derived sources, such as guar gum, gum arabic, locust bean gum, and starches, remain dominant due to their natural origin and prevalence in clean-label and vegan products.

Seaweed-derived thickeners like carrageenan, agar, and alginate are increasingly finding application in dairy and plant-based products, especially in stabilizing non-dairy equivalents. Microbial sources such as gellan gum, curdlan, and xanthan gum are gaining popularity because they are versatile and provide consistent performance in a range of food uses.

Gelatin, which is animal-derived gelatin is still the dominant thickener in confectionery and pharmaceutical uses, but its use is diminishing because more and more consumers prefer plant-based products. Artificial thickeners like carboxymethyl cellulose and methylcellulose are extensively employed in processed food and gluten-free products, with excellent stability and texture modification. Fact.MR believes that the source segment within the food thickening agents industry will expand at a rate close to 7.0% CAGR from 2025 to 2035.

Segmentation

By Application :

Bakery & Confectionery, Meat & Poultry, Sauces & Dressings, Beverages, Dairy Products, Others.

By Source :

Plant (Guar Gum, Gum Arabic, Locust Bean Gum, Pectin, Starches, Others), Seaweed (Carrageenan, Agar, Alginate), Microbial (Gellan Gum, Curdlan, Xanthan Gum), Animal (Gelatin), Synthetic (Carboxy Methyl Cellulose (CMC), Methyl Cellulose).

By Region :

North America, Latin America, Western Europe, Eastern Europe, APEJ, Japan, Middle East & Africa.

- Frequently Asked Questions -

What are food thickening agents used for?

They improve texture, consistency, and stability in bakery, dairy, sauces, and beverages.

What are common sources of food thickeners?

They come from plants (starches, guar gum), seaweed (carrageenan), microbes (xanthan gum), and animals (gelatin).

How do food thickeners enhance products?

They prevent separation, improve mouthfeel, and create a smooth, uniform texture.

Are food thickening agents regulated?

Yes, agencies like the FDA, EFSA, and FSANZ ensure safety and compliance.

What is driving the demand for food thickeners?

Clean-label trends, plant-based alternatives, and food innovation are key drivers.

Author:

S.N. Jha

Editor:

Anushree Karale