High Temperature Elastomers Market Outlook (2025 to 2035)

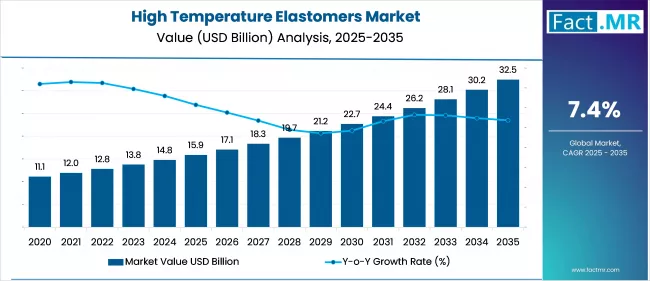

The global high temperature elastomers market is expected to reach USD 32.5 billion by 2035, up from USD 14.8 billion in 2024. During the forecast period from 2025 to 2035, the industry is projected to expand at a CAGR of 7.4%, driven by demand from the automotive, aerospace, and industrial sectors, where elastomers are required to perform under high-temperature conditions.

Elastomers, such as silicone, fluorocarbon, and perfluoroelastomers, are being used as seals, gaskets, and insulation as industries seek high-performance materials that can withstand thermal stress. Their adoption is also being supported by technological progress and increasing interest in material longevity and system reliability in high-temperature and mission-critical applications.

What are the drivers of the High Temperature Elastomers Market?

The global market for high-temperature elastomers is expected to grow due to the increasing demand for thermally stable materials in advanced automotive, aerospace, and other industries. Elastomers such as silicone, fluorocarbon, and perfluoroelastomers are being increasingly used in precision-engineered seals, hoses, and gaskets, as components are subjected to extreme heat, high pressure, and chemical resistance.

Another factor actively contributing to the shift to high-performance elastomeric materials is the increasing emphasis on fuel efficiency and emission-related regulatory requirements. Meanwhile, the functional applicability of elastomers in high-temperature electronics, oil and gas exploration, and next-generation propulsion systems is augmenting their use. The dynamic investments in R&D are improving both commercial uptake and material development for critical applications.

What are the regional trends of the High Temperature Elastomers Market?

The regional dynamics of the high-temperature elastomers market reflect varying levels of industrial maturity, regulatory setups, and the intensity of applications. North America has been at the forefront of innovation-driven adoption, with the aerospace, automotive, and oil and gas sectors representing key areas of use, particularly in the U.S., where OEMs emphasize material performance under thermal stress.

Europe focuses on regulatory conformity and CO2 neutrality, which further promotes the consumption of fluorinated elastomers in electric mobility and green aviation. Germany and France are nations that have been working on material certification and the development of specialty compounds.

Automobile manufacturing, electronics, and energy infrastructure are also experiencing increased consumption in the Asia-Pacific region through rapid industrialization in China, India, and South Korea. Latin America is experiencing growth in petrochemical and transport-related applications, while the Middle East and Africa present emerging opportunities linked to infrastructure development and investment in local manufacturing capabilities.

What are the challenges and restraining factors of the High Temperature Elastomers Market?

The high-temperature elastomers market faces challenges related to price, the complexity of processing, and the performance of the material under different conditions. High-performance elastomers, such as perfluoroelastomers and fluorosilicones, are associated with elevated production costs, which limit their use in sectors where cost sensitivity is a concern.

Moreover, their stringent processing needs necessitate an accurate fabrication space, which hinders compliance by smaller manufacturers. Performance reliability is another concern, particularly when degradation results from chemical incompatibility, repeated thermal cycling, or mechanical fatigue under extreme conditions.

Environmental compliance in synthesis also poses its challenges, especially in Europe. The absence of standardized testing procedures also complicates benchmarking across suppliers, resulting in challenges in material selection and extended timelines for validation by end-users.

Country-Wise Insights

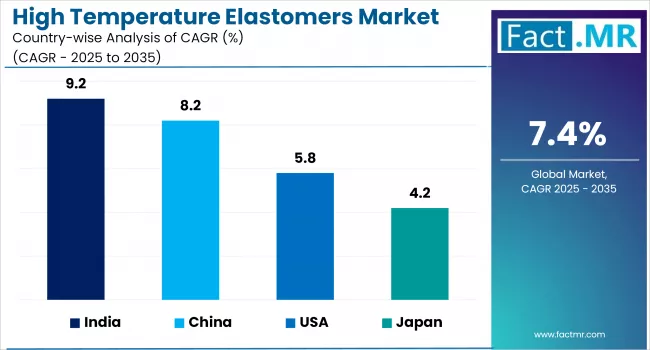

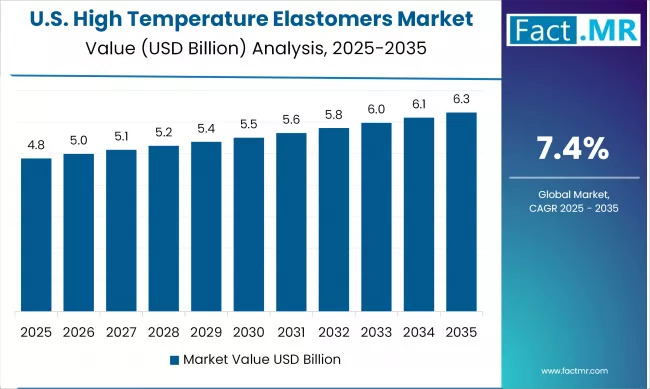

The United States drives innovation in high-temperature elastomer applications

The United States is a leading country in the high-temperature elastomers market, supported by its established aerospace, defense, automotive, and oil and gas industries. Thermal integrity and the availability of materials over long periods, as required by NASA and DoD, are driving the demand for FFKM, fluorosilicone, and silicone elastomers.

High-temperature insulating materials and thermal gaskets are experiencing increased consumption due to the rise in the manufacturing of EVs. Regulatory requirements, such as CAFE standards and EPA emission standards, are also gaining increased market traction. Key industrial regions, including Texas, Michigan, and California, are experiencing the adoption of advanced elastomers into mission-critical systems, as OEMs and tier-1 suppliers strategically partner in R&D.

Germany leads in automotive-grade high-temperature elastomer integration

The demand for high-temperature elastomers in Germany is driven by the requirements of precision engineering and advanced automotive manufacturing. OEMs such as BMW, Volkswagen, and Mercedes-Benz are utilizing fluorocarbon and silicone elastomers in engine compartment applications that are exposed to elevated temperatures and chemical exposure.

The shift towards e-mobility, turbocharged engines and light systems has further enhanced the elastomeric specification requirements. EU REACH and Blue Angel program regulatory focus is facilitating the use of durable material with low emissions. The presence of high levels of R&D cooperation between polymer suppliers, auto-component makers, and applied science institutes in areas like Bavaria and Baden-Wurttemberg is maintaining German dominance of elastomer formulation and range of application.

China’s industrial expansion fuels high-temperature elastomer consumption growth

The high-temperature elastomers market in China is expanding gradually, alongside its automotive, electronic, and petrochemical industries. The use of elastomers in the form of thermal sealing, e-mobility insulation, and refinery equipment is being driven by national policies in favor of industrial modernization and emission reduction.

Elastomer-integrated manufacturing is underway in provinces as Jiangsu, Zhejiang and Guangdong. Innovations in EV batteries, high-speed rail, and solar energy components are increasing domestic demand for fluorosilicone and FKM elastomers.

The governmental effort in import substitution in high-performance materials is helping in improving the production rate locally. Moreover, technology is advancing through strategic alliances between Chinese material producers and international chemical companies.

Category-Wise Analysis

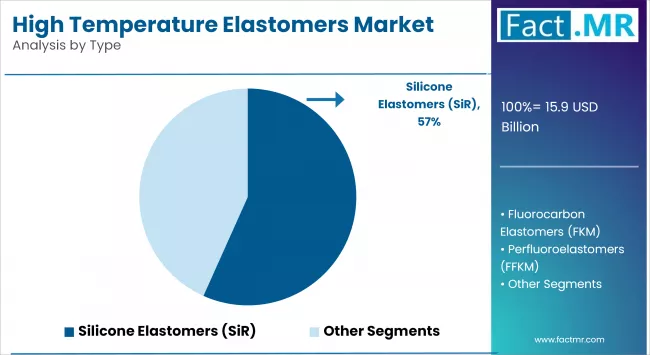

FKM elastomers deliver heat and chemical resistance for durability

Fluorocarbon elastomers (FKM) are widely used among high temperature elastomers because of their rare ability to withstand high temperatures, fuels, oils and abrasive chemicals. The materials are applied in automotive powertrain systems, aerospace propulsion, and oilfield sealing requirements since these materials are able to maintain mechanical integrity at temperatures above 250°C.

New formulations are being developed to perform in low-compression-set and chemically volatile conditions. Improved thermal cycling and fluid resistance are achieved through FKM elastomers co-formulated with nano-loaders and processable polymer blends. Their extensive integration into emission control systems and high-pressure engine zones has made them a standard solution for OEMs seeking reliable, durable, and regulation-compliant materials for thermally demanding components.

High-temp seals and gaskets ensure performance under thermal stress

High-temperature elastomers have been widely applied in seals and gaskets because they are used universally in maintaining pressure, containing fluids, and providing thermal insulation in most mission-critical systems. Automotive turbochargers, aircraft engines, and chemical reactors require elastomers that can maintain their elastic properties while providing sealing capabilities at elevated temperatures under frequent dynamic mechanical stress.

Superior reliability is now achieved through multilayer and co-extruded sealing systems composed of silicone, FKM, and FFKM. With the electrification, miniaturization, and light-weighting designs, their high-temp sealing solutions will be increasingly application-specific, with a focus on reducing the compression set, the ability to withstand thermal aging, and compatibility with bio-based fuels and lubricants.

Automotive sector drives elastomer demand for thermal reliability solutions

The automotive industry is one of the primary end-use sectors for high-temperature elastomers, driven by the evolution of drivetrain technologies, increased operating temperatures, and regulatory requirements related to emissions and durability. Gaskets, turbo hoses, air intake systems and sensor enclosures are also made of high-performance elastomers that resist thermal variation and chemical exposure.

The increasing adoption of hybrid and electric vehicles is raising the demand for elastomers in battery sealing, thermal insulation systems, and electrical protection valves. OEMs are collaborating with elastomer compounders to develop lightweight, low-VOC, and thermally resistant formulations. As internal combustion engine platforms advance and electrified vehicle architectures expand, the role of thermal elastomers becomes central to component longevity and system reliability.

Competitive Analysis

Key players in the high temperature elastomers industry include Dow, Wacker Chemie AG, Momentive, Shin-Etsu Chemical, Solvay, Daikin Industries, 3M, KCC Corporation, DuPont and China National Bluestar Group Co. Ltd.

Industries are placing increasing emphasis on heat-resistant, chemically stable elastomers that can operate in high-stress conditions across various sectors, including the automotive, aerospace, electronics, and oil and gas industries. The market is experiencing steady growth.

The performance-based formulation with the focus on high-performance demands of OEMs, i.e., to improve durability, thermal integrity, and operational reliability of mission-critical applications, is critical. The product innovation strategies are also being remodeled by the regulatory pressure to emissions and material sustainability.

To fulfill changing thermal and mechanical requirements, manufacturers are investing in advanced fluorosilicone, FFKM, and hybrid polymer technologies. Priorities include achieving low compression set, extended service life, and compatibility with a range of fuels. Strategic efforts include backward integration, expanding regional manufacturing capacity, and forming research and development partnerships. The market remains competitive due to ongoing material differentiation, varied testing protocols, and capabilities in precision molding.

Recent Development

- In April 2025, DuPont launched a new generation of Viton low-carbon fluoroelastomers with improved thermal stability and a 20 percent reduced carbon footprint, aimed at high-pressure seals in water infrastructure and automotive applications. The technology enhances durability in extreme conditions (up to 220 °C) and reduces production emissions, promoting sustainable infrastructure solutions.

- In May 2025, Solvay revealed a new high-performance, chemically resistant PEEK elastomer with better performance in the high-pressure fire suppression system and cooling pipelines. It is an innovation made with bio-based additives, which improves lifespan in challenging temperatures (up to 250 °C) and is in compliance with strict environmental regulations.

Fact.MR has provided detailed information about the price points of key manufacturers of the High Temperature Elastomers Market positioned across regions, sales growth, production capacity, and speculative technological expansion, in the recently published report.

Methodology and Industry Tracking Approach

The global high temperature elastomers market report by Fact.MR used the input of 11,800 stakeholders in 30 countries, with at least 300 legitimate actors being interviewed by regional markets. Around 65 percent of the respondents were end users and integrators (e.g., automotive OEMs, aerospace contractors, component molders, and electronics firms), and 35 percent were domain experts (e.g., polymer scientists, materials engineers, and supply chain leaders).

The data gathering period spanned from August 2025 to June 2026, capturing both current and future trends, thermal performance norms, purchase patterns, and developmental preferences related to compliance risks within the value chain of elastomeric materials. All the answers were regionally weighted to follow the dynamics of the global elastomer markets and application density.

More than 280 confirmed records were utilized in the analysis, such as technical datasheets, R&D pipelines, regulatory disclosures, material safety records, and trade reports. The conclusions in the report regarding pricing trends, demand forecasts and competitive position were confirmed with a variety of quantitative models such as multivariate regression and models of the material lifecycle.

With Fact.MR monitoring consumer behavior, product efficacy, industry trends, and market opportunities since 2018, this report is becoming an authoritative source of information that stakeholders can rely on.

Segmentation of High Temperature Elastomers Market

-

By Type :

- Silicone Elastomers (SiR)

- Fluorocarbon Elastomers (FKM)

- Perfluoroelastomers (FFKM)

- Fluorosilicone Elastomers (FVMQ)

- Polyacrylate Elastomers (ACM)

- Ethylene Acrylic Elastomers (AEM)

- Others

-

By Processing Method :

- Injection Molding

- Compression Molding

- Extrusion

- 3D Printing / Additive Manufacturing

- Others (Transfer Molding, etc.)

-

By Application :

- Seals & Gaskets

- Hoses & Tubing

- O-rings

- Wire & Cable Insulation

- Engine Components

- Heat Shields

- Valve Stems & Connectors

- Other Custom Molded Parts

-

By End-Use Industry :

- Automotive

- Aerospace & Defense

- Electronics & Semiconductors

- Oil & Gas

- Industrial Machinery

- Energy & Power (including Solar and Wind)

- Chemical Processing

- Healthcare & Medical Devices

- Others (Food Processing, Marine, etc.)

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What was the Global High Temperature Elastomers Market Size Reported by Fact.MR for 2025?

The global high temperature elastomers market was valued at USD 15.9 billion in 2025.

Who are the Major Players Operating in the High Temperature Elastomers Market?

Prominent players in the market are Dow, Wacker Chemie AG, Momentive, Shin-Etsu Chemical, Solvay, Daikin Industries, 3M, KCC Corporation, among others.

What is the Estimated Valuation of the High Temperature Elastomers Market in 2035?

The market is expected to reach a valuation of USD 32.5 billion in 2035.

What Value CAGR did the High Temperature Elastomers Market Exhibit Over the Last Five Years?

The historic growth rate of the high temperature elastomers market was 6.8% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed