High Speed Steel Market Outlook (2025-2035)

The global high-speed steel market is projected to increase from USD 2.9 billion in 2025 to USD 5.5 billion by 2035, with a CAGR of 6.6% during the forecast period. The increasing demand for strong precision cutting tools in industrial automation drives growth. Their use makes them ideal for applications requiring high wear resistance, hardness at elevated temperatures, and reliable performance in sectors like metal cutting, automotive, and heavy machinery.

-2025-to-2035.webp)

Quick Facts about High Speed Steel Market

- Industry Value (2025): USD 2.9 Billion

- Projected Value (2035): USD 5.5 Billion

- Forecast CAGR (2025 to 2035): 6.6%

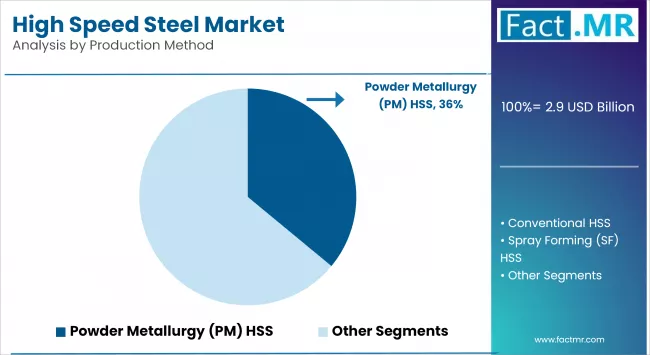

- Leading Segment (2025): Powder Metallurgy (PM) HSS (36% Market Share)

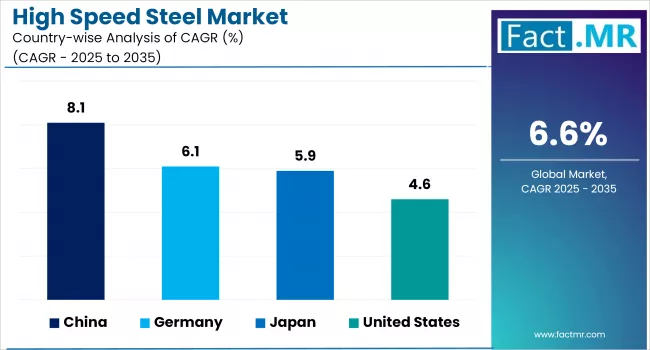

- Country Growth Rate (2025 to 2035): China (8.1% CAGR)

- Top Key Players: Graphite India Ltd., NACHI-FUJIKOSHI CORP., Tiangong International Co. Ltd., and ThyssenKrupp AG

What are the Drivers of High Speed Steel Market?

The continued growth of global automotive production primarily drives the development of the high-speed steel market. The International Organization of Motor Vehicle Manufacturers (OICA) estimates that global vehicle production will exceed 94 million units in 2023. This expansion increases demand for high-precision, long-lasting tools for machining components such as crankshafts, camshafts, and engine valves, where HSS is preferred for its thermal resistance and long service life.

The aerospace industry's emphasis on high-performance tools drives up HSS demand. Aircraft manufacturers such as Boeing and Airbus need cutting tools that can withstand high temperatures and mechanical stress when machining superalloys and composite materials.

Additionally, the demand for metal cutting tools in the general engineering, maintenance, and fabrication sectors is driving market growth. HSS tools are affordable, easy to regrind, and adaptable, making them appealing to small and medium-sized businesses. These practical benefits ensure consistent consumption across a wide range of industries worldwide.

What are the Regional Trends of High Speed Steel Market?

High-speed steels are also popular in North America and Europe due to established industrial sectors and ongoing R&D. The U.S. is a major North American market with a strong automotive and aerospace industry. Demand for high-performance cutting and drilling tools in these sectors is driving high-speed steel adoption.

High-speed steels are also popular in Europe due to their advanced manufacturing and innovation. Germany, France, and the U.K. are major contributors to the demand for automotive and industrial machinery.

Asia Pacific accounts for the largest share of global high-speed steel demand, led by China, Japan, and India, where rapid industrialization, infrastructure development, and robust manufacturing bases are driving market growth. With significant investments in production and technology, the region's automotive and aerospace industries are growing.

High-speed steel market growth in Latin America and the Middle East & Africa is slower compared to Asia Pacific and North America. In Latin America, countries like Brazil and Mexico are key markets, driven by expanding industrial and manufacturing sectors. Meanwhile, the Middle East & Africa are increasing investments in industrial infrastructure and economic diversification. As demand for high-performance tools rises across construction, mining, and energy industries, the adoption of high-speed steels is growing, supporting steady market expansion in these regions.

What are the Challenges and Restraining Factors of High Speed Steel Market?

High-speed steel (HSS) is up against stiff competition from carbide-based and ceramic cutting tools, which provide superior hardness, cutting speed, and wear resistance. While HSS is inexpensive, its performance limitations in high-speed, high-temperature environments limit its usefulness in modern, automated CNC machining.

Another challenge is the increased use of advanced manufacturing technologies such as laser cutting, waterjet cutting, and additive manufacturing. These non-traditional methods frequently eliminate the need for traditional tooling materials such as HSS, limiting demand in industries shifting toward such innovations.

Environmental regulations and sustainability concerns also present challenges. HSS production requires a lot of energy and produces a lot of emissions, particularly due to the alloys it contains. Stricter environmental compliance standards in developed countries, such as those imposed by the EU's REACH regulations, may raise manufacturing costs or necessitate facility upgrades.

High-speed steel's relatively slower innovation rate when compared to emerging superalloy-based materials has an impact on its competitiveness in high-value applications, particularly aerospace and precision electronics.

Country-Wise Outlook

United States Strong Industrial Base Driving High-Speed Steel Demand

The U.S. advanced manufacturing sector and strong demand for precision tooling. HSS is widely used in industries such as automotive, aerospace, and industrial machinery, where durability, thermal resistance, and cutting performance are essential. The U.S. also has a strong metal fabrication sector, which drives demand for dependable cutting tools.

The resurgence of domestic manufacturing, aided by policies such as the Inflation Reduction Act and reshoring trends, is a significant driver in the U.S. high-speed steel market. This has resulted in more capital investment in machine shops and tool production facilities. For instance, the cutting tools market in the United States alone will exceed $4.3 billion by 2023, with HSS tools accounting for a sizable portion due to their cost-effectiveness and versatility in high-mix, low-volume applications.

The regulatory environment in the U.S. promotes high-quality manufacturing standards. Tool steel grades and performance are governed by ANSI and ASTM specifications, ensuring consistent quality for HSS products produced domestically and imported. The U.S. government also enforces strict safety and environmental regulations through agencies such as OSHA and the EPA, urging businesses to use cleaner and safer toolmaking processes.

-2025-to-2035.webp)

China witnesses Rapid Market Growth Backed by Expansive Manufacturing and Industrial Growth

China is the world's leading producer and consumer of high-speed steel, due to its extensive manufacturing base. Because of its superior wear resistance and thermal stability, HSS is in high demand in the country's thriving automotive, toolmaking, and heavy machinery industries.

China continues to invest in R&D to improve metallurgical properties and reduce its reliance on imported high-performance steel. Institutions such as the Central Iron and Steel Research Institute (CISRI) have worked with domestic manufacturers to improve the performance of cobalt-free and environmentally friendly HSS grades, which are becoming increasingly popular due to global sustainability demands.

The "Made in China 2025" initiative has emphasized advanced manufacturing and material innovation, with a focus on upgrading domestic tooling technologies. Furthermore, environmental regulations are encouraging cleaner steel processing methods, influencing the market to adopt higher-efficiency, lower-emission HSS production methods.

With the rapid growth of the electric vehicle (EV) industry, companies such as BYD and CATL are increasingly in need of precision dies and cutting tools for battery casings and lightweight materials, applications where HSS remains critical. This demand is driving local producers to create more specialized grades of high-speed steel.

Japan's Precision Industries Fuel High-Speed Steel Demand

Japan is a key player in the global high-speed steel market, owing to its precision-oriented industrial sectors. The automotive, electronics, and metal tooling industries in the country all require high-quality cutting tools that are efficient and perform well. HSS remains a popular material due to its ability to maintain hardness at high temperatures, making it ideal for high-precision machining applications.

One of the main drivers is Japan's strong automotive manufacturing base. With brands such as Toyota, Honda, and Nissan maintaining global production standards, there is a steady demand for long-lasting cutting and drilling equipment. HSS tools are widely used in the manufacturing of engine and transmission parts, where wear resistance and dimensional accuracy are critical.

Increasing use of advanced coatings like TiAlN (Titanium Aluminium Nitride) on HSS tools to improve longevity and efficiency. Japanese manufacturers are investing in R&D to develop coated HSS variants that can compete with carbide tools, particularly in applications requiring flexibility and cost efficiency.

In terms of regulation, Japan adheres to strict industrial safety and quality standards (for example, JIS Japanese Industrial Standards), ensuring that HSS products used in the country meet high-performance and environmental compliance standards. These standards encourage domestic manufacturers to produce high-quality HSS products that compete globally.

Category-wise Analysis

Powder Metallurgy (PM) to Exhibit Leading by Production Method

Powder Metallurgy (PM) HSS dominates the high-speed steel market. High-speed steel is made by compacting and sintering metal powders. This method controls alloy composition precisely, improving uniformity and alloying component addition. Powder-produced steel formation produces a homogeneous microstructure with finer, more uniform carbide dispersion, improving dimensional stability, grindability, and toughness.

This technology can also make highly alloyed grades that standard steelmaking cannot. It is increasingly used for mechanical and CNC tooling. Except for high-temperature alloys and exotics, it can be used for grinding.

Conventional HSS is the fastest-growing segment in the high-speed steel market, due to its use of a variety of cutting tools, drills, taps, and other applications that require both high-speed machining and durability. Traditional methods of producing conventional HSS include ingot casting and forging. The alloy is melted and cast, then hot worked into the desired shapes, such as bars, sheets, or billets.

For many years, conventional HSS manufacturing processes were widely used. The resulting material, like high-speed steels, has excellent hardness, wear, and heat resistance.

T-type to Exhibit Leading by Grade

T-type high-speed steels dominate the high-speed steel market. T-type high-speed steels, which contain tungsten, are well-known for their high hardness and heat resistance. These steels are widely used in applications requiring high operating temperatures.

Their ability to maintain hardness at high temperatures makes them ideal for heavy-duty cutting tools and applications requiring significant thermal stability. The growing demand for high-performance tools in industries like automotive and aerospace is driving the use of T-type high-speed steels.

M-type high-speed steels are the fastest-growing segment in the high speed steel market, as these molybdenum-based and have excellent wear resistance and toughness. These steels are commonly used in applications requiring high durability and longevity.

M-type high-speed steels are especially popular in manufacturing environments where wear and tear resistance is critical, such as the manufacture of high-precision cutting and drilling tools. The increased emphasis on efficiency and cost-effectiveness in manufacturing processes is driving up demand for M-type high-speed steels.

Cutting Tools to Exhibit Leading by Application

Cutting tools dominate the high-speed steel market, driven by the demand for high-precision and long-lasting tools in a variety of manufacturing processes. High-speed steels are required for the production of cutting tools that can maintain their sharpness and performance even at high speeds and temperatures. High-speed steel cutting tools are particularly important in the automotive and aerospace industries for producing complex components efficiently.

Milling tools are the fastest-growing segment in the high speed steel market, due to their ability to deliver high performance and precision. High-speed steel milling tools are used in a variety of machining processes to shape and form materials precisely. High-speed steel milling tools are particularly beneficial to the industrial machinery sector because they increase productivity and reduce downtime.

Continued advancements in milling technology, as well as the growing adoption of automation in manufacturing, are expected to drive up demand for high-speed steels in this application.

Automobile to Exhibit Leading by End-Use Industry

The automobile industry dominates the high-speed steel market, driven by the need for long-lasting, high-performance tools in the production of automotive components. High-speed steels are required for making cutting and drilling tools that can withstand the high-speed and high-temperature conditions found in automotive manufacturing. The increased production of vehicles, as well as the growing trend toward electric cars, is expected to drive demand for high-speed steels in the automotive sector.

High-speed steels are the fastest-growing segment, as these are used in the aerospace industry to make a variety of components with high strength and thermal stability. High-speed steels' ability to retain hardness and performance at high temperatures makes them ideal for aerospace applications.

The continued growth of air travel and advancements in aerospace technology are driving up demand for high-speed steels in this industry. The aerospace industry's emphasis on precision and dependability highlights the significance of high-speed steels in this market.

Competitive Analysis

The global High-Speed Steel (HSS) market is becoming increasingly competitive, distinguished by technological innovation, a diverse product offering, and a strong presence of both global and regional players. Manufacturers compete based on material performance, cost-efficiency, durability, and the ability to meet end-user-specific requirements.

Major players are constantly investing in R&D to improve the toughness, heat resistance, and wear resistance of their HSS products. This innovation is especially significant in industries like automotive, aerospace, and industrial machinery, where cutting precision and thermal stability are critical.

HSS manufacturers are increasingly focusing on tailored grades to serve specific applications. Due to its superior heat tolerance, cobalt-based HSS is increasingly being used in aerospace and heavy-duty machining. Manufacturers are also developing hybrid alloys and coating technologies (such as TiN or AlTiN coatings) to increase tool life and reduce downtime, improving overall market competitiveness. As end-user industries change, particularly with the shift toward lighter-weight and more difficult-to-machine materials such as titanium and composites, HSS manufacturers must adapt to the evolving needs and performance benchmarks.

Sustainability is also emerging as a competitive factor. To meet increasing environmental regulations, companies are incorporating eco-friendly production methods and recyclable steel content. The incorporation of AI and smart manufacturing processes into HSS production improves product quality while lowering manufacturing waste.

Key players in the high-speed steel industry include Erasteel, Kennametal, Voestalpine AG, Graphite India Ltd., NACHI-FUJIKOSHI CORP., Tiangong International Co., Ltd, ThyssenKrupp AG, Sandvik AB, Hitachi Metals Ltd., DAIDO STEEL, and other players.

Recent Development

- In December 2024, Sumitomo Electric Industries introduced the SumiDrill™ GDX series, an indexable insert drill. These drills are designed to be cost-effective, reduce carbide usage, and eliminate the need for regrinding, making them particularly suitable for industries such as automotive.

- In December 2023, Dormer Pramet, a leading global manufacturer and supplier of metal cutting tools and part of the Sandvik Group, launched an expanded product line specifically tailored for the Indian market. This introduction aimed to meet the increasing demand for enhanced productivity and cost-efficiency in India's evolving engineering landscape.

Segmentation of High Speed Steel Market

-

By Production Method :

- Conventional HSS

- Powder Metallurgy (PM) HSS

- Spray Forming (SF) HSS

-

By Grade :

- M Grade

- T Grade

- Advance Grade

-

By Application :

- Cutting Tools

- Drills

- Taps

- Milling Cutters

- Tools Bits

- Hobbing Cutters

- Saw Blades

- Router Bits

- Metal Cutting

- Milling

- Others

- Cutting Tools

-

By End-Use Industry :

- Automobiles

- Manufacturing

- Aerospace

- Mechanical Engineering

- Construction

- Others

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What is the Global High Speed Steel Market size in 2025?

The high speed steel market is valued at USD 2.9 billion in 2025.

Who are the Major Players Operating in the High Speed Steel Market?

Prominent players in the market include Graphite India Ltd., NACHI-FUJIKOSHI CORP., Tiangong International Co. Ltd, and ThyssenKrupp AG, Sandvik AB.

What is the Estimated Valuation of the High Speed Steel Market by 2035?

The market is expected to reach a valuation of USD 5.5 billion by 2035.

What Value CAGR Did the High Speed Steel Market Exhibit ovee the Last Five Years?

The historic growth rate of the high speed steel market is 5.7% from 2020-2024.

Author:

S.N. Jha

Editor:

Naved Ahmed