Kidney Dialysis Equipment and Supplies Market Outlook (2025 to 2035)

The kidney dialysis equipment and supplies market is valued at USD 24.3 billion in 2025. As per Fact.MR’s analysis, the kidney dialysis equipment and supplies industry will grow at a CAGR of 5.0% and reach USD 39.6 billion by 2035.

In 2024, the kidney dialysis supplies and equipment industry sustained its trend of gradual growth, driven by continuous growth in the number of chronic kidney disease (CKD) cases and increased demand for affordable renal care options.

The most significant trend was witnessed among patient choices toward home-based dialysis treatments, further fueled by post-pandemic focus on decentralized healthcare. Technological advances, particularly in wearable and portable dialysis devices, picked up considerable momentum and found broader usage in both mature and emerging healthcare systems.

Moving forward to 2025, the industry is ready for rapid growth as health infrastructures across the globe ramp up efforts to adopt next-generation dialysis technologies. Current clinical trials and approvals will introduce a significant influx of intelligent, AI-based dialysis machines into the commercial domains, improving treatment customization and patient adherence.

Strategic investments in developing markets, primarily in Asia and Latin America, will extend further the segment footprint, catalysed by improving awareness, strengthened reimbursement patterns, and a geographical expansion of dialysis centres.

| Metric | Value |

|---|---|

| Industry Value (2025E) | USD 24.3 billion |

| Industry Value (2035F) | USD 39.6 billion |

| CAGR (2025 to 2035) | 5.0% |

Fact.MR Survey Results: Kidney Dialysis Equipment and Supplies Industry Dynamics Based on Stakeholder Perspectives

(Surveyed Q4 2024, n=450 stakeholder participants evenly distributed across manufacturers, distributors, healthcare providers, and patients in the USA, Western Europe, Japan, and South Korea)

Most Critical Stakeholder Priorities

- Enhancing Patient Outcomes: 80% of stakeholders all over the world ranked enhancing patient outcomes as a "critical" priority.

- Cost-Effectiveness: 74% viewed cost-effective dialysis solutions in order to make it more accessible, particularly for developing countries.

Regional Difference:

- USA: 69% stressed the requirements of advanced home dialysis solutions since patients increasingly demand more accessible and affordable technologies.

- Western Europe: 85% identified sustainability of dialysis solutions as key, with a focus on minimizing the carbon footprint of dialysis machines.

- Japan/South Korea: 62% mentioned the difficulty of reconciling space constraints with the necessity for advanced dialysis equipment due to urban limitations.

Adopting Advanced Technologies

High Variance

- USA: 55% of clinicians employed remote monitoring devices to monitor patient vital signs and dialysis efficiency.

- Western Europe: 48% implemented automated dialysis machines with AI for enhanced patient management, led by Germany at 59%.

- Japan: Only a 28% of dialysis centers adopted high-end technologies, with most employing older hemodialysis machines for cost reasons.

- South Korea: 40% implemented hybrid dialysis systems integrating hemodialysis and peritoneal dialysis for increased flexibility in treatment.

Convergent and Divergent Points of View Regarding ROI

- 70% of USA healthcare stakeholders saw automation and home dialysis as a long-term cost-saving investment, but 50% in Japan still depended on manual systems.

Material Preferences

Consensus:

- Steel: Chosen by 67% of the world for the durability and strength of dialysis machines.

Variance:

- Western Europe: 55% chose aluminum as it is lighter and more environmentally friendly, with most facilities choosing recyclable materials.

- Japan/South Korea: 45% preferred hybrid materials, steel-aluminum combination, to strike a balance between cost and durability, particularly in humidity and corrosion-prone areas.

- USA: 68% of stakeholders still employed conventional stainless steel parts due to their durability and simplicity of cleaning.

Price Sensitivity

Shared Challenges:

- 85% of stakeholders across the world emphasized the rising expense of dialysis equipment materials, especially those utilized in equipment production.

Regional Differences:

- USA/Western Europe: 60% indicated willingness to pay an extra 10-15% for high-tech, automated dialysis machines.

- Japan/South Korea: 72% of stakeholders preferred lower-priced models (below USD 10,000), while just 14% were interested in high-end, automated machines.

- South Korea: 50% of stakeholders asked for leasing arrangements to minimize initial expenses, versus 22% in the USA.

Pain Points in the Value Chain

Manufacturers:

- USA: 60% of manufacturers mentioned increasing costs of production, especially in materials such as titanium and specialty tubing.

- Western Europe: 52% had trouble with complicated regulatory certifications (e.g., CE marking).

- Japan: 58% referred to supply chain delays caused by semiconductor shortages impacting equipment manufacturing.

Distributors:

- USA: 65% cited long lead times from overseas suppliers as a cause of stock shortages in some areas.

- Western Europe: 50% cited aggressive competition from low-cost producers in Eastern Europe.

- Japan/South Korea: 62% cited difficulty reaching rural or small clinics due to transport problems.

Users (Healthcare Providers/Patients):

- USA: 40% of healthcare providers cited excessive maintenance expenses of sophisticated dialysis machines.

- Western Europe: 38% mentioned lack of ability to train personnel on new dialysis machines.

- Japan: 55% of the dialysis patients were worried about the costs of home dialysis kits.

Future Investment Priorities

Alignment:

- 70% of international manufacturers intend to grow investments in automated dialysis machines and remote monitoring systems to enhance patient outcomes.

Divergence:

- USA: 59% are interested in developing home dialysis options to enable easier treatments for patients.

- Western Europe: 55% intend to invest in green initiatives, targeting carbon-neutral dialysis machines by 2030.

- Japan/South Korea: 50% of the stakeholders are placing emphasis on innovations that minimize the space needed for dialysis machines in order to make them more suitable for small healthcare centers.

Impact on Regulations

- USA: 72% of the stakeholders indicated that policy adjustments in Medicare reimbursement for dialysis sessions, particularly home dialysis, have had a considerable impact on decision-making.

- Western Europe: 78% of the stakeholders opined that tighter EU health laws and the European Green Deal will lead to the increased uptake of greener dialysis solutions.

- Japan/South Korea: 35% of the stakeholders were of the view that regulatory shifts had a modest effect, given that enforcement of dialysis laws tends to be weaker than in the USA or Europe.

Conclusion: Variance vs. Consensus

High Consensus:

- Key issues such as improving patient outcomes, cost sensitivity, and the rising cost of dialysis materials are global challenges.

Key Variances:

- USA: Significant interest in home dialysis solutions and automation, compared to Japan/South Korea, where cost sensitivity and a more cautious approach prevail.

- Western Europe: Leading in sustainability efforts, while Asia favors more pragmatic, cost-efficient solutions.

Strategic Insight:

Dialysis solutions must be customized to local requirements-automation in the USA, sustainability in Europe, and space-efficient designs in Asia. Manufacturers will have to change their products accordingly to thrive in various sectors.

Government Regulations

| Country | Government Regulations |

|---|---|

| United States (USA) | Medicare and Medicaid reimbursement for dialysis therapies are of special importance as part of sector access. Home dialysis is receiving increased attention in light of governmental incentives. The FDA oversees the regulation of dialysis equipment in 21 CFR 890, Class II approval necessary for all devices. |

| India | The government is promoting additional dialysis centers under national health programs. Rural areas still lack healthcare infrastructure. The Central Drugs Standard Control Organization (CDSCO) controls medical devices, and registration and quality standards are needed for dialysis products. |

| China | The government is supporting healthcare reforms such as dialysis equipment and treatment subsidies. National Medical Products Administration (NMPA) is responsible for assuring that dialysis devices comply with safety requirements, which involves compulsory registration prior to sale. |

| United Kingdom (UK) | NHS funding covers the treatment with dialysis but increasingly there's pressure for a more sustainable alternative. The Medicines and Healthcare products Regulatory Agency (MHRA) requires that medical devices must comply with safety standards, of which CE marking is the minimum requirement for the majority of dialysis equipment. |

| Germany | The government encourages high-tech dialysis therapy with public health insurance. The German Institute for Standardization (DIN) enforces EU standards and demands CE marking of all dialysis machines distributed. |

| South Korea | Policies are aimed at expanding access to dialysis, particularly among the elderly. The Ministry of Food and Drug Safety (MFDS) demands regulatory clearance and safety certifications for dialysis machines prior to sector release. |

| Japan | Japan's government favors home dialysis, and National Health Insurance reimburses for its costs. Dialysis equipment is certified by the Pharmaceuticals and Medical Devices Agency (PMDA) in strict accordance with Japanese safety standards. |

| France | Dialysis therapy is under the coverage of the French public health system. The ANSM (National Agency for the Safety of Medicines and Health Products) verifies dialysis equipment to meet EU specifications and applies for CE marking for legal sale. |

| Italy | Italian government encourages dialysis access, particularly for older patients. The Italian Medicines Agency (AIFA) strictly regulates dialysis equipment, demanding CE marking and compliance with EU directives. [Source: WHO] |

| Australia-New Zealand | Both nations have robust healthcare policies that provide universal access to dialysis. Australia's Therapeutic Goods Administration (TGA) and New Zealand's Medsafe mandate compulsory compliance with medical device regulations, such as CE or TGA certification for dialysis equipment. |

Market Analysis

The kidney dialysis equipment and supplies industry is set on an upward growth path, led by the growing worldwide prevalence of chronic kidney disease and rising use of home dialysis solutions. Innovation in portable and AI-supported devices is transforming delivery of treatment and increasing access in the underserved regions. Companies with user-focused next-generation dialysis systems will benefit the most, while legacy device companies with little room for maneuvering will lose industry share.

Top 3 Strategic Imperatives for Stakeholders

Prioritize Home-Based Dialysis Solutions

Executives need to invest in the creation and upscaling of mobile, easy-to-use dialysis devices specifically designed for home applications to address the increasing demand for decentralized care and enhance patient compliance.

Align with AI and Smart Technology Trends

The stakeholders need to speed up the incorporation of AI-powered monitoring and personalization functionalities into dialysis machines in order to stay competitive as the industry transitions towards precision and remote-care technologies.

Strengthen Global Distribution and Strategic Partnerships

To capture emerging industry opportunities, firms need to extend their distribution networks, seek joint ventures with local healthcare providers, and undertake targeted M&A to strengthen R&D capabilities and regional presence.

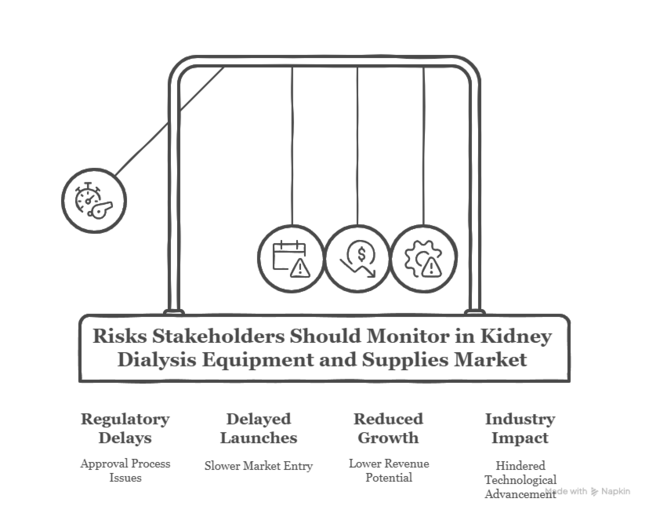

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability - Impact |

|---|---|

| Regulatory delays in approval of advanced dialysis technologies - Time-consuming and intricate approval processes can delay product launches, impacting time-to-industry and top-line growth. | Medium - High |

| Limited reimbursement policies in developing nations - Insufficient insurance coverage and weak policy environments may discourage adoption and industry penetration. | High - Medium |

| Raw material and component supply chain disruptions - Geopolitical tensions or delivery breakdowns are able to defer production and push up costs. | Medium - High |

1-Year Executive Watch-List

| Priority | Immediate Action |

|---|---|

| Accelerate Home-Based Dialysis Deployment | Perform feasibility analyses and initiate pilot programs for compact home dialysis systems in high-demand urban centers |

| Embed AI and Remote Monitoring Capabilities | Embark on strategic OEM partnerships to jointly develop next-gen intelligent dialysis platforms with real-time monitoring |

| Deepen Footprint in High-Growth Economies | Form regional partnerships and expedite regulatory clearances to scale access in underserved geographies |

For the Boardroom

To gain a competitive edge, companies must reinvent renal care delivery through innovation, personalization, and accessibility expansion. The subsequent growth phase in the kidney dialysis equipment and supplies industry is reliant on quicker innovation in portable and AI-driven solutions, facilitating a transition from clinic-focused to patient-centric models. Businesses need to shift towards intelligent, home-enabled products that complement changing healthcare infrastructure and demographic needs.

This strategy requires the redirection of R&D spend to predictive diagnostics and real-time monitoring, and at the same time, furthering supply chain resilience and regional regulatory collaboration. Boardroom agendas now need to encompass the establishment of strategic partnerships, investment in digital health integration, and aligning product pipelines to address the aging population and high-burden emerging sectors.

Segment-wise Analysis

By Type

According to the analysis, hemodialysis is anticipated to be the most profitable segment in the kidney dialysis equipment and supplies sector during the forecast period. The segment is anticipated to gain from its extensive use, especially because of its established position in the treatment of end-stage renal disease (ESRD) patients and the growing number of dialysis centers globally. In addition, innovations in home and portable hemodialysis equipment will propel expansion, so this segment will be particularly desirable within developed and developing sectors.

The CAGR for hemodialysis has been estimated to be 5.1% by 2035. The devices and technologies will witness greater investments because of the aging population and increasing incidence of chronic kidney diseases, such as diabetes and hypertension, both of which are prime causes of kidney failure.

By End User

According to the analysis, hospitals will be the most profitable segment for kidney dialysis equipment and supplies between 2025 to 2035 with a CAGR of 5.2%. This is mainly because of the huge demand for dialysis treatment in hospitals, where large numbers of critical and end-stage renal disease (ESRD) patients are being treated.

Hospitals provide sophisticated facilities for specialized treatment and are likely to embrace state-of-the-art dialysis technologies, including AI-based monitoring systems and portable dialysis units, making them a focal point for innovation and demand in this space. Hospitals will remain the largest end user segment due to their ability to accommodate complicated cases, deliver experienced medical professionals, and undertake long-term dialysis processes.

Country-wise Analysis

United States

The sector in the USA is fueled by an increasing population and a high prevalence of chronic kidney disease (CKD), most notably in patients with diabetes and hypertension. The growth in dialysis technology, including portable dialysis units and home dialysis, has improved the availability of care to patients outside of the hospital setting. End-stage renal disease (ESRD) rates continue to increase, driving the need for increased dialysis services.

The availability of sophisticated medical facilities, along with growing awareness and breakthrough technologies, renders the USA a global leader in the kidney dialysis industry. Dialysis center expansion and home care services further drive industry growth, making it one of the largest contributors to the global landscape. Fact.MR suggests that the CAGR of the industry in the United States will be 5.3% from 2025 to 2035.

India

India is confronted with an alarming increase in chronic kidney disease (CKD), fueled by rising diabetes, hypertension, and an aging population. The country is witnessing a transition towards more sophisticated renal care, and dialysis procedures are on the increase due to urbanization as well as lifestyle transitions.

Equitable access to treatment in rural areas continues to be challenged. The efforts of the Indian government toward enhancing healthcare infrastructure, such as the setting up of additional dialysis centers, will propel growth.

Enhanced affordability and availability of home dialysis solutions are likely to decrease hospital costs and enhance patients' quality of life. The growth is likely to be fueled by healthcare consciousness and advancements in medical technology. Fact.MR projects that the CAGR of the landscape in India will be 5.1% from 2025 to 2035.

China

China's kidney dialysis industry is experiencing fast growth as a result of an increasing incidence of chronic kidney disease (CKD) fueled by an aging population and high diabetes and hypertension rates. China's urban areas are experiencing high demand for dialysis, but rural areas are still behind in terms of accessibility.

The growing middle class in the country is also contributing to increased demand for sophisticated healthcare services, including home dialysis options. Advances in technology, including wearable dialysis devices and artificial intelligence-based machines, will revolutionize renal treatment in the nation. With greater emphasis on patient-centered care and enhanced affordability, the industry will witness substantial growth in the near future. Fact.MR forecasts that China’s sales will grow at a CAGR of 5.0% through the assessment period.

United Kingdom

Fact.MR suggests that the UK’s revenue for the market grow at a CAGR of 5.0% from 2025 to 2035. Even though the healthcare system in the country is well-established, the increasing demand for dialysis will strain resources, so increasing dialysis centers and home care will be a priority.

The UK kidney dialysis industry is driven by its growing population and increasing instances of chronic kidney disease (CKD), especially in older adults. The National Health Service (NHS) significantly contributes to delivering dialysis treatments, making them widely available across the nation. With a growing emphasis on home-based dialysis options, patients are increasingly turning to treatments that give them more autonomy and do not overburden hospital resources.

Germany

Germany's kidney dialysis industry is growing because of a rising population of elderly persons and high incidence of chronic kidney disease (CKD). In addition, advances in technology, such as automated dialysis systems and telemedicine for monitoring, are enhancing care quality. With ongoing technological advancements in medical technology and enhanced integration of home dialysis services, Germany’s sales will be growing with a CAGR of 5.2% from 2025 to 2035.

The nation's healthcare sector is well developed, with favorable support for superior renal care. There is growing momentum toward home dialysis options, with patients and healthcare providers seeking to limit hospital visits. The emphasis of the German government on enhancing healthcare access and providing a strong reimbursement policies for dialysis treatments fosters industry growth.

South Korea

South Korea's kidney dialysis industry is transforming rapidly due to a growing older population and rising cases of chronic kidney disease (CKD). The nation's strong healthcare infrastructure, aided by governmental programs, targets the growth of dialysis services, both hospital-based and home dialysis, in an effort to meet the growing demand. As home dialysis solutions become more sought after, companies are developing more portable and easier-to-use devices to meet the patients’ needs.

The advances in technology in renal care, including AI-based dialysis machines, are improving treatment efficiency. Increasing healthcare expenditure and increasing population awareness about CKD are fueling industry growth. Fact.MR forecasts that the CAGR of South Korea’s revenue for the industry will grow at 5.1% during the assessment period.

Japan

Japan’s sales of the industry will grow at a CAGR of 5.0% from 2025 to 2035. The country is observing a consistent rise in the need for kidney dialysis as a result of an aging society and a high incidence of chronic kidney disease (CKD), fuelled by diabetes and hypertension. The government is intent on widening access to dialysis care through policy, to enable more people to access treatment in a timely manner.

There is also an increasing trend toward home dialysis in Japan, as improved dialysis technology allows patients to better control their condition at home. Moreover, Japan's established healthcare infrastructure and increased uptake of advanced dialysis systems, including robot-assisted and portable systems, are likely to drive industry growth.

France

France's industry for kidney dialysis equipment and supplies is expected to grow with a CAGR of 5.2% during the forecast period, due to population aging and an increasing incidence of chronic kidney disease (CKD). As it has a strong healthcare system, France is addressing patient access to dialysis, especially in terms of additional funds for dialysis centers and home care. Greater demand for home dialysis is driving the industry, with patients opting for easier and more cost-effective therapies.

Advancements in dialysis technology, including more effective hemodialysis machines and wearable technology, are also propelling the industry. As the French government focuses on reforming healthcare and making it more accessible, the industry is also set to experience steady growth.

Italy

Italy's revenue for the industry is being driven by a growing population and high prevalence of chronic kidney disease (CKD). The demand for dialysis treatments is increasing, especially in areas with hypertension and diabetes prevalence. The strategy of the government to enhance the accessibility of renal care, by raising the number of centers performing dialysis and financing home dialysis procedures, is favoring industry growth.

Technological developments in dialysis equipment, such as more compact machines and computerized systems, should enhance the quality of treatment. As knowledge of CKD increases and demand for home dialysis from patients increases, Italy's sector has the potential to expand. Fact.MR projects that the CAGR of the industry in Italy will grow at a CAGR of 5.1% from 2025 to 2035.

Australia-New Zealand

The Australia and New Zealand kidney dialysis sectors are growing as a result of an older population and growing incidence of chronic kidney disease (CKD). Both nations boast established healthcare infrastructure that is further emphasizing home dialysis solutions as a means of enhancing patient ease and minimizing hospital load. Developing technology in the form of more portable dialysis machines and artificially intelligent devices is likely to feature prominently in fuelling the sector's growth.

The increasing number of dialysis centers and rising adoption of home dialysis therapies will also drive industrial growth further. The industry in these countries is expected to grow at a CAGR of 5.0% during the forecast period.

Competitive Landscape

The industry for kidney dialysis is a moderately consolidated sector with few giants like Fresenius Medical Care and DaVita dominating large shares of the sector. Major players in the dialysis industry are competing by adopting various strategies, including competitive pricing strategies designed to expand patient access, yet without compromising on profitability.

Strategic collaborations with healthcare providers and technology companies are being used to implement advanced solutions and broaden service offerings.

In March 2024, Fresenius Medical Care has announced its merger with InterWell Health and Cricket Health. The merger is directed towards delivering a comprehensive approach to kidney care from all phases of kidney disease, with an emphasis on value-based care. The merger is directed towards improving care for kidney disease patients, further positioning Fresenius as a sector leader.

In July 2024, the USA Federal Trade Commission (FTC) opened an investigation of DaVita and Fresenius Medical Care. The investigation looks into whether noncompete contracts between nephrologists working for these firms are preventing industry competition and limiting patient access to multiple dialysis suppliers. This regulatory inquiry points to existing issues over monopolistic practices within the sector.

Baxter took a major strategic step in August 2024, agreeing to sell its kidney care business unit, Vantive, to the Carlyle Group for USD 3.8 billion. This deal enables Baxter to concentrate on its core activity, while the acquisition reflects the Carlyle Group's firm belief in the growth prospect of the kidney care industry [Source: Wikipedia].

Market Share Analysis

Fresenius Medical Care- ~35-40%

Fresenius offers end-to-end renal care solution, ranging from hemodialysis machines, dialyzers, to dialysis fluids. It has the largest dialysis clinic network globally and invests considerably in home dialysis technologies.

Baxter International- ~20-25%

A leader in peritoneal dialysis (PD), Baxter is a specialist in automated PD systems such as the HomeChoice Claria, as well as hemodialysis machines and disposables. Its aggressive R&D efforts and strategic acquisitions support its leadership in developed and emerging sectors.

DaVita Inc.- ~10-15%

Fundamentally a dialysis services operator (running more than 3,000 clinics worldwide), DaVita is also aligned with equipment companies in supplying dialysis machines and disposables. Its vertically integrated platform enhances its grip in the United States and growth sectors.

B. Braun (Germany) - ~8-12%

A leading developer of hemodialysis technology, B. Braun provides high-efficiency dialysis systems (e.g., Dialog+) and biocompatible filters. It has a robust presence in Europe and Asia and emphasizes infection control and patient safety.

Nikkiso Co., Ltd. (Japan) - ~5-8%

Known for its mini, user-friendly hemodialysis equipment (e.g., Nikkiso Aqualia), Nikkiso dominates home and acute dialysis products. Its state-of-the-art blood purification technology is taking roots in North America and Japan.

Asahi Kasei Corporation (Japan) - ~4-7%

An expert in hollow-fiber dialyzers (e.g., APS series), Asahi Kasei deals in high-performance filtration solutions. It has alliances with the industry leaders and is growing in the emerging economies through cost-competitive solutions.

Other Key Players

- Nipro Corporation

- Toray Medical Co., Ltd.

- Medtronic

- Rockwell Medical

- Diaverum

- Outset Medical

- SWS Hemodialysis Care

- Weigao Group

- JMS Co., Ltd.

- Shenzhen Mindray Bio-Medical Electronics

- Becton, Dickinson and Company (BD)

- Medivators (Cantel Medical)

- Allmed Medical Care Holdings

- Infomed

- Biosun Medical Technology

Segmentation

Segmentation by Type:

- Hemodialysis

- Peritoneal Dialysis

- CRRT Systems

Segmentation by End User:

- Hospitals

- Clinics

- Others

Segmentation by Region:

- North America

- Latin America

- Europe

- East Asia

- South Asia

- Oceania

- Middle East and Africa (MEA)

- Frequently Asked Questions -

What are the most important growth drivers in the kidney dialysis industry?

The rise in chronic kidney diseases, aging populations, and technological advancements in dialysis are the most important drivers of industry growth.

How are kidney dialysis companies innovating to hold their position in the landscape?

Companies are concentrating on portable dialysis devices, home dialysis options, and the use of AI to enhance patient care and treatment outcomes.

Who are the top key players in the industry?

The top key players of the industry include Fresenius Medical Care, Baxter International, DaVita Inc, B. Braun, Nikkiso Co., Ltd., Asahi Kasei Corporation.

Which areas are experiencing the most rapid expansion in kidney dialysis services?

Asia-Pacific regions, such as India and China, are experiencing rapid growth based on increasing disease incidence and better access to healthcare services.

How are mergers and acquisitions transforming the kidney dialysis sector?

Recent acquisitions, like Fresenius Medical Care's acquisition of InterWell Health, are improving service levels and broadening the scope of dialysis providers, with a focus on value-based care.

Author:

Md Sanaullah

Editor:

Anushree Karale