Solid Electrolyte Materials Market Outlook (2025 to 2035)

The global solid electrolyte materials market is expected to reach USD 6,558 million by 2035, up from USD 983.8 million in 2024. During the forecast period from 2025 to 2035, the industry is projected to expand at a CAGR of 18.5%.

The solid electrolyte materials market is gaining momentum as a key enabler in the next generation of energy storage systems. With rising demand for safer, high-performance batteries in electric vehicles and portable electronics, these materials offer enhanced ionic conductivity and thermal stability. Their relevance is underscored by the accelerating R&D investments and commercialization efforts that are shaping the future of solid-state battery technology.

| Metric | Value |

|---|---|

| Industry Size (2025E) | USD 1,201 million |

| Industry Value (2035F) | USD 6,558 million |

| CAGR (2025 to 2035) | 18.5% |

What are the drivers of the Solid Electrolyte Materials market?

The solid electrolyte materials market is gaining traction due to transformative shifts in energy storage technologies, particularly the industry’s move toward solid-state batteries. With a global push for decarbonization, the need for efficient, high-energy-density storage has intensified, positioning solid electrolytes as a pivotal component in next-generation battery architectures. Unlike liquid counterparts, these materials enable safer operations under extreme conditions, significantly lowering the risk of thermal runaway and increasing operational reliability.

The heightened pace of electrification throughout the transportation sector is a further impelling factor. Automaker OEMs are investing in battery platforms that require solid electrolytes for improved safety profiles and smaller designs. The adoption of solid-state configurations in high-end electric vehicles is likely to drive commercial-scale demand forward.

The surge of strategic partnerships and licensing agreements among battery producers and material innovators is hastening the commercialization timeline. As manufacturers transition from laboratory-scale to pilot-scale production, solid electrolyte materials are poised to play a key role in the global battery supply chain revolution.

What are the regional trends of the Solid Electrolyte Materials market?

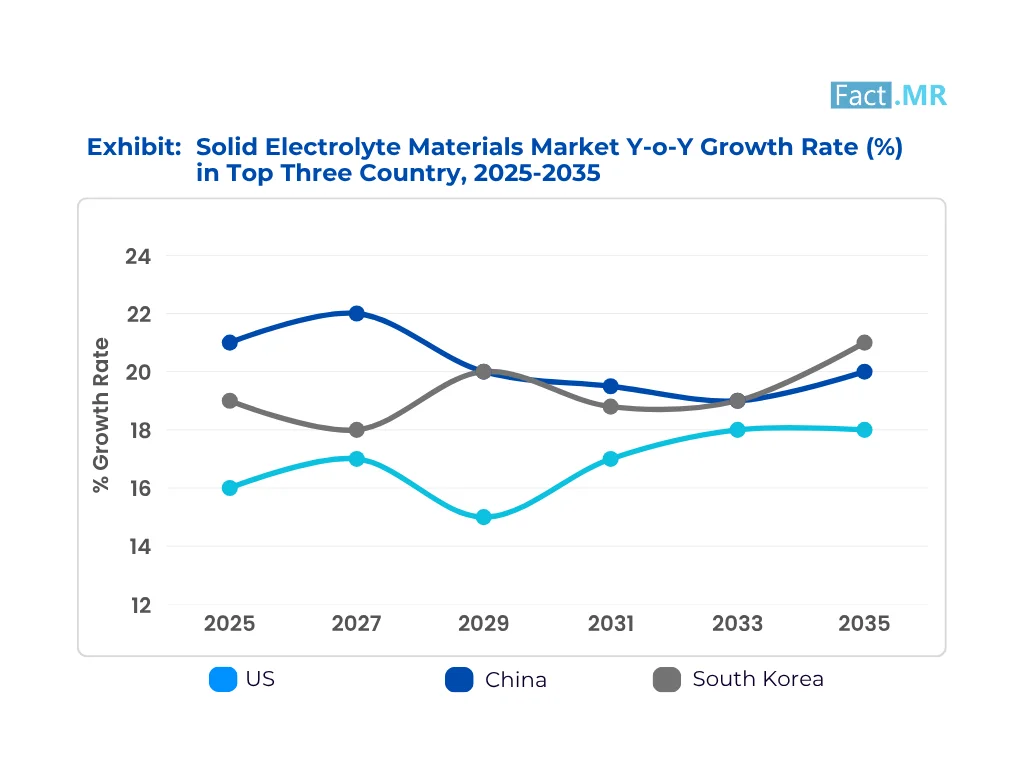

Policy support, innovation ecosystems, and industry strategy define regional dynamics for solid electrolyte materials. Automotive electrification plans and federal funding initiatives in North America, particularly in the United States, are driving significant investments in solid-state battery research and development. The presence of leading material innovators and the emergence of large-scale battery factories are strengthening domestic production capabilities, creating downstream demand for solid electrolyte components.

In Europe, regional cohesion around energy independence and sustainability is driving the development of local value chains for advanced battery materials. Incentives and public-private partnerships by governments are enhancing infrastructure development for the manufacture of solid-state batteries. The policy environment also supports the use of non-flammable and low-impact materials, enabling the swift integration of solid electrolytes in electric mobility and stationary energy storage systems.

The Asia-Pacific region remains unmatched in terms of manufacturing scale and vertical integration. Japan remains at the forefront in leading-edge material development and early commercialization, whereas South Korea focuses on value-added chemistry and strong quality control. State-supported programs and ambitious electrification goals are accelerating the industrial-scale deployment of sulfide-based materials for electrolytes in China.

Other developing countries, such as Brazil and the UAE, are pursuing strategic placements in niche markets, with an emphasis on importing technology and small-scale assembly. These regions may serve as secondary hubs as global supply chains diversify in response to geopolitical and economic pressures.

What are the challenges and restraining factors of the Solid Electrolyte Materials market?

The market faces technical and structural headwinds that complicate large-scale adoption. Chief among them is the complex synthesis of solid electrolyte compounds, which often necessitate ultra-pure precursors and controlled environments. These factors contribute to elevated capital and operational expenditures, making cost parity with conventional electrolytes a distant target in the near term.

Performance limitations, particularly at the interface between electrodes and electrolytes, continue to hinder reliability. Issues such as interfacial delamination, contact degradation, and resistance buildup compromise efficiency and restrict cycle life. Such challenges demand novel engineering approaches and material combinations, extending development timelines.

Supply chain-wise, raw material supply is still a bottleneck. Supplies of high-purity lithium, sulfides, and rare earth elements are subject to periodic shortages, resulting in volatile pricing and supply disruptions. This instability discourages long-term procurement commitments, particularly from original equipment manufacturers (OEMs) scaling up production.

Country-Wise Insights

Federal Energy Policy and Material Localization Shape the USA Trajectory

The United States is advancing solid-state battery development through targeted government programs focused on domestic materials innovation and system safety. Policy-driven R&D efforts are prioritizing solid electrolytes that meet non-flammability and long-cycle requirements, with a focus on integration into grid-scale storage and electrified transport platforms. Emphasis is placed on oxide and polymer-based materials with stable electrochemical windows and process scalability.

Institutions are working to resolve challenges at the electrode-electrolyte interface, particularly in lithium metal configurations, where interfacial resistance and dendritic growth remain key concerns. Concurrently, shifts in procurement policy are pushing for local sourcing of critical components, with solid electrolytes identified as a priority material.

Pilot demonstrations, funded through public-private programs, are being conducted across select utility-scale and defense applications. These initiatives not only support technology validation but also inform early-stage commercialization pathways that align with national resilience and sustainability goals.

Industrial Planning and Safety Standards Drive Chinese Advancements

China’s approach to solid electrolyte development is rooted in coordinated industrial planning, with emphasis on regional clustering and upstream integration. Local governments are implementing incentive structures tied to electrolyte performance metrics, including cycle stability, thermal stability, and moisture resistance. Sulfide-based electrolytes remain the focal point of R&D, with refinements underway to simplify synthesis steps and enhance structural integrity under typical cell assembly conditions.

Policy frameworks are reinforcing the shift toward solid-state configurations in public transit systems, energy storage facilities, and distributed mobility applications. Research centers are engaging in application-specific testing, aligning materials with modular cell formats used in compact vehicles and urban power backup units.

Recent updates to battery safety codes and end-of-life handling protocols are prompting recalibration of material selection criteria. This evolving regulatory and production environment is creating conditions conducive to iterative testing, certification, and pre-commercial deployment across multiple second-tier industrial zones.

Research Integration and Export Framework Guide Korean Growth

South Korea is developing its solid electrolyte capabilities through a combination of academic-industry collaboration and export-oriented manufacturing models. National efforts are focused on enabling the high-purity, low-defect production of oxide and sulfide-based electrolytes compatible with emerging solid-state battery formats. Fabrication processes, such as tape casting and pressure sintering, are being optimized for stable interfacial contact and reduced resistance under cycling conditions.

A significant portion of ongoing work is focused on ensuring cross-border certification, particularly for automotive-grade cells designed for use in cold climates and requiring high mechanical stability. Thin-film and layered structures are being tested for adaptability in high-density consumer electronics and mobility devices.

Public research programs are supporting validation runs on semi-automated lines to assess cost metrics and process repeatability. As solid-state batteries gain attention from international buyers, Korean suppliers are positioning their electrolyte technologies to meet evolving import standards and technical compliance benchmarks across multiple jurisdictions.

Category-Wise Analysis

Polymer-Based Electrolytes Enable Flexible Design in Consumer Devices

Polymer-based electrolytes are gaining renewed interest in the solid-state battery supply chain due to their inherent flexibility and ease of processing. Although they provide lower ionic conductivity than their ceramic or sulfide counterparts, their capacity to create thin, lightweight, and conformable films positions them for use in small consumer devices and new wearables. These electrolytes, typically polyethylene oxide (PEO) or PMMA-based, are being optimized with lithium salts and nanoparticle additives to enhance conductivity and thermal properties.

Original equipment manufacturers of electronics are specifically interested in developing safer battery arrangements with non-flammable, solid-state structures, particularly for portable and body-contact applications. As device miniaturization accelerates, the processability and mechanical properties of polymer-based electrolytes position them well for integration into roll-to-roll production formats. With rising demand for bendable displays and wearable health monitors, polymer electrolytes are expected to witness modest but steady growth, especially in Asia’s consumer electronics manufacturing hubs.

Medium Ion Conductivity Supports Stable and Scalable Battery Integration

Medium-ion conductive electrolytes, such as sulfide-based electrolytes, provide a balance of conductivity and interfacial flexibility that is critical for enabling the development of large-format solid-state batteries. Such electrolytes exhibit adequate mobility of ions to enable stable electrochemical performance and lower processing complexity than comparable high-conductivity ceramic equivalents. Medium-conductivity electrolytes are gaining adoption in applications that require moderate energy density and stable cycling, including grid support batteries and hybrid systems.

One of the significant benefits is that they can be operated under less extreme pressure and temperature conditions, allowing use with standard cell assembly methods. Chinese and South Korean manufacturers are investing in solid-state platforms that utilize medium-conductivity materials to meet the demand for longer-lived, safer storage solutions for both mobile and stationary applications.

Recent developments in sulfur-based and argyrodite-type materials are improving stability in ambient environments, addressing previous concerns around moisture sensitivity. This segment is expected to scale as commercialization of mid-tier solid-state cells accelerates globally.

Medical Devices Drive Demand for Solid-State Microbattery Innovation

Medical devices are becoming a high-priority end-use application for solid electrolyte materials, driven by the need for compact, biocompatible, and reliable power sources in life-sustaining technologies. Pacemakers and neurostimulators, for instance, need batteries that will provide steady output over many years with zero tolerance for failure. Solid-state batteries incorporating solid electrolytes offer greater safety by eliminating leakage hazards, as well as higher energy density in a limited space.

Solid electrolytes made from polymers and thin films have particular applicability in implantable and wearable devices, where biostability and form factor are paramount. Pressure to promote patient safety through regulation is driving the implementation of these chemistries, led by North America and Europe, where approvals for devices increasingly favor non-flammable materials. With healthcare markets expanding and digital therapeutics on the rise, the medical device sector presents a promising growth frontier for solid electrolyte adoption, particularly as microbattery production processes become standardized and scalable.

Competitive Analysis

Key players in the solid electrolyte materials industry include LG Chem Ltd., Samsung SDI Co., Ltd., NEI Corporation, Ohara Inc., Empower Materials, Ampcera Corp., Ionic Materials Inc., Toshima Manufacturing Co. Ltd., Solid Power Inc., QuantumScape Corporation, Toyota Motor Corporation, ProLogium Technology, BYD Company Ltd., CATL (Contemporary Amperex Technology Co. Ltd.), and Ensurge Micropower ASA.

The market is expanding due to the growth in demand for safer battery solutions in electric vehicles, consumer electronics, and energy storage applications. Concerns over liquid electrolyte constraints and the desire for higher energy densities are fueling the transition.

Developments in sulfide, oxide, and polymer-based electrolytes are shaping product innovation. Companies are focusing on lithium-metal compatibility, improved ion conductivity, and processing stability. Efforts are also directed toward environmentally conscious production methods, scalable manufacturing, and integration with existing battery supply chains to support broader application and adoption.

Recent Development

- In January 2025, SK On announced major R&D milestones in all-solid-state battery (ASSB) technology, showcasing innovations like sulfide-based electrolyte and lithium metal anode solutions. These breakthroughs aim to enhance battery safety, lifespan, and energy density, accelerating the commercial viability of ASSBs and reinforcing SK On’s position in next-generation EV battery development.

- In June 2024, TDK unveiled a micro solid-state battery with a record energy density of 1,000 Wh/L, using proprietary oxide-based solid electrolyte and lithium alloy anodes. This breakthrough, enabled by advanced material technology, paves the way for safer, longer-lasting, miniaturized batteries in medical, wearable, and IoT applications.

Fact.MR has provided detailed information about the price points of key manufacturers of the solid electrolyte materials market positioned across regions, sales growth, production capacity, and speculative technological expansion, in the recently published report.

Methodology and Industry Tracking Approach

The 2025 Global solid electrolyte materials market report by Fact.MR surveyed 12,500 stakeholders across 35 countries, with a minimum of 350 respondents per market. Two-thirds were end users or producers (e.g., battery manufacturers, electric vehicle OEMs, solid-state battery developers), and one-third were industry professionals (e.g., supply chain managers, materials scientists, energy storage consultants).

Data collected from May 2024 to April 2025 captured market trends, demand, opportunities, investments, unmet needs, and risks across the value chain. Responses were weighted to reflect regional market shares and demographics.

The report examined more than 300 materials, including academic journals, patents, regulatory and financial filings, to provide accurate information with the help of advanced statistical analysis, such as regression analysis.

With Fact.MR monitoring consumer behavior, product efficacy, industry trends, and market opportunities since 2018, this report is becoming an authoritative source of information that stakeholders can rely on.

Segmentation of Solid Electrolyte Materials Market

-

By Product Type :

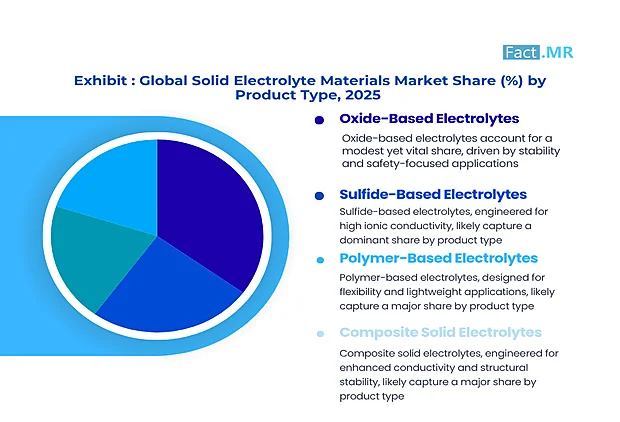

- Oxide-Based Electrolytes

- Sulfide-Based Electrolytes

- Polymer-Based Electrolytes

- Composite Solid Electrolytes

-

By Ion Conductivity :

- High

- Medium

- Low

-

By End Use Application :

- Automotive

- Renewable Energy Storage

- Consumer Electronics

- Smartphones

- Laptops

- Smartwatches

- Others

- Aerospace and Defense

- Satellites

- Military communications

- Missiles

- Medical Devices

- Pacemakers

- Neurostimulators

- Industrial Equipment & Sensors

- Smart sensors

- IoT devices

- Robotics

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What was the Global Solid Electrolyte Materials Market Size Reported by Fact.MR for 2025?

The Global Solid Electrolyte Materials Market was valued at USD 1,201 million in 2025.

Who are the Major Players Operating in the Solid Electrolyte Materials Market?

Prominent players in the market are include LG Chem Ltd., Samsung SDI Co., Ltd., NEI Corporation, Ohara Inc., Empower Materials, Ampcera Corp., Ionic Materials Inc., among others.

What is the Estimated Valuation of the Solid Electrolyte Materials Market in 2035?

The market is expected to reach a valuation of USD 6,558 million in 2035.

What Value CAGR did the Solid Electrolyte Materials Market Exhibit Over the Last Five Years?

The historic growth rate of the Solid Electrolyte Materials Market was 18.1% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed