Medical Flexible Packaging Market Outlook (2025 to 2035)

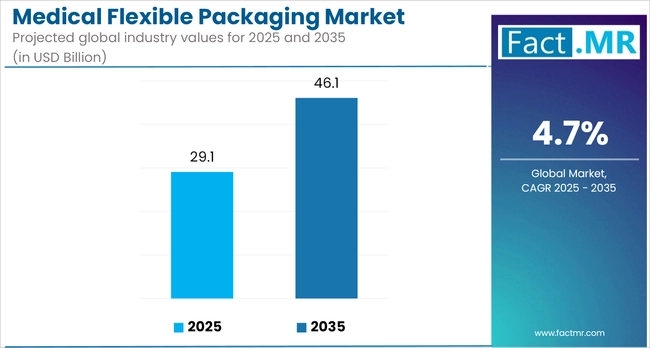

The global medical flexible packaging market is projected to increase from USD 29.1 billion in 2025 to USD 46.1 billion by 2035, with an annual growth rate of 4.7%, driven by the rising demand for sterile, lightweight, and cost-efficient packaging across the pharmaceutical and medical device sectors. Increased use of injectable drugs, diagnostic kits, and home-based care products is boosting adoption.

Innovations in recyclable and high-barrier materials, along with strict regulatory standards, are further shaping the market. The Asia-Pacific region is expected to experience the fastest growth, driven by the expansion of healthcare infrastructure and local manufacturing.

What are the Drivers of the Medical Flexible Packaging Market?

The medical flexible packaging market is gaining momentum due to intersecting trends reshaping the healthcare landscape. The rising incidence of chronic conditions globally is fueling demand for pharmaceuticals and medical devices, which in turn is driving the need for packaging that ensures product sterility, safety, and integrity.

A growing emphasis on home healthcare and the self-administration of drugs, injectables, and diagnostic kits has pushed manufacturers to adopt lightweight, user-friendly packaging formats. Regulatory agencies, such as the FDA and EMA, continue to raise the bar on sterility, traceability, and barrier performance, areas where flexible packaging is proving highly effective.

At the same time, manufacturers are facing growing pressure to reduce their environmental impact. This has led to an industry-wide shift toward recyclable, mono-material films and other sustainable alternatives. The increased use of biologics and temperature-sensitive therapies, including vaccines, is also elevating the importance of advanced flexible packaging that can maintain product stability throughout increasingly complex cold chain logistics.

Cost-efficiency and shorter production cycles are further reinforcing the appeal of flexible packaging, especially for small-batch manufacturing. Markets in India, Brazil, and Southeast Asia are opening up new growth avenues as pharmaceutical production expands and healthcare access improves.

Additionally, the adoption of smart packaging features such as tamper-evident seals, QR codes, and digital tracking is enhancing supply chain transparency and product security. These factors collectively underscore the strategic role of flexible packaging in meeting the evolving needs of global healthcare delivery.

What are the Regional Trends of the Medical Flexible Packaging Market?

The medical flexible packaging market is shaped by a variety of regional dynamics, influenced by differences in healthcare systems, regulatory frameworks, manufacturing capabilities, and demographic trends.

North America continues to lead, largely due to the United States’ well-established healthcare infrastructure, high pharmaceutical expenditures, and stringent regulatory oversight. The presence of major pharmaceutical and medical technology companies, along with the FDA’s strict requirements for sterility, traceability, and packaging validation, has fostered innovation in high-performance flexible packaging. Additionally, growing demand for biologics and home-based treatments has accelerated the adoption of barrier-protective and user-friendly formats.

Europe maintains steady momentum, supported by cohesive regulatory structures, such as the EU’s Medical Device Regulation (MDR), and robust sustainability policies. Countries such as Germany, France, and the UK play significant roles, leveraging advanced pharma manufacturing and government-backed initiatives that encourage recyclable and low-emission packaging. The region is also at the forefront of smart packaging innovation, with increasing interest in tamper-evident and serialized formats.

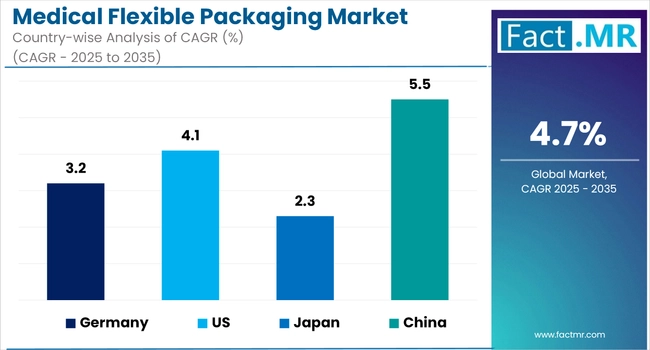

The Asia-Pacific region stands out as the fastest-growing, driven by expanding healthcare access, population growth, and increasing domestic pharmaceutical production. China and India are key players, offering cost-effective manufacturing, a strong generics market, and improving alignment with global packaging standards. Export growth from both countries is also fueling demand for internationally compliant packaging. Meanwhile, Southeast Asian nations are becoming new investment hubs as their healthcare infrastructure and private sector involvement continue to improve.

Latin America is seeing increased traction, especially in Brazil and Mexico. Growing pharmaceutical production, expanding public and private healthcare services, and gradual regulatory upgrades are driving a shift toward flexible packaging solutions that strike a balance between compliance, performance, and affordability.

The Middle East and Africa, though still emerging, show long-term potential. Countries like the UAE and South Africa are benefiting from improved healthcare logistics, increased imports of medical products, and greater involvement from multinational pharmaceutical companies. As these regions modernize their healthcare systems, demand for durable and efficient packaging is expected to grow.

What are the Challenges and Restraining Factors of the Medical Flexible Packaging Market?

While the medical flexible packaging market is on a growth trajectory, challenges continue to limit its broader potential, including regulatory hurdles, economic pressures, and supply chain vulnerabilities.

A significant challenge is navigating the intricate regulatory landscape. Packaging for medical and pharmaceutical use must comply with stringent global standards regarding sterility, barrier integrity, labeling, and material safety. Regulations such as the U.S. FDA requirements, the EU’s Medical Device Regulation (MDR), and various ISO certifications necessitate extensive testing, validation, and documentation. For smaller companies or those operating in emerging markets, achieving full compliance can delay product launches and raise operational costs.

Material-related challenges also pose risks. The industry relies heavily on polymers like polyethylene, polypropylene, and multilayer high-barrier films, all of which are subject to price fluctuations tied to petrochemical markets. Disruptions caused by geopolitical tensions, natural disasters, or supply chain bottlenecks can lead to unstable input costs and complicate production planning.

Efforts to improve sustainability, though gaining traction, also face limitations. While the shift toward recyclable and biodegradable packaging is necessary, these alternative materials still fall short of meeting medical-grade requirements, especially in terms of barrier protection and compatibility with sterilization processes. As a result, progress toward greener solutions in healthcare remains slower than in other packaging sectors.

Logistics adds another layer of complexity. The increasing use of biologics and other temperature-sensitive drugs has heightened reliance on cold chain distribution, necessitating packaging solutions that perform reliably under variable conditions. Any disruption, be it a pandemic, trade restriction, or raw material shortage, can cause delays and impact product availability.

Lastly, pricing pressures are a constant concern in public healthcare systems and markets with tight pharmaceutical pricing controls. In these settings, manufacturers must deliver compliant, high-performance packaging while keeping costs low, which often limits their ability to invest in innovation or adopt newer, more sustainable materials.

Together, these operational, regulatory, and economic pressures highlight the need for balanced strategies that support both compliance and innovation in an increasingly cost-sensitive and quality-driven market.

Country-Wise Outlook

Evolving Dynamics in the USA Medical Flexible Packaging Market: Innovation, Regulation, and Sustainability Driving Growth

The USA medical flexible packaging market continues to experience steady growth, supported by a combination of regulatory rigor, evolving healthcare models, and advances in packaging technology. With the FDA maintaining high standards for sterility, safety, and traceability, manufacturers are increasingly turning to multi-layer barrier films and tamper-evident solutions to meet compliance demands.

The growing emphasis on outpatient and home-based care is also reshaping packaging needs, driving demand for lighter, easy-to-use formats suitable for injectables, diagnostics, and wearable medical devices. At the same time, sustainability is gaining ground.

Companies are expanding their use of recyclable and compostable mono-materials, aligning with both ESG commitments and shifting regulatory expectations. Materials like bioplastics and engineered polymers are becoming common, offering environmental benefits without sacrificing product performance.

Smart packaging technologies, such as RFID tags, QR codes, and serialized tracking, are also on the rise, helping to improve supply chain visibility and enhance product security. With a mature R&D infrastructure and strong manufacturing capabilities, the USA is well-positioned to remain at the forefront of innovation in medical flexible packaging.

China’s Medical Flexible Packaging Market: Advancing Through Innovation, Regulation, and Global Integration

China is emerging as a major force in the medical flexible packaging market, driven by large-scale healthcare investments, a growing elderly population, and strong manufacturing capabilities. With an integrated supply chain and access to key polymers like polyethylene and PET, the country benefits from cost-efficient, high-volume production.

Rising chronic disease rates and broader healthcare access, supported by initiatives such as "Healthy China 2030," are driving domestic demand for sterile, high-barrier packaging in pharmaceuticals and diagnostics. The growth of biologics, injectables, and self-administered treatments further boosts demand for compliant and reliable packaging solutions.

China is also a key exporter, supplying flexible medical packaging across Asia, Europe, and Africa. In response to international standards, manufacturers are upgrading their processes and materials, while also advancing sustainability efforts through the use of recyclable films and reduced PVC usage.

Innovation is playing a larger role, with smart packaging features, such as anti-counterfeit measures and serialized tracking, gaining momentum. Combined with its expanding healthcare sector and global reach, China remains a central player in shaping the future of medical flexible packaging.

Japan’s Medical Flexible Packaging Market: Innovation and Precision in a Rapidly Aging Healthcare Landscape

Japan’s medical flexible packaging market is growing steadily, driven by its aging population, strict regulatory standards, and a well-established pharmaceutical sector. With over 28% of citizens aged 65 and above, demand for secure, sterile, and user-friendly packaging, particularly for chronic care and home-based treatments, is increasing.

The country’s regulatory body, PMDA, enforces high safety and quality standards, prompting manufacturers to adopt multilayer and high-barrier films that ensure drug stability and protection. Innovation in materials science is also a priority, with companies developing lighter, recyclable, and bio-based packaging that aligns with Japan’s Green Growth Strategy.

As a major exporter of pharmaceutical products, Japan continues to invest in packaging solutions that meet international standards, featuring serialized labels, anti-counterfeit elements, and temperature resistance. This focus on precision, sustainability, and global compliance positions Japan as a key player in the evolution of medical flexible packaging.

Category-wise Analysis

Pouches & Bags to Hold Dominant Share Among Product Types in Medical Flexible Packaging Market

Pouches and bags are expected to maintain a leading position among product types in the medical flexible packaging market, driven by their versatility, cost efficiency, and compatibility with a wide range of medical and pharmaceutical applications. These formats offer a practical solution for packaging sterile products such as surgical instruments, diagnostic kits, wound care items, and IV fluids. Their lightweight structure reduces transportation costs, while advanced sealing technologies ensure product integrity and contamination prevention.

The healthcare industry’s increasing focus on single-use and unit-dose packaging in hospital and home-care settings has further elevated demand for flexible pouches. Resealable, tamper-evident, and peelable pouch formats are gaining traction due to their ease of use and compliance with regulatory standards. Additionally, the growing adoption of high-barrier films in pouch manufacturing enhances protection against moisture, oxygen, and UV exposure, which is important for biologics, prefilled syringes, and temperature-sensitive products.

Innovation in material composition, including the integration of recyclable mono-materials and medical-grade laminates, is also contributing to the segment’s momentum. With manufacturers increasingly investing in eco-friendly alternatives that meet sterilization and performance requirements, pouches and bags remain well-positioned to support both sustainability goals and functional demands.

Moreover, the ability to customize sizes, shapes, and closure systems makes these packaging formats adaptable across various therapeutic areas and distribution channels. As healthcare systems expand outpatient care and direct-to-patient delivery models, demand for reliable, compact, and compliant packaging continues to grow, reinforcing the leadership of pouches and bags in the medical flexible packaging landscape.

Polyethylene to Hold Dominant Share Among Material Types in Medical Flexible Packaging Market

Pouches and bags continue to lead the medical flexible packaging market due to their versatility, cost-effectiveness, and suitability for a wide range of healthcare applications. They are widely used for sterile packaging of surgical tools, diagnostics, wound care, and IV fluids, offering lightweight and secure solutions that reduce shipping costs and ensure contamination prevention.

The growing focus on single-use and unit-dose formats, particularly in hospitals and home care settings, is driving demand for resealable, tamper-evident, and peelable pouch designs. High-barrier films are increasingly being integrated to protect sensitive products, such as biologics and prefilled syringes, from moisture, oxygen, and UV exposure.

As sustainability gains importance, recyclable and bio-based polyethylene variants are being adopted, with mono-material innovations aligning with regulatory and environmental goals. Its proven reliability and adaptability ensure polyethylene’s continued dominance in the medical flexible packaging market.

The pharmaceuticals manufacturing category is expected to hold the Leading Share in the Medical Flexible Packaging Market by End User

Pharmaceutical manufacturing is expected to lead the medical flexible packaging market, driven by the expansion of drug production, rising prevalence of chronic diseases, and the growing need for safe and compliant packaging. As companies scale up the production of generics, biologics, and specialty drugs, demand for high-barrier pouches, sachets, strip packs, and blister laminates continues to rise due to their ability to preserve drug stability and support unit-dose formats.

Cold chain requirements for temperature-sensitive products, such as vaccines, have accelerated the adoption of multilayer films and thermoformable laminates. Regulatory bodies such as the FDA and EMA are also enforcing stricter packaging standards, prompting greater investment in tamper-evident, sterile, and traceable materials.

As global pharmaceutical supply chains become complex, packaging must ensure product integrity during long-distance transit. Features like serialization, anti-counterfeiting, and smart labeling are increasingly embedded in flexible formats to enhance compliance and security.

East Asia holds the Leading Share in the Medical Flexible Packaging Market

East Asia remains a key leader in the medical flexible packaging market, backed by advanced manufacturing capabilities, growing healthcare demand, and strong pharmaceutical export activity. China drives regional momentum with its large-scale production capacity and integrated supply chain, supported by policy initiatives such as "Healthy China 2030," which prioritizes pharmaceutical and medtech growth.

Japan contributes through its stringent regulatory standards, aging population, and consistent demand for high-value, home-care-compatible packaging. The country’s leadership in precision engineering and sustainable material innovation further strengthens the region’s position.

South Korea is gaining traction with its expanding biotech sector and adoption of smart packaging technologies, aided by strong government support for pharma infrastructure and innovation.

The region’s focus on recyclable, mono-material, and biodegradable solutions reflects global sustainability trends and reinforces its role as a hub for both volume and innovation. East Asia’s strategic mix of scale, quality, and regulatory alignment ensures its continued dominance in the global medical flexible packaging landscape.

Competitive Analysis

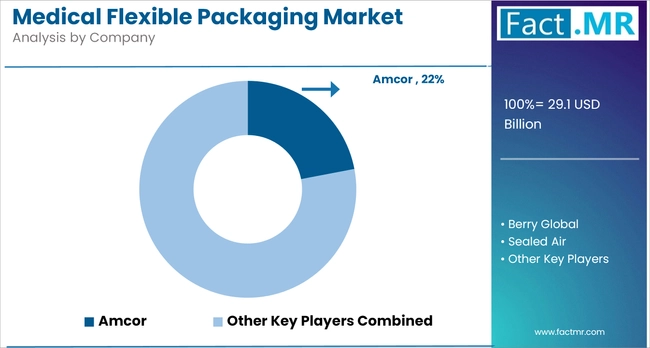

The medical flexible packaging market is highly competitive, led by global players such as Amcor, Sealed Air, Huhtamaki, Mondi, and Constantia Flexibles, who drive growth through material innovation, regulatory compliance, and sustainability initiatives.

Companies like BD and Catalent leverage pharmaceutical expertise to deliver specialized packaging for biologics and injectables, while Berry Global, AptarGroup, and Sonoco focus on recyclable formats and smart packaging solutions.

Datwyler Holding adds value through advanced sealing systems, and regional players continue to emerge with niche offerings in biocompatible and high-performance materials. As regulatory demands tighten and sustainability goals advance, market leadership increasingly depends on innovation, scale, and supply chain agility.

Recent Development

- In 2024, Amcor opened an advanced coating facility in Selangor, Malaysia, the first in Asia capable of producing both top and bottom substrates for sterile medical packaging. The facility enhances regional supply chain resilience.

- In 2024, Coveris acquired HADEPOL FLEXO in Poland to strengthen flexible packaging capabilities across Europe.

Segmentation of the Medical Flexible Packaging Market

-

By Product Type :

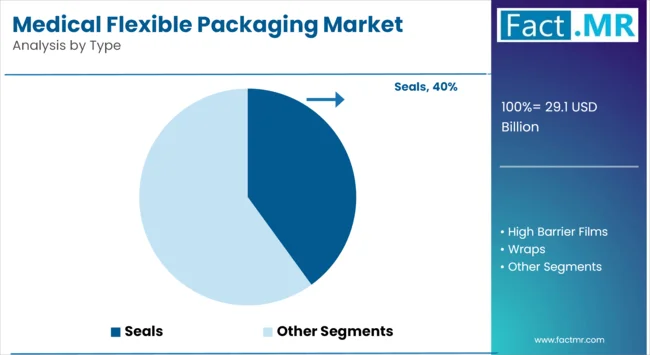

- Seals

- High Barrier Films

- Wraps

- Pouches & Bags

- Lids & Labels

- Others

-

By Material Type :

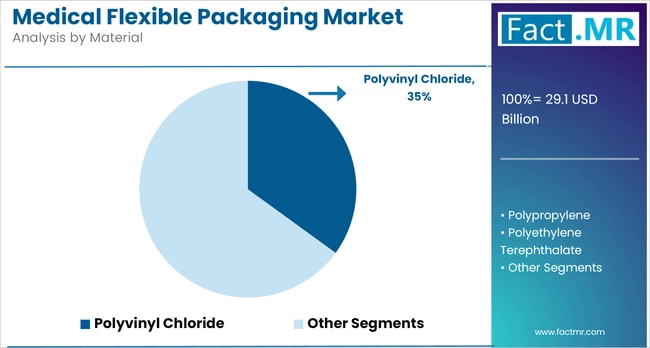

- Polyvinyl Chloride

- Polypropylene

- Polyethylene Terephthalate

- Polyethylene

- Paper

- Aluminium

- Others

-

By End User :

- Pharmaceutical Manufacturing

- Medical Device Manufacturing

- Implant Manufacturing

- Contract Packaging

- Others

-

By Region :

- North America

- Latin America

- Europe

- East Asia

- South Asia

- Oceania

- MEA

- Frequently Asked Questions -

What is the Global Medical Flexible Packaging Market Size in 2025?

The medical flexible packaging market is valued at USD 29.1 billion in 2025.

Who are the Major Players Operating in the Medical Flexible Packaging Market?

Prominent players in the medical flexible packaging market include Amcor Limited, Bemis Company Inc., Sealed Air Corporation, Huhtamaki Oyj, Mondi Group Plc, Constantia Flexibles Group GmbH, and others.

What is the Estimated Valuation of the Medical Flexible Packaging Market by 2035?

The medical flexible packaging market is expected to reach a valuation of USD 46.1 billion by 2035.

What Value CAGR Did the Medical Flexible Packaging Market Exhibit over the Last Five Years?

The historic growth rate of the medical flexible packaging market was 3.10% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed