Delayed Coker Unit Process Technology Market (2025 to 2035)

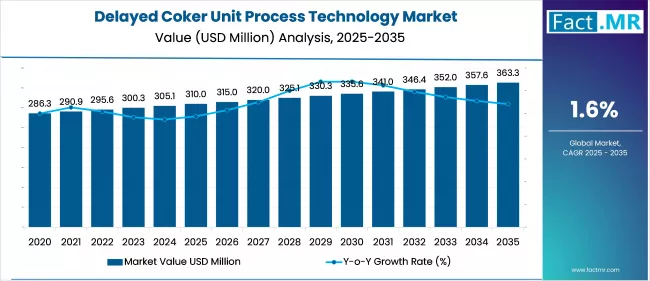

The global delayed coker unit process technology market is expected to reach USD 363.3 million by 2035, up from USD 306.9 million in 2024. During the forecast period 2025 to 2035, the industry is projected to expand at a CAGR of 1.6%.

The market for delayed coker unit (DCU) process technology is driven by the increasing demand for upgrading heavy oil and converting residues, as well as the decreasing supply of light crude. DCUs are being increasingly utilized by refineries to maximize distillate product yields, minimize coke formation, and enhance economic margins.

Integration with downstream petrochemical routes and environmental compliance requirements also support the growing role of DCU adoption in contemporary refinery optimization and residue valorization solution.

What are the drivers of the Delayed Coker Unit Process Technology Market?

The delayed coker unit (DCU) process technology market is currently undergoing progressive development, as growth in demand for heavy residue regeneration and optimized distillate recovery has been observed across refineries. With light crude supplies declining and international fuel quality regulations becoming more stringent, DCU installations are expected to take priority in upgrading low-value feedstocks into lighter and compliant fuels.

The pressure of regulatory initiatives, including IMO 2020 and desulfurization requirements, is directing refiners towards deeper conversion technologies that are compatible with the green fuel standards. There is also the benefit of increased crude-to-chemicals integration, where DCUs enhance the yield of naphtha and aromatics in the market.

The growing demand for needle coke and anode-grade coke is creating additional revenue opportunities. Strategic expansions of refineries in the Asia-Pacific and the Middle East are strengthening the demand for DCU process technologies in the long term.

What are the regional trends of the Delayed Coker Unit Process Technology Market?

Varying levels of refinery modernization characterize the technology market for the delayed coker unit (DCU) process, the introduction of residue upgrade requirements, and evolving regional regulatory frameworks. North America is in a developed phase, with capacity additions primarily focused on increasing liquid yield flexibility and petrochemical integration, particularly on the Gulf Coast of the U.S.

The RepowerEU initiative is encouraging Europe to pursue selected DCU upgrades to support decarbonization efforts and reduce dependency on fuel oil sources. Significant development is taking place in the Asian-Pacific region as China, India, and Southeast Asian countries develop refineries to process heavier crudes and reduce the quantity of imported products.

Latin America is also expanding the use of DCU to improve conversion economics and diversify its downstream operations. Integrated refining-petrochemical hubs are enhancing delayed coking deployment in the Middle East through investments considered part of broader strategic development plans.

What are the challenges and restraining factors of the Delayed Coker Unit Process Technology Market?

The global process technology market for the delayed coker unit (DCU) faces several key issues, including process complexity, environmental compliance, and operational risk. A hindering factor is the high capital requirements and long commissioning schedules associated with DCU installation, which restrict its use in cost-sensitive refineries or facilities with limited space.

Operationally, the coke drum cycle is a bottleneck and it can often cause equipment stress, thermal fatigue and unplanned shutdowns. The disposal of waste petroleum coke, including high-sulfur varieties, is also a potentially landfill-filling byproduct of their management, which further introduces even stringent standards at the carbon and particulate levels.

In emerging regions, the lack of qualified technical specialists and sophisticated control systems limits the optimization of processes. Downstream value chain fragmentation, weak and uneven policy incentives differentiated across markets that benefit specific bases, also complicates investment decisions and the dissemination of DCU technologies.

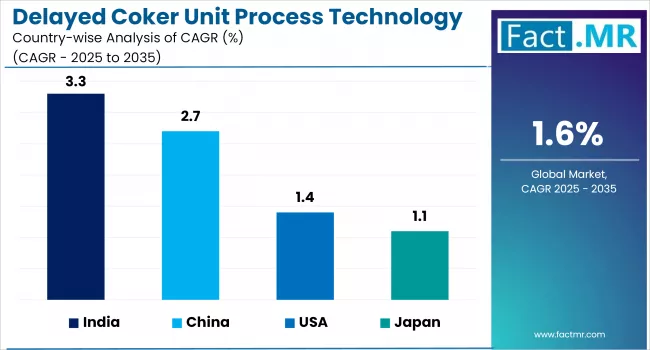

Country-Wise Insights

U.S. boosts DCU adoption to process heavy crudes profitably

The purchase of the delayed coker unit market in the U.S. has been driven by the actions required to upgrade heavy, sour crude blends in different complex refinery structures, particularly in the Gulf Coast. DCUs are purchased by the refinery for their ability to increase yields in light products and high-grade petroleum coke, which is used in the aluminum and steel sectors.

To meet emission requirements, refiners are upgrading their coke drum technology to low-emission systems and automating quenching processes. There is integrated downstream infrastructure for handling and valorizing coker products.

Such upgrades and retrofits are aided by the presence of licensors and experienced EPC companies. Cokers play a special role in enabling refinery profitability under changing fuel mix conditions and sulfur limits.

China expands DCUs for refining efficiency and petrochemical integration

The development of the DCU market in China is expanding due to state-organized refinery modernization. The upgrading of refineries aims to improve the efficiency of heavy crude processing and minimize dependence on imported refined products. Large DCUs are being commissioned by national oil companies, such as Sinopec and CNPC, to supply petroleum companies with light fuels and naphtha to petrochemical complexes.

The focus is also on digital automation, the heat recovery system, and environmental control, aligning with carbon neutrality targets. Regions with industrial clusters, such as Shandong and Guangdong, are key locations for coking investments. China continues to record capacity additions in DCUs globally, supported by government policy and increased demand for petcoke in the industrial sector.

India leverages DCUs for residue upgrading and fuel maximization

The DCU market in India is based on the presence of high-complexity refineries in the country, which are increasingly utilizing delayed coking to convert bottom-of-the-barrel residues into value-added transport fuels. The prominent refiners in India, Indian Oil and Reliance Industries, operate DCUs to manage feedstocks that are dependent on imports and to optimize liquid fuel output.

The growing domestic demand for petcoke as a fuel in the cement and power industries enhances downstream integration. The CPCB's environmental policies are encouraging refiners to implement cleaner quenching and vapor recovery systems. The investments in new grassroots plants and brownfield expansions, particularly in Gujarat and Maharashtra, position India as a regional leader in high-efficiency residue upgrading technologies, such as delayed coking.

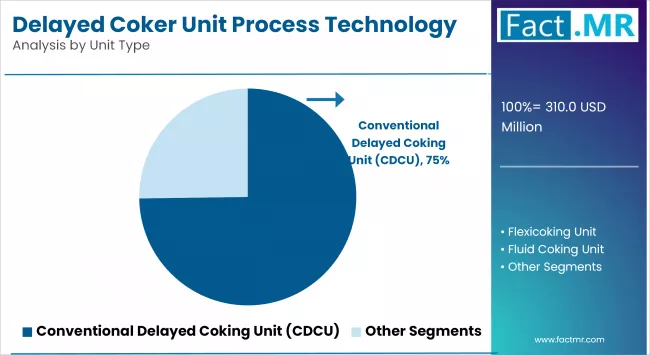

Category-Wise Analysis

Conventional DCUs dominate for flexible, cost-effective residue conversion

Conventional DCUs remain widely adopted because of their established technological base, flexibility in handling various feedstocks, and compatibility with large-scale refinery operations. These units are used to operate semi-continuous batch processes with the use of paired drums of coke. The refiners have access to control the timing of these cycles, vapor-liquid separation, and coking fouling.

Modular furnace designs and coke handling systems are increasingly tailored to specific applications and locations based on yield requirements and safety factors. Uptime is being improved by advanced metallurgy, predictive monitoring of drum integrity and optimized steam quenching. With the global trend toward more stringent fuel quality standards, conventional DCUs are being reconfigured to increase middle distillate output and produce petcoke suited to downstream industrial needs.

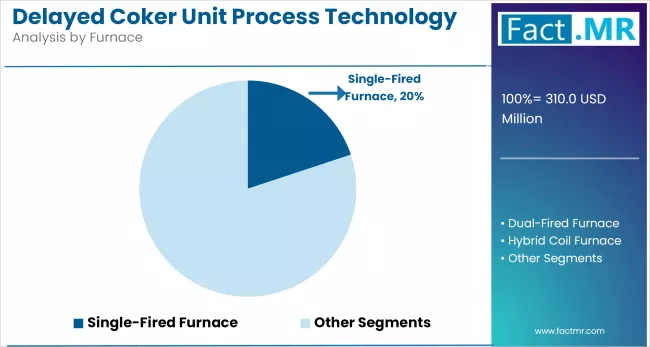

Single-fired furnaces dominate DCU for efficiency, simplicity, and reliability

The Single-Fired Furnace segment remains dominant in delayed coking technology due to its simplified design, reduced capital investment requirements, and adaptability to conventional DCU plant designs. The key to maintaining thermal efficiency, reducing hot-spot formation, and maximizing run lengths in high-severity residue cracking processes lies in optimal heat flux management and coil metallurgy. Lining of furnace arrangements is more customized to accommodate feedstock variations, with any special temperature control systems saving energy without compromising the integrity of the coil.

To alleviate fouling and coke deposition, special refractory linings and improved burner designs are being installed. Single-fired furnaces will continue to be a part of the thermal backbone in integrated upgrading schemes as refineries increase the throughput.

Optimized cracking boosts liquid yields, supporting fuel-petrochemical integration

Light fuel fabrication has emerged as the most beneficial economic factor in delayed coking activities, as refiners concentrate on the abundance of transport fuel and petrochemical feedstock. New high-thermal cracking control methods are both increasing selectivity to higher-value naphtha and distillates (selectivity into high-value products) and limiting excessive coke formation (minimization of coke formation). Accurate drum temperature profile and quench run modelling improvements increase the liquid yield efficiency whilst not compromising unit stability.

This is integrated with both downstream hydro treaters and catalytic reforming to meet the ultra-low sulfur in fuels requirements. With refiner demand shifting to petrochemicals, the delayed coking severity is being adjusted by the refiner to produce naphtha with the optimum combination of olefin and aromatics recovery, creating a nexus between fuels and chemicals.

Competitive Analysis

Key players in the delayed coker unit process technology industry include Bechtel Corporation, Lummus Technology, Wood PLC, Honeywell UOP, WorleyParsons Limited, Sulzer, CNPC, SUPCON, MOGAS Industries, Technip Energies, and HPCL.

The market for delayed coker unit (DCU) process technology is expanding, with increasingly significant focus on residue valorization, compliance-based upgrades, and petrochemical integration, being the priority of refiners. Key technology licensors in the coker segment, including Bechtel, Wood, Lummus Technology, and CB&I, are investing in modular coker projects, automated drum-switching systems, and low-emission coke-handling technologies.

A new level of competition is emerging based on thermal efficiency, reduction of the cycle times, and compatibility with complex crude slates. Players are entering strategic collaborations with refinery operators to provide turnkey solutions and post-commissioning services. Demand in Asia and the Middle East has also grown sufficiently to create regional manufacturing hubs, supporting localized fabrication and service capabilities.

Recent Development

- In March 2025, Honeywell acquired Sundyne to expand its Critical Equipment Portfolio and Aftermarket Services. With the addition of Sundyne's disposable package of products and equipment, combined with the process automation features of Honeywell Forge, we will be well-positioned to provide customers with a broader range of solutions.

- In August 2023, Lummus Technology also licensed its Novolen polypropylene process reactors and high-performance catalysts to its polypropylene plants at the HPCL Rajasthan Refinery. This type of licensing agreement serves to highlight that Lummus Technology offers refining and petrochemical clients more enhanced and holistic process technologies that are used in large-scale projects, such as large-scale refinery and petrochemical plants, in order to aid in developing refining and petrochemical integration in the Indian sector.

Fact.MR has provided detailed information about the price points of key manufacturers in the Delayed Coker Unit Process Technology Market, positioned across regions, including sales growth, production capacity, and speculative technological expansion, in the recently published report.

Methodology and Industry Tracking Approach

The Fact.MR Global Delayed (DCU) Process Technology Market report 2025 carried out the insights of 9,800 stakeholders across 28 countries with refining-intensive, with a minimum of 300 respondents in each country. The respondent group was sized with refinery engineers, EPC contractors, process licensors, operations managers and regulators.

The research was conducted in July 2025 - June 2026, during which investment trends, technology preferences, limitation within operation and upgrade plans were retrieved. The replied responses were weighted based on regional complexity as well as the penetration of DCU at the refineries. More than 250 sources, including technical whitepapers, project tenders, patent filings, and emissions regulations, were also incorporated, based on sophisticated regression models and sensitivity analysis, to provide technology adoption forecasts.

With Fact.MR monitoring consumer behavior, product efficacy, industry trends, and market opportunities since 2018, this report is becoming an authoritative source of information that stakeholders can rely on.

Segmentation of Delayed Coker Unit Process Technology Market

-

By Unit Type :

- Conventional Delayed Coking Unit (CDCU)

- Flexicoking Unit

- Fluid Coking Unit

- Continuous Coking Unit

-

By Furnace Type :

- Single-Fired Furnace

- Dual-Fired Furnace

- Hybrid Coil Furnace

-

By Application :

- Light Fuel Production (Gasoline, Diesel, Naphtha)

- Petroleum Coke Generation

- Crude-to-Chemicals Integration

- Residue Upgrading

- Feedstock for Gasification Units

-

By End Use :

- National Oil Companies (NOCs)

- Independent Refiners

- Integrated Oil & Gas Majors

- Petrochemical Companies

- Public Sector Refineries

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What was the Global Delayed Coker Unit Process Technology Market Size Reported by Fact.MR for 2025?

The global delayed coker unit process technology market was valued at USD 310 million in 2025.

Who are the Major Players Operating in the Delayed Coker Unit Process Technology Market?

Prominent players in the market are Bechtel Corporation, Lummus Technology, Wood PLC, Honeywell UOP, Worley Parsons Limited, Sulzer, CNPC, SUPCON, among others.

What is the Estimated Valuation of the Delayed Coker Unit Process Technology Market in 2035?

The market is expected to reach a valuation of USD 363.3 million in 2035.

What Value CAGR did the Delayed Coker Unit Process Technology Market Exhibit Over the Last Five Years?

The historic growth rate of the delayed coker unit process technology market was 1% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Naved Ahmed