Halloumi Cheese Market Outlook (2025 to 2035)

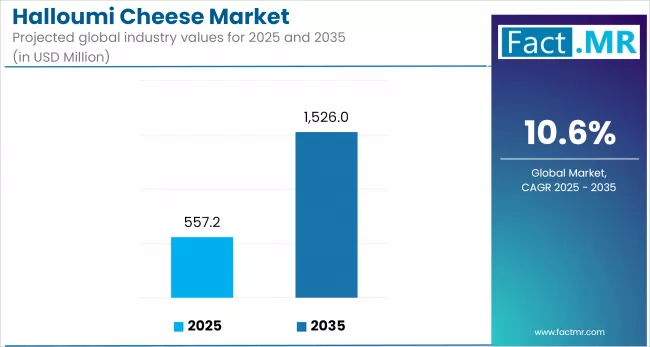

The global halloumi cheese market expected to reach USD 1,526 million by 2035, up from USD 501.5 million in 2024. During the forecast period 2025 to 2035, the industry is projected to expand at a CAGR of 10.6%, driven by various factors, including increased global demand for ethnic and functional dairy products, vegetarian and flexitarian lifestyles, growing modern retail and foodservice distribution, and trends toward premiumization in PDO-certified varieties.

Collectively, these drivers place Halloumi among the rapidly growing segments in specialty cheese, merging cultural authenticity with health positioning and culinary versatility across developed and emerging markets.

What key drivers are driving growth in the global Halloumi Cheese market today?

The primary factor driving the halloumi cheese market globally is the growing preference among consumers for plant-based, protein-fortified diets. Owing to its texture and grilling compatibility, Halloumi has also been embraced by consumers seeking meatless, healthier sources of protein. Its ability to grill without melting makes it particularly appealing, making it suitable for both gourmet and casual dining.

The growing popularity of Mediterranean cuisine has further introduced halloumi to a global audience. Increased activity in health-conscious niches, coupled with rising demand from QSR and fine-dining segments, continues to support the growth trajectory of halloumi cheese.

What are the key consumer-driven trends shaping the future of the Halloumi cheese market?

Halloumi cheese is currently influenced by market trends centered around innovation and customization. There has been notable growth in flavored varieties such as mint, chili, and smoked, depending on brand preferences. Organic and low-fat options are also gaining traction due to prevailing health and wellness trends.

Retail formats such as sliced and grated Halloumi have proven convenient and effective in reaching household consumers. There is also a clear shift toward clean-label products, as consumers express preferences for cheese made from fewer and more identifiable ingredients. All these trends reflect a rapidly evolving market shaped by consumer demand for quality, flavor, and dietary relevance.

What are the key factors restraining growth in the global Halloumi Cheese market today?

The halloumi cheese industry is growing, yet several hurdles remain. Regulatory impediments, particularly regarding geographical indication protections and labeling standards, pose challenges to global trade. A relatively high price can limit accessibility for cost-sensitive consumers.

Positioned between traditional production methods, scalability limitations may restrict supply growth. Shelf life and cold-chain logistics are critical for non-traditional markets, where cultural unfamiliarity may further hinder market penetration. Lastly, slow growth may be exacerbated by competition from other protein-rich dairy alternatives and plant-based cheese options, unless Halloumi manufacturers prioritize innovation and effective marketing strategies.

Which regions are experiencing the fastest growth in the global Halloumi Cheese Market, and why?

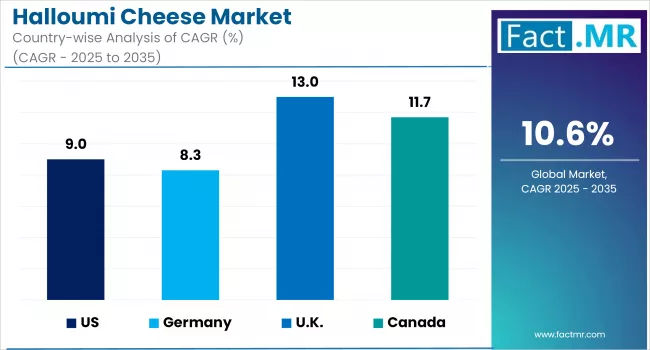

The North American market of halloumi cheese is growing steadily due to increasing consumer curiosity about foreign cuisines and vegetarian protein sources. Demand in urban centers across the United States and Canada continues to rise, particularly through foodservice channels and specialty stores, driven by product innovations such as flavored and organic halloumi.

Middle Eastern Asia is proving a potential market of the halloumi cheese, through increased exposure to the Mediterranean and the middle classes. Japan and South Koreans are on the forefront with increased demand by the health conscious consumers. The area is positively capitalizing on the changing retail channels and the influence of the West culinary in the urban food markets.

The United Kingdom is chief consumer of the halloumi cheese market in Western Europe, which is the main producer of the global halloumi cheese market. The fact that cheese is a common food in Mediterranean diets, corresponds to the local taste in broad-use, protein-rich foods. The penetration is further powered by excellent retail distribution, developed culinary familiarity, and innovation of organic and flavored types.

Country-wise Outlook

Health-Conscious Consumers and Functional Ingredients Boost USA Halloumi Cheese Market

The market size of halloumi cheese in USA shows continuous growth owing to the shift in consumer preference inclination into nutrient-added and enriched bakery products. The rise in interest that is being taken with regard to wellness and clean-label ingredient is pushing the big bakers towards investment towards natural preservatives like halloumi cheese.

This shift aligns with the broader transformation in eating behavior that emphasizes health, transparency, and functional value. Artisan and organic breads, which often include Halloumi cheese, are gaining popularity as consumers increasingly seek high-quality, additive-free options.

Frozen dough products, which appeal to convenience-focused retail stores, represent a promising application area for Halloumi cheese, reinforcing its advantage in extending shelf life without compromising taste or flavor.

Clean-Label Compliance and Dairy Innovation Propel Germany’s Halloumi Cheese Market

Regulatory compliance and growing consumer demand for clean-label products are driving the German halloumi cheese market. Food producers have increasingly turned to natural preservatives to meet the stringent European food safety standards and consumer expectations for additive-free and organic food options.

Halloumi cheese has gained relevance in both the dairy and bakery markets, as it helps prevent spoilage without compromising taste or texture. As clean-label guidelines become more prominent, food manufacturers are adopting Halloumi cheese to preserve product integrity and offer consumers what is perceived as a natural and sustainable preservative option in food products.

Heritage Cuisine and Gourmet Consumption Spur UK Halloumi Cheese Market

In the UK, the halloumi cheese market has been experiencing steady growth as consumers increasingly embrace gourmet and Mediterranean-style eating habits. As consumers continue to explore artisanal and ethnic foods, halloumi cheese has become a staple in both home cooking and restaurant menus. The British market is increasingly aligning with clean eating preferences, driving demand for dairy products with minimal processing.

Halloumi is also being creatively incorporated into ready-to-eat meals and street food offerings, aligning with urban consumption patterns and premiumization trends. The rise of vegan and flexitarian lifestyles is further encouraging the development of hybrid dairy substitutes that replicate the texture and cookability of halloumi.

Category-Wise Market Outlook

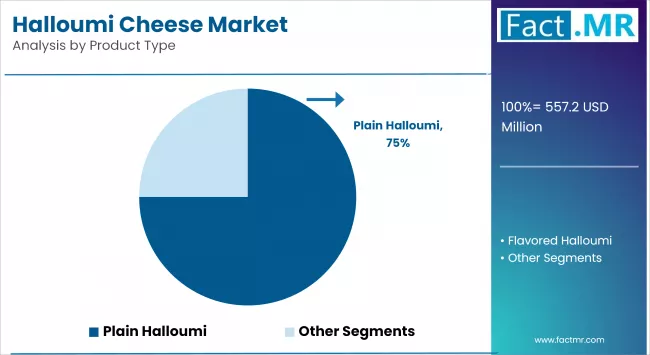

Flavored Halloumi Gains Momentum Amid Palate Diversification and Gourmet Trends

The rapidly growing product type in the halloumi cheese market is flavored halloumi. The increasing consumer tendency toward adventurous and diverse taste preferences is encouraging the growth of variants with herb, spice, and smoked flavor profiles.

This trend aligns with the rise of gourmet snacking and the global popularity of Mediterranean cuisine. Foodservice providers and restaurants are incorporating flavored halloumi as a signature ingredient in both traditional and fusion-style dishes.

The novelty of flavoring not only enhances consumer appeal but also supports the product’s premium positioning, particularly in Western Europe and North America.

Organic Halloumi Surges Forward as Clean Label and Ethical Consumption Prevail

Super-accelerated growth is being experienced by organic halloumi with the increased development of clean-label goods, growing concerns about animal welfare, and sustainable farming. Consumers are becoming more proactive in purchasing dairy products that are free from artificial additives and produced using organic feed and humane methods.

Trust and adoption are further accelerated by regulatory bodies in both Europe and North America, which provide certification standards for organic products. Organic cheese is gaining shelf presence in retail stores, with Halloumi emerging as one of the most popular and health-conscious indulgent options.

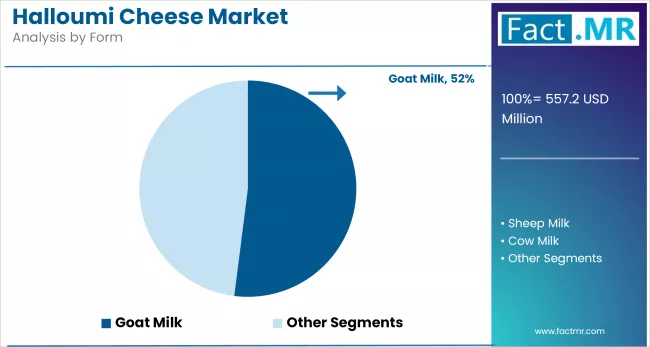

Goat Milk-Based Halloumi Sees Rapid Uptake Amid Digestibility and Niche Positioning

Goat milk halloumi is becoming increasingly popular as it is believed to be digested and tastes differently. It attracts those consumers who are lactose intolerant and the need to get an alternative to the cheese based on cow milk.

The segment is also enjoying a fresh demand in artisanal and farm-origin dairy, connected in many cases to conventional cheese making technologies of areas such as Cyprus and the Middle East. Its high nutritional level and its position as a high end dairy product are escalating demand within the health and gourmet sectors.

Sliced Halloumi Leads in Convenience-Oriented Consumption Patterns

The swiftly growing format is sliced Halloumi, driven by the demand for convenient solutions in ready-to-cook and ready-to-eat foodservice. As consumers increasingly prioritize convenience, sometimes over traditional product formats, pre-sliced options are gaining traction in both domestic retail and, notably, the HoReCa sector.

It can be grilled without making much effort, can be uniformly divided into portions, which is why it is suitable to use it with burgers, sandwiches, and salads. The tendency can be especially strong in the urban environment where hurried customers need the quick gourmet-style fast food ingredients.

Online Retail Emerges as the Fastest Channel Fueled by Direct-to-Consumer Dynamics

The online retail will be growing tremendously as the distribution channel of choice and the reason is due to the proliferation of e-commerce and direct-to-consumer approaches. Consumer changes due to the pandemic shopping behavior made people browse online to check out exotic and handmade cheeses.

Online penetration is being powered by subscription boxes, farm to door delivery options and easy digital ordering. Cold chain logistics is also being optimized to increase the integrity of the products, something that is pushing people to buy novel gourmet foods such as halloumi that has a short shelf life.

Foodservice Sector Propels Halloumi Demand Amid Menu Innovation and Global Cuisine Trends

The foodservice segment is registering the fastest rate of development in terms of end-use, driven by growing usage in casual, fine dining, and quick-service restaurants. Owing to its versatility, grilling capability, and firmness, Halloumi is favored by chefs specializing in Mediterranean and fusion cuisines.

The trend also impacts the segment that experiences increasing consumption of vegetarian and flexitarian meals with halloumi replacing meat in wraps, skewers and burgers. The global demand is witnessing increased adoption of halloumi in the foodservice environments in emerging markets within Middle East, Asia-Pacific, and Latin America.

Competitive Analysis

Competitive Outlook: Halloumi Cheese Market

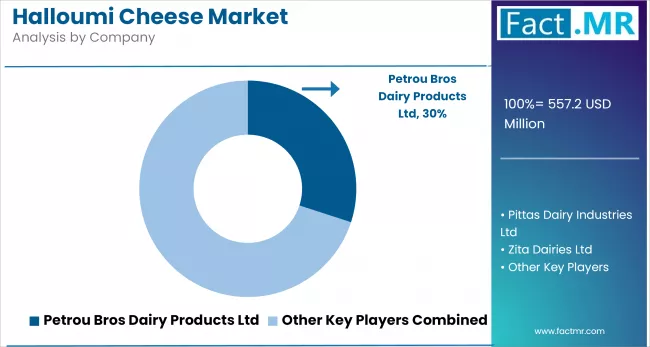

In the halloumi cheese market, both traditional Cypriot producers and multinational dairy corporations are present, though their influence and impact on market progression differ. Such Cypriot enterprises as Petrou Bros Dairy Products Ltd, Zita Dairies Ltd, or Charalambides Christis Ltd maintain the ancient style of production, which guarantees the authenticity and quality. The market share is high and under the brand name ALAMBRA, the company deeply dominated the market as it exports to more than 40 countries, with high quality standards attained by Petrou Bros.

The focus of Zita Dairies is the combination of conventional historic methods and contemporary knowledge, and the Halloumi obtained by this method has a Protected Designation of Origin (P.D.O.). The chief dairy business in Cyprus is Charalambides Christis which has concentrated on Halloumi as the key export product and also comes in different forms using cow, goat and sheep milk as ingredients.

This has given Halloumi a wider presence in the world with other international players such as Arla Foods amba and Nordex Food dominating the world. Apetina is a brand that deals with various types of cheese sold under the name of Apetina (Halloumi) primarily in more than 30 countries by Arla.

Nordex Food has dealt with white cheese (Halloumi, in particular) and distributes products in over 70 countries across the globe. These businesses make use of wide scale distribution channels and marketing plan to popularize halloumi all around the world and this has helped the spread of halloumi products to new regions as well.

Key players of halloumi cheese industry are Petrou Bros Dairy Products Ltd, Pittas, Dairy Industries Ltd, Zita Dairies Ltd, Charalambides Christis Ltd, Lactalis Group, Achnagal Dairies Ltd, Arla Foods amba, Nordex Food, Dodoni, GRILLIES.

Recent Development:

- In 2024, Agathangelou introduced a fully automatic Halloumi/grilled cheese production line, enhancing efficiency and consistency in cheese manufacturing. This innovation combines traditional cheese-making techniques with modern automation to meet increasing demand while maintaining artisanal quality.

- In February 2024, a former airline pilot in Cyprus began producing Halloumi exclusively from ewe’s milk, defending traditional methods amidst a heated debate over Halloumi’s ingredients. His artisanal approach, promoted via social media, highlights the ongoing clash between commercial viability and traditional authenticity in Cyprus’s Halloumi production.

Fact.MR has provided detailed information about the price points of key manufacturers of the Halloumi Cheese Market positioned across regions, sales growth, production capacity, and speculative technological expansion, in the recently published report.

Methodology and Industry Tracking Approach

The 2025 global halloumi cheese market report by Fact.MR sets a new benchmark in strategic market intelligence, delivering a precision-driven, data-intensive view of Halloumi Cheese’s expanding influence across global foodservice, premium dairy innovation, and sustainable nutrition systems. Anchored in insights from over 7,500 stakeholders across 35 countries, each contributing 300+ qualified responses, the report offers unmatched analytical depth, regional breadth, and industry relevance.

The respondent architecture was meticulously constructed to ensure 360° perspectives, two-thirds composed of end users and strategic decision-makers, including innovation heads, procurement leads, category managers, and sustainability officers from leading food & beverage, hospitality, and retail organizations. The remaining one-third comprised domain experts such as dairy technologists, food scientists, quality auditors, cold-chain specialists, and export consultants engaged across Mediterranean cheese production, clean-label dairy, and gourmet retail segments.

Spanning an in-depth research cycle from July 2024 to June 2025, the report tracks transformative shifts in the Halloumi Cheese market, including milk source optimization (e.g., mixed vs. single-origin), processing innovations (automated pressing, energy-efficient brining), application diversification (plant-based analogues, flavored formats, ready-to-grill packs), and regulatory evolution surrounding PDO labeling, cross-border trade standards, and shelf-life extensions. Stratified modeling ensured rigorous weighting of insights by geography, stakeholder role, and distribution tier.

Built on more than 250 validated sources, including trade data, food safety regulations, patent filings, whitepapers, and proprietary retail audits, the study applies advanced analytics such as segmentation clustering, trend forecasting, and regression modeling to deliver high-confidence, forward-looking insights.

With continuous monitoring since 2018, this 2025 edition is an indispensable resource for dairy processors, CPG innovation teams, foodservice strategists, sustainability-focused sourcing groups, and institutional investors seeking to lead in the fast-evolving halloumi cheese economy.

Segmentation of Halloumi Cheese Market Research

-

By Product Type :

- Plain Halloumi

- Flavored Halloumi

-

By Nature :

- Organic

- Conventional

-

By Milk Source :

- Goat Milk

- Sheep Milk

- Cow Milk

- Mixed (Goat/Sheep/Cow)

-

By Form :

- Sliced

- Blocks

- Crumbled

- Grated

-

By Distribution Channel :

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- HoReCa (Hotels, Restaurants, Cafés)

- Others

-

By End Use :

- Household

- Foodservice

- Food Processors

- Institutional

- Others

-

By Region :

- North America

- Latin America

- Western Europe

- Eastern Europe

- East Asia

- South Asia & Pacific

- Middle East & Africa

- Frequently Asked Questions -

What was the Global Halloumi Cheese Market Size Reported by Fact.MR for 2024?

The global halloumi cheese market was valued at USD 501.5 Million in 2024.

Who are the Major Players Operating in the Halloumi Cheese Market?

Prominent players in the market are Petrou Bros Dairy Products Ltd, Pittas, Dairy Industries Ltd, Zita Dairies Ltd, Charalambides Christis Ltd, Lactalis Group, Achnagal Dairies Ltd, Arla Foods amba, Nordex Food, Dodoni, GRILLIES.

What is the Estimated Valuation of the Halloumi Cheese Market in 2035?

The market is expected to reach a valuation of USD 1,526 Million in 2035.

What Value CAGR did the Halloumi Cheese Market Exhibit Over the Last Five Years?

The historic growth rate of the halloumi cheese market was 10% from 2020 to 2024.

Author:

S.N. Jha

Editor:

Anushree Karale